Real estate developer. Former hedge funder at BlackRock, Caxton. Ground up.

Joined February 2022

- Tweets 2,805

- Following 327

- Followers 883

- Likes 4,446

142 Photos and videos

Jun 11

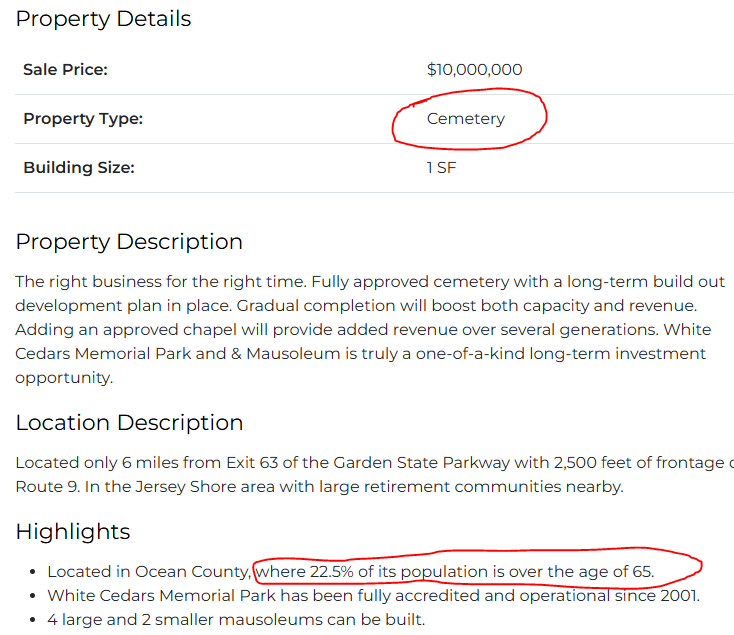

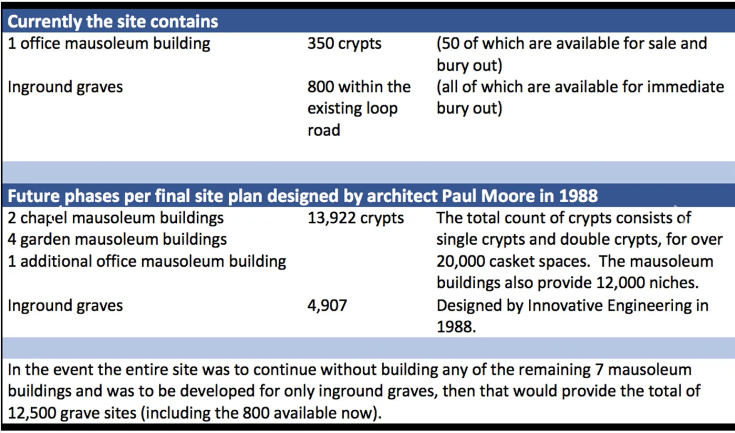

New real estate niche just dropped -

Forget about trying to capture a small piece of the baby boomer "wealth transfer".

Instead, profit directly from each death!

An amazing opportunity you will be ***dying*** to get your hands on!

11

3,253

Jun 10

Entitlement risk - what is it, and who should get paid for it?

Real estate sellers can be a funny crowd. Each thinks their parcel is special, irreplaceable, and uniquely valuable.

Some even think they should be compensated based on what is theoretically possible - not what is realistic or even probably.

As a consumer, you would never pay a new car price for the collection of materials needed to build that car - steel, aluminum, glass, plastic, rubber, copper.

Why? Because you would still need to spend time and money, use your expertise, and take all sorts of risk to assemble the car yourself.

And yet, many sellers of developable land want to be paid as if they were handing over the keys to a brand-new car - when in reality - they are simple selling some of the components necessary to build that car.

As a general rule - whomever takes the entitlement risk should be compensated for that risk.

Deals where sellers don't understand basic risk return requirements are an easy pass.

1

63

Jun 9

One of NYC's most iconic office buildings just hit the market — and junior CMBS bondholders are about to be wiped out.

RXR listed the Helmsley Building (230 Park Ave) at $670M. That's priced at the debt basis - roughly $481/sf - and might be overly optimistic.

The CMBS deal was originated by Morgan Stanley in 2021 at a $1.2B appraised value. The $240M senior tranche looks fine. The junior tranches don't. Morgan Stanley itself will also take a loss as the originator, thanks to post-GFC risk retention requirements.

A century-old New York icon listed at a 44% haircut to last sale, just a few blocks from where Citadel, JP Morgan, and Extell are making billion-dollar office bets. Perfect example of the different between brand new Class A office and older buildings that need significant updates.

3

7

38

54,851

May 28

Gary Barnett just closed on yet another Midtown East site.

Extell paid $39M for 165 East 56th Street this week. This is another 75k-110k ft you can add to his previous purchases:

→ $19M for the Friars Club building at 57 East 55th Street

→ Under contract on 110 East 55th Street AND 111 East 54th Street

→ $36M in air rights over Saint Thomas Church at 678 Fifth Avenue

That's a billion $ bet on Midtown East.

The end game isn't public yet and won't be for awhile. But this is the same developer building a $1B office tower at 570 Fifth Ave, a 1,200-foot residential skyscraper on the former ABC campus, and a 70-story condo at 50 West 66th Street.

Manhattan is dead, they said. Mamdani is destroying the greatest city in the world, they said.

Someone forgot to tell Gary.

1

2

23

6,531

AG retweeted

May 27

Proptech loves a productivity stat. "80% time savings," "64% more productivity," "10x faster processes." Nobody can show you the math on any of them, because they're manufactured primarily to raise capital.

Those stats also miss the focus of what software should actually do, which is one reason tools built for development and construction fail so often. Real estate is capital-intensive, and the cost of forcing a useless tool onto a live project is much higher here than in most industries. This is why new software adoption in the industry is so tough. If your team is depending on the software for cost management, wasted time isn't just an inconvenience.

Like a lot of work in development, cost management takes time. The point isn't speed, it's getting it right, and getting it right is what produces clean data, fewer surprises, and a team that doesn't get blindsided. Done well, it also ends up being faster.

That's more nuanced than what fits on a pitch deck slide.

About 80 people have joined the beta tester opt-in, which is more than we expected, and from a wide enough range of company types that it feels like a real cross-section of the development industry.

Large national shops, family-run companies that have been around for decades, emerging developers, and small but mighty teams.

Thank you to everyone who signed up. I'm genuinely excited that this many people are willing to give The BigACR a shot, and to see how it performs in the hands of teams beyond our own.

We're closing the beta tester opt-in tonight, and the first onboarding email goes out tomorrow.

The waitlist will stay open until launch, and joining it is the best way to hear from us as things move forward.

2

1

16

2,476

May 27

Manhattan office rents just hit $340/sq ft.

The media keeps telling you that Manhattan is dead. Meanwhile, the market is quietly rewriting records.

In April 2026, 9 West 57th Street — home to Apollo Global Management, Chanel, and the Qatar Investment Authority — signed a lease at $340/sq ft.

And it's not a one-off:

→ 425 Park Avenue broke the $300 barrier back in 2022 when Citadel took occupancy

→ SL Green's One Vanderbilt is now in that same rarified tier

→ 3 leases over $300/sq ft have been signed since January 2025 alone

→ 2026 marks the first time NYC has seen TWO $300 leases in a single year

The supply picture tells the real story. Trophy office availability in Manhattan has dropped from 18.4% to 8.3% in just four years. In the Plaza District? A staggering 3.3%. Only 4 new trophy buildings are scheduled to deliver before 2030 — and most of that space is already spoken for.

Financial firms, law firms, and AI companies are all competing for the same shrinking pool of elite space.

In 2021, $200/sq ft felt like a ceiling. Now it's not even noteworthy.

$350/sq ft is expected before the end of 2026. $400 is now entering the conversation.

The obituary for NYC office real estate was written way too soon.

3

161

May 16

Literally giving away some of the secret sauce.

Abundance theory in action.

May 16

Blown away by the response to the announcement of the BigACR.

20 people signed up within 36 hours to test the software. I wasn't expecting that much interest.

The most interesting thing about the folks who signed up, so far, is how many teams consistently run multiple $50mm projects with teams of <5.

A great reminder that most development shops are small businesses, and that professionalizing our shops is one of the best ways to derisk our operations.

This is why we built the software for MADDPROJECT.

We are leaving the beta tester sign up open for the next week and then reverting to waitlist only.

I will do my best to share often, so we can reach a few more people who are interested in participating.

Thank you all!

4

132

AG retweeted

May 14

Five years ago, I started building the BIG ACR for our own development shop.

We've run it on every MADDPROJECT job since.

I built it because cost management is the highest-stakes, lowest-trained part of development, and every firm has a general approach, but every project lead runs their own version of it.

The BIG ACR reads the documents your team already produces, checks the math, and walks the reviewer through the details with the same discipline we apply on every project.

(There is no need to have the GC or trades log in to yet another portal.)

For the last eight months we've been getting it ready for the outside world.

It's a version of MADDPROJECT that scales without us in the room.

We built it for project owners and allocators who often have no independent way to check the numbers and rely on the GC's payment applications to keep track of costs.

For investors who want to read the same ACR their GPs are reading.

For new teams who want senior-level review discipline from day one.

For firms running multiple projects who want every one held to the same standard.

And for the firms we'd typically turn down for full development management, who can now get our cost management discipline.

We are excited to launch our waitlist today, and we are looking for a small group of beta testers ahead of a Q3 launch.

bigacr dot com

10

4

37

5,404

May 14

If you think real estate development has highs and lows you should try running a hedge fund book. Literally minute by minute feedback on how right you are and how much $$ you are making or losing.

Not to say RE dev isn’t emotional.

Real estate development is the extreme of all emotions.

Highs when you get cash flow and big wire transfers. Sucks like nothing else when a deal goes bad.

Mentally prepare for these extremes.

Know that today's situation won't last.

Tomorrow will be different.

1

130

May 14

The headlines about New York City and San Francisco have been relentless for years. Crime. Exodus. Remote work. Office vacancies. The death of the urban core narrative has been a cottage industry unto itself.

Someone forgot to tell the apartment market.

Equity Residential — one of the largest publicly traded apartment REITs in the country, with over 85,000 units across 312 properties — recently reported Q1 2026 earnings, and the two cities everyone loves to write off were the stars of the show. New York and San Francisco together drove roughly 30% of the company's net operating income, and CEO Mark Parrell credited both markets with delivering first-quarter performance that "exceeded expectations."

The reason? Strong demand from higher-earning renters, well-located product, and — critically — modest levels of new supply. While other markets like Denver and Seattle are wrestling with overbuilding, New York and San Francisco are characterized by structural supply constraints that aren't going away anytime soon. That's a landlord's market, whatever the op-eds say.

This is what a narrative violation looks like. Not a viral moment, not a dramatic turnaround announcement — just a blue-chip institutional investor quietly reporting that the cities everyone counted out are outperforming, quarter after quarter, because the fundamentals never actually broke.

Urban density, job concentration, and housing scarcity are powerful forces. They don't show up in think pieces. They show up in earnings calls.

2

2

125

May 6

Shocking.

May 6

The private Sunbelt multifamily REIT formed by Scott Everett's S2 is now telegraphing a total equity wipeout, according to new investor comms from partner Trinity reviewed by The Promote.

"Said another way, while the common equity was marked at $0.73 per share as of Q4 2025, S2 is currently focused on maximizing value for mezzanine investors, and equity investors should expect a full loss of capital."

More for Insiders later today. REIT has 9K units so a BFD.

4

280

May 4

lol if a prospective employer asks you this question, the answer is always some version of “try to make even more next year”. Play the game, people.

May 3

Ken Griffin weeded out a candidate by asking “if you made $10 million what would you do?”

“I would quit and I would climb the highest peaks around the world.”

Griffin wanted him to say “how they’d climb the next mountain at Citadel” instead

2

229

May 2

On Jane Street: If you read and understand the below, read about their activity in the Indian options market, then apply those strategies to ~every listed market in the world, combined with huge regulatory, technology, and talent advantages vs competitors, you’ll begin to understand how they make so much money.

May 1

Curious how Jane Street made $40 billion last year with few negative days? Here’s one example:

- Between 1990-2000, there was only one exchange-listed product to trade natural gas: the NYMEX (now CME) physically-settled futures contract

- In 2000, ICE realized there was demand for a financially settled (swap) futures contract and introduced it

- CME countered and listed their own swap future

At this point, the products were primarily for institutional and sophisticated individuals with a commodities account. But as commodities boomed in the 2000s, exchanges created new contracts to increase access and appeal to retail traders.

- the NYSE introduced an ETF (UNG) that followed natural gas prices in 2007

- More ETFs followed that offered ability to bet on a price decline and to get 2x or 3x leverage

- CME introduced a mini contract that was 1/4th the size of the original

The next evolution was to appeal to the pure speculator by expanding the market to less regulated exchanges, widening access globally, increasing leverage, and creating daily bets.

- CME introduced the micro contract that is 1/10th the size of the original

- CME and ICE introduced contracts that expire each trading day

- Hyperliquid and Binance offer unregulated, on-chain, high leverage, perpetual nat gas contracts for non-US uses

- Kalshi offers same day binary contracts. Other prediction markets are moving forward as well.

Now add other iterations on settlement days for the contracts and options on everything listed above.

Note that all of these contracts settle (perps notwithstanding) against the original CME physical futures contract. But instead of one way to trade the product, there are dozens. This creates an opportunity to make markets across all of these surfaces and arbitrage among them. And that's what Jane Street and other similar HFT shops do (among many, many other things).

Nat gas for delivery at Henry Hub, Louisiana is just one product. Take all the ways to trade equities, currencies, commodities, crypto, interest rates, etc across all the different exchanges in all the jurisdictions and the opportunity of making $50 here and $1000 there adds up to an enormous, low-risk money making machine.

This opportunity originates from the large variety of ways people desire to trade random financial instruments and the various products designed for them. This creates a hugely profitable opportunity for the HFTs. They provide a valuable service of creating liquidity for those seeking to trade. Whether that trading is smart and profitable for the average punter on the other side is a different story.

1

1

223

Apr 30

I still receive recruiter outreach 3x/week for an industry I no longer work in.

Apr 30

Up until a few months ago, I would ignore all the recruiter outreach offering me to go in-house. Especially those offering a 'great opportunity' to work on projects 1/10 the size of the ones we are working on.

Mostly, these emails annoyed me because of how little diligence these people do. They have a paying client that they're certainly not servicing properly.

Then, I decided to respond to every one of them with a company resume and an offer to provide a proposal for services.

Not a single response, yet.

Will report later if that changes.

2

4

1,142

Apr 30

Right up there with “people often ask me”

Apr 30

When I tell you these people selling info products “borrow credibility” this is what I mean.

“I just spoke to a guy”

“My friend Steve”.

“I just had someone on my podcast who”.

They hope you blur your eyes enough that you start to view them as serious business people not entrepornographers.

1

1

119

Apr 30

These have gone too far!

Straight up gibberish

Had a Jane Street interview in 2019.

Round 8. Interviewer texts: 'Equinox Brookfield. 6 AM. Bring a calculator you won't use.'

I show up. He's on the StairMaster reading a printout of the CBOE VIX term structure.

Doesn't get off. Nods at the machine next to him.

'You see that guy on the rower? Goldman MD. Comes here every morning at 6:04. Leaves at 6:38. What's the implied vol on his arrival time?'

'I don't know his variance.'

'Sample size of one year, 250 sessions. Standard deviation is 90 seconds. Annualize it.'

I do the math in my head. '90 seconds times sqrt(250). About 24 minutes annualized.'

'Wrong. You annualized like it's a return. Time-of-arrival doesn't compound. It's a Poisson process with drift. The correct answer is his arrival is more punctual than the 6 train. Now price me an option on whether he shows up tomorrow.'

I think for a second. 'If he's been here 250 days in a row, base rate is 99.6%. But you have to adjust for his vacation schedule and probability of injury, call it 96%.'

'Strike?'

'$10 if he shows, $0 if he doesn't.'

'I'll sell you that option for $9.40.'

I think about it. 'No. Expected value is $9.60. You're underpricing by 20 cents.'

'Correct. Now why am I selling it to you?'

I freeze.

'Because I just saw him limp on the way in. You're buying my information for 20 cents. You overpaid.'

We get off the machines. Walk to the smoothie bar. He orders a $19 smoothie, doesn't drink it.

'Last question. The girl behind the counter makes 200 smoothies per morning. She has perfect information on who's actually here and who's faking it. Citadel guys leak their attendance to her every day for the price of a tip. If I gave you $50,000 to set up a market on which Citadel PM gets fired this quarter, what's your bid-ask?'

'Insider trading.'

'Wrong answer. There's no public security. Try again.'

I think. 'I'd quote 8 to 12 percent on any given PM. Spread of 4 points to cover adverse selection. Tighten the spread for PMs I have data on.'

'Where do you get the data?'

'The smoothie girl.'

'Good. How much do you pay her?'

'10% of P&L.'

'Wrong. You pay her a flat $200 a week. If you pay her on P&L she becomes your counterparty. Right now she's your data source. Don't conflate edges.'

He hands me the untouched smoothie.

'Throw this out on Vesey Street, not in the building. The staff knows what gets wasted. Outside, it was consumed. Same smoothie, different signal.'

I do it.

Thursday I get the email.

'Offer rescinded. Your bid-ask on the PM market was too tight. 4 points doesn't cover the tail. The girl is a single point of failure and you didn't price her counterparty risk. Also you held the smoothie in your right hand. Right-handers throw with their right hand. Camera saw the hesitation.'

4

428

Apr 24

If you just do some version of the below, use a daily face moisturizer with spf, and aren’t an alcoholic, you’ll age better than 99% of the population.

And yet, most people will spend a lifetime trying to buy their way into good health.

The investment: ~5 hours a week. Lifting heavy objects 3x a week, 2 work sets per exercise, 2-3 exercises (at least one compound movement) to failure and hiking or jog for an hour or so 1X a week, sprint intervals one day (usually 4 days after leg day…)

… for 35 years

2

3

1,624

Apr 24

A quick primer on how NYC rent regulation actually works.

This confuses a lot of people, so here's the breakdown:

Rent stabilization caps annual rent increases and guarantees lease renewals. It applies to buildings built before 1973, plus newer buildings that received 421-a, J-51, or 485-x tax incentives. About 41% of NYC's 2.3 million rental units fall into this category.

Rent control is far more restrictive — limiting increases for units continuously occupied since before July 1971 in pre-1947 buildings. Once a massive category (500,000 units in 1978), it now covers just 14,000 units and is effectively a relic.

Good Cause Eviction, the newest layer, now protects an additional 15–20% of unregulated units from eviction without legal cause and limits rent increases.

All of these regulations apply to for-rent apartment units only. For-sale condominium units have no regulations.

1

2

163

Apr 23

Condos FTW

Condos are how many of us became homeowners. We need them more than ever as single family homes are increasingly out of reach. Yet almost no one is building them. Policymakers could fix this like flipping a switch. Here’s how:

1

5

202

Apr 22

This post did huge numbers but I think the algo picked up on the church comment.

Yes many of these banks trade well below tangible book, but there are reasons (ROE too low, no div, no liquidity, no growth to name a few).

Unless you are buying these via demutualization (aka at IPO) do not waste your money on this crap.

Apr 20

I have built a spreadsheet. It has 847 rows. Each row is a community bank in the United States with a market cap below $200 million, a price-to-tangible-book ratio under 0.85, a non-performing loan ratio below 0.4%, and a CEO who has been in the role for at least twelve years. I update it every Sunday from 6 AM to 11 AM while my family attends church without me. I have visited the headquarters of nineteen of these banks in person. I have eaten a complimentary lobby cookie at each one. The cookies are how you can tell. A bank with a good cookie is a bank that respects its depositors. A bank with a stale cookie is a bank that will be acquired within 36 months at a 40% premium. I am never wrong about the cookies. The cookies have never lied to me. The cookies are the only thing left that tells the truth.

1

2

586