Finance YouTube, X, Substack, Reddit — every idea tracked, every voice ranked.

Joined May 2026

- Tweets 144

- Following 33

- Followers 2,199

- Likes 24

94 Photos and videos

Pinned Tweet

Jun 4

What is Buzzberg? 🧵

Buzzberg uses AI to analyze thousands of tweets, videos, Substacks and Reddit posts from top market voices — extracting trade ideas, tracking entry prices and measuring performance over time.

Here's a quick tour👇:

3

2

11

1,904

Buzzberg Daily report.

We scanned every video, Substack article, and research tweet in Buzzberg’s 24h feed.

The biggest signal: AI capex is shifting from a “mega-cap spender” story to a full infrastructure supply-chain story.

The market is separating the companies funding the buildout from the companies getting paid by it.

The cleaner alpha is down the stack: networking silicon, optical interconnects, memory, power distribution, transformers, cooling, grid equipment, onsite power, and physical AI sensors.

Today’s map: suppliers over spenders.👇

2

355

Company map from the 24h scan:

$MRVL: cleanest catalyst setup. S&P 500 inclusion on Jun 22 creates forced passive demand, while AI infra demand supports the core story: 800G/1.6T optics, AI switching, custom XPUs, and raised FY27/FY28 outlook.

$LITE/$AAOI: optical bottleneck trade. AI clusters need more lasers, transceivers, and interconnects as bandwidth demand scales. $LITE is the cleaner optics expression; $AAOI is the higher-beta version.

$NVDA/$SMH: broad “paid by capex” exposure. The video takeaway was to own the semiconductor/input layer where AI spend becomes revenue, not necessarily every company writing the capex checks.

$NVT/$CECO /#HPS.A.TO/$ORA /$VRT : power, grid, thermal, and always-on energy. Data centers are becoming a transformer, electrical distribution, cooling, ventilation, and power-generation problem. $VRT is obvious; the edge may be one layer below.

$FCEL : speculative carbon-capture angle. If onsite gas generation becomes part of AI data-center power, carbon capture can attach to that stack.

$OUST: Physical AI sensors/perception. If the next AI cycle moves into robots, autonomy, and industrial systems, perception hardware becomes a real infrastructure layer.

$SPCX/$RKLB: space-flow trade. $SPCX is driven by index/flow mechanics post-IPO; $RKLB is the more accessible public proxy if attention keeps moving into space infrastructure.

1

508

You can check the entry on every one of his longs on his Buzzberg page or ask our MCP👇

Just as a recap, these were all my core European longs:

1. $SIVE

2. $LPK

3. $SOI

4. $RPI

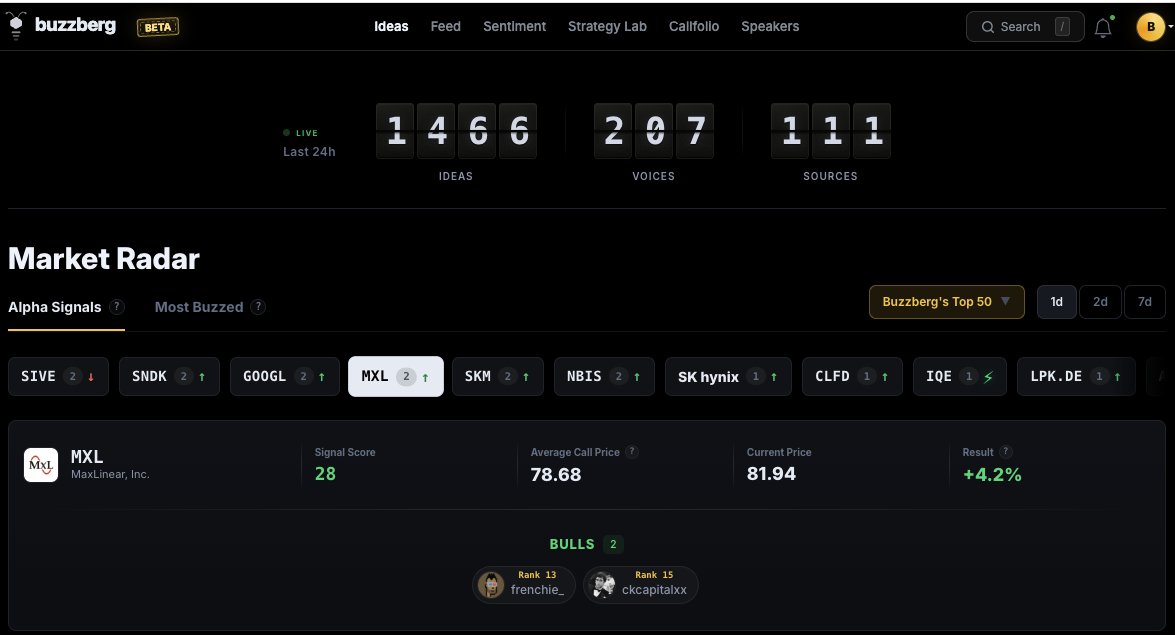

5. $IQE

6. $ALRIB

7. $XFAB

Sivers: As you know by now, core laser chokepoint over next generation photonics, from 1.6T pluggables to CPO.

Embedded in many hyperscaler suppliers from Jabil to Ayar. Should go brrr 2027 but markets are forward looking, so ramps qualifications should get priced in now.

LPK Laser - Glass core substrate "monopoly" with LIDE.

"More than 80% of major global players have selected our equipment for process validation, learning and scaling to mass production"

Soitec - Silicon photonics SoI substrate pure monopoly while coming out of legacy drag segments.

Raspberry Pi - Was my fun idea around Raspberry Pis being used for AI hardware deployments.

Previously this thing was mainly educational or hobby boards, but now used for edge/local AI. Just thought revenue increase would be extremely material and it played out well.

IQE - Critical epiwafer player for your Western photonics like Macom, Tower, Lumentum, and others.

Was kinda going under, but thought their latent capacity relative to Landmark was undervalued.

Also given how important it was, I thought that your downstream players Govs wouldn't let it go under, so it was more of a moonshot idea earlier in the year.

Lot more derisked now, very important.

Riber - Kinda monopoly in the MBE space, exposure to Quantum / quantum dot silicon photonics.

Found out from OSINT help from a friend latentvalue that Microsoft Quantum was buying their machines, so this was direct hyperscaler validation kinda de-risked at current MCs.

XFab - SiC foundry backed by EU/US CHIPS Act with power semi upside. (152% Y/Y growth for their sic vertical).

Main growth was their silicon photonics foundry past 2027 that's getting evaled by nvidia. And that they're leading Europe's value chain efforts in photonics, kinda like an early tower semi.

We'll see how this plays out, thought power semi exposure low P/B would derisk the company until they scale their photbunchonics efforts.

From my own personal thoughts:

Out of the maybe $SOI has already been re-rated the most? But I'm holding anyway.

$LPK and $ALRIB I think are still undervalued despite their monopolies.

$RPI is just kinda seeing how things go at this point, would be hilarious if they ended up like a mini nvidia for low end edge ai.

$IQE probably has a long way to go given new tower long term agreement, alongside macom. And if they convert latent capacity, I still think it has a chance of rerating like landmark.

$XFAB idk if im missing something or are markets missing something. you have nvidia as a direct eval of their silicon photonics foundry, and it's trading below replacement P/B. i think im right though.

$SIVE I see has the highest upside out of all of them given laser company ability to vertically integrate, acquire companies downstream to make their lasers more valuable, etc. Just like coherent/lumentum.

There's like 1-2 more random ones that aren't really material, but just in general.

These are the ones I've liked the most.

2

2

716

Jun 14

we're opening Buzzberg's MCP in demo access.

you can now ask Claude things like:

deep dive on $AAOI

when did [account] first mention $NVDA

what are speakers saying today, and where do they disagree

and a lot more. we're rolling it out gradually, so 10 demo codes for now.

want one? comment below follow so we can DM it to you.

202

Jun 15

New on Buzzberg: Unique X Followers Reach for every ticker.

Now you can see not just how many voices are bullish, bearish, or neutral, but the actual unique audience behind each side.

If 10 bullish speakers have 5M followers combined but 1M overlap, Buzzberg counts the real reach: 4M unique followers.

A cleaner way to understand how much audience is behind each market narrative.

2

210

Jun 14

we're opening Buzzberg's MCP in demo access.

you can now ask Claude things like:

deep dive on $AAOI

when did [account] first mention $NVDA

what are speakers saying today, and where do they disagree

and a lot more. we're rolling it out gradually, so 10 demo codes for now.

want one? comment below follow so we can DM it to you.

3

3

523

Jun 13

two big things just landed on sentiment page.

1️⃣ heatmap, rebuilt — the whole market's sentiment in one view, broken down by sector or theme, with a Buzzberg Top 50 filter.

2️⃣ narrative mindshare — what's the market talking about, and how's that shifting? watch themes grow and shrink, click into the names, see who's surging — over 30d, 90d, or year-to-date 👇

1

6

429

Jun 13

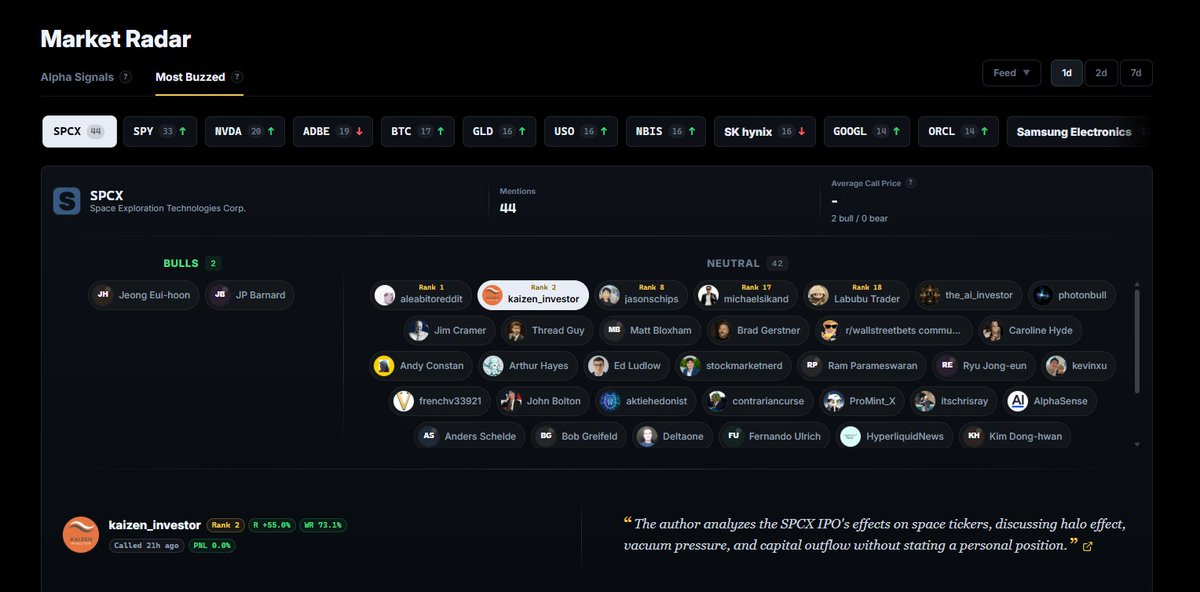

Yesterday, before the open, we said nobody agreed on the SpaceX trade.

Day one didn't resolve it. It just moved the fight to a new battleground.

$SPCX priced at $135, opened around $150, ran as much as 30% intraday, and closed 19% near $161 — a ~$2.1T company on day one.

The records are absurd: the biggest IPO in history, ~$75B raised, more than all 38 other Nasdaq IPOs this year combined. SpaceX instantly became one of the 7 most valuable public companies on earth — bigger than Tesla. It was the biggest retail IPO debut on record, beating Coinbase, and made @elonmusk the world's first trillionaire.

Around 4,400 SpaceX employees became millionaires overnight. Not just executives. Not just engineers. Welders, cafeteria staff, and people who held equity through the private years.

So is it worth it?

Nobody really disputes the company. They dispute the price.

SpaceX is now valued at roughly 94–125x annual sales, on a business that made around $19B last year and reportedly lost around $4B. As @IncomeSharks put it: Amazon earns $77B in profit at a ~$2.5T valuation. SpaceX loses money at ~$2.1T.

That's the bear case in one comparison.

The bulls say that misses the point.

@jimcramer called it "A " and "the best deal I can remember," with a $2.5T target and a 1–2 year holding period — while warning investors to brace for massive volatility.

@AviFelman framed it as a market-structure trade: tiny float forced index buying Elon premium = career risk to short.

Bob Greifeld, former Nasdaq CEO, admitted the math doesn't work at ~100x sales — but said investors aren't buying the math. They're buying aspiration.

Antonio Gracias, SpaceX board member and the second-largest shareholder after Musk, says he is holding "as long as I possibly can." His frame isn't aerospace. It's the full stack: energy → compute → launch → orbital compute. A $28.5T market up for grabs.

@Scaramucci's verdict on the doubters is blunt: people who bet against Elon tend to get wiped out. His Amazon analogy: great companies can look insanely expensive, crash hard, and still reward long-term holders if the platform keeps compounding.

The bears don't attack the company. They attack the price.

Jim Chanos says Starlink is real, but much of the rest — xAI, Starship, orbital compute, space data centers — is still "hopes and dreams." His sharper point: SpaceX may be shifting from AI software upside into renting compute to Anthropic and Google. That looks less like software and more like a hardware landlord: lower margin, more capital intensive, less magical.

That AI money is not imaginary, though. Bloomberg's @EdLudlow flagged the catch: Anthropic reportedly pays SpaceX around $1.25B/month for compute, and Google more than $900M/month — but both contracts can reportedly be cancelled on 90 days' notice.

His sharper question: if SpaceX has the compute, why rent it out instead of training its own models?

The most sobering bear take came from @moninvestor: hyped IPOs often fall first, then fly. Uber bottomed −70%, Meta −77%, Robinhood −92%, Coinbase −93%, Rivian −95%. His argument: the best entry usually comes later, not on day one.

But the smartest trade may not have been $SPCX itself. It was the fallout.

Cash rushed into $SPCX and out of the rest of the space trade. $SPCE, $FLY, $ASTS and $RKLB all got hit as capital rotated toward SpaceX. @BurggrabenH called the IPO "a vacuum cleaner" for the whole space sector.

That split the desk. One camp is buying the dip in space names — $SPCX at ~$2T while $ASTS sits around $32B makes the gap look unreal, as @retail_mourinho pointed out. The other camp thinks capital keeps rotating toward the cleaner, larger headline leader.

The real fight comes later.

Forced buying is bullish: MSCI already moved, Nasdaq 100 could follow, S&P 500 may come later. Price-insensitive demand hitting a tiny float.

Real supply is bearish: when insider shares unlock, the market finally sees how much stock wants out at a $2T valuation.

Day one went to the bulls. The lockup is the bears' turn.

Jun 12

1/

SpaceX starts trading on Nasdaq today. $135 a share, ~$1.75T valuation, a record $75B raise.

We ran hundreds of takes from YouTube, X, Reddit and Substack through our database.

Everyone agrees it's a great company.

Nobody agrees on the trade. 🧵

1

4

964

Jun 13

Every voice and call in this thread is on Buzzberg — who said it, when, and how their past calls actually played out. You can check all of it yourself: buzzberg.ai

285

Jun 13

you don't have to wait a year.

all 4 pitches from the @theallinpod best ideas competition, live leaderboard

buzzberg.ai/competitions/all…

Jun 12

Hey @chamath can we check in on the return on each of the 4 pitches from AIL in a year?

2

441

Jun 12

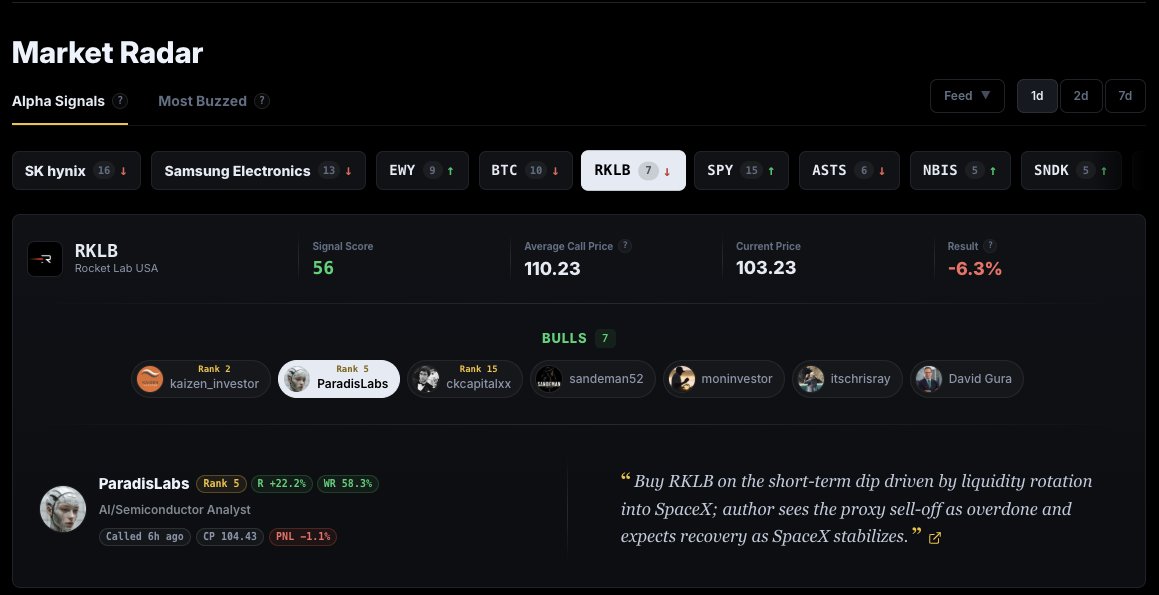

📡 Buzzberg Daily Market Radar.

constants in life: death, taxes, korean youtube bullish on memory.

meanwhile a lot of speakers are buying $ASTS and $RKLB today — thesis: the selloff is just capital rotating into spacex-ipo allocations, fundamentals unchanged, and the listing brings new eyes to public space names

1

499

Jun 12

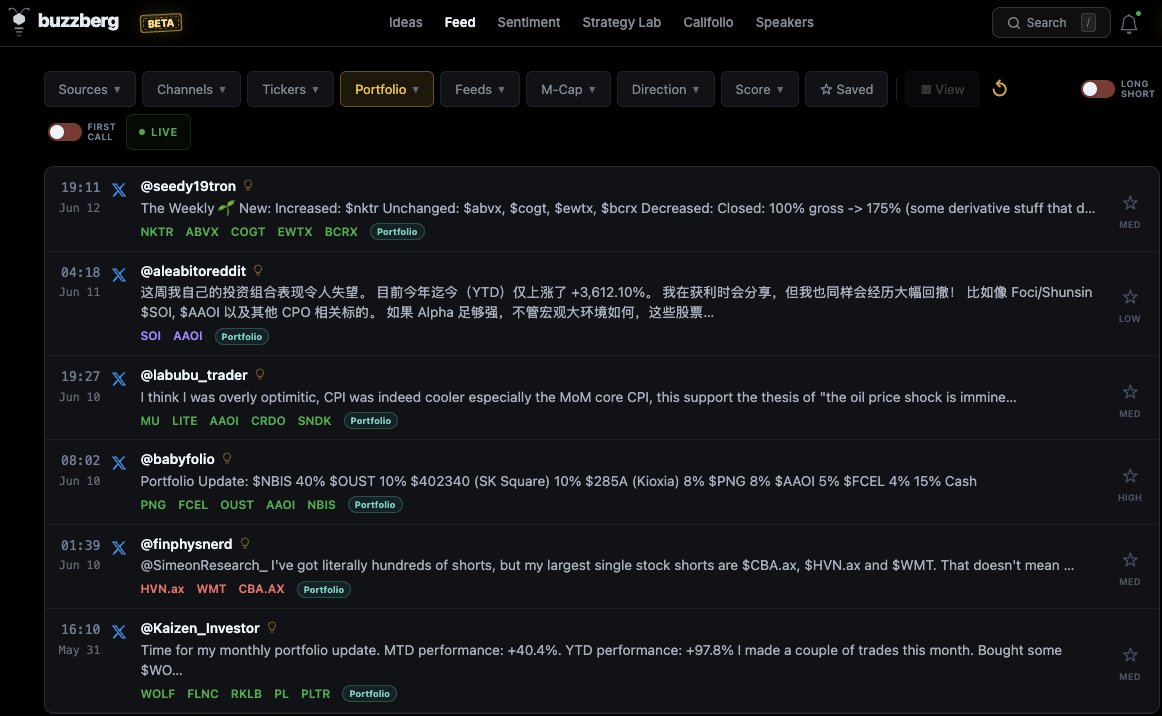

the post-type filters might be the most underrated thing we've shipped.

research / portfolio updates / stock lists / news — one tap each.

flipped on "portfolio" today — top of the feed: @seedy19tron 's weekly biotech update.👇

1

2

389

Jun 12

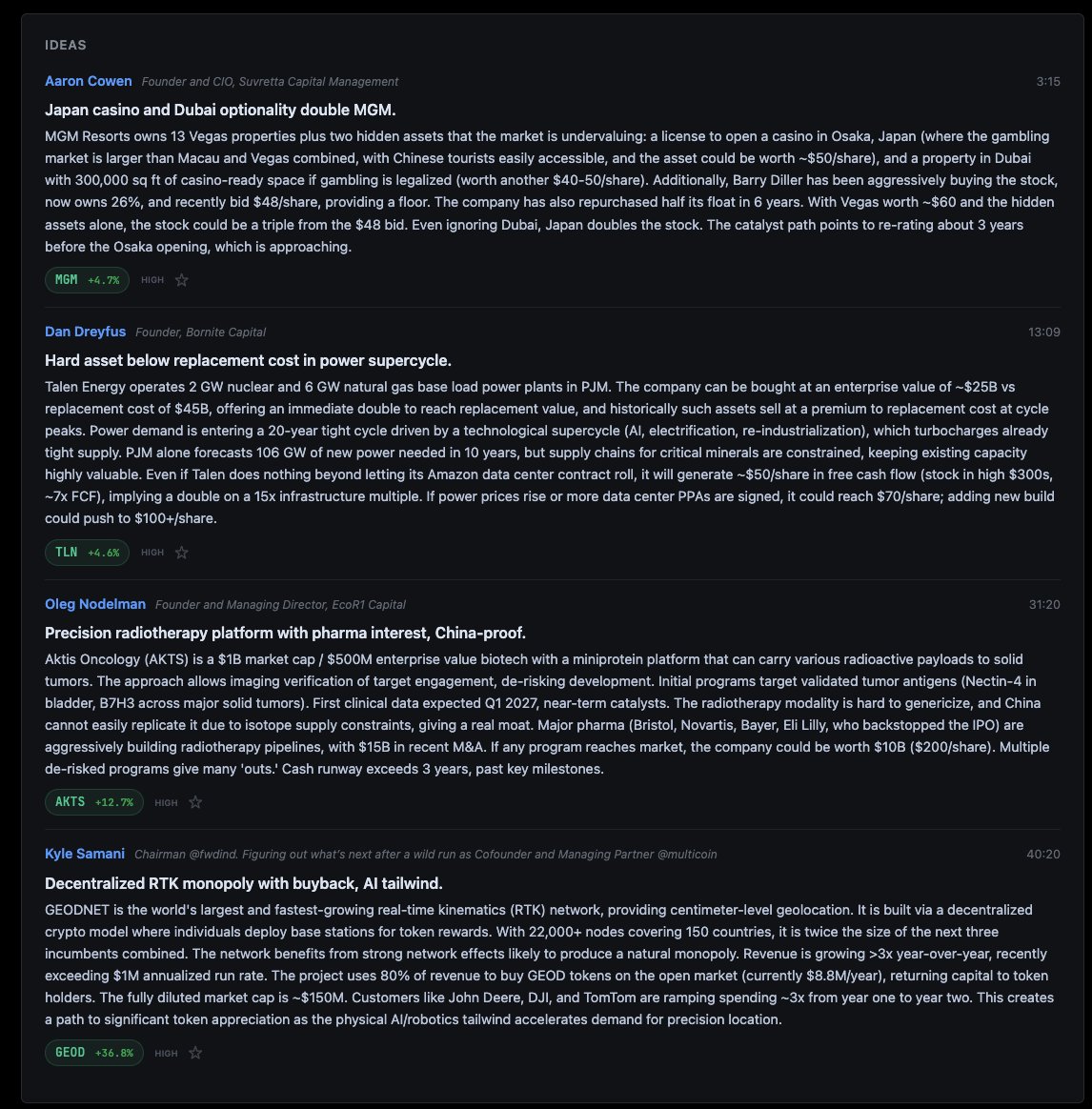

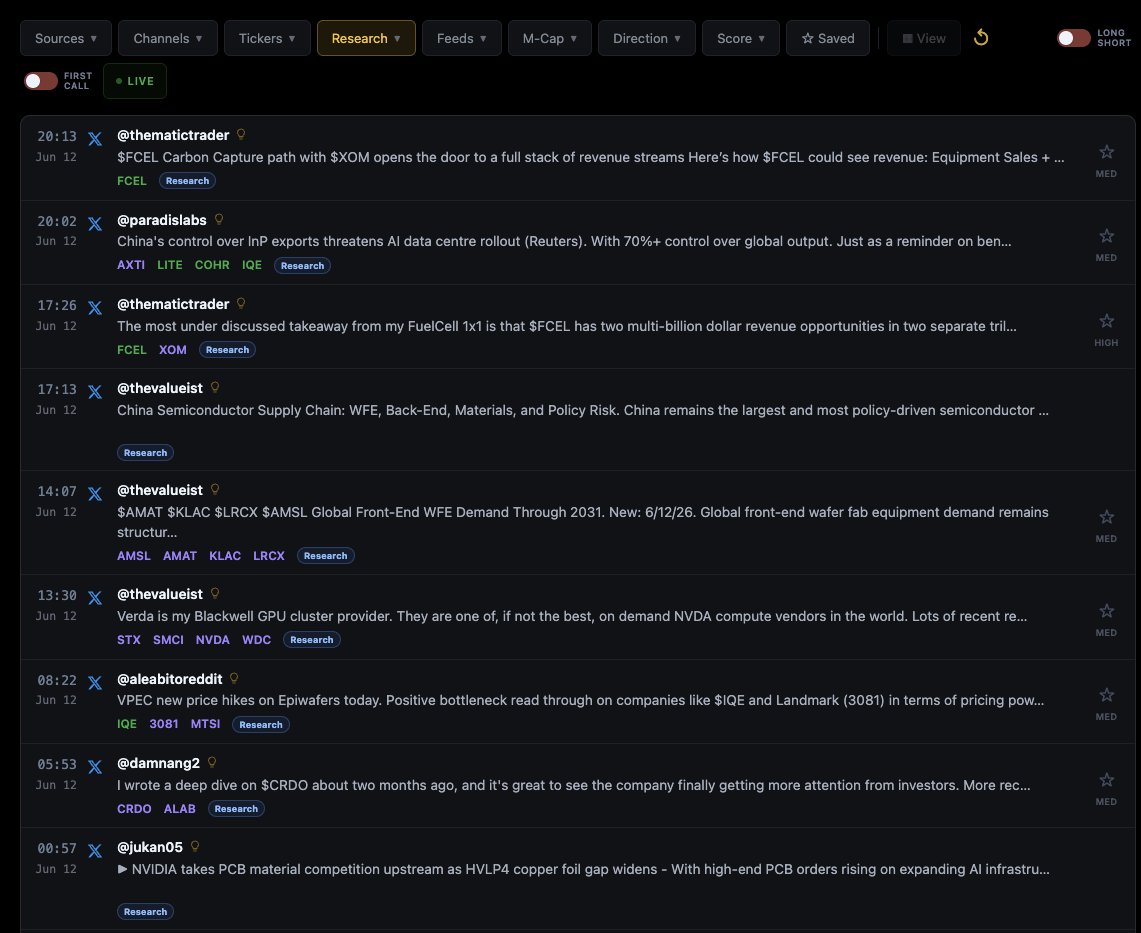

now flip the same filter to "research" — the feed turns into a reading list:

@TheValueist on china semis global WFE demand through 2031 @ThematicTrader 's $FCEL deep dive@damnang2's $CRDO deep dive @jukan05 on nvidia pushing PCB materials upstream @ParadisLabs on china's InP export grip @aleabitoreddit on epiwafer price hikes

1

2

467

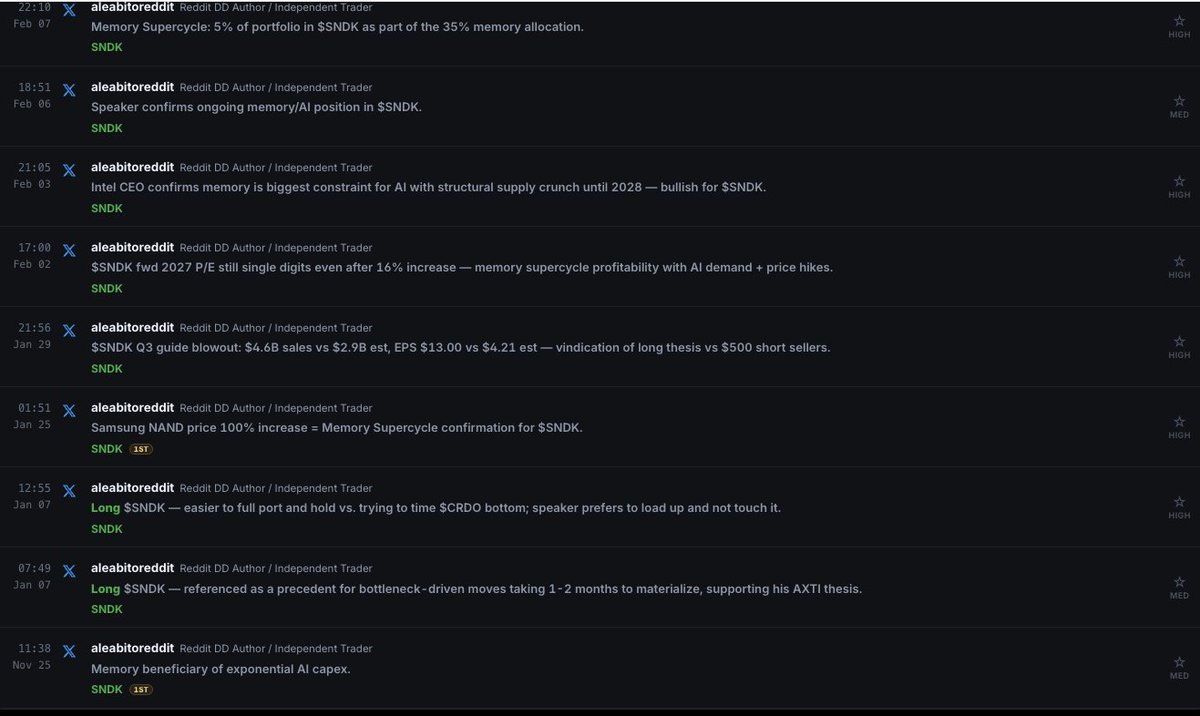

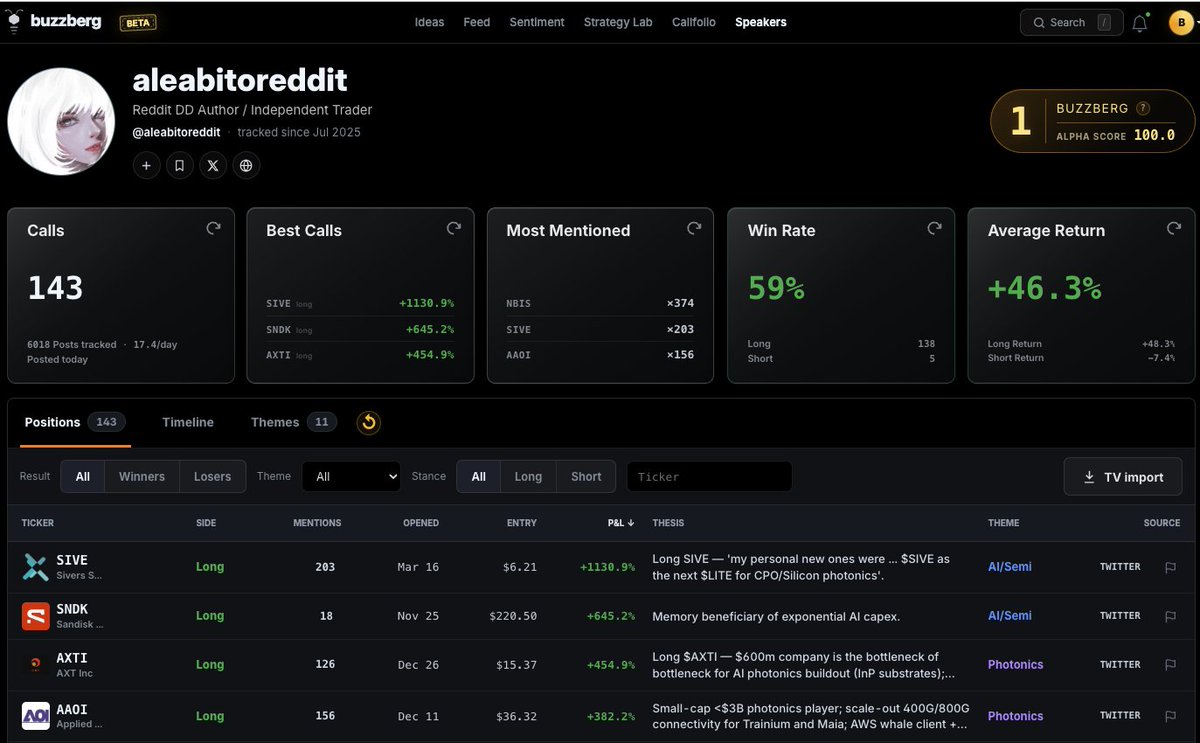

Jun 12

$SNDK is @aleabitoreddit 's #2 call on buzzberg, right after $SIVE.

first mention in our tape: nov 25, ~$220 — "memory beneficiary of exponential AI capex."

today: knocking on $2000.

full stats every $SNDK mention are on his speaker card

Jun 12

All the $SNDK short sellers went extinct.

Can’t believe it’s almost $2000 now?

That aside feels like everyone is just waiting for the $SPCX IPO in a few hours.

3

5

761

Jun 12

1

295

Jun 12

5/

Bob Greifeld, ex-CEO of Nasdaq, asks the question nobody wants answered: what happens when lock-ups expire and real supply hits the tape?

@cryptobyrde brings a calculator: at $2T, even a "small" 7% float is enormous dollars. The low-float story dies on contact with arithmetic.

1

1

276

Jun 12

Every take in this thread — sources, quotes, tickers — aggregated here: buzzberg.ai. And yes, we'll be tracking who was right.

1

246

Jun 12

Want to dig through all takes yourself?

Every $SPCX call in one place →

buzzberg.ai/trade-ideas/tick…

209