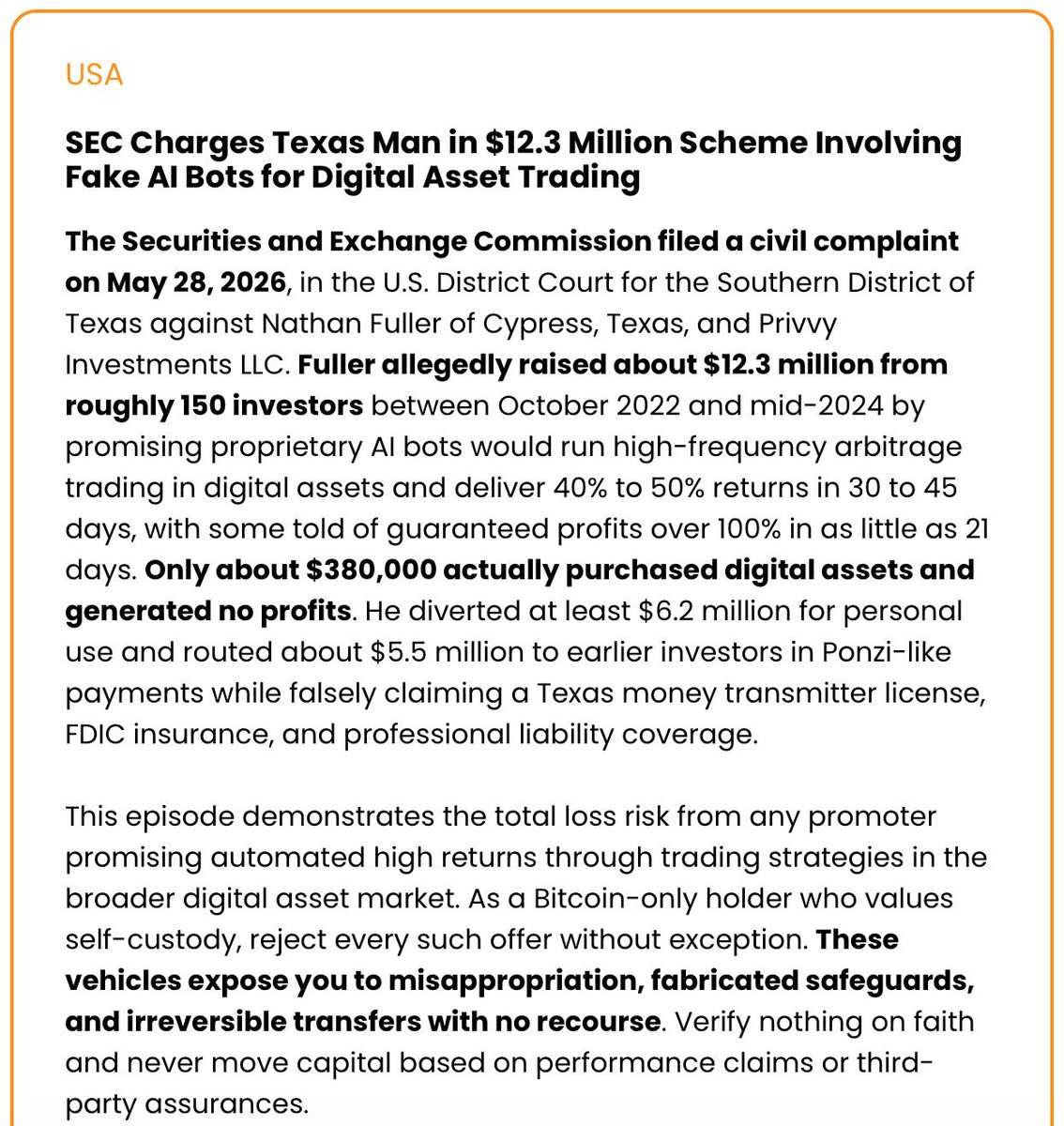

I'm a dad navigating life with geospatial data, BTC/blockchain, health tips, and fighting for freedom. Geodata & crypto affect us all! I don't respond to DMs!

Joined August 2010

- Tweets 12,953

- Following 2,930

- Followers 2,272

- Likes 100,506

1,336 Photos and videos

I am Pixels 🇺🇸 retweeted

Jun 11

This is the best ad for suppressors, ever.

115

686

7,833

406,404

I am Pixels 🇺🇸 retweeted

Jun 10

Employment Friday delivered one of the strongest jobs reports in recent memory. Non-farm payrolls came in at 172,000, blowing past the 88,000 expectation. Upward revisions added another 93,000. Wages grew at ~0.3%.

The market sold off anyway.

@CathieDWood thinks investors have the story backwards. Productivity is running near 3%. Unit labor costs are near half a percent. She says that is not an inflationary setup but a boom with contained costs.

The yield curve is flattening despite a ~55% surge in oil prices over three months. The bond market is not buying the inflation narrative. Neither are we. If the Iran war resolves and oil pulls back, inflation could go negative this year.

Capital spending has broken out of a 30-year range. The AI infrastructure buildout is creating a ripple effect across manufacturing. SpaceXAI built Colossus for roughly $30 billion and Anthropic is paying $15 billion a year to use it. We believe the returns on this infrastructure are unlike anything in prior technology cycles.

On the dollar, gold, and the inflation trade: prediction markets are pricing in a US Dollar Index reversal toward 101.9, gold peaked the day Kevin Warsh was appointed, and Cathie Wood believes the inflation trade may already be over.

From where we sit, the economy is healthier than the headlines suggest, inflation is lower than people fear, and the AI infrastructure cycle is just getting started.

3

3

40

14,765

I am Pixels 🇺🇸 retweeted

Based Bitcoin not participating in Pride Month

67

151

2,371

78,072

I am Pixels 🇺🇸 retweeted

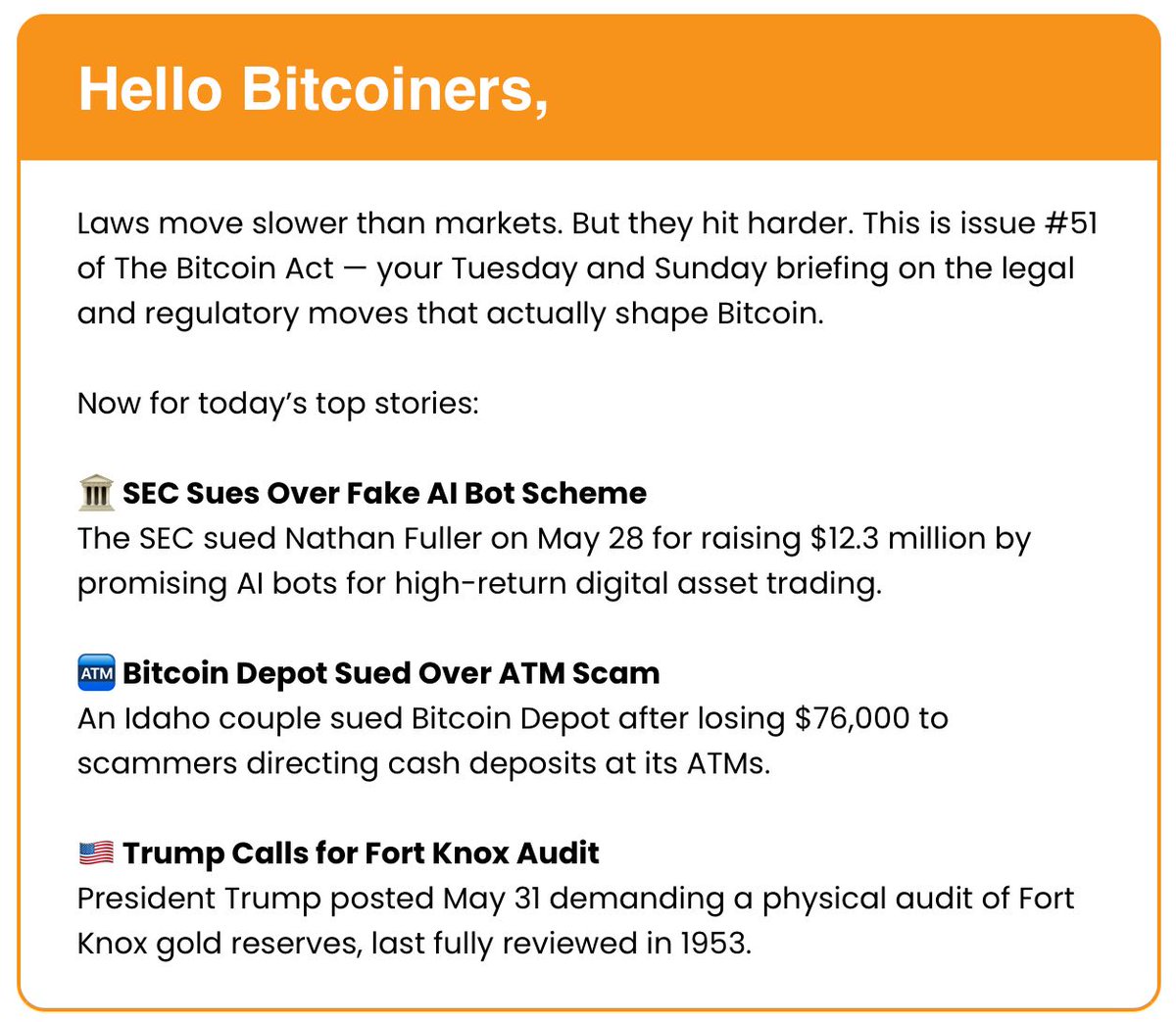

⚡️ Issue #51 of The Bitcoin Act newsletter is live!

🧡 Dive into the latest global moves reshaping #Bitcoin regulation and adoption.

👉 For subscribers, don’t forget to check and claim your free sats!

👉 Full issue here: thebitcoinact.xyz

3

4

16

378

May 16

💯

May 15

No Trump judges, no voter ID SAVE Act, 50 bills already passed by the house in limbo.

Pardon my language, but this guy is a worthless piece of shit. He’s worse than a grifter Democrat. Fetterman has done more for the Republican platform than this weasel. Treacherous rat.

1

2

25

I am Pixels 🇺🇸 retweeted

May 13

Today I got the opportunity to show Georgia state senator Greg Dolezal around the property that @GeorgiaPower is trying to take from my family through eminent domain. I will not stop fighting!

307

3,671

11,823

221,704

I am Pixels 🇺🇸 retweeted

May 14

1.8% volatility. 4.35 Sharpe. 11.5% yield. Record date tomorrow. Today is Stretch Day. $STRC

350

560

5,699

243,331

May 12

Small steps compound into vast change. Incremental improvements & daily discipline are a quiet refinement to build a life of strength. It's not the grand gesture but the steady hand that shapes the future.

1

6

32

I am Pixels 🇺🇸 retweeted

May 10

Since I won 120,00 I’ll give one person 10k who likes this tweet and follows me.

Let’s go

16,653

8,620

216,494

11,461,902

I am Pixels 🇺🇸 retweeted

May 9

$STRC is credit engineered for income, stability, liquidity, and principal protection. It is backed by our BTC and USD assets and supported by active treasury operations. We structured it as preferred equity rather than debt to make it more scalable, durable, global, and useful.

447

688

6,637

277,146

I am Pixels 🇺🇸 retweeted

🚨 GIVEAWAY 🚨

We’re giving away a BitForge Nano Ghost Edition — a home-worthy Bitcoin miner designed to be seen, not hidden in a shed.

To enter:

Follow @TheSoloMiningCo

Repost this post

Reply with where you’d put it and why.

Winner announced 1st June 2026

The Solo Mining Co: Your Rigs, Your Rewards. ⚡

830

818

894

48,306

I am Pixels 🇺🇸 retweeted

⚡ GIVEAWAY — 121,000 sats ⚡

I'm giving away 121,000 sats to one Bitcoiner.

To enter:

✅ Repost this post

✅ Follow @The_Bitcoin_Act

✅ Subscribe → thebitcoinact.xyz

Winner picked in 24h. #Bitcoin #Giveaway

141

133

164

3,958

I am Pixels 🇺🇸 retweeted

May 1

Happy Free Sats Friday! 🔥

1. Reply with your #bitcoin lightning address ⚡️

2. We'll send you some sats

3. Ends at 3pm GMT

This week’s sponsor: @englishlakes 🧡

A group of 3 hotels accepting #Bitcoin, located in the Lake District & North Lancashire 🇬🇧

More info in the comments 👇

1,272

317

783

32,917