Author, Marketcrafters: The 100-Year Struggle to Shape the American Economy. Co-Founder & Chair @EconomicSecProj.

Joined February 2009

- Tweets 2,043

- Following 1,350

- Followers 40,870

- Likes 499

53 Photos and videos

Chris Hughes retweeted

May 7

Come to @BrookingsInst Tuesday 5/12 where I'll ask @SenAdamSchiff all about prediction markets, and a panel of experts like @CFR_org Lazarus, @tphillips, and @Kalshi Heaslip will debate this moderated by @WSJ @kryshur. Register here:

brookings.edu/events/the-ris…

SCOOP: Campaign staff are gaming prediction markets using internal data to make timely bets on their candidates — winning “thousands.”

One staffer told me it would have been “foolish” not to bet. Another staffer called it the “Wild West”

npr.org/2026/05/07/nx-s1-579…

6

16

6,170

Chris Hughes retweeted

Apr 28

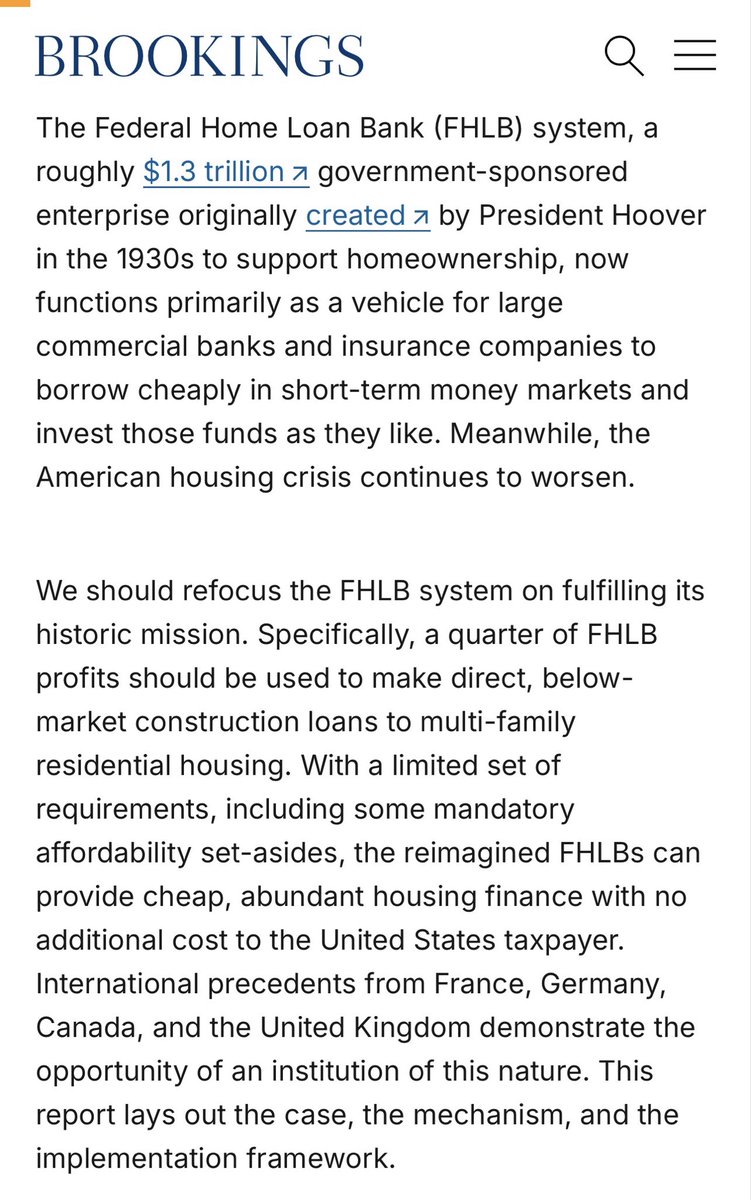

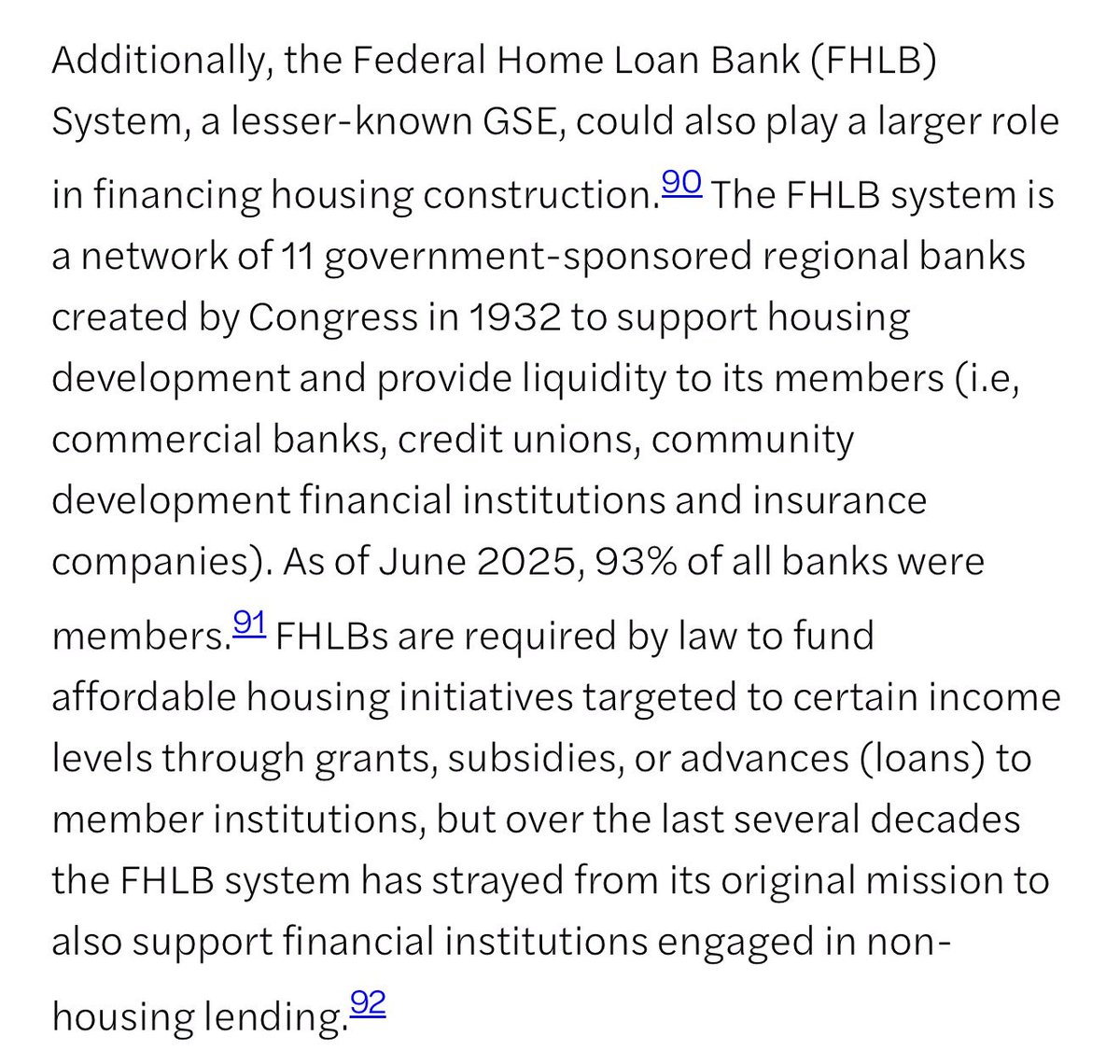

How to build almost 200,000 new affordable houses a year by returning the FHLB system to its original housing mission from what it’s become, profits for financial firms. My latest w/@chrishughes in @BrookingsEcon

brookings.edu/articles/refor…

6

14

1,331

Apr 27

More details on a low-cost way to quickly build ourselves out of the housing crisis. And no, it doesn't involve zoning reform. New report I co-authored with @Aarondklein from @BrookingsInst

brookings.edu/articles/refor…

1

3

3

2,732

Chris Hughes retweeted

Apr 8

Love this piece by @chrishughes on leveraging the Federal Home Loan Banks to invest in housing construction, including affordable housing. @MikeFellman and J.W. Mason made the same case in their @Groundwork paper:

America has a housing crisis, and we can’t begin to address it by just focusing on increasing supply and loosening red tape. We have to look at how housing gets financed, and we might be failing to utilize one of our best tools: a nearly 100-year-old bank that could do just that.

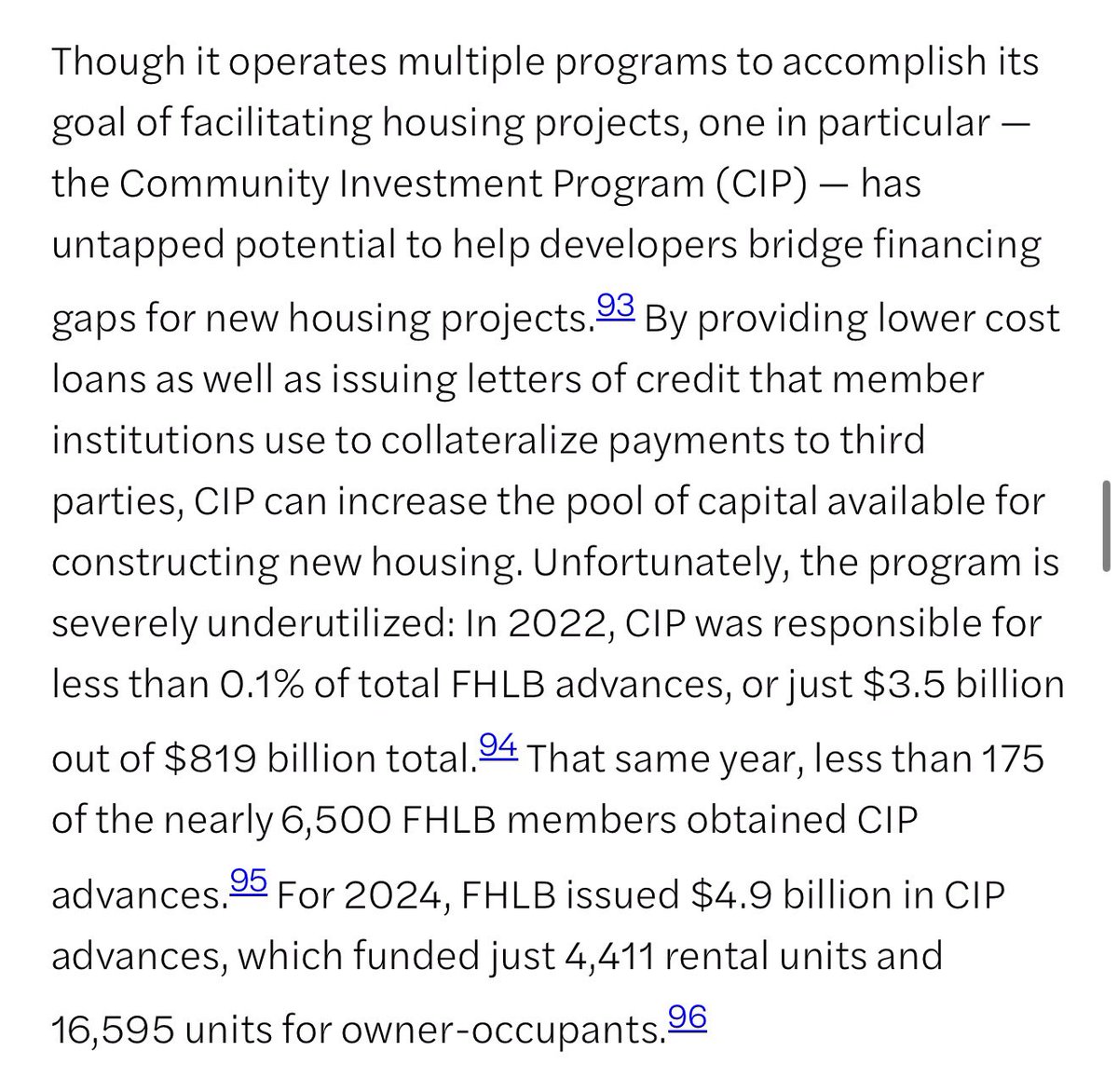

The Federal Home Loan Bank System (FHLB), created in 1932, is a New Deal-era network of 11 regional banks with 6,500 member institutions intended to provide financing to American families at preferred rates (typically at 2-3% below commercial banks).

But the FHLB is no longer fulfilling its original promise to prospective homeowners; instead, it primarily services big banks and insurers who wisely recognized they could get cheaper rates. Today, only 13 cents of every dollar the FHLB earns goes toward affordable housing, and more than 40% of its member institutions don’t even give out mortgages.

This leaves a funding gap for medium-sized multifamily buildings, or the "missing middle" as housing experts call it. These are housing units too small for big developers and too large for conventional mortgages. But cheaper loans could finally make these projects viable, opening up a whole new stream of housing supply.

In a new @nytimes op-ed, ESP co-founder @chrishughes breaks down how we can redirect FHLB lending towards multifamily construction, produce 200K new units a year, and get more Americans into homes – without any cost to taxpayers. He argues we can make the FHLB serve the American people again and, with it, chip away at the country’s housing crisis. nytimes.com/2026/04/08/opini…

3

15

51

8,974

Chris Hughes retweeted

Apr 8

Fantastic must read article by @chrishughes in @nytimes laying out an aggressive, progressive vision to tackle housing and turn the FHLB from a source of bank profits to an engine powering homeownership for young Americans. My gift to you:

nytimes.com/2026/04/08/opini…

2

7

948

Chris Hughes retweeted

AI systems are now writing code, diagnosing diseases, designing buildings, and even generating art. Tools like @ChatGPTapp, @claudeai, @GoogleDeepMind, and autonomous robots are reshaping industries once thought immune to automation. Will AI usher in a new era of prosperity and leisure or a future of unemployment and inequality?

Featured Debaters:

Dr. @ruchowdh, @chrishughes (@economicsecproj), Simon Johnson @baselinescene

(@MITshapingwork), and @AndrewYang. Moderated by @JohnDonvan.

This is the fifth debate of The Hopkins Forum series, co-presented by @snfagora of @johnshopkinsu and @opentodebateorg. Photo credit: Poll Bravo of @JHUBloombergCtr.

Watch now on YouTube, or listen on Spotify and Apple Podcasts.

4

7

22

11,812

Chris Hughes retweeted

Feb 11

Live Debate: @AndrewYang, @chrishughes, Simon Johnson (@baselinescene), and Rumma Chowdhury on AI & the Future of Work

Tools like ChatGPT, Claude, and autonomous robots are transforming industries once thought automation-proof — fueling fears of widespread job loss. Will AI Make Work Obsolete?

📅 Wednesday, February 25 | 6:45 PM

📍 @JHUBloombergCtr | Reception to follow

Presented by @SNFAgora and @opentodebateorg

Reserve your free tickets before they sell out: bit.ly/workobsolete

5

2

13

51,382

Feb 24

How much value does the Fed's operating system create for commercial banks? In a new @BrookingsInst paper, Josh Younger and I quantify two channels of transfer from the public to the private sector under ample reserves, peaking as high as $200bn annually brookings.edu/articles/the-f…

1

4

8

921

Feb 24

I explain what's going on in plain English on Substack here open.substack.com/pub/chrish…

1

416

Jan 20

Bank regulation and monetary policy are inextricably intertwined. The Supreme Court should let both stay independent from the White House open.substack.com/pub/chrish…

1

3

650

Chris Hughes retweeted

Jan 13

Cryptocurrency is an asset masquerading as a payment instrument. Congress did not see through this illusion and created a dangerous loophole allowing "rewards" for stablecoins that don't add up. If Congress doesn't close this loophole problems are coming.

brookings.edu/articles/inter…

12

11

20

18,017

Jan 12

Congress just authorized a $200 billion foreign investment bank, and almost no one noticed. The Development Finance Corporation could reshape American statecraft. But under this WH it could also become a tool for corruption. My latest in @ForeignPolicy foreignpolicy.com/2026/01/12…

3

662

Chris Hughes retweeted

7 Nov 2025

Come join us in a conversation with @chrishughes and @JWMason1 on Monday, November 17!

6

11

2,940

Chris Hughes retweeted

11 Nov 2025

Facebook Co-Founder & Economic Security Project Co-Chair @chrishughes discusses President Trump's industrial policy & the government's role in data center investment: cnb.cx/3XrDfIg

3

2

4

8,004

Chris Hughes retweeted

10 Nov 2025

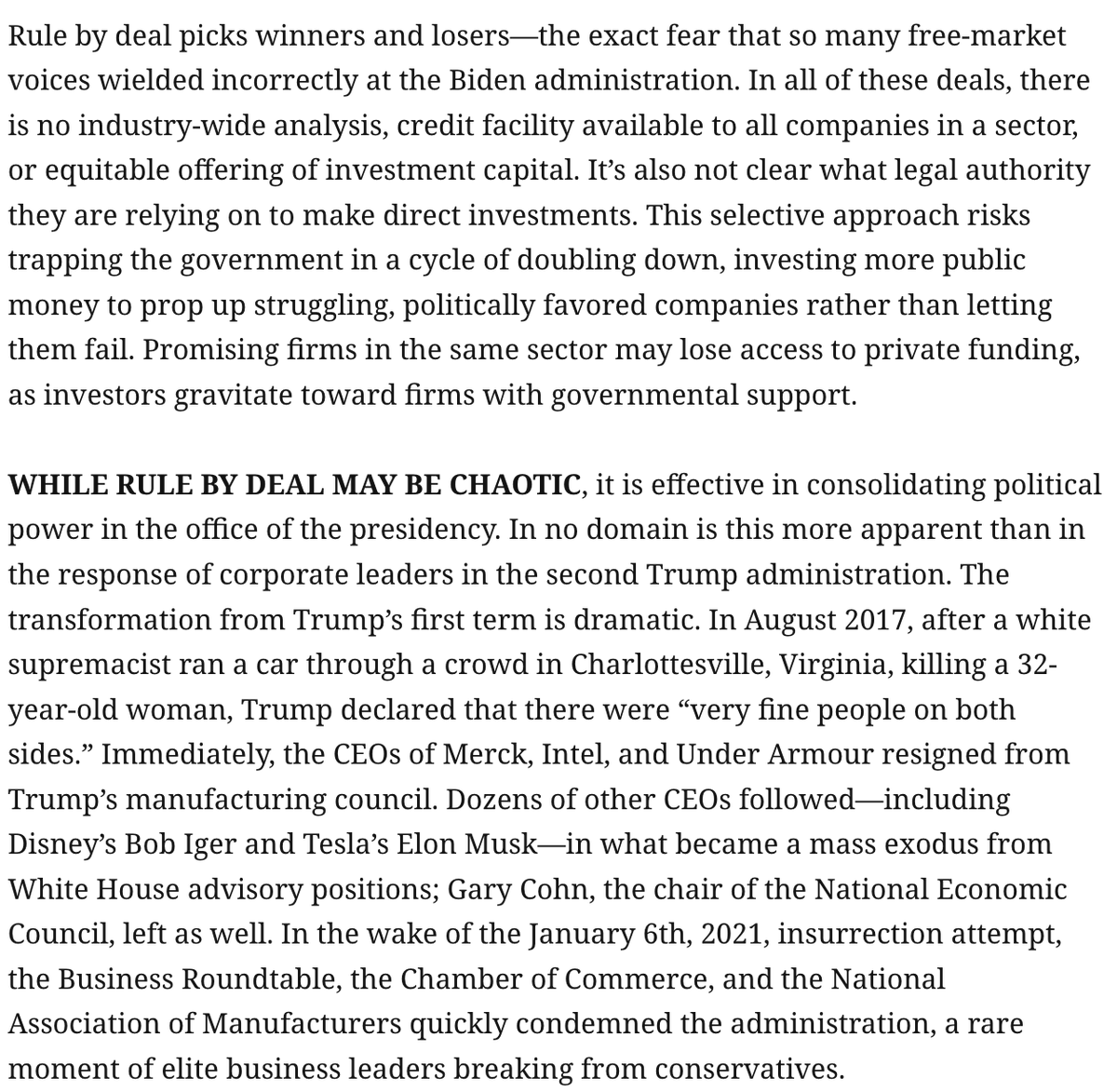

Trump has positioned himself as a leader who rules by the art of the deal. But far from a master organizer of state capitalism, Trump’s deals with the private sector seem to lack any coherence. From @chrishughes:

trib.al/cTElMzO

2

5

1,475

Chris Hughes retweeted

10 Nov 2025

We have some shutdown stuff coming, but I want to turn your attention to this great piece from @chrishughes , who has really done the best analysis on what Trump economics is: not industrial policy or right populism or America First. It's rule by deal.

prospect.org/2025/11/10/trum…

4

33

83

8,180

23 Sep 2025

RT @the_vello: Graham Platner held his first town hall this evening in Ellsworth.

Over 850 people showed up.

We thought we’d get 200 peo…

193

Chris Hughes retweeted

21 Sep 2025

We are fast becoming a banana republic, with two standards of justice. If you oppose the leader, you go to jail just for speech. If you're a loyalist, you get immunity for your crimes.

That's what happens in Iran - not the United States. This is a decision moment for America.

5,491

7,458

29,335

1,206,257

Chris Hughes retweeted

5 Sep 2025

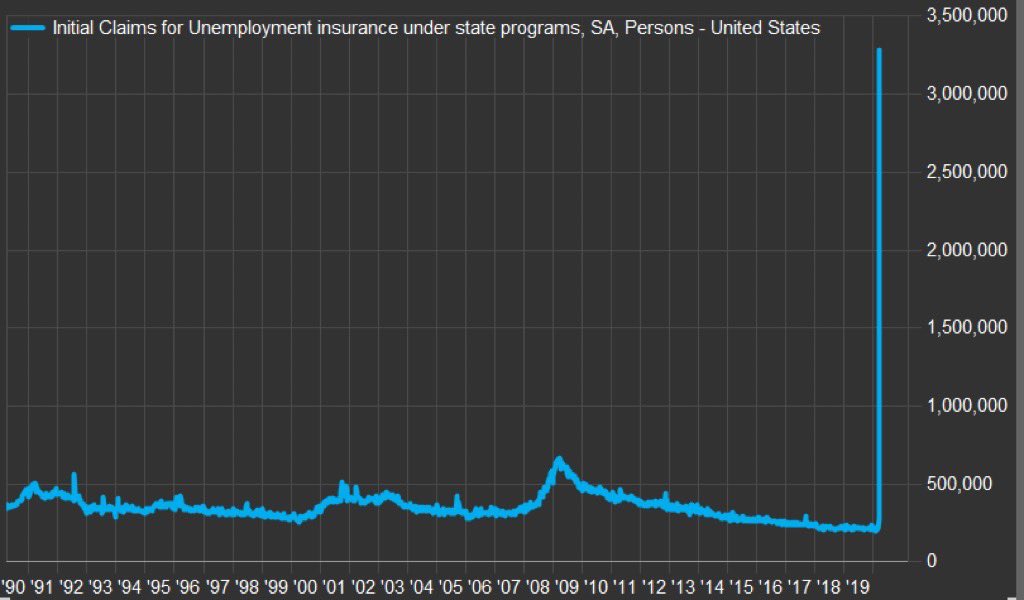

Job growth usually only weakens like this when we're headed for a recession

There may be reasons why this time is different (immigration, partial trade shock reversal), but the data is poor

Accounting for all the revisions, Reported 1-Quarter job growth is now just 37k/month

9

76

289

91,100

Chris Hughes retweeted

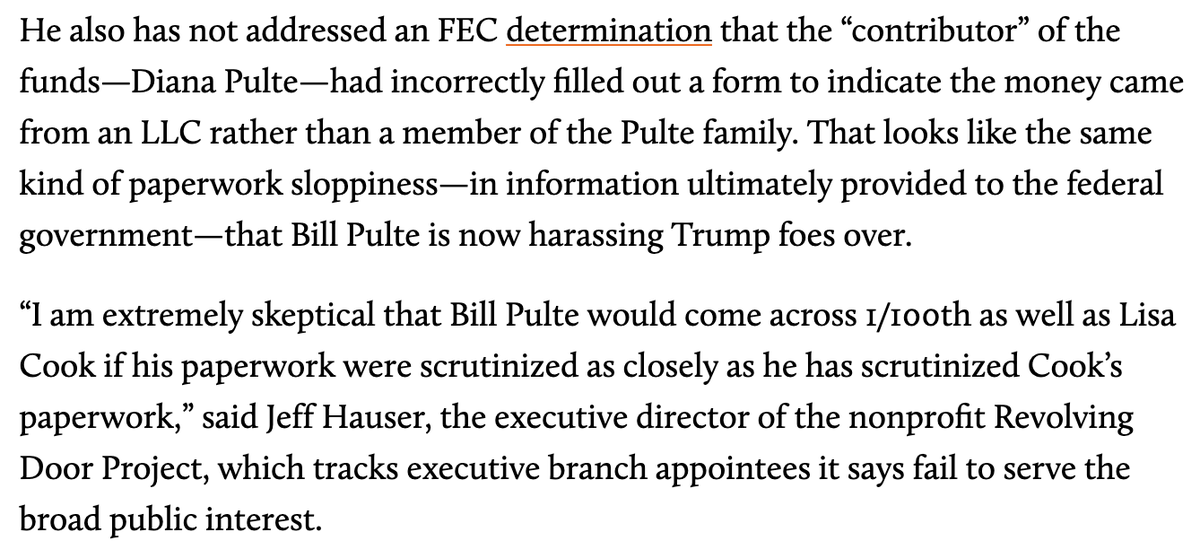

29 Aug 2025

"Pulte did not respond to questions about why the donation went through a shell company, if he was involved in the donation credited to his wife, or whether the large donation helped him land his job in the administration."

12

391

767

44,981