Joined February 2025

- Tweets 1,142

- Following 383

- Followers 4,729

- Likes 1,501

354 Photos and videos

Pinned Tweet

Jun 12

In collaboration with GoldFix (Vince Lanci) @Sorenthek The Competent Investor is happy to introduce our weekly Market Show. Please let us know what you think, we're still polishing a few details and are welcoming of any suggestions. Thanks! #Markets

4

12

34

3,038

Jun 12

What a lovely chart

1

18

1,766

Jun 11

The bond market's dysfunction is largely a Western issue linked to passive investing, according to Green. Investors need to recognize these shifts. #BondMarket @profplum99

1

1

9

711

Tom Bodrovics retweeted

Jun 11

The last time gold and silver sat where they're sitting right now, gold ran 240% and silver ran 320%.

The same 4-phase pattern is repeating:

1) Panic selling

2) Fear settles

3) Central banks accumulates

4) Breaks past new highs

Why I believe we're in Phase 2 right now:

27

80

592

67,330

Tom Bodrovics retweeted

If you wonder how gold price could be tanking in the face of spiking systemic risks, recall that credit protection on subprime mortgage bonds was tanking in 2005-2007.

After 2008, they made a movie about the few who stuck w/their conviction & kept buying.

32

80

843

80,052

Jun 10

In today's complex world, many mistake models for reality. As @ctindale notes, this delusion leads to critical dependencies that are now being exposed. It's time to rethink our approach to #Global supply chains. #Economy competentinvestor.com/fallin…

3

12

2,299

Jun 9

Again…

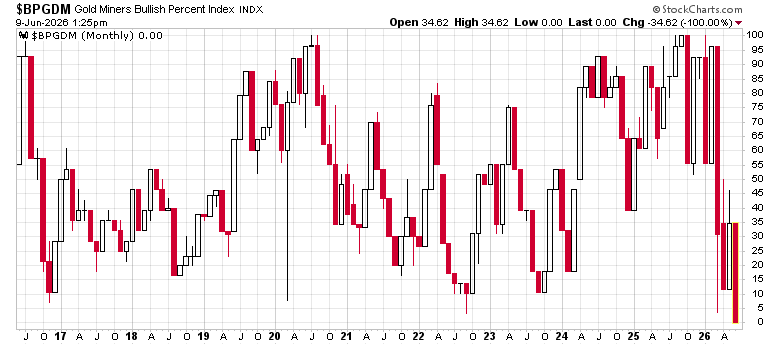

Jun 9

The Gold Miners Bullish Percent Index drops to zero. Yes, you read that correctly. Historical 👀🔥

Total capitulation.

2

5

33

3,801

Tom Bodrovics retweeted

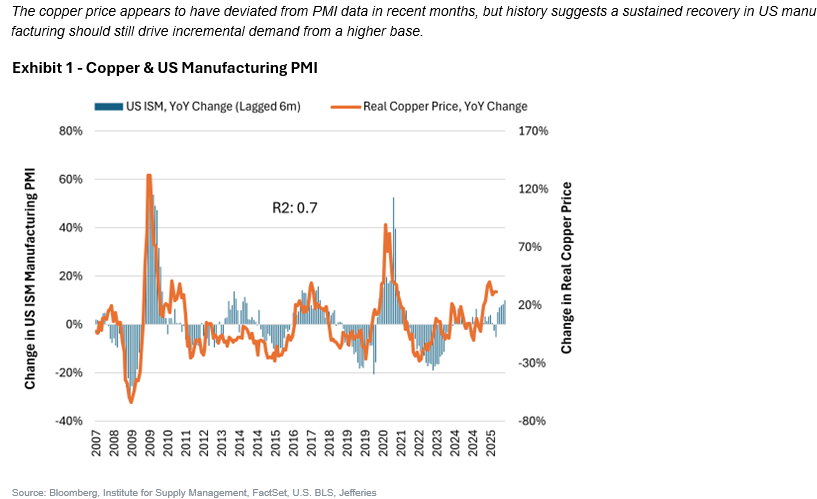

@Jefferies' analysis out this morning states that they expect the US to drive up all industrial commodities... with copper as the best performer.

"Our analysis suggests the recovery in US PMI data should begin to feed through into copper demand in the coming months (the index has been >50 for 5 months after 3 years of weakness). At the same time, the potential for targeted credit easing in China and sustained fiscal expansion in the US support the backdrop for global money supply growth from current levels. Note that US M2 grew at a 7.2% compounded annual growth rate (CAGR) from 1971 until August 2022, but has grown at an average rate of just 0.8% since then, suggesting the Fed has significant room to ease as long as inflation subsides.

Copper should be the best‑performing major commodity within our coverage in a scenario where global M2 growth and US manufacturing activity simultaneously accelerate, but all industrial metals should benefit. A recession due to a sustained oil price spike or Fed rate hikes are clear risks. However, we believe the signs pointing toward a potential multi-year upcycle skew the risk/reward trade-off to the upside and support our call for a rising copper price to a (real) peak of $8.00/lb by 2030-31.

3

24

96

6,280

Tom Bodrovics retweeted

Jun 8

AI-related CapEx is bigger than every CapEx cycle in history.

All previous CapEx manias have resulted in massive write-offs.

This time will not be different.

39

256

883

140,875

Tom Bodrovics retweeted

Jun 8

Here are gold holdings of the central bank of Turkey. Looks like we have come a long way in terms of cleaning out.

zerohedge.com/the-market-ear…

7

12

86

52,169

Tom Bodrovics retweeted

BREAKING: Iran says it has now fully blocked the Bab el-Mandeb Strait, along with the complete closure of the Strait of Hormuz, with the next step being strikes on oil, gas and energy infrastructure of US-allied Gulf countries in response to today's Israeli strikes on the Petrochemical Complex, per a source close to Iran's Ghalibaf.

141

1,801

7,843

574,614

Jun 6

Explore @UrbanKaoboy Michael Kao's four macro quadrants that define economic scenarios, from #stagflation to the ideal Goldilocks environment. Understanding these could become a key reference for investors. #Disinflation #Commodities

1

11

906

Jun 6

Michael Kao (@UrbanKaoboy) discusses the economy's precarious balance, stating, "we're currently walking a tightrope between wildly divergent macro outcomes." Is inflation or stagnation ahead? #Economy #Stagflation

3

4

16

4,901

Tom Bodrovics retweeted

What just happened?

The S&P 500 just erased nearly -$2 TRILLION of market cap just hours after 3rd strongest US jobs report in 18 months.

Meanwhile, Bitcoin is officially down over -50% from its record high in October 2025.

What's happening? Let us explain.

(a thread)

735

2,237

16,519

5,624,232

Tom Bodrovics retweeted

Jun 5

What we are watching in markets are the first cracks in the illusion that the US can fund $2T deficits in perpetuity, fund debt-funded AI buildouts, reshore the industrial base, fund the Iran war, and roll over existing US Federal debt without YCC or its functional equivalent.

114

276

1,945

132,405

Tom Bodrovics retweeted

Jun 5

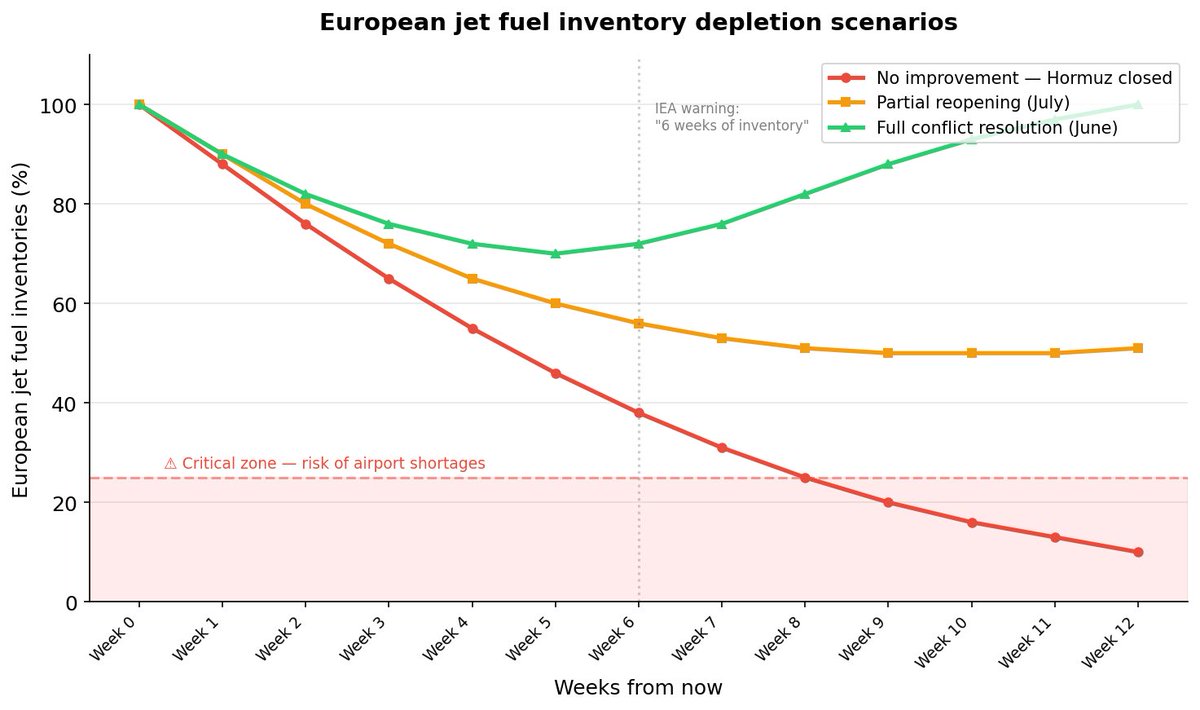

Europe’s jet fuel situation is deteriorating rapidly.

Spain, France, Italy, and others have warned private aviation operators that jet fuel may be unavailable this summer…at any price. Commercial aviation isn’t immune: 30–50% of flights will face disruption or cancellation.

After 97 days of inventory draws, distillate supplies are heading below critical levels. If the IRGC’s stance on highly enriched uranium remains unchanged, euro-area shortages could become critical within two months.

86

282

1,067

196,923

Tom Bodrovics retweeted

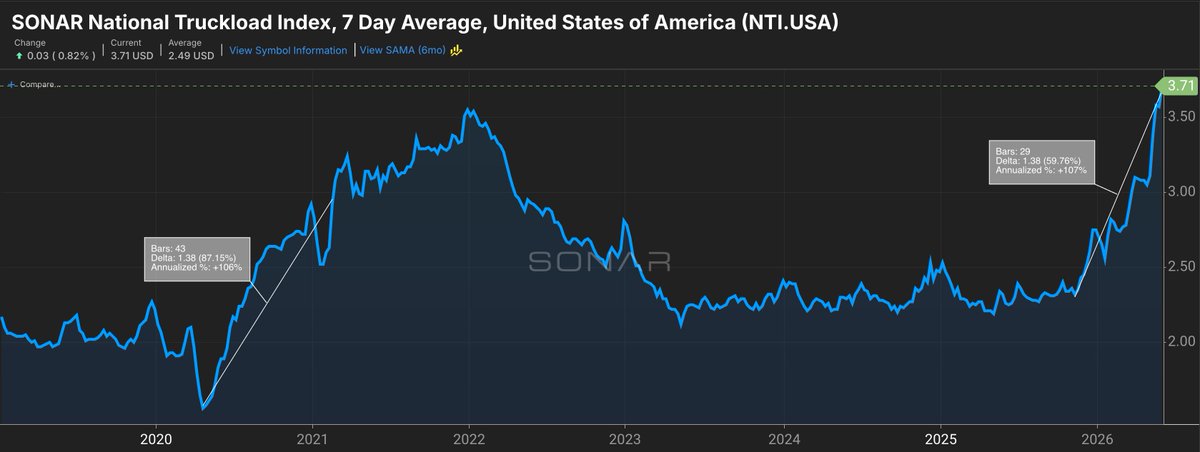

Trucking spot rates have never moved up this fast, ever - including early COVID.

The weekly average for truckload spot rates moves to a new all-time high of $3.71/mile.

It took 43 weeks for spot rates to increase by $1.38/mile during early COVID (April - Feb 2021).

It has taken only 29 weeks to achieve the same increase (Nov 2025 - June 2026).

37

130

660

71,128

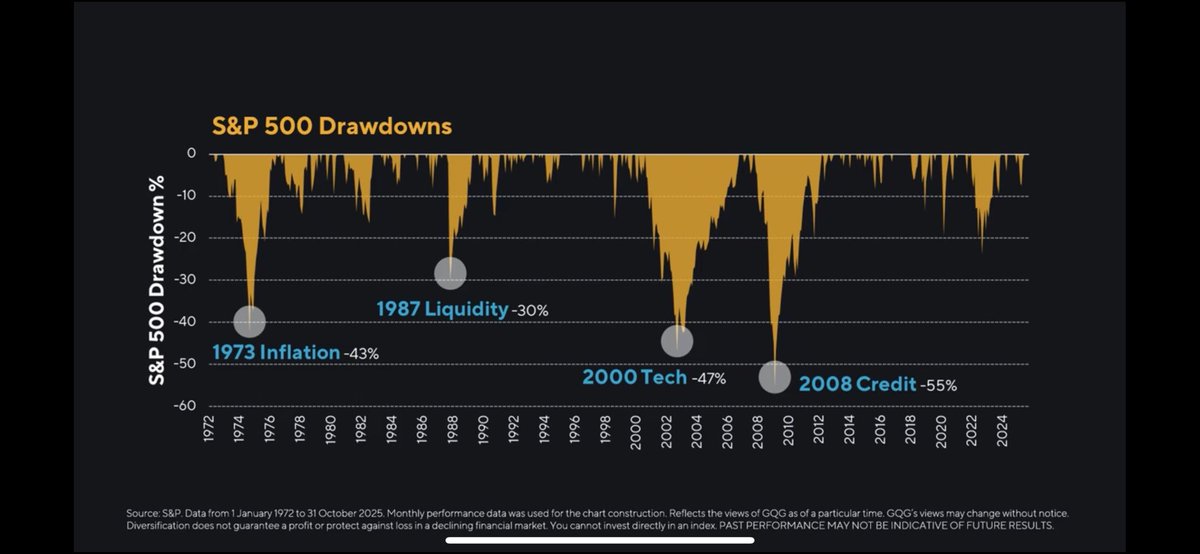

Jun 3

All 4 market risks present at once 😳😳

🚨 We may be looking at the rarest market setup in 50 years.

The S&P 500's four historic drawdowns since 1972:

– 1973 Inflation: -43%

– 1987 Liquidity: -30%

– 2000 Tech: -47%

– 2008 Credit: -55%

Each one was driven by ONE dominant risk.

Right now, all four are present at the same time.

1. INFLATION

A commodity supercycle. Energy, metals, agriculture all in multi-year base breakouts. The Fed's preferred inflation gauge has been above 2% for 18 of the last 24 months.

2. LIQUIDITY

The largest equity supply shock since 2000. SpaceX, OpenAI, Anthropic raising ~$275B combined. Google flipping from $60B/year buybacks to $80B net issuance. Over $1 trillion of IPO and lockup supply hitting the Russell 3000 in 2026.

3. TECH

Semiconductors trading 73% above their 200-day moving average – the largest stretch since March 2000. Climax run signals across the AI complex. Micron, Palantir, SMCI, the SOX index, all showing the textbook O'Neil sell pattern.

4. CREDIT

Apollo, KKR, BlackRock, Blue Owl, Cliffwater, Partners Group – all gating redemptions on their evergreen funds in the last 90 days. The private credit machine is freezing in real time.

Never in 50 years have all four risks been simultaneously present.

But here's the part nobody talks about

While the AI Big 10 has gone vertical, quality stocks have been left for dead.

– Berkshire Hathaway: trailing the S&P 500 by hundreds of basis points

– Coca-Cola, Procter & Gamble, Pepsi: trading at multi-year relative lows

– HEICO, Union Pacific, MSCI: making boring new highs while everyone watches Nvidia

– Healthcare vs. S&P 500: 25-year relative low

The last time this happened?

December 1999. Barron's ran a cover titled "What's Wrong, Warren?" – mocking Buffett for being a dinosaur, for missing the internet, for refusing to pay for growth at any price.

Berkshire was down 19% in 1999 while the Nasdaq was up 85%.

What followed:

– Berkshire 29% over the next 24 months

– Nasdaq -78% over the next 30 months

The setup today

Four historic risks stacked simultaneously, while the boring, durable, cash-flowing businesses that always survive these regimes have been treated like dead money for years.

The math doesn't get more asymmetric than this.

Quality stocks aren't out of style.

They're being orphaned.

That's when generational positions are built.

The boring stuff hasn't worked for a long time.

History suggests that's exactly the moment it starts to.

1

7

1,453