cryptoyolo.algo | Living on the blockchain cryptoyolo7.nft bc1qywcj6zd0jme6kc8ukrxf5n9w2hx0f8qzs6fwu2

Joined October 2021

- Tweets 4,698

- Following 754

- Followers 1,761

- Likes 2,340

100 Photos and videos

CryptoYOLO retweeted

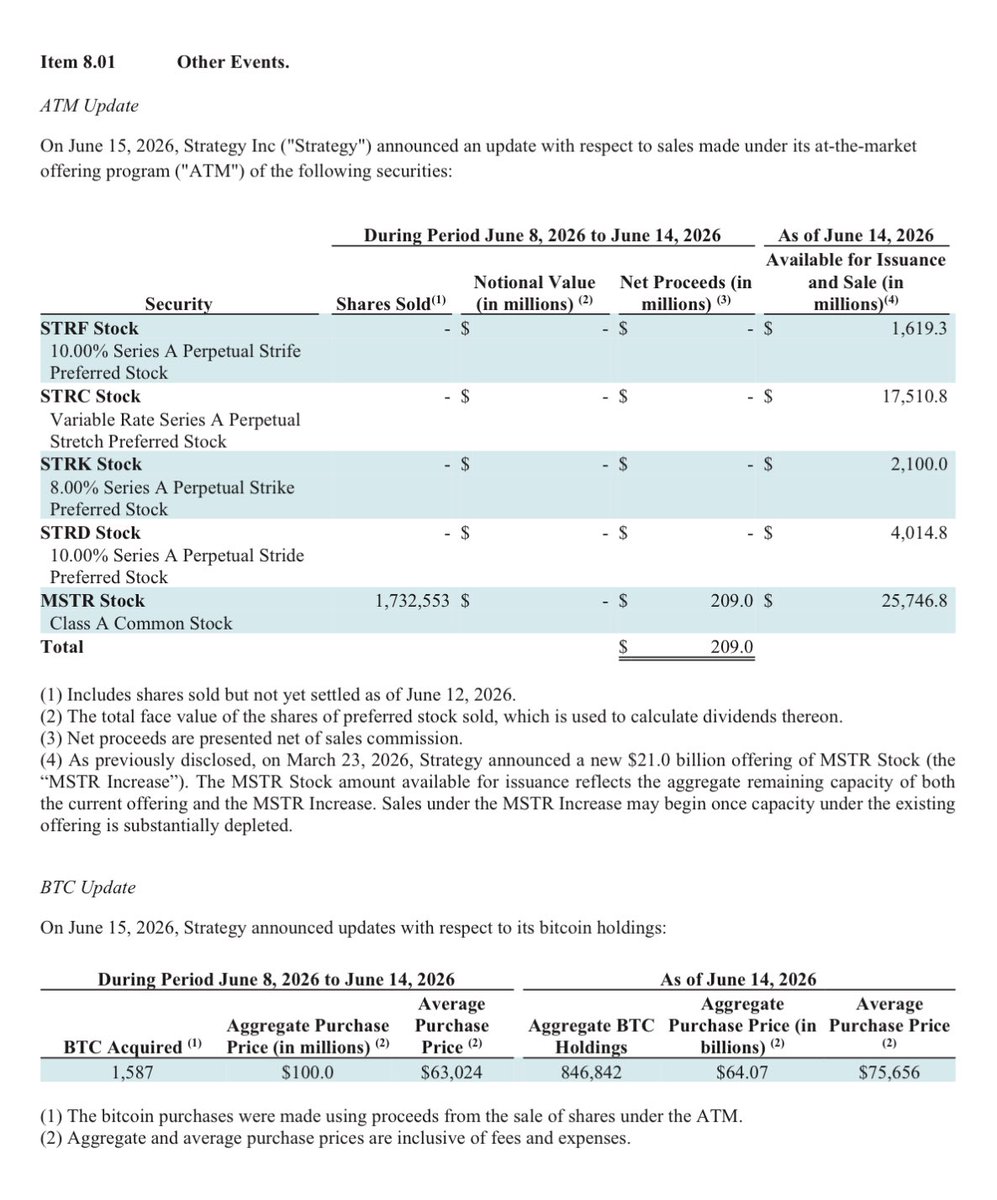

Strategy has acquired 1,587 BTC for $100 million to increase our $BTC Reserve to ₿846,842. We have also increased our USD Reserve by $100 million to $1.1 billion. $MSTR $STRC strategy.com/press/strategy-…

870

1,643

12,981

817,881

CryptoYOLO retweeted

Jun 11

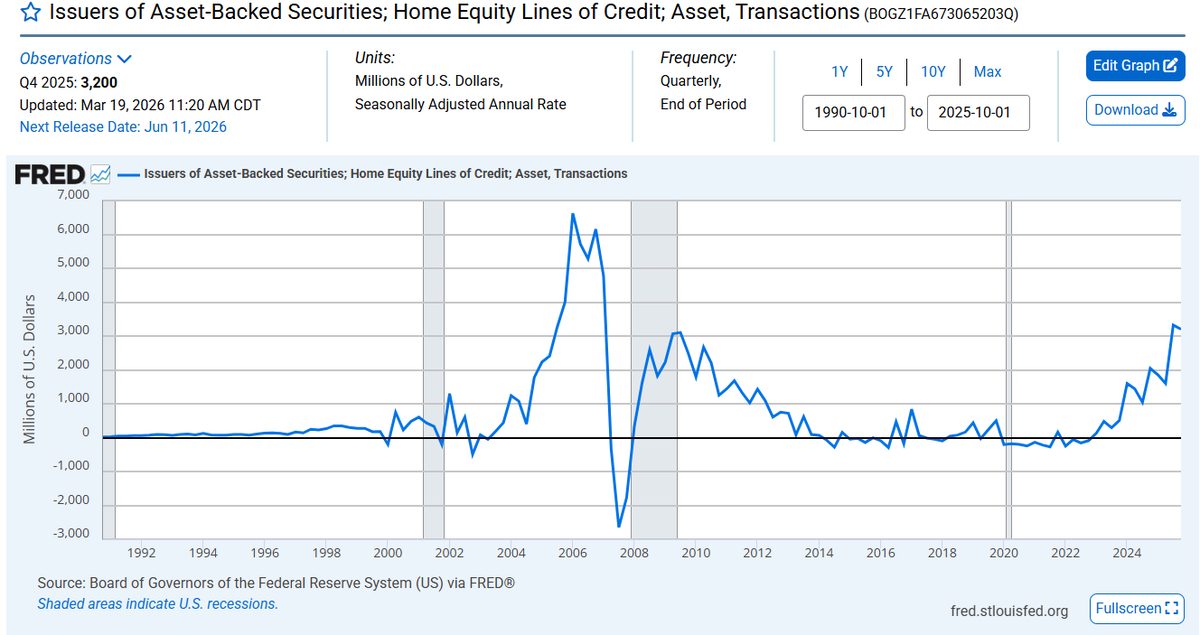

Today I’m watching one FRED series as part of the $FIGR thesis:

HELOC assets held by ABS issuers ( transactions)

Not Figure-specific, but relevant.

I already wrote about the holdings data showing growing demand for $FIGR securitizations, with large institutional names showing up and some exposure growing.

Now I want to see the broader supply-side picture:

Are HELOC assets actually moving back into ABS structures?

The chart clearly shows acceleration over the last few quarters, after years where the market was basically asleep.

Next print comes today.

Will update.

May 26

Reading Morningstar DBRS’ reports on $FIGR ’s securitizations is a must.

Not because I care so much about the exact terms of the notes.

But because these reports are packed with the kind of data I want to know as an investor.

So no worries, I did the job for you.

Starting with the technicals:

1. The pools are mostly junior-lien HELOCs ~ 88% of it.

2. Borrower quality looks pretty solid on paper, with the latest fund reporting a weighted average FICO of 747.

3. Utilization is already very high, around 98%

Now the interesting part is how Morningstar viewing $FIGR 's underwriting practices, and how it rates it.

The Pros:

Morningstar clearly sees advantages in Figure’s model.

The loans are fixed-rate, fully amortizing, no balloon, and with short draw periods-

Better than many traditional HELOCs.

But.. the Cons:

Since Figure uses proprietary income verification, FICO 9, AVMs/BPOs instead of full appraisals, and electronic lien search instead of title insurance,

Morningstar treats parts of it as less than traditional underwriting and applies valuation haircuts, reduces junior-lien recoveries, and steps up expected losses.

And yet, the senior notes still get AAA ratings, even after the rating agency applies the drawbacks, the structure still supports it.

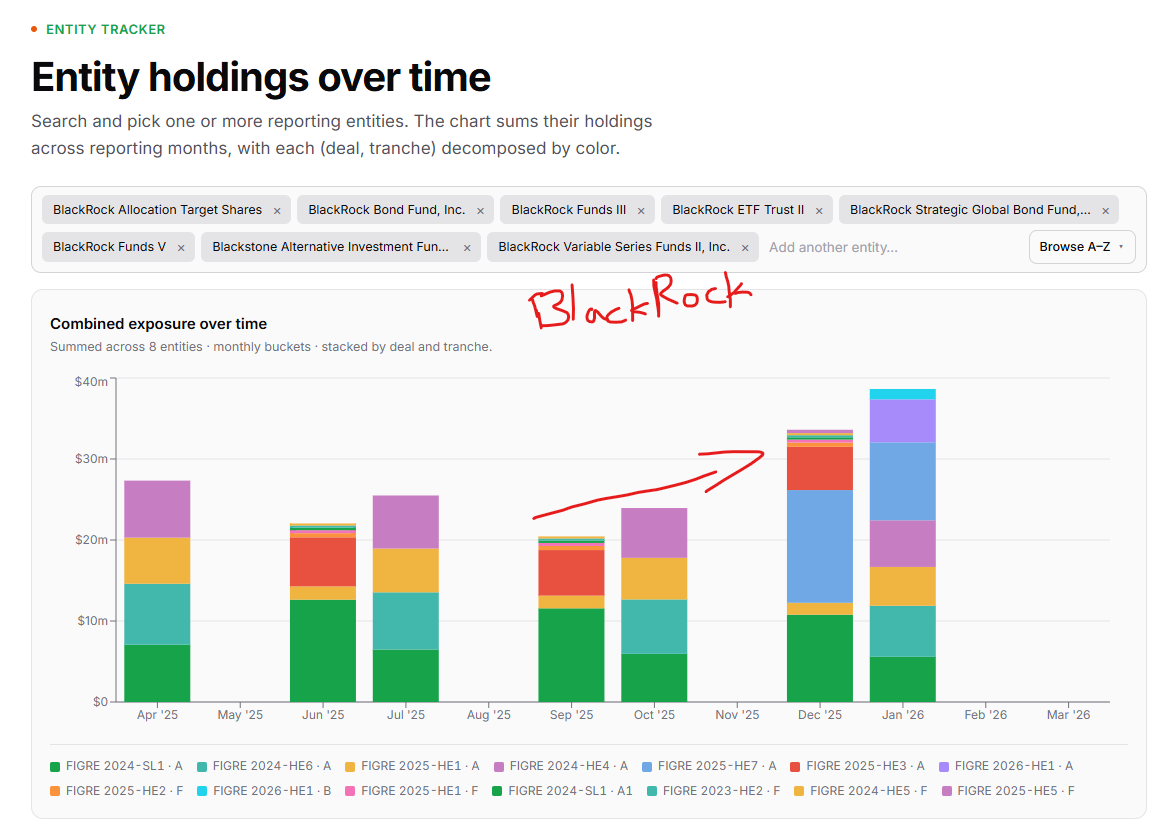

Looking at actual demand you can see large institutional names showing up in the holdings data.

Like BlackRock / J. P. Morgan exposure that's growing.

I think that's the most promising signal here.

If you want to drill down in $FIGR 's securitization (and origination) data check the visualization I've built ⏬

1

2

11

2,395

Exciting news: We entered into an agreement to acquire Kiavi, bringing the country's #1 Residential Transition Loan (also known as "fix and flip”) platform into the leading home equity marketplace.

The deal marks a deepening of our relationship with Sixth Street. We are purchasing Kiavi’s technology platform, and a new JV between Figure and Sixth Street will originate RTL loans off Kiavi’s balance sheet and sell them via our blockchain-native marketplace, Figure Connect.

This is big news for our network of 380 partners. We're also introducing Adaptor, our newest AI feature with agent-to-agent capability, built to eliminate months of administrative headaches as we onboard new partners. A big day at Figure!

Check out this story with Figure CEO @MBTannenbaum and Bloomberg's @pat_clark ↓

bloomberg.com/news/articles/…

9

11

71

6,598

The Prime Market is the largest in on-chain credit in DeFi. @serotonin_hq explains how @RockawayX ladders in ↓

2

7

34

3,443

CryptoYOLO retweeted

Jun 8

We're delighted to announce that AVLT/USDC is live on @Morpho Ethereum mainnet.

We've seeded the market with $4M in USDC. Available to borrow against AVLT & available to loop right now.

Bringing AVLT lending markets to Ethereum opens the door to a depth of liquidity, a class of depositor, and a level of composability the strategy was always built for.

First in get the best rates. The loop is open.

@alturax

We are happy to announce that our AVLT/USDC market is now live on Morpho ETH Mainnet.

@0xAlphaping will deploy $4M in USDC, fully available for borrowing and looping right now.

Borrow USDC against AVLT and loop for up to 80% APY on your AVLT.

Make your money go the distance 🦉

20

14

50

1,760

CryptoYOLO retweeted

Jun 8

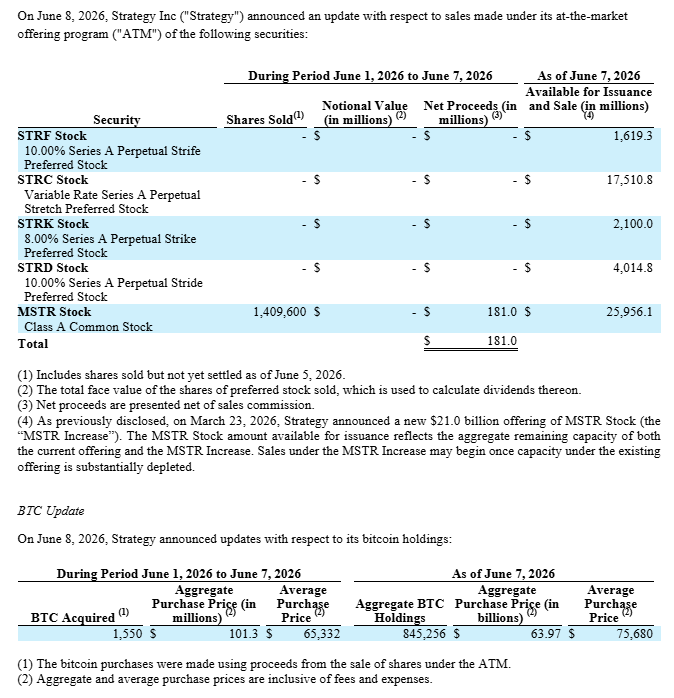

Strategy has acquired 1,550 BTC for $101 million to increase our $BTC Reserve to ₿845,256. We have also increased our USD Reserve by $100 million to $1.0 billion. $MSTR $STRC strategy.com/press/strategy-…

2,608

4,098

31,674

6,052,617

CryptoYOLO retweeted

Jun 8

$STRC and $MSTR shareholders have approved the amendment to move $STRC dividends from monthly to semi-monthly. Under the new cadence, the first record date is June 30 and the first payment date is July 15. Thank you to every shareholder who voted. strategy.com/press/strategy-…

656

1,105

11,442

689,917

CryptoYOLO retweeted

Let’s host it in Midland, TX. Give share holders a tour of all the facilities, then top it off with a Bonus dividend check payment for waiting patiently!Unlike our Board members monthly payments and bonuses.

1

1

202

CryptoYOLO retweeted

$FIGR reported $1.4B monthly consumer loan marketplace vol for May, 135% YoY. We are lowering costs and adding liquidity where it didn't historically exist.

So we beat on ... boats against the current :)

12

17

126

9,116

We’re democratizing capital markets. @financeguy74 tested Democratized Prime and dove into our partnership with Credibly.

Here’s what he found.

• Simplified and efficient lending and borrowing, compared to the process of getting a warehouse line.

• Pool availability for auto loans and HELOCs.

• Reduced friction should enable Credibly to pass savings onto its small business customers.

Read the full article from deBanked ↓

debanked.com/2026/05/soon-yo…

4

6

36

4,966

CryptoYOLO retweeted

May 28

2,000 vaults on @Morpho. 500 with real capital.

The infrastructure won. Now it's about who operates it with mandate clarity, collateral discipline, and risk legibility.

That's where the differentiation happens.

The future is bright.

May 27

"There are today around 2,000 vaults on @Morpho, and about 500 of them hold around $100K. Vaults enable a kind of modularity that's genuinely unprecedented in the history of both DeFi and finance"

- @PaulFrambot (@Morpho) 🎙️ "Future of "Finance w/ @BukovskiBuko3 (@TheBigWhale_) & Amy Oldenburg (@MorganStanley)

1

13

438

CryptoYOLO retweeted

May 26

Reading Morningstar DBRS’ reports on $FIGR ’s securitizations is a must.

Not because I care so much about the exact terms of the notes.

But because these reports are packed with the kind of data I want to know as an investor.

So no worries, I did the job for you.

Starting with the technicals:

1. The pools are mostly junior-lien HELOCs ~ 88% of it.

2. Borrower quality looks pretty solid on paper, with the latest fund reporting a weighted average FICO of 747.

3. Utilization is already very high, around 98%

Now the interesting part is how Morningstar viewing $FIGR 's underwriting practices, and how it rates it.

The Pros:

Morningstar clearly sees advantages in Figure’s model.

The loans are fixed-rate, fully amortizing, no balloon, and with short draw periods-

Better than many traditional HELOCs.

But.. the Cons:

Since Figure uses proprietary income verification, FICO 9, AVMs/BPOs instead of full appraisals, and electronic lien search instead of title insurance,

Morningstar treats parts of it as less than traditional underwriting and applies valuation haircuts, reduces junior-lien recoveries, and steps up expected losses.

And yet, the senior notes still get AAA ratings, even after the rating agency applies the drawbacks, the structure still supports it.

Looking at actual demand you can see large institutional names showing up in the holdings data.

Like BlackRock / J. P. Morgan exposure that's growing.

I think that's the most promising signal here.

If you want to drill down in $FIGR 's securitization (and origination) data check the visualization I've built ⏬

2

4

19

8,307

CryptoYOLO retweeted

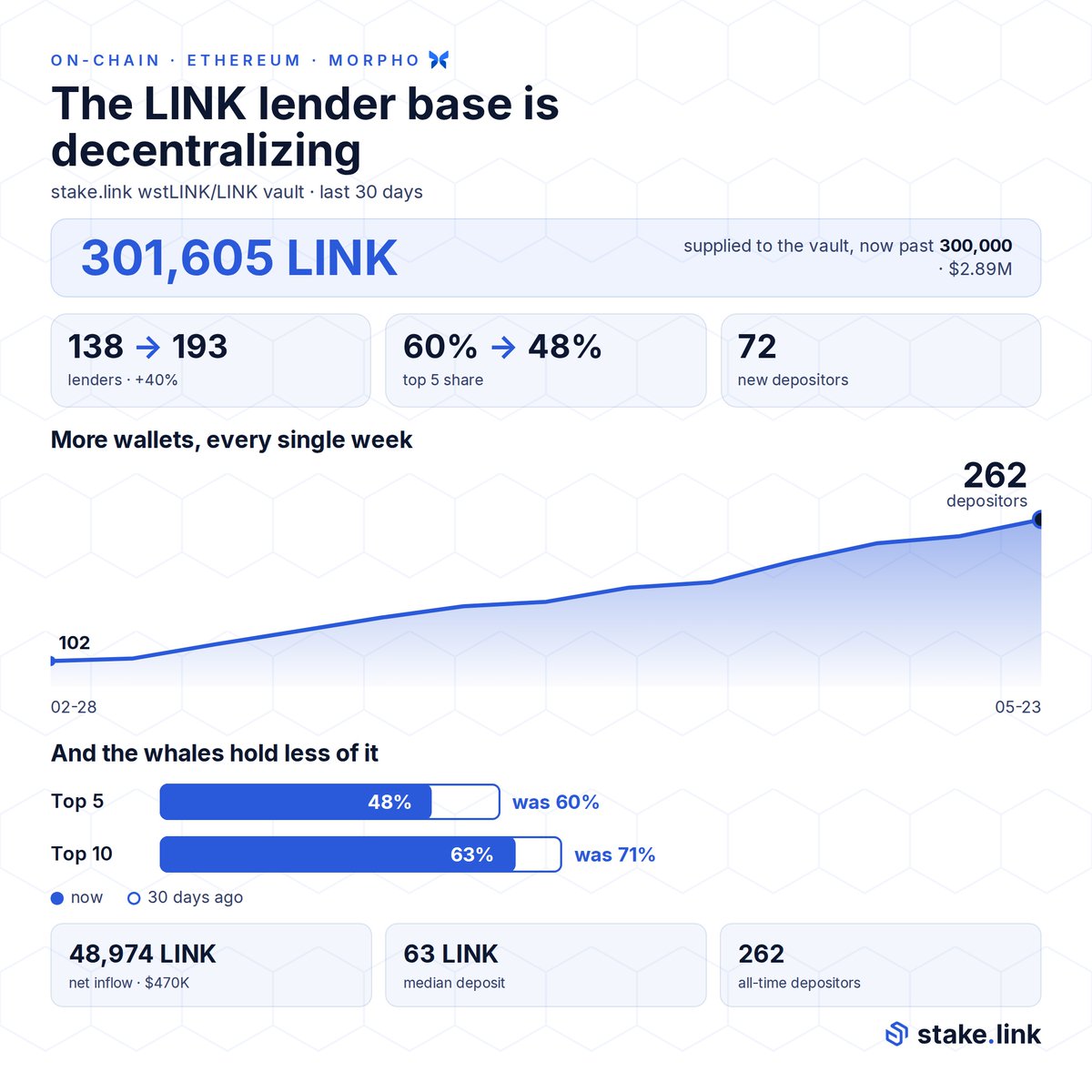

May 25

Alpha LINK Enhanced V2 crosses 300,000 LINK.

$2.9M in the vault. 193 lenders. Top 5 concentration down from 60% to 48%.

LINK lending against stLINK collateral. Yield from the Chainlink staking ecosystem.

Built with @stakedotlink.

@Morpho

May 25

We're excited to cross 300,000 LINK deposits in the @Morpho🦋lending pool

@stakedotlink <> DeFi <> @chainlink

35

1

9

540

May 24

This is the way. Native on chain issuance of real shares convertible 1:1 to NASDAQ!

May 24

You know what isn't delayed? @Figure trading on OPEN. 24x7 limit order book (market making 5x18 and working to expand). Access to DeFi. Works under the current SEC rules. This is the way.

3

357

CryptoYOLO retweeted

May 24

You know what isn't delayed? @Figure trading on OPEN. 24x7 limit order book (market making 5x18 and working to expand). Access to DeFi. Works under the current SEC rules. This is the way.

May 22

SEC delays plan to allow trading of tokenized stocks due to concerns and pushback

Scoop via @pattersonscott

10

9

93

15,961

In accordance with the rsETH technical recovery plan, WETH LTVs on Aave V3 Ethereum Core, Ethereum Prime, Arbitrum, Base, Mantle, and Linea have been restored to their pre-incident values.

WETH now operates as normal across all affected V3 deployments.

105

88

751

83,822