Some play Checkers, while others play Chess ♟️ 👑 This is why Ryan Cohen is the Best..!! Don’t give up. Don’t give in. Keep going and Never Stop. I am Dog.

Joined March 2021

- Tweets 32,441

- Following 121

- Followers 5,828

- Likes 148,487

10,826 Photos and videos

Pinned Tweet

May 6

Ryan Cohen is going to rock eBay's World. I wouldn't doubt for a second, that RC has been thinking about and planning this move since 2019.

The video below is from the Chewy IPO day on June 13, 2019. Ryan is describing how he did it with Chewy, and imo, how he is going to do it, with eBay. A seemingly simple method, yet nobody else in his Ryan's unique position as an activist investor, corporate operator, and capital allocator seems to be able to replicate Ryan's vision, including Ryan's work ethic.

Ryan Cohen has it figured out. Full Stop.

youtu.be/Z31hgjEyVIc

1

7

40

6,495

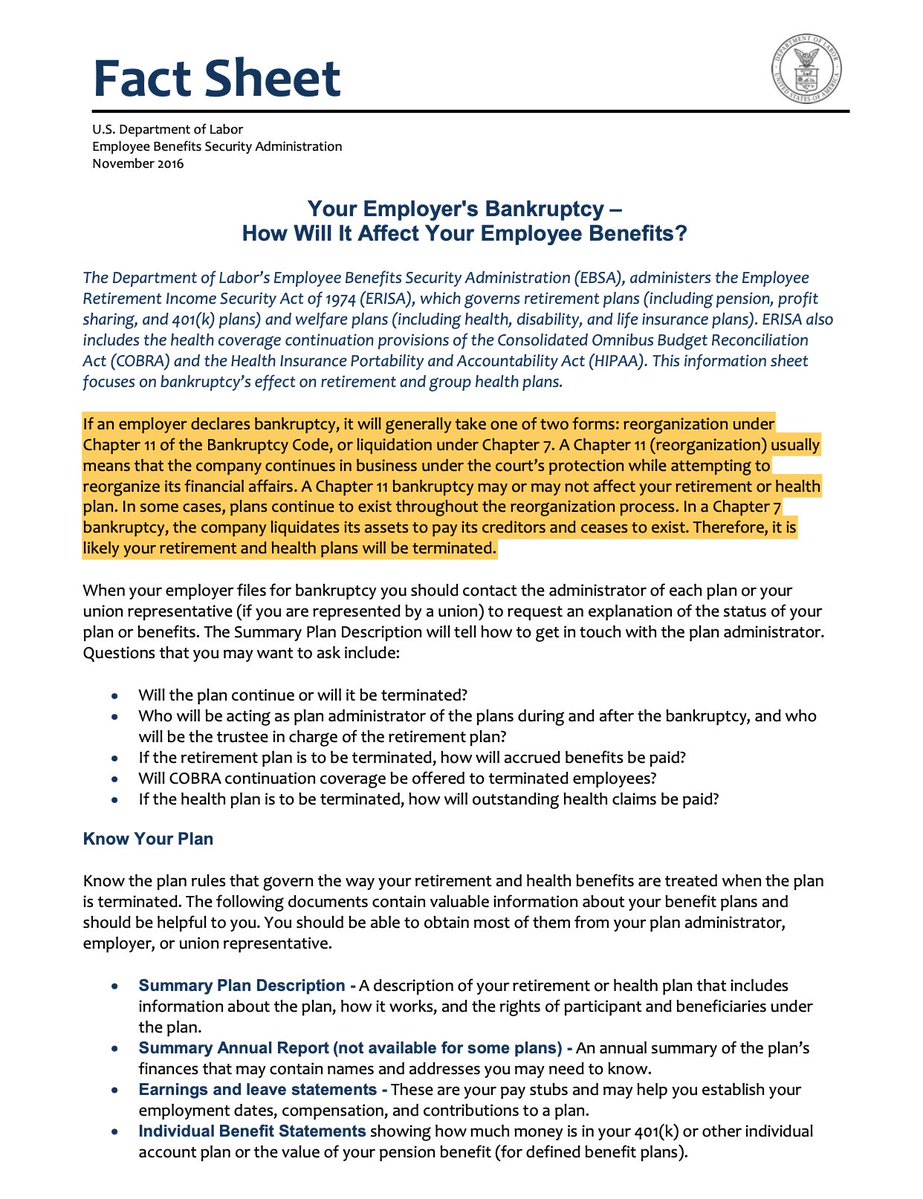

An attorney states "I am informed and believe" to allege a fact that they cannot prove with personal knowledge at that exact moment, but which they reasonably accept as true based on evidence, witness statements, or documents.

I am not an attorney, this is neither legal nor financial advice. I am a dog.

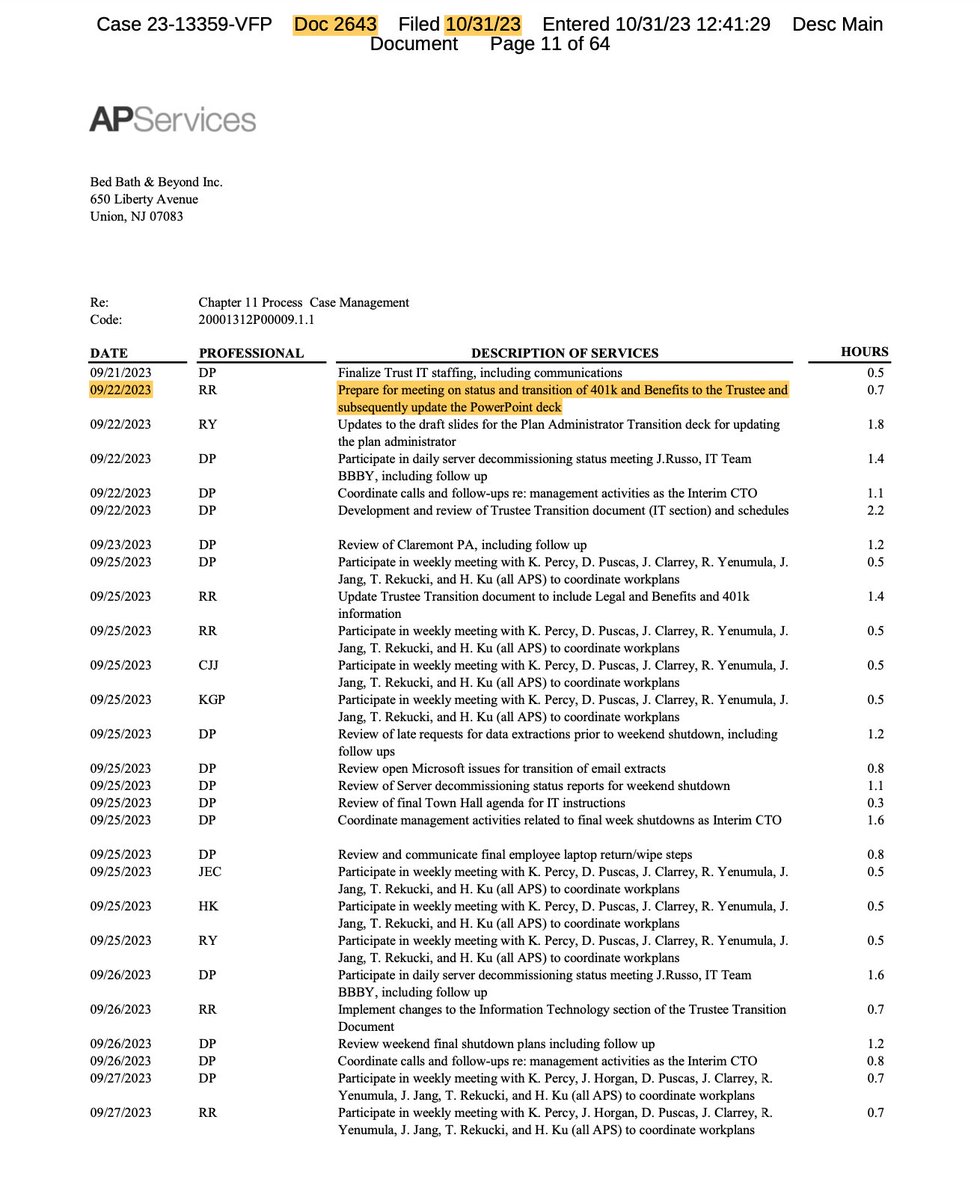

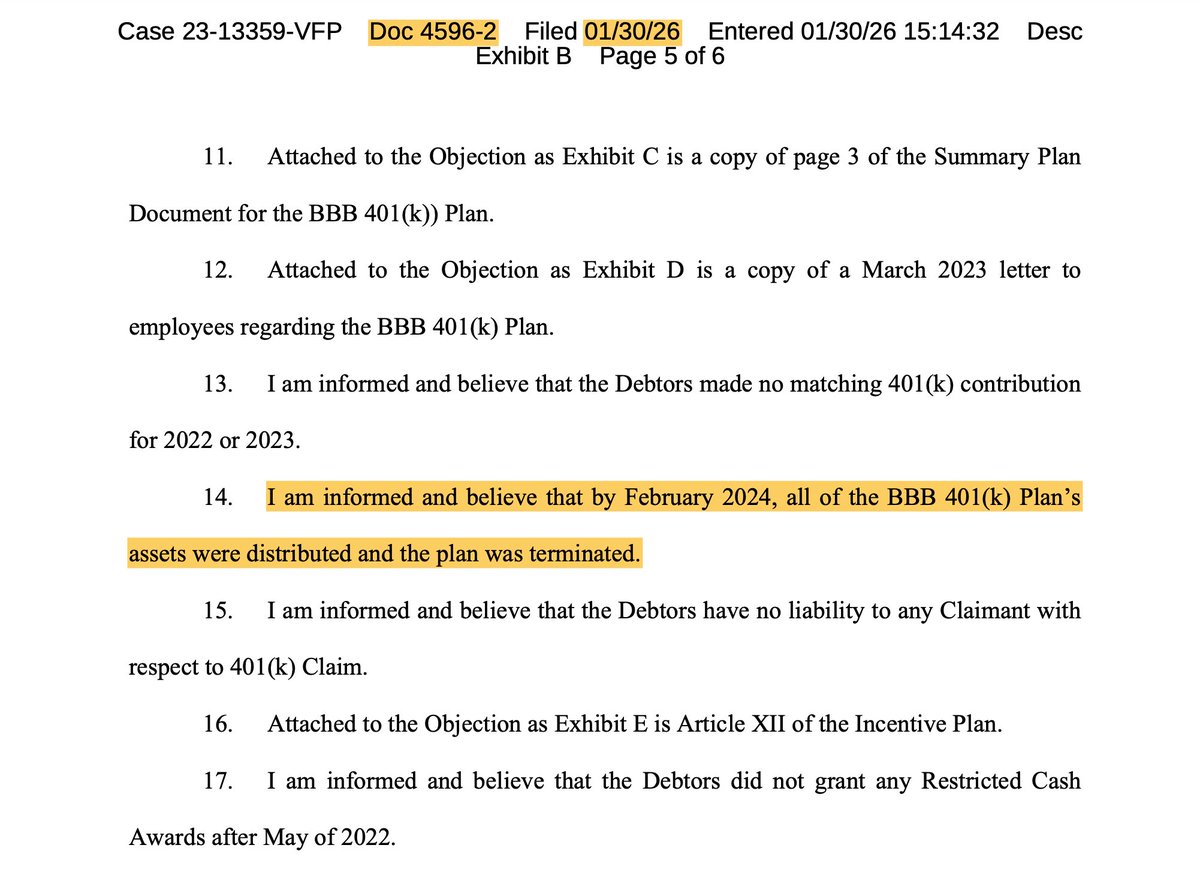

I am informed and believe, that the legacy DK-Butterfly 401(k) plan's assets and benefits were transitioned to the Trustee on 22SEPT2023 by Alix Partners.

In addition, I am informed and believe that one year later, in September 2024, the 401(k) plan's assets were distributed and the 401(k) plan was terminated by someone other than The PlanMan, as he was also informed and believed, which is what I believe, as I informed myself.

5

33

1,094

I am informed and believe, that the legacy DK-Butterfly 401(k) plan's assets and benefits were transitioned to the Trustee on 22SEPT2023 by Alix Partners.

In addition, I am informed and believe that one year later, in September 2024, the 401(k) plan's assets were distributed and the 401(k) plan was terminated by someone other than The PlanMan, as he was also informed and believed, which is what I believe, as I informed myself.

2

12

99

3,899

DirtΞvader retweeted

🚨 JUST IN — CONFIRMED: ELON MUSK is coming to the White House with President Trump tomorrow for the UFC Freedom 250 fight

LFG! Elon is showing up for Team America! 🇺🇸

DANA WHITE: "He'll be here! He'll be here tomorrow!" 🔥 @elonmusk @danawhite

154

1,428

12,032

286,454

Speaking of betting it all on Black... I didn't start this game to be able to say "Fuck You", and imo, neither should you. I passed that level a long time ago, and some of you have too. You just don't know it yet.

5

3

57

2,855

DirtΞvader retweeted

eBay's shareholder vote is this week, I expect Proposal 4 to pass and give Ryan Cohen a direct path onto the board 👇

5

25

280

10,772

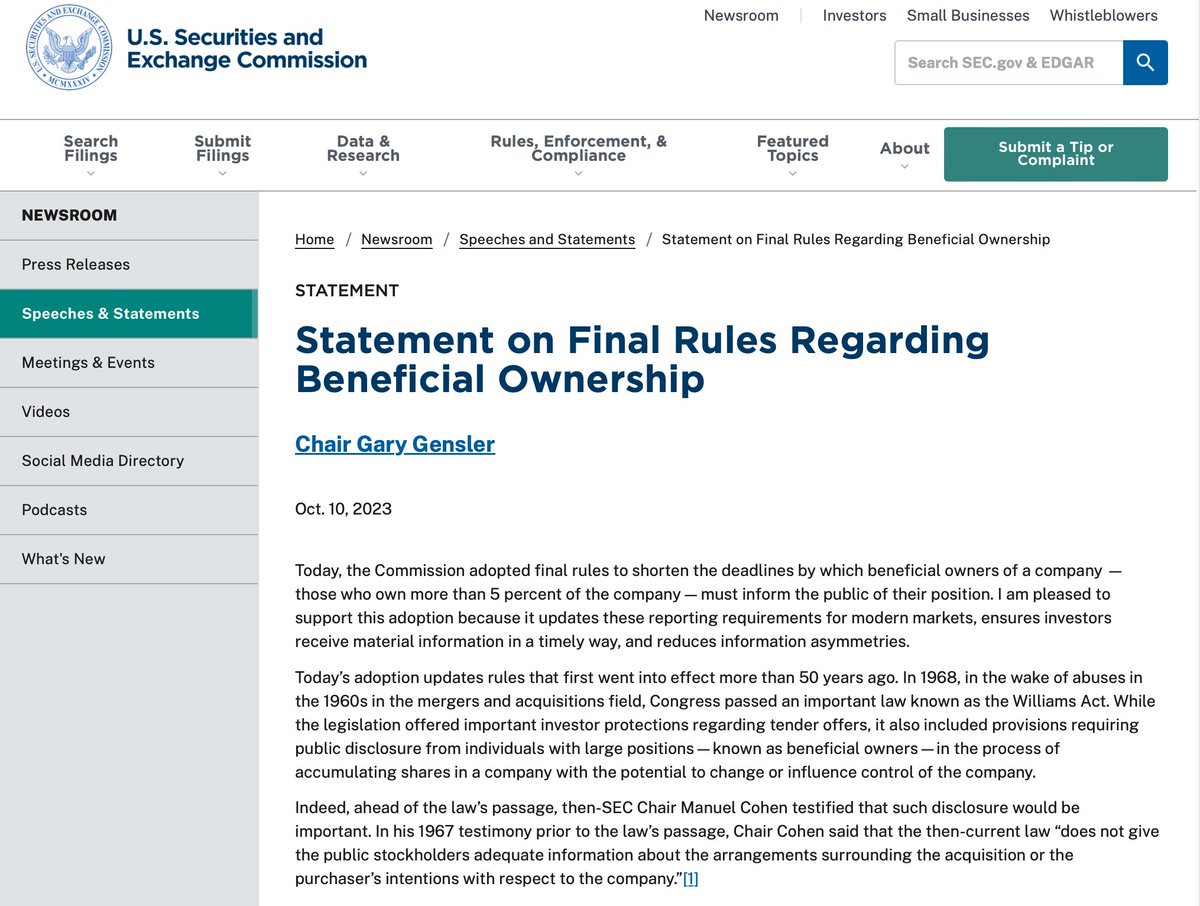

Fun fact: Gary Gensler has no hair. 👨🦲

10 October 2023

Perfect timing for the SEC to change the Ownership Disclosure Rules.

First:

When someone acquires shares in a company with the intent to control that company the new Rule after 10OCT2023 shortens the initial filing deadline for Schedule 13D from 10 calendar days to 5 business days.

Second:

The new rules for Amendments filed via Schedule 13D/A clarifies the filing deadline from "promptly" to 2 business days.

Key RC Dates:

20230930-DK-Butterfly, Inc. f/k/a Bed Bugs & Bath

======================

07MAR2022 13D filed by RC Ventures LLC

25MAR2022 13D/A filed by RC Ventures LLC

15AUG2022 FORM 3 filed by Ryan Cohen

16AUG2022 13D/A filed by RC Ventures LLC

18AUG2022 13D/A filed by RC Ventures LLC

With that knowledge, now you know, that the corrupt Bed Bugs & Bath Board, CFO, and CEO had a plan when they snuck in that Share BuyBack after the Cooperation Agreement with Ryan Cohen, signed on 24MAR2022.

And, you probably also realize that The PlanMan's third try at the Section 16(b) Case against Ryan Cohen, will fail just like the first two 16(b) cases that were dismissed. Being a betting Dog, I'll wager it all on Black, that this Dismissal will be with Prejudice.

So, with that knowledge, and the timing of more than a few Professional Billing Statements that were only up to, and including 21September2023. I wonder what happened during the 10 following days...?

Because, if there were a Change in Control that took place on the 21st of September, 2023 or any day thereafter, a private-for-profit entity would still need to file a Form indicating the Change-In-Control, but since Bed Bugs & Bath was no longer a public company after the Effective Date of September 29, 2023 and the shares were cancelled, the requirement to file anything regarding a Change In Control for public consumption after the date of 21SEP2023 ceased to exist.

iykyk

Ref: Cornell Law School Rule for Change in Control

34 CFR § 600.31 - Change in ownership resulting in a change in control for private nonprofit, private for-profit and public institutions.

law.cornell.edu/cfr/text/34/…

Ref: White & Case: SEC Adopts Rule Amendments to Modernize Beneficial Ownership Reporting

whitecase.com/insight-alert/…

Ref: U.S. Securities & Exchange Commission

sec.gov/newsroom/speeches-st…

4

6

44

1,945

DirtΞvader retweeted

WE ARE LIVE! 🔴

Ripping @GameStop @PowerPacks for the community! Come join us and have fun!

Pokemon, basketball, baseball, American football, REAL football and more!

x.com/i/broadcasts/1oKMvvrpM…

5

37

141

4,168

DirtΞvader retweeted

Jun 13

🔴 LIVE POKÉMON RIP NIGHT!

Saturday 13th June!

9pm UK / 4pm ET / 1pm PT

Win this PSA 10 Team Rocket's Houndoom worth $45! 🐺🔥

Winner drawn live on the stream.

Enter for FREE! 👇

roaringsensei.com/giveaway

@gamestop @powerpacks

38

57

111

7,674

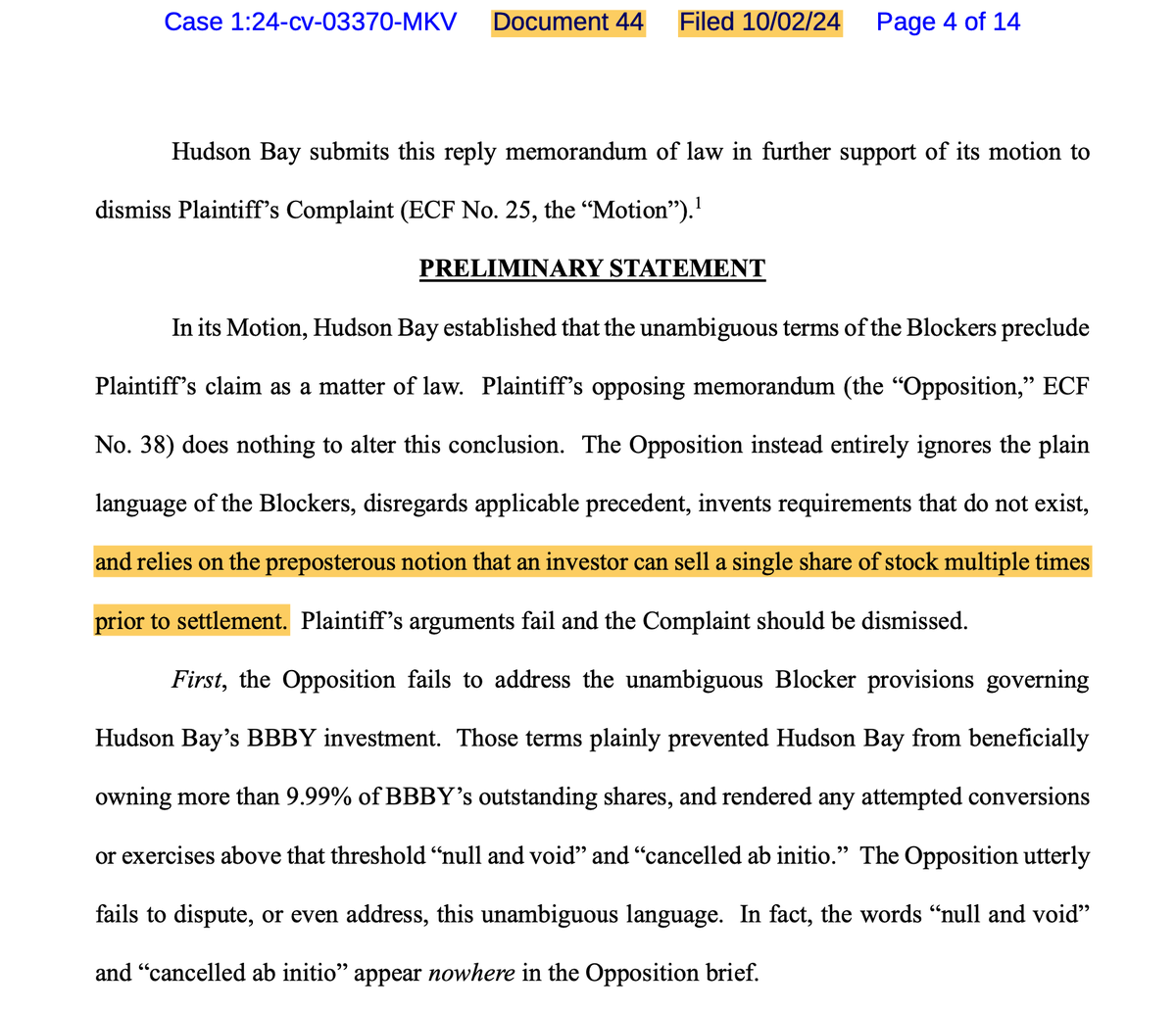

This Doc 44 in the earlier case of The PlanMan vs HBC case 24-03370, is the argument by HBC's attorneys in support of dismissal of the case and a perfect example of the phrase and the meaning of "You can't have your cake and eat it too". Because if you do eat your cake, you essentially eat yourself.

DTCC, SEC, FINRA, Market Makers, Hedge Funds, The blindly paid MSM, all of the characters that opine that the U.S. Capitol Markets are not corrupt, would be accusing themselves of what they really are.

And that will never happen, and is Preposterous...!!

Why, imo, does The PlanMan go through the exercise to sue..? It sets the stage for immediate dismissal for any wise crackers that will undoubtedly make attempts to bring court cases after this exit from Chapter 11 Bankruptcy is finally done, but still overdue.

That's what they get for 1920's settlement standards, like a kid courier hauling a bag of stock certificates down Wall Street at the end of the day, but 2 msec trade executions on the Exchanges, when the piles of stock trades in the dark pools, eventually see the light of day.

Bernie Madoff's Vision of How To Win Trades and Influence Compromised People with Money, Part II. The Citadel Edition. Soon to hit bookshelves soon.

..sometimes it is fun, after reading about CFC, FSHCO, HOLDCO, and Pari passu and stumbling across this post from last year. Says it right there in Doc 44 what the intention was for the Hudson Bay transactions that began in Feb of 2023. Even though a really regarded entity didn't have control, in the legal sense of the word, they actually did.

Just an observation: Somebody left the gate open at the funny farm last night, judging by the trending "bbbyq" and they were coming out and attacking @jake2b like flies on a rib roast. I'm still undecided how many are pretending to be morons, and how many really are Bona Fide Morons. 😂

2

14

73

3,610

..sometimes it is fun, after reading about CFC, FSHCO, HOLDCO, and Pari passu and stumbling across this post from last year. Says it right there in Doc 44 what the intention was for the Hudson Bay transactions that began in Feb of 2023. Even though a really regarded entity didn't have control, in the legal sense of the word, they actually did.

Just an observation: Somebody left the gate open at the funny farm last night, judging by the trending "bbbyq" and they were coming out and attacking @jake2b like flies on a rib roast. I'm still undecided how many are pretending to be morons, and how many really are Bona Fide Morons. 😂

22 Nov 2025

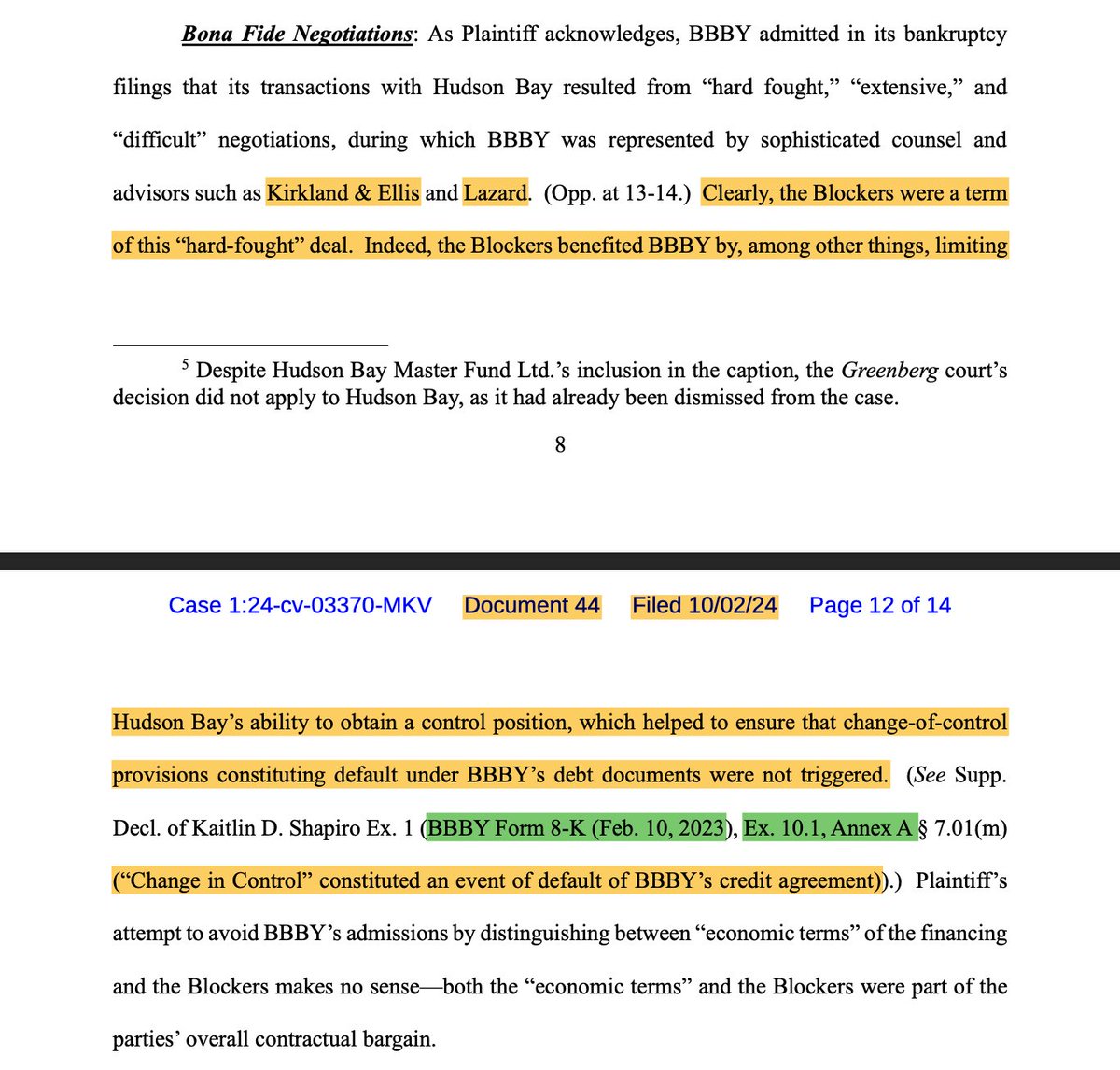

Just a thought... The Goldberg/Hunter vs. HBC Appeals case could be more important than just a run of the mill Appeal. And it is all because of the screen print below from Doc 44 filed in the dismissed (w/prejudice) Case 1:24-cv-03370-MKV that makes this statement:

=======

"...Clearly, the Blockers were a term of this “hard-fought” deal. Indeed, the Blockers benefited BBBY by, among other things, limiting Hudson Bay’s ability to obtain a control position, which helped to ensure that change-of-control provisions constituting default under BBBY’s debt documents were not triggered.

...."Change in Control” constituted an event of default of BBBY’s credit agreement)."

=======

Link to the dismissed HBC case: 24-03370

courtlistener.com/docket/684…

So it would appear that the outcome of the PlanMan Hunter Appeal is (imo) a BIG deal.

As Judge Mary Kay Vyskocil dismissed the Case (1:24-cv-03370-MKV) Doc 53 is the Judge's Opinion & Order Granting Motion to Dismiss. I don't see anything with regard to Change-of-Control in her Opinion filing, but it could reasonably acknowledge and support HBC's argument that a "Change-of-Control" did NOT take place.

Depending on the outcome of the Appeals case, filed as 20230930-DK-Butterfly-1, Inc. v. HBC Investments LLC, 25-2728, (2d Cir.), if the Appeal is denied, all is good. If the Appeal is granted, then HBC 50% ownership change by any 5% or larger equity holder, could potentially qualify for Change-of-Control, and at a minimum, the Change-of-Control could be back on the table.

Link to the Appeals case: 25-2728

courtlistener.com/docket/718…

Great article by Gibbons Law below, or search up "Howe" on my timeline. Chris Howe is the attorney from Alvarez & Marsal, who was involved with this case, but he is also an industry expert on ownership change scenarios. I posted some excerpts of his videos over the last few years.

Directly below is a link from Gibbons Law, discussing how a company evaluates, and determine if a Change-of-Control has taken place.

Link to that article.

gibbonslaw.com/resources/pub…

Everyone should by now have a pretty good feel of the implications if HBC's ownership of BBBY shares "did" qualify as a Change-of-Control. It could negatively affect the usage of the acquired Tax Attributes per the requirements of a 382(l)(5) (aka The HomeRun) election.

Feb 2023 to March 2023, was the time period that HBC was buying, exercising, and selling shares.

Both Kirkland & Ellis and Lazard, I am sure, fully vetted and determined from the First NOL Order, and subsequent filings, referencing Change-of-Control multiple upon multiple times after the Bed Bath, buybuy Baby, and Harmon brands were sold, knew that a change of control did not take place.

After a while, I'll see if I can locate the specifics around that 3-Year LookBack period test for changes in ownership. Such as, is it three years to the day the test was performed, three years to the month, quarter, or even calendar year..? ...because I don't know.

But I do know this, as Chris Howe explained on one of his videos that I posted, the election to select either the 382(l)(5) and 382(l)(6) exemption, is made at the point of filing a timely filed Tax Return, which could be April 15th, or as late as October 15th if it qualifies for late filing.

Either way.. Game-On..!!

1

6

46

5,806

DirtΞvader retweeted

May 3

Cry harder about a once in a lifetime investment...😭

GameStop eBay's valuation when it gets the Cohen treatment will be a mean lean money making machine.

Dilution argument is mute. It is valuation of the business. I don't give two flips if there are 2 million shares outstanding, when the business hits $100B it doesn't matter. Amazon has 10.76 Billion shares outstanding. It does not matter, so think of another BS comment.

Oh wait.. Unless you are one of the many who will be paying for it. Two sides to every trade and all short sellers will become buyers.

Every single person, who shoots down the unfathomable potential of this move, does not have a new short position, imo. Because you would be insane to take a short position on a Company like GameStop with $9B in cash, three years of profitability, and a Board and CEO who are aligned with shareholders.

Ryan Cohen has only been perfecting his craft of running successful businesses since he was 15. Ryan Cohen is the only person on this planet that has taken on Amazon, and beat them at their own game with Chewy. Now GameStop, and soon eBay.

The only person in history... E V E R.

Ryan Cohen didn't become a billionaire to disappear on a super yacht for the rest of his life. He is a man with moral fortitude and business ethics instilled by his late father, Ted Cohen. And he is not afraid to call out the BS engrained in society by those billionaires that have disappeared on their SuperYachts, whose only tie to their original businesses is promoting media propaganda to allow them to stay wealthy.

So how long have you been short..? And if I am wrong, and you are just an agitator. Get on board, or sit back and watch.

3

28

1,073

DirtΞvader retweeted

May 6

Ryan Cohen is going to rock eBay's World. I wouldn't doubt for a second, that RC has been thinking about and planning this move since 2019.

The video below is from the Chewy IPO day on June 13, 2019. Ryan is describing how he did it with Chewy, and imo, how he is going to do it, with eBay. A seemingly simple method, yet nobody else in his Ryan's unique position as an activist investor, corporate operator, and capital allocator seems to be able to replicate Ryan's vision, including Ryan's work ethic.

Ryan Cohen has it figured out. Full Stop.

youtu.be/Z31hgjEyVIc

1

7

40

6,495

links to easily navigate my profile:

Hudson Bay Capital—

• x.com/sboho/status/177134918…

• x.com/sboho/status/178609705…

• x.com/sboho/status/178606814…

• x.com/sboho/status/178605439…

• x.com/sboho/status/182351132…

• x.com/sboho/status/178897379…

• x.com/sboho/status/178645164…

• x.com/sboho/status/178609705…

• x.com/sboho/status/178606814…

• x.com/sboho/status/176809523…

• x.com/sboho/status/170925593…

Net Operating Losses (NOL)—

• x.com/sboho/status/176762882…

• x.com/sboho/status/175455285…

• x.com/sboho/status/173771355…

• x.com/sboho/status/172010820…

• x.com/sboho/status/172964844…

• x.com/sboho/status/172308047…

•reddit.com/r/BBBY/comments/1…

•reddit.com/r/BBBY/comments/1…

•reddit.com/r/BBBY/comments/1…

Lazard—

• x.com/sboho/status/179258137…

• x.com/sboho/status/179257384…

• x.com/sboho/status/179256614…

•reddit.com/r/BBBY/comments/1…

Ryan Cohen's 16(b)—

• x.com/sboho/status/176360317…

• x.com/sboho/status/174734172…

• x.com/sboho/status/174695470…

• x.com/sboho/status/174734172…

Ryan Cohen's Class Action—

• x.com/sboho/status/179204360…

• x.com/sboho/status/179202509…

• x.com/sboho/status/179086875…

• x.com/sboho/status/177634567…

• x.com/sboho/status/175856843…

Form 25, Form 15 and Going Dark—

• x.com/sboho/status/173211914…

• x.com/sboho/status/171178861…

• x.com/sboho/status/171176841…

• x.com/sboho/status/171176841…

• x.com/sboho/status/171139900…

•reddit.com/r/BBBY/comments/1…

$GME New Class and Blockchain Shares—

• x.com/sboho/status/184912888…

• x.com/sboho/status/184185955…

• x.com/sboho/status/183623118…

• x.com/sboho/status/179163422…

• x.com/sboho/status/179155259…

• x.com/sboho/status/179163422…

#GME Investment Policy—

• x.com/sboho/status/178541881…

• x.com/sboho/status/182444849…

• x.com/sboho/status/182444849…

• x.com/sboho/status/178541881…

• x.com/sboho/status/173252015…

$BBBY #BBBY $BBBYQ #BBBYQ

re: Hudson Bay and the great conversation that it has started.

Let's look back at the work Kirkland did, going to August 2023:

Specifically the language. It's important that they denote a potential Section 16 reporting claim.

Further down, we have a reporting issue.

I believe that these could be the result of the combination of RC and HBC's holdings. From the cooperation/standstill, RC was allowed to increase his position to 19.99%.

From the share buybacks, he was pushed from 9.8% to 11.8%.

Now, if you look at HBC at 9.99% limit and RC at his purchase which concluded at 9.8% limit, you are under 19.99% with 19.97%.

However, if you take RC's pushed 11.8%, you arrive at 21.79% ownership and are in violation of the standstill.

Could this have been the move to establish "harm" and justify a future suit? Or to assist in a suit brought forward by Mr. Goldberg? I don't know.

—

Then we also have the fun topic of the new HBC 16(b). So let me pose a question..

What if the Section 16(b) is not the result of HBC going over 9.99% (they can't), but because the window of time from RC's sell on August 18 to HBC's entry on February 8 is less than 6 months?

That is a violation, if they are related.

This only applies if RC and HBC are related—if RC is an attribution party (affiliate) through the HBC deal, this is a violation of 16(b). Their combined ownership is greater than 10% and the time between the sale and the buy is less than 6 months.

I wonder if that is why it is under seal?

I also wonder, is that why JP Morgan was in such a rush on the weekend of February 4-5 to declare the Company insolvent and push it into Chapter 7, well before the grace period to repay the bond note had expired?

fun times. 🥷

$BBBY #BBBY $BBBYQ #BBBYQ

63

142

614

361,931

DirtΞvader retweeted

May 14

eBay: “neither credible or attractive”

Ryan Cohen: “You are literally obese”

4

8

142

4,768

Jun 12

Creating more inventory for RC’s money making machine.

Grade 8

Grade 9

Grade 10

Going from 1 grading hub in the U.S, to 3. Exciting times ahead.

13 Sep 2025

Good thing @PSA is getting ready too... It has always been about scale. Who is the Grand Master at scaling a business category while growing smiles and grins & delighting customers..? You know who.😉

"Faster estimated turnaround times are anticipated as PSA announces plans to add two U.S.-based grading facilities by 2026. All ticket grading services are designated for a new outpost in Plano, Texas, while to the southeast, an expansive operation is underway in Boca Raton, Florida. Both locations intend to increase PSA’s grading capacity as demand continues to rise for trading cards, tickets, and other collectibles."

The Plan has been in motion, long before most would ever believe. No question about that. The 🐶 is happy to just be along for the ride. 😊

psacard.com/articles/article…

1

23

2,426

Jun 12

Prediction: Hotter than hot

Texas and Florida will have grading operations too. Or so I read.

Jun 12

The biggest difference between now and 2021?

When PSA reopened back then, the hobby had cooled off.

If the hobby is still this hot when value submissions return, the next wave of orders could be enormous.

5

1,760

DirtΞvader retweeted

a story in four pictures🦋

29

61

496

17,737

Jun 12

🚀 Two RocketMen and Little X 🚀

1

51

2,498

DirtΞvader retweeted

Jun 12

LOL… This is amazing 🇺🇸

JUST IN: SpaceX is now worth more than Canada

Community note

SpaceX's market cap is about $2 trillion. Canada's GDP is about $2.5 trillion per year. The post compares the company's valuation to the country's annual economic output.

finance.yahoo.com/quote/SPAX.PVT/ worldometers.info/gdp/canada-gdp/

1,629

2,759

28,453

1,296,716