Expanding Bitcoin Markets at @Bitflow (co-founder); OMSCS ‘20 🐝;

Joined September 2019

- Tweets 2,984

- Following 2,990

- Followers 13,677

- Likes 28,909

236 Photos and videos

dylan.btc retweeted

Jun 8

The biggest greenfield in crypto for the last few years hasn't changed.

BTC DeFi.

A crazy amount of liquidity just sitting there waiting for the right application.

Bitflow and Ordinal Hive are two companies I am pretty bullish on.

4

1

8

513

dylan.btc retweeted

Jun 8

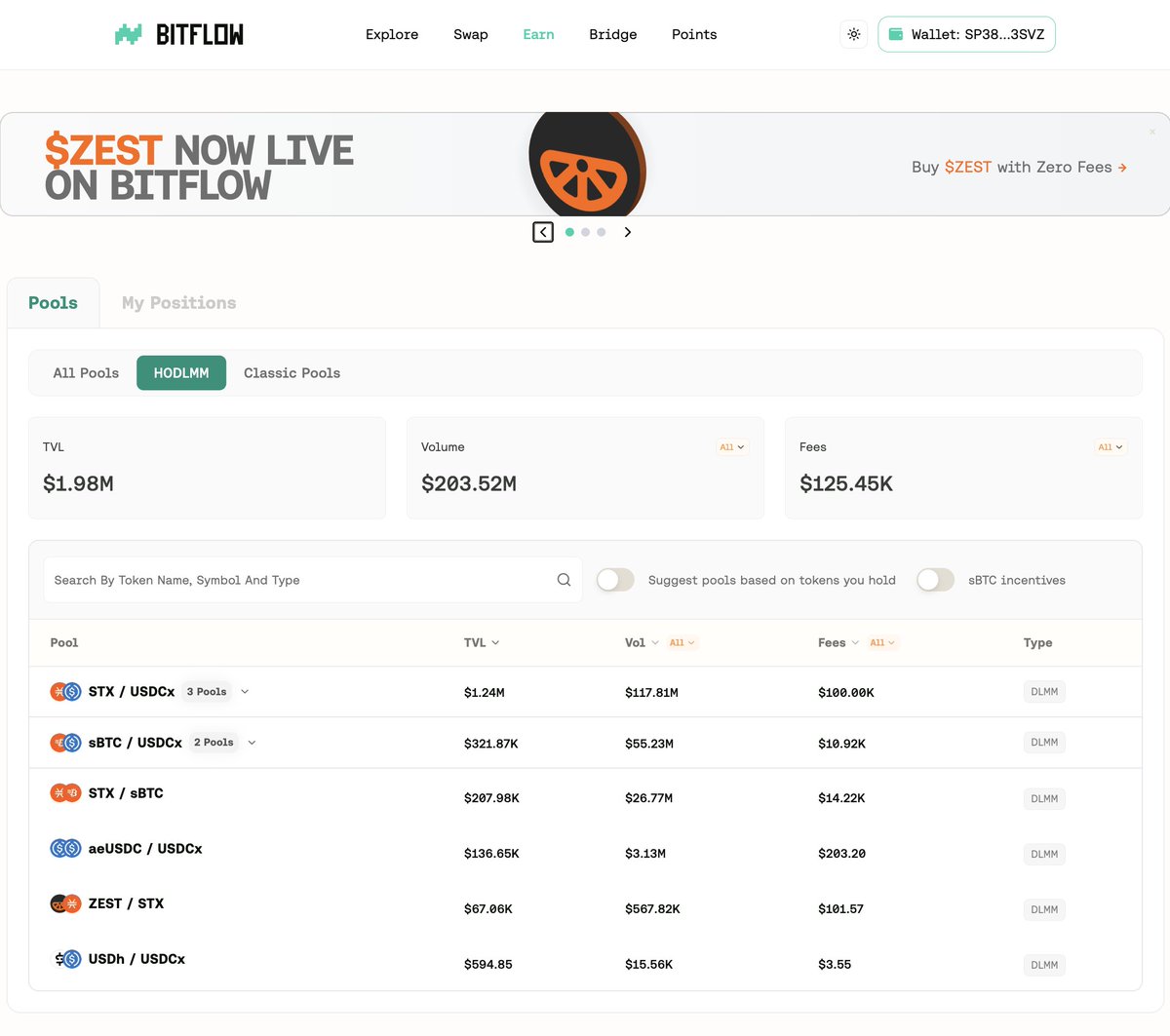

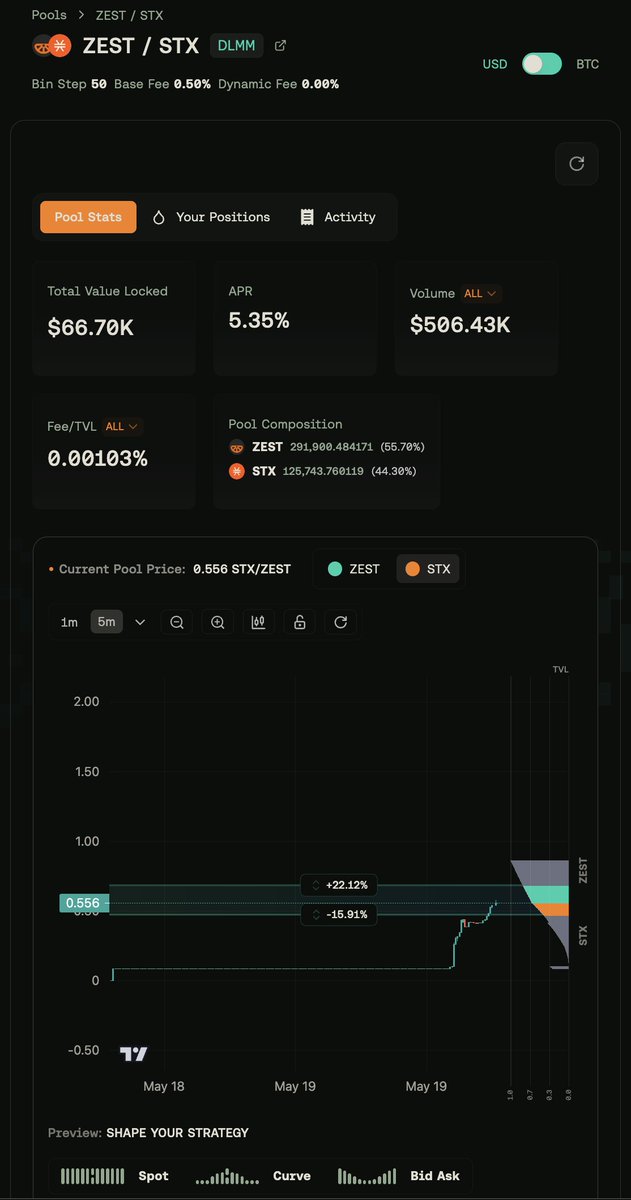

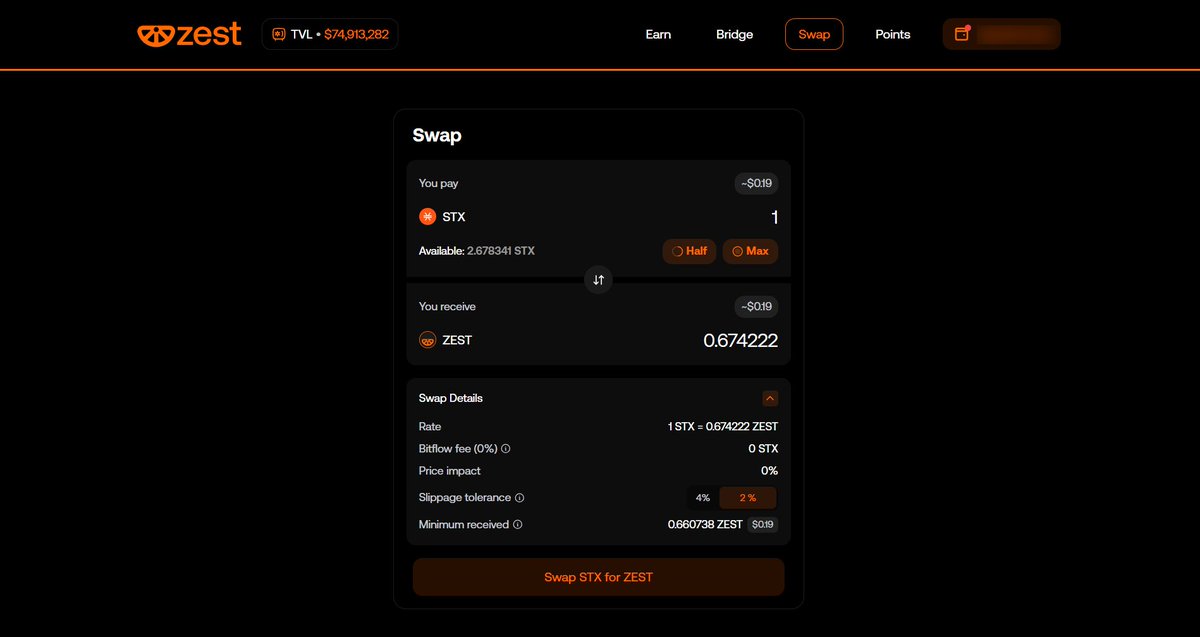

$ZEST swap feature is now live on @ZestProtocol app UI with ZEST/ STX pair available

The swap feature on the Zest UI uses Bitflow's audited HODLMM contracts. So there is no worry to be made.

❌No new contracts, no forks, no extra fees added.

✅ Same pool, same router, same on-chain safety guarantees, just frontend on Zest UI.

Swap $ZEST here 👇

4

6

34

1,567

dylan.btc retweeted

Jun 5

Buying Bitcoin today is front running the forced diversification of a completely AI saturated equity market.

With not one, not two, but three massive inclusion of 5 Trillion dollars of equity value into the index, diversification requires venturing out on the risk curve.

91

147

2,026

229,910

dylan.btc retweeted

Jun 5

Looks like a good entry point, like before mainnet and before Nakamoto and the respective growth (NFA).

3

1

28

1,282

dylan.btc retweeted

Jun 5

Thoughts on Stacks (blockstack:native) and markets:

- The four year cycle stays true. Bitcoin highs are muted but lows also likely muted.

- The AI models discovering bugs issue is real. Flight to safety will be a trend to watch.

- Bitcoin stayed simple with verifiable and transparent supply. All additional functionality can be built on top.

- Stacks optimized for safety and went for a decidable language (Clarity). Safety will end up being *the* thing to optimize for.

- There is likely going to be one maybe two Bitcoin L2s that take all/most of the traffic.

- After Bitcoin gets a quantum upgrade, depending on new signatures, Bitcoin bandwidth will likely decrease by 50%-97%; highlighting increased need for L2s.

- Bitcoin staking is a $100B market with increased demand for BTC on BTC yield coming from institutions and DATs.

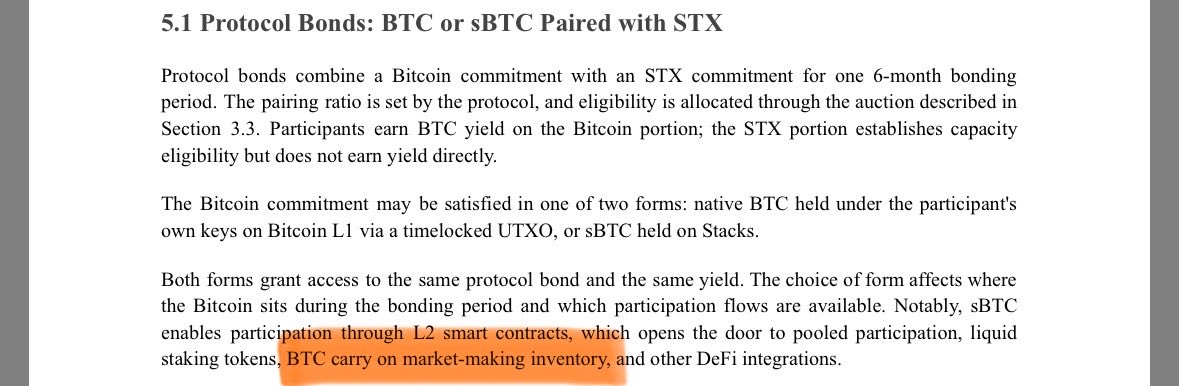

- Stacks has seen two cycles before (1) mainnet launch (BTC smart contracts), (2) Nakamoto launch (speed & sBTC), now we’re working on (3) Bitcoin Protocol Bonds launch that unlocks the largest market yet.

- Last year, the ecosystem restructured for operational efficiency plus a new treasury. Stacks Labs is well funded, laser-focused, and hyped up about the new launch.

- Stacks is Lindy in crypto & Bitcoin at this point. Largest Bitcoin project by marketcap & active devs for 5 years. When BTC starts to recover, so will STX but as higher beta.

- Bitcoin might reach $150K-$250K next cycle (halving is early 2028) which is a 3-4x, Stacks is more in the 20-50x range given higher beta history and upcoming catalyst of Bitcoin Protocol Bonds. (Not financial advice and more on protocol bonds later).

- In the chart below, there were only three times in history for lowest entry points. Before mainnet when everything was unproven, before Nakamoto, and now.

- The upcoming SIP for protocol bonds launch will likely get accepted, with good feedback from community to drop/adjust the boosted rewards period (I support adjusting/removing this variable.)

We’re buying here and then patiently waiting next 6-months for protocol bonds to go live, markets to bottom out, and our thesis of Bitcoin as the king asset with a thriving on-chain BTC economy to play out. Let’s go! 🟧

68

84

313

38,572

dylan.btc retweeted

Jun 1

Saylor / Strategy selling a few raspberries isn’t causing bitcoin to crash. The reality is that there is a massive parabolic spike in AI-related equities that is vacuuming up all excess liquidity, multiples of bitcoin’s market cap. On top of that, labor market is healthy and energy prices are up, so sentiment for dovish rate cuts is nowhere to be found. Bitcoin’s fundamentals have never been better even if the macro environment isn’t doing it any favors.

98

129

1,629

68,737

dylan.btc retweeted

May 29

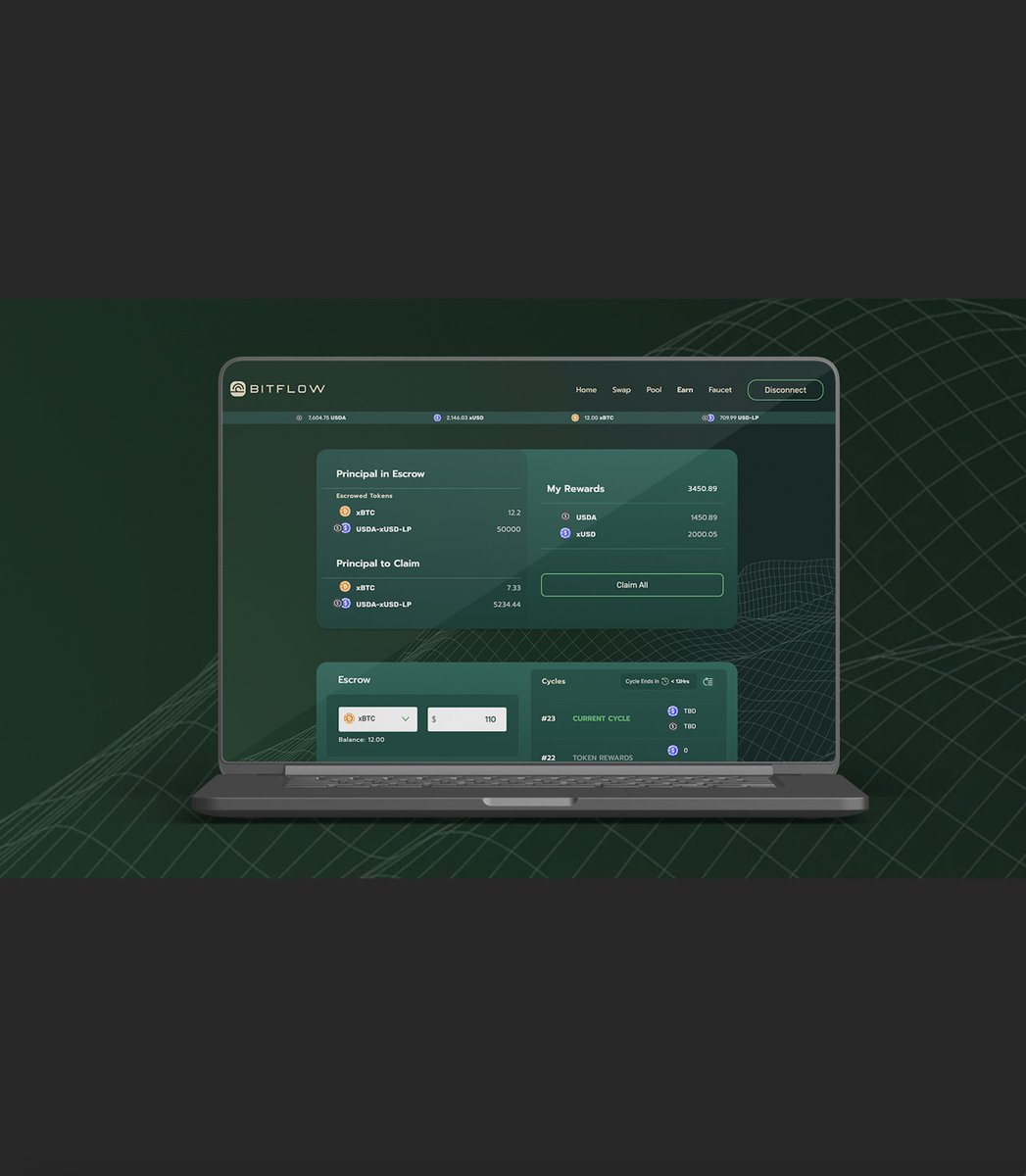

The Bitflow crew is top-tier.

Team just shipped a 🔥 dashboard to see all your agents actions and position in one view.

Best part? Everything is open-source and you'll be able to run the front-end on your own machine soon.

1/ Your AI Bitcoin agent runs 24/7. Now you can actually see what it's doing:

The BFF Army Agent Dashboard is live, for operators and agents on @bitflow x @aibtcdev

Read-only. Public APIs. No wallet connection required

🤖 bff.army/agent-dashboard

3

11

650

dylan.btc retweeted

May 28

BIG news.

@UTXOmgmt, the Bitcoin native asset management arm of Nakamoto Inc., is the inaugural participant in Bitcoin Staking on Stacks.

This means institutional BTC earning BTC yield, without ever leaving the base layer.

52

57

264

57,667

dylan.btc retweeted

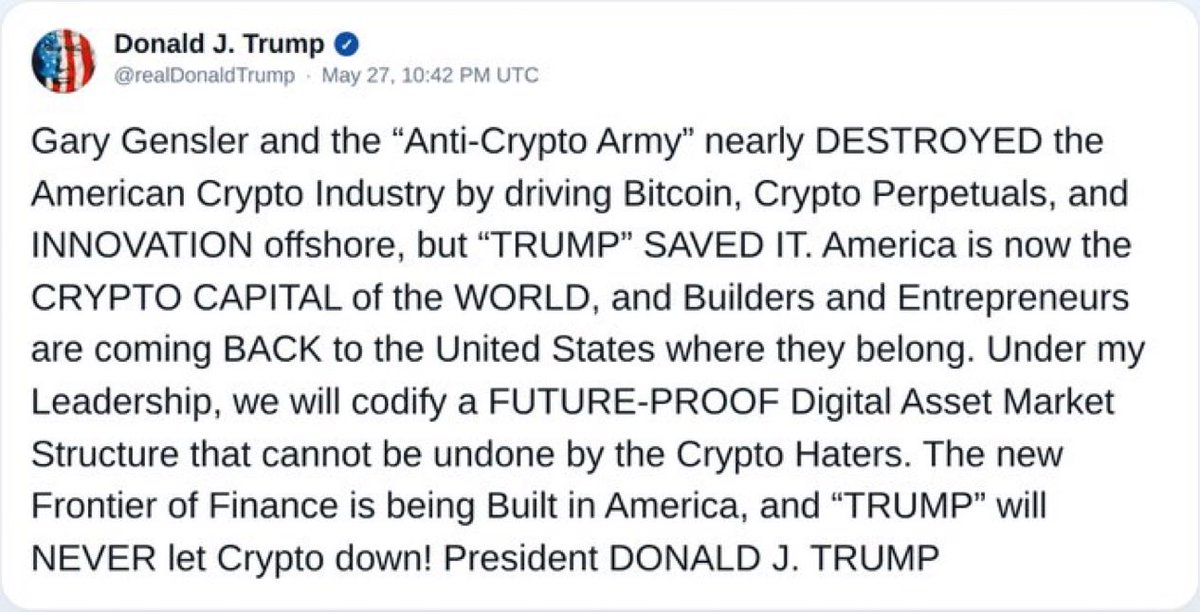

May 28

So Trump is explicitly mentioning reshoring “Crypto Perpetuals” and we get a red day huh

17

7

198

12,778

dylan.btc retweeted

May 25

we are firmly in the era of all assets and all markets becoming meme-ified

agentic investing is going to accelerate the volatility as assets trade on attention and narrative positioning

and obliterate traditional wealth management

my body (and portfolio) is ready 🤠

21

7

80

6,768

dylan.btc retweeted

May 25

Crypto is a legit and indeed inevitable technology. Usually such things are net positive.

113

336

2,849

326,716

7

13

57

6,228

I don’t think anyone serious is arguing that RFQs replace orderbooks entirely. And nobody is crowning RFQs over orderbooks.

**Notice how Lucas drew a distinction in his response in the video below rather than call one model superior to the other.

CLOBs and RFQs optimise for different things and solve different market structure problems.

Orderbooks are excellent for native price discovery. Nobody disputes that. Hyperliquid and Lighter are fantastic examples of this.

But the bigger bottleneck for scaling global on-chain markets is not price discovery. It’s liquidity sourcing.

You cannot realistically bootstrap deep crypto-native orderbooks for every commodity, FX pair, index, equity basket, or global market. Fragmentation eventually becomes a problem.

That’s where RFQ architecture becomes powerful.

RFQs are designed to connect DeFi to existing liquidity rather than rebuilding every market from scratch. And ironically, many of the largest TradFi markets today, FX, bonds, OTC derivatives, and institutional block trading, are heavily RFQ-driven.

A smart RFQ system aggregating multiple liquidity sources can absolutely provide better effective execution in many situations.

And yes, “last look” concerns are valid, but that’s mostly in poorly designed RFQ systems.

Interestingly, even Lighter just announced “Lighter RFQ” specifically to handle large RWA positions with lower slippage and better pricing.

That alone should tell you that even strong CLOB systems eventually recognise that RFQ infrastructure becomes extremely useful once you start dealing with RWAs, larger size, fragmented liquidity, and TradFi-style execution.

So RFQs are not some “inferior fake market structure.”They solve a different problem.

The future is probably not RFQ vs CLOB.

It’s hybrid systems combining:

• price discovery

• smart routing

• aggregated liquidity

• institutional access

• efficient execution

We need to stop with this nonsense of crowning RFQs over Orderbooks.

I’ve written about this before but once more wanted to share

Orderbooks like Lighter are venue for Price Discovery; where the price is set. The price is based on supply and demand.

RFQ models like Variational is a venue for Price Taking. It literally copies the price from elsewhere; physically cannot offer better pricing than the venue it hedges on without taking directional risk.

Simple math: RFQ Price = Source Price Hedging Fees Profit.

Actually, Variational isn't even a competitor to Hyperliquid/ Lighter; it is a customer of them when you check deep.

There is also the Last Look problem:

- In orderbook: If you see a price and click buy, you get filled. The engine is neutral, in Lighter's case it's proved by ZK that you get the fill you intended.

- In RFQ: You request a price. The MM (or OLP) looks at your request, looks at the market, and then decides if they want to take the trade. If you are profitable, the RFQ engine can simply start rejecting your quotes, can delay them or giving you worse pricing.

So please stop crowning RFQs. Most they can become an aggregator of actual trading venues.

2

5

60

6,317

“We’ll see whether Ethereum maintains its lead with a foundation that isn’t willing to fight for it.”

No chance

May 21

I think Ethereum’s original sin was not considering tokenomics with every move it made from Dencun on.

The ultrasound money thesis was a good one and with Dencun (or the L2 roadmap generally) they should have stopped to say that this was going to hurt the ultrasound money thesis and consider how to preserve it.

Most people, like David, don’t want to believe in something that isn’t also putting up points on the scoreboard.

When the main offering becomes ideology/communism and money/tokenomics/capitalism are overlooked, the peasants are going to revolt — as they’ve been doing for two years now.

Look at the public reaction to Tomasz: broad praise, a sense of hope, excitement, the price pumping … only for him to be gone a year later with the new ED being someone who cannot even be found online except for a Wayback Machine url with his name that has some really questionable statements on it (and I should say the EF denied that this website, which was taken down a few weeks after he was appointed to the board, is his). They’re going to be really mad at me for even mentioning that but in the place of a void, these are the kinds of things people will glom onto.

Then there was the manifesto — I mean, mandate, which they backtracked on forcing people to sign. (Btw, this is the second bit of news that seems to relate to Bastian. And now the third would be all these departures. There’s nothing else for us to point at and say about him — when I searched for his name on Google News just now only 14 links came up. He seems to be some kind of invisible hand behind the scenes.)

I don’t think ideology and capitalism/tokenomics/number go up are mutually exclusive. I think you can have CROPS values and also consider how each step of the roadmap affects the tokenomics and even have teams for BD/ecosystem growth.

It feels like the EF doesn’t realize the moment that crypto is in. The competition is only just starting. We are in the phase of real world adoption. The Ethereum Foundation’s CROPS principles are great ones, and they are worth fighting for. But the EF seems to want to sit back on its laurels and act above it all when all its competitors are all getting down and dirty on the field to gain market share.

Maybe it is the right approach. I don’t know. I’m just saying that more competitive people won’t align with it. And so they will leave … and community members will as well.

I personally don’t think it’s good for Ethereum if its most competitive people depart. Ethereum’s unwillingness to stop the brain drain will only benefit its competitors — or spawn new ones. Giving a shit about price and tokenomics and BD doesn’t hurt CROPS. It just helps ensure that these principles get spread to more people and that other chains that don’t have these principles don’t get a leg up.

All the commentary may be pointless. It seems Vitalik tried what everyone wanted and it didn’t align with his vision, so he brought in a new person he felt more comfortable with. It makes me sad to see people become so disaffected with Ethereum, but maybe this is V’s Brian Armstrong/no politics at Coinbase moment where he lays down what the EF will work on and asks everyone else to leave. That was the right move for Coinbase, but I view them as fundamentally different issues. We’ll see whether Ethereum maintains its lead with a foundation that isn’t willing to fight for it.

1

1

5

576