Roaming x and looking for interesting investment opportunities

Joined February 2017

- Tweets 27,320

- Following 3,690

- Followers 4,562

- Likes 55,492

1,318 Photos and videos

Star-lord retweeted

Tether did extensive research on ethereum:0x6985884c4392d348587b19cb9eaaf157f13271cd and decided to buy a bag

Arkinvest bought a bag

Citadel securities bought a bag

These teams have some of the best research teams on the planet

That’s the signal

something most people might not know:

ethereum:0x6985884c4392d348587b19cb9eaaf157f13271cd is the only token for Zero, LayerZero (labs and protocol) and Stargate.

• Gas

• Staking

• Every fee from every zone

• LayerZero fee switch

• Stargate buybacks.

All of it routes to one asset.

Most L1s(e.g sui:native ) launch a fresh token to capture their own activity.

Zero refused.

One asset captures it all.

3

3

33

1,903

Star-lord retweeted

something most people might not know:

ethereum:0x6985884c4392d348587b19cb9eaaf157f13271cd is the only token for Zero, LayerZero (labs and protocol) and Stargate.

• Gas

• Staking

• Every fee from every zone

• LayerZero fee switch

• Stargate buybacks.

All of it routes to one asset.

Most L1s(e.g sui:native ) launch a fresh token to capture their own activity.

Zero refused.

One asset captures it all.

6

6

48

4,373

Star-lord retweeted

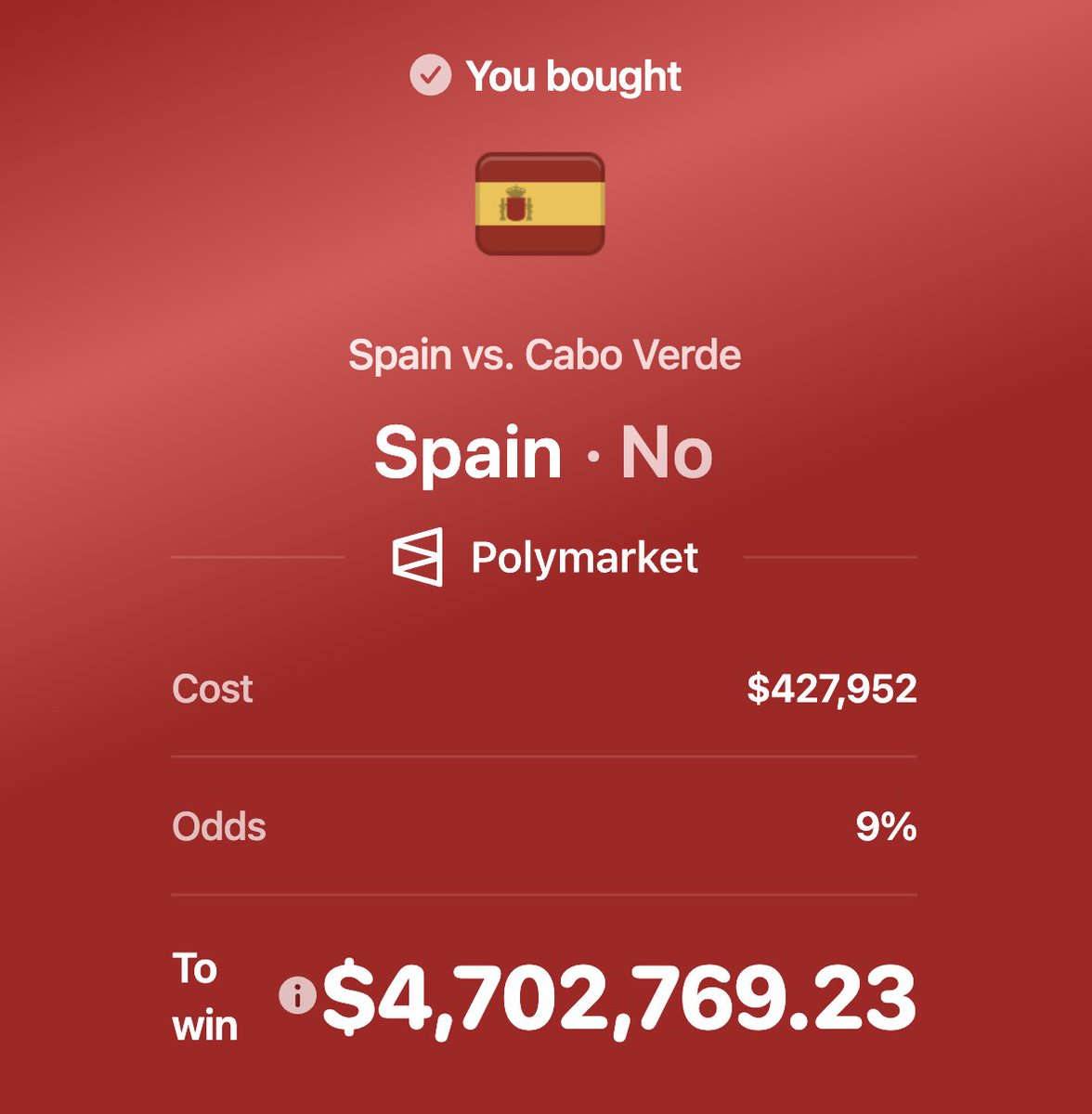

🚨BREAKING: Someone named “fishalive” put $400k on Spain NOT to win vs Cabo Verde at 9% odds...

This trade just cashed out $4,702,769.23 on Polymarket

849

2,532

47,831

4,971,415

Star-lord retweeted

Jun 15

SpaceX fear has passed

Iran war is over

Time to send everything

Let's print

51

21

727

94,109

Star-lord retweeted

Jun 15

20

18

177

67,711

Star-lord retweeted

No positions in $WOLF right now, but I’m cheering it on anyway since it’s a core part of American supply chains.

Still think financials are a bit toxic, but maybe with more market support subsidies it will go brrr

8

1

99

21,351

Star-lord retweeted

Jun 15

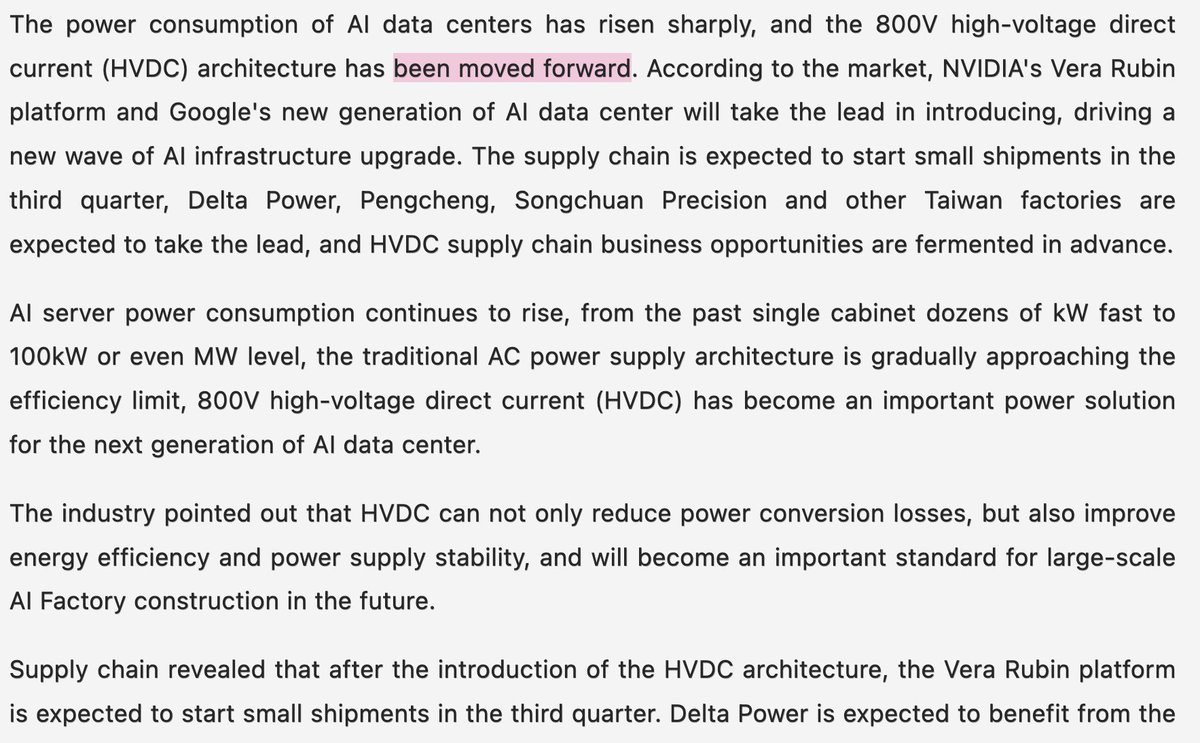

$NVDA and $GOOGL lead 800V DC ahead of schedule.

"Ahead of schedule", pulled up to Q3 2026 with small volume shipments starting .

- Delta Electronics (2308), $VRT

- Song Chuan Precision (7788)

- Schneider Electric, Eaton, Siemens.

All flagged as beneficiaries.

"Market sources indicate that Nvidia’s Vera Rubin platform and Google’s next-generation AI data centers will be the first to adopt the technology"

Source: Commercial Times

The power semi trade should be happy to hear this.

Jun 10

Morgan Stanley: $NVDA has denied the reports 800V DC has been pushed back.

Recent SemiAnalysis reports run contrary to our own checks at Computex.

Bro this has gotta be the dumbest CPO/800V selloff I’ve seen.

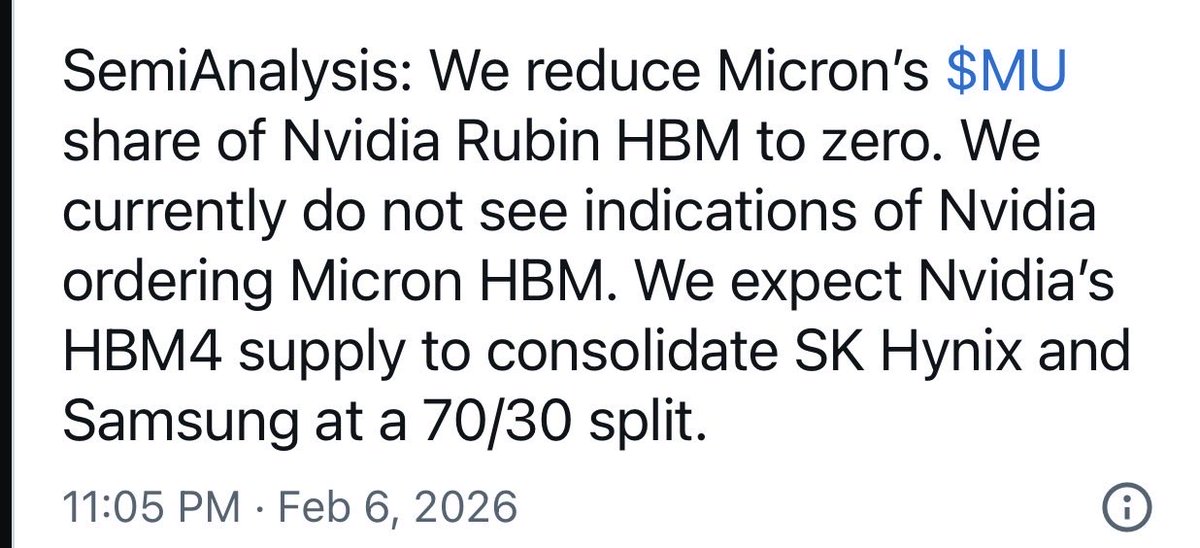

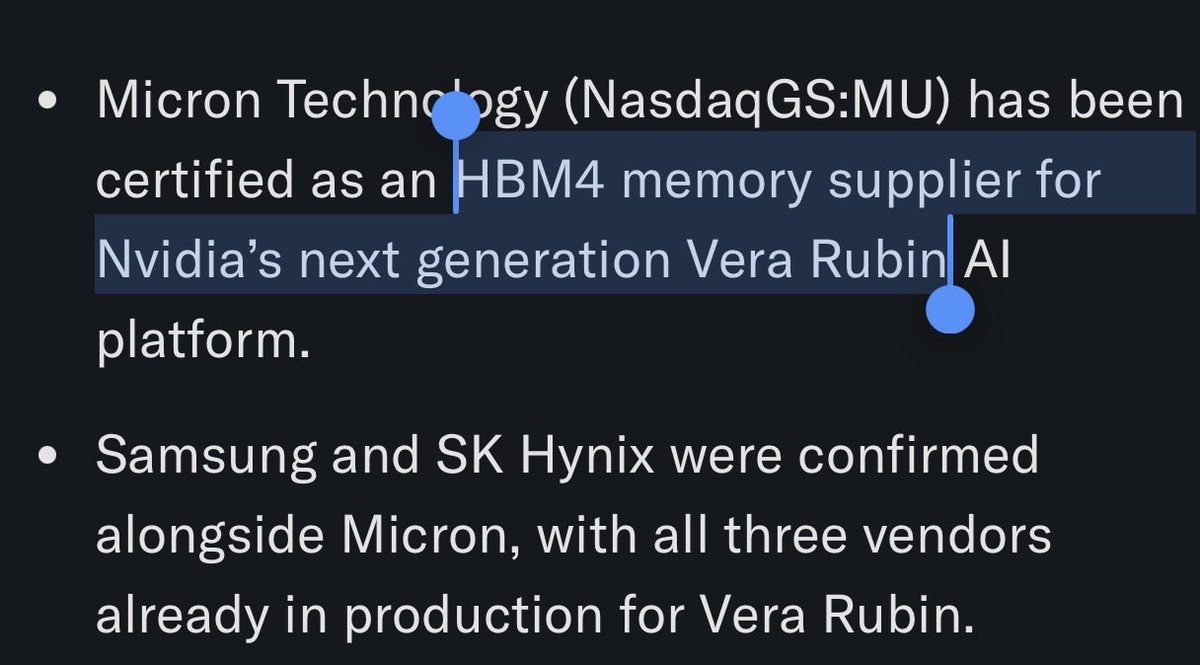

Since the selloff from their claim $MU had 0 share of Nvidia HBM4

213

211

1,333

802,998

Star-lord retweeted

Jun 15

$NVDA Vera Rubin & $GOOGL next-gen AI data centers are pulling 800V DC adoption ahead of schedule with shipments expected in Q3 2026.

The shift to 800V becomes a forced upgrade as AI racks move toward megawatt-scale power increasing power-semiconductor content in every rack.

49

78

869

122,258

22h

$wolf is going to rip

Taiwanese Media: Vera Rubin to Adopt 800V HVDC, With Small-Volume Shipments Starting in Q3

ctee.com.tw/news/20260615700…

3

816

Star-lord retweeted

Jun 15

power semi time to rip

Taiwanese Media: Vera Rubin to Adopt 800V HVDC, With Small-Volume Shipments Starting in Q3

ctee.com.tw/news/20260615700…

17

7

329

77,002

Star-lord retweeted

Jun 14

BREAKING: 🇺🇸🇮🇷 President Trump says peace deal with Iran is officially complete and the Strait of Hormuz is now open.

1,231

2,430

21,646

4,908,249

Jun 14

Jun 14

$CARDS 10x off the bottom for those who've been paying attention, has doubled in the past month will all relevant metrics still up & to the right

good for solana to see another app having breakout success

3

430

Jun 14

I feel like i own too little $NBIS

Jun 14

$NVDA CEO Jensen Huang praised $NBIS at its Inflection event saying it rebuilt its platform for the AI era & scaled “from one data center to gigawatt scale AI factories in just two years.

Nebius is positioning itself for the next AI cloud shift by moving from tokenmaxxing to valuemaxxing with infrastructure built where demand actually lives.

337

MOST PEOPLE HAVE NO IDEA HOW GOOD OF AN INVESTOR GOOGLE IS

6% OF SPACEX

14% OF ANTHROPIC

75% OF WAYMO

$900M INTO SPACEX IN 2015 →

NOW WORTH $115B

$13B INTO ANTHROPIC → NOW WORTH $140B

WAYMO JUST RAISED $16B AT A $126B VALUATION → GOOGLE’S STAKE WORTH ~$95B.

THOSE THREE BETS ALONE ARE WORTH OVER $350B AND THEY HAVE 100’S MORE SMALLER ONES $GOOGL

JUST IN: Google’s $900 million investment in SpaceX has reportedly grown to $100 billion

605

1,730

13,873

2,313,154

Star-lord retweeted

Jun 13

HORRIFIC FOOTAGE: A 21-year-old woman was pushed off a 40-meter bridge in Limeira, Brazil by bungee jump workers who failed to attach her safety rope. She died from the fall.

1,427

1,487

11,130

9,425,747

Star-lord retweeted

Jun 11

that everyone is writing off @LayerZero_Core team's upcoming ZERO blockchain as 'muh we don't need another L1 bro..' but it is actually different and $ZRO will violently re-price upwards.

1

9

550

Star-lord retweeted

Jun 13

Holy fuck I am so fucking hard right now $AAOI

Jun 13

Some napkin math on $AAOI:

> Management explicitly told you that their mid-2027 target is $471M transceiver revenue - that's $5.65B annualized just from their 100G/400G, 800G and 1.6T lines.

> The biggest risk is management doesn't achieve this (it is ultimately a huge ramp, but one they've raised capital for). But if they do, that puts AAOI at roughly 2.4–2.9x P/S at today's market cap. That is stupid cheap compared to larger optical peers: Lumentum trades around 15x FY2027 sales and Coherent around 8x FY2027 sales.

> CPO laser also sits on top as a free option (GS already predicts this will reach ~$100B in 2028).

> $AAOI (pluggables) will be a big beneficiary if CPO is delayed as Semi Analysis argues in their CPO report.

I think $AAOI, while not without risk, presents great risk to reward. NFA - I am long.

Full analysis below, including my take on the "risk" that management is unable to succeed in ramping production.

3

1

39

9,990

Jun 13

I’m long $zro. Launching new chain soon that could actually be competitor to solana. Also tokenomics improved greatly.

Jun 3

ZRO Updates

More ZRO has been bought back and locked up than sold into the market. Institutions and buybacks have taken 19.77% of supply in 18 months, while 63.8% of ZRO unlocked to investors still hasn't moved. $112.7M has gone into ZRO buybacks since September 2025, one of the largest programs in crypto.

ZRO is the only asset in the LayerZero ecosystem. All economic value from Zero, LayerZero, and Stargate flows back to it.

Every token expresses a view. ZRO's first was that there'd be many chains, no single winner, and value would accrue to whatever connected them. Now LayerZero has moved $267B across 165 chains.

The next view is bigger. Money and markets are the two largest waves finance will ever see, and both are already onchain. Zero was built for this moment. Coming this fall.

5

1,116

Star-lord retweeted

Jun 13

quickly learning that @beezie is one of the better tcg gachas out, legitimately think its en route to #2

and you can also farm points for potential airdrop

14

6

79

23,115

Star-lord retweeted

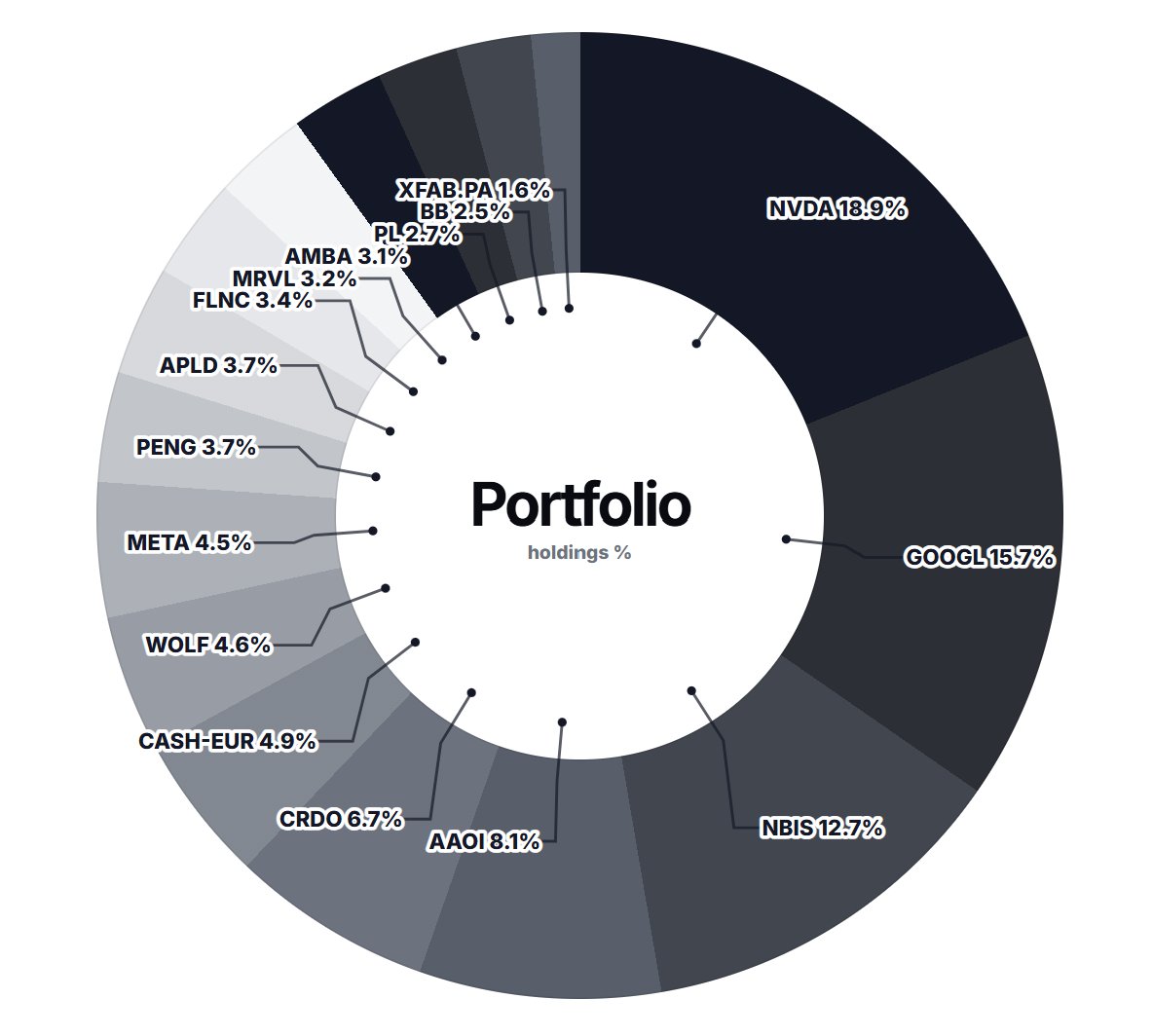

From here and into the foreseeable future (1-3 years) I believe:

$AAOI can pull a 4-5x

$MXL can pull a 8-10x

$WOLF can pull a 10-14x

Obviously macro can affect the timeframe, but that’s why I divide my portfolio into 2. One portfolio (with different stocks) that works as a buffer that absorbs all my overthinking. That way I won’t make any impulsive decisions on my 2nd portfolio that contains names like the above where I have a particularly high conviction.

I don’t wish to give macro much power as I can’t control it. I find this approach to be helpful on the psychological side of things.

8

10

149

20,340