The evolution of venture capital. Invest in early-stage start-ups with a tokenized fund for unparalleled liquidity. More at truescopeventures.com.

Joined March 2024

- Tweets 102

- Following 297

- Followers 53

- Likes 169

8 Photos and videos

TrueScope Ventures retweeted

🏦 BIG BANKS RECOGNIZE RWAs

"What clients really want is to be multi-border, multi-asset, and to be able to do these things 24/7" - $2T CITI bank CFO, Mark Mason

Tokenization is inevitable. 🔥

55

117

599

52,498

TrueScope Ventures retweeted

STEAK 'N SHAKE COO SAYS, "BITCOIN IS FASTER THAN CREDIT CARDS. WE ARE SAVING 50% IN PROCESSING FEES."

"WE ARE SEEING A SPIKE IN GROWTH AFTER ACCEPTING BITCOIN" 🚀

158

430

4,041

185,446

TrueScope Ventures retweeted

Canton Network “most liquid assets will go on-chain in the next five years”

Hundreds of trillions of dollars will come pouring in.

Some companies will issue direct.

Many networks will connect and interoperate.

Hundreds of Trillions: Tokenization Revolution 💎📈

According to the latest WEF report, there is over $255 TRILLION in marketable securities just waiting to be "unlocked" through Distributed Ledger Technology (DLT). 🔓

Here’s why the game has changed:

🔹 Instant Settlement (T 0): Say goodbye to the "waiting three days for my money" era.

🔹 Fractional Ownership: High-value assets like private equity are being sliced into affordable pieces. Everyone gets a seat at the table.

🔹 24/7 Markets: The world doesn't stop at 4 PM, and now, neither does trading.

🔹 Programmability: Smart contracts = compliance and dividends that run themselves. 🤖

The "exploratory phase" is officially dead. We are now in the execution era, where assets don't just sit there, they move, compose, and work harder. ⛓️🚀

12

87

214

39,572

TrueScope Ventures retweeted

Jan 20

BREAKING: $7 TRILLION UBS BANK CEO SAYS CRYPTO IS THE FUTURE OF BANKING AND FINANCE!

130

412

2,672

129,675

This is true

7

TrueScope Ventures retweeted

Jan 15

🔔 The Senate Banking Committee Should be Ashamed of Themselves.

Are you kidding me??? You guys tried to take away crypto decentralization without the public knowing… SHAME ON YOU.

Thank you to @Coinbase CEO @brian_armstrong and his team for standing up for the people on this matter.

The Government is trying to DESTROY crypto.

People, you NEED to do research on this an SPEAK UP. This could be very bad for crypto if your voices aren’t heard….

8

48

181

3,627

TrueScope Ventures retweeted

Jan 15

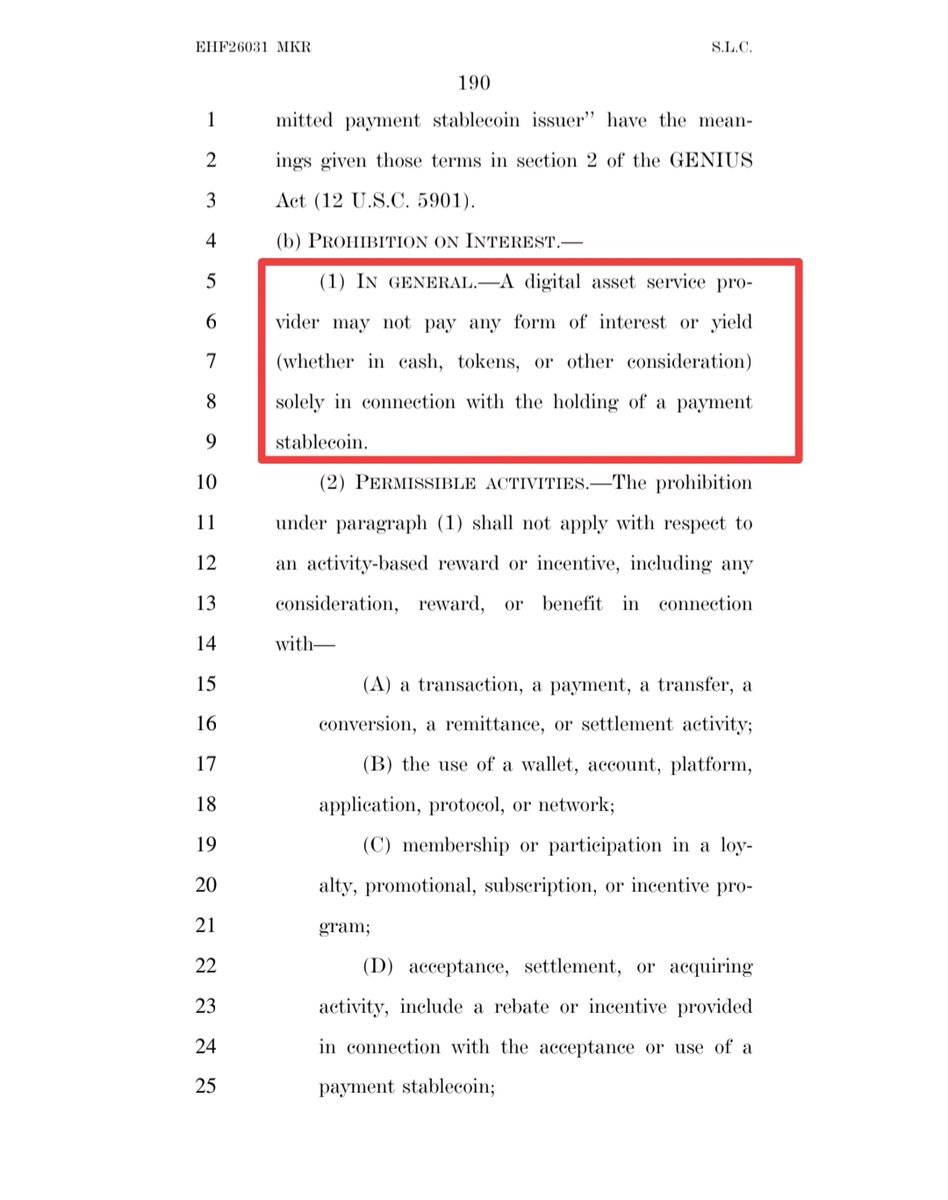

Stablecoins that pay interest would torpedo fictional reserve banking.

Delivering a world where your deposits are actually backed.

That's why banks are trying to cripple them.

53 banking associations just wrote themselves a $6.6 trillion protection bill.

They called it the CLARITY Act.

Here is what they do not want you to understand.

Banks pay depositors 0.1% interest. Stablecoin issuers hold Treasury bills earning 4.5%. If stablecoins could pass that yield to users, banks lose the deposit war. They cannot compete. The math is fatal.

So they made competition illegal.

The Kansas City Fed calculated what happens if stablecoins pay competitive rates. Banks lose 25.9% of deposits. $1.5 trillion in lending capacity vanishes. The entire community banking model collapses.

Their solution was not innovation. Their solution was legislation.

The CLARITY Act everyone is celebrating contains Section 404 prohibiting yield payments through any mechanism. Not just from issuers. From exchanges. From affiliates. From partners. Every single pathway to competitive returns, closed by statute.

Brian Armstrong reviewed the 278-page draft for 48 hours. He withdrew Coinbase support at 11pm. The markup was postponed by morning. He saw what Wall Street analysts missed entirely.

This is not crypto regulation.

This is Dodd-Frank for digital assets. Incumbents writing rules that crush competitors. Regulatory capture so brazen they published the lobbying letters on their own websites.

The American Bankers Association. 52 state banking associations. The Community Bankers Council. All coordinating to eliminate an industry they cannot beat in open markets.

Meanwhile China made e-CNY interest-bearing on December 29.

America is banning stablecoin yield while Beijing is paying it.

The crypto industry spent years begging for regulatory clarity.

They got it.

Clarity that $6.6 trillion in deposits will be protected at any cost. Clarity that banks write the rules. Clarity that if you cannot win in markets, you win in Congress.

This is the largest regulatory capture event in American financial history.

And it is being sold as innovation policy.

105

623

2,453

85,469

TrueScope Ventures retweeted

Jan 15

This is why banks oppose stablecoin yield.

If stablecoins pay interest, deposits leave banks. That means less leverage, less lending, and less profit.

Blocking yield is solely about protecting the banking model.

Jan 13

Stablecoins are better than banks.

But this part of CLARITY ACT sets rules around when stablecoin yield is allowed.

It prohibits digital asset service providers from paying interest/yield when the only condition is holding a stablecoin. But it does not apply to rewards that are tied to specific actions.

Incentives connected to actions like transactions, transfers or settlements, wallet or application use, and participation in loyalty programs.

The effect is to separate passive balance based yield from activity based rewards.

Stablecoins can still generate returns when they are used within a network or application, but not when they are held idle.

If this sticks, they would not be permitted to function as interest bearing instruments in the same way as deposit accounts.

Banks see what’s coming and this blocks competition.

85

259

1,134

79,559

TrueScope Ventures retweeted

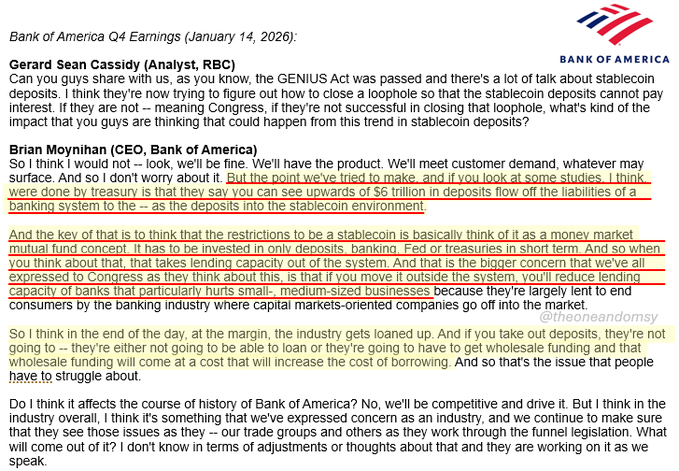

Jan 14

Brian Armstrong makes sense here. The current Senate compromise is worse than no bill at all. Sounds like the banks have been meddling.

Jan 14

BREAKING: Coinbase CEO Brian Armstrong says Coinbase "can't support" the crypto market structure legislation as currently written 👀

"We'd rather have no bill than a bad bill."

91

256

1,754

110,755

27 Jun 2025

A significant step was taken this week as it was announced that @FannieMae and @FreddieMac will include homeowners #bitcoin and other #crypto holdings as criteria when they purchase mortgages from banks.

1

1

64

27 Jun 2025

This is a huge step. The goal of this administration is to privatize the GSE's. That goal can be achieved by tokenizing mortgage backed securities. Tokenized MBS will decentralize the market as it re-invents the mortgage lifecycle.

1

23

27 Jun 2025

19

TrueScope Ventures retweeted

25 Jun 2025

⚡️ LATEST: Paradigm will join a $100M funding round for prediction platform Kalshi, pushing its valuation over $1B.

54

20

164

28,602

10 Jun 2025

The traditional relationship between Limited Partners and #venturecapital funds is changing, challenging long-held assumptions about the roles of its key players. truescopeventures.com/wp-con…

1

9

10 Jun 2025

At TrueScope Ventures, we apply the crypto ecosystem model to our Limited Partners in order to establish a growth network for our portfolio companies.

1

6

10 Jun 2025

We are innovators, we invest in innovators, and we invest with innovators. The emerging LP ecosystem is superior to the traditional model because it creates a better experience for everyone.

8