Roger Farmer's Economic Window. Professor of Economics, Warwick University and Distinguished Professor of Economics UCLA.

Joined March 2009

- Tweets 9,456

- Following 554

- Followers 15,414

- Likes 5,278

395 Photos and videos

Pinned Tweet

30 Oct 2025

No, the NK model is neither elegant nor useful.

The IS/LM model was useful — but incomplete — because its core equations summarize observable empirical relationships between aggregates. The attempt to graft a forward looking ‘Phillips curve’ onto the model was an unmitigated disaster. @jasonfurman @FrancoisGeerolf @monacelt

1. The Euler equation is an elegant description of the first order condition of a representative agent with perfect foresight. That agent does not exist. A much better foundation for understanding how consumption moves over time was Friedman’s permanent income hypothesis. And since the work of Truman Bewley, we have a firm foundation for that equation that is grounded in borrowing constraints and incomplete markets in a heterogeneous agent model.

2. The NK Phillips curve does not characterize any observable empirical regularity. It never has. The original Phillips curve, a connection between wage inflation and unemployment in UK data, disappeared soon after Phillips published his eponymous article. The reason it takes a semester to teach the NK Phillips curve is that it requires a set of ugly non refutable theoretical contortions that only a mother could love.

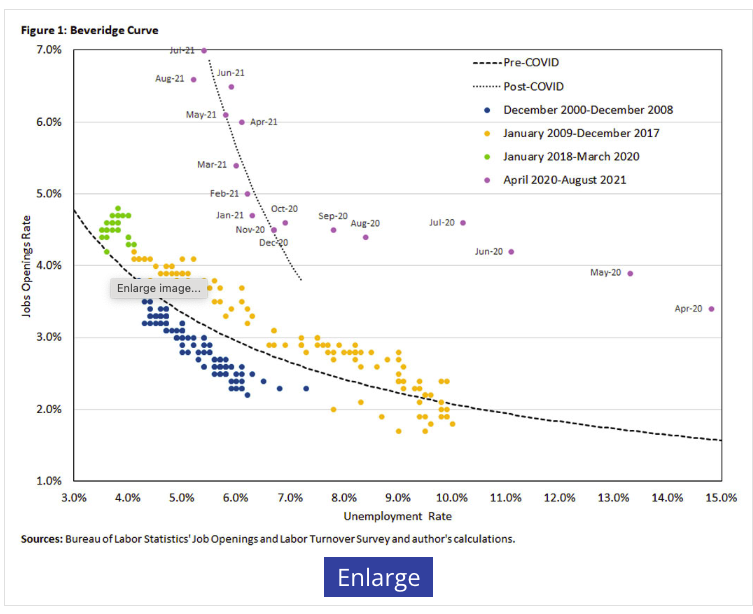

3. The NK model has no unemployment. People voluntarily change their labor supply behavior in response to ‘shocks’, the consequences of which are correctly forecast. That assumption does not fit with what we know about labor markets. I blogged about that here

rogerfarmer.com/rogerfarmerb…

4. The NK model assumes that employment (not unemployment) fluctuates around a stationary ‘natural rate of unemployment’. I wrote about that here

static1.squarespace.com/stat…

Fed economists spend countless hours attempting to estimate this ‘natural rate’. This is a Sisyphean task since the unemployment rate in data is essentially a random walk.

The correct strategy at this point is to abandon much of the rational expectations revolution and to reconstruct macroeconomics beginning with what we knew circa 1960. This, I believe, is already beginning. There is a large body of theorists working on Bewley models and that group has concluded that rational expectations was a misstep. See, for example, the recent working paper by @ben_moll

benjaminmoll.com/wp-content/…

I am not as convinced as Ben, that our models must be nonlinear with global solution methods since, if Ben’s approach is successful, even linearized models in aggregates will likely display very different properties from either NK or classical RBC economies. But dropping the full implications of rational expectations is a promising way forward.

30 Oct 2025

I don’t like the word “science” for this sort of thing.

But this is a very useful way to understand the world, consider some of the most important macroeconomic policy debates, and a flexible framework that you can build on to add different nuances and complexities.

9

57

281

89,588

Roger E. A. Farmer retweeted

3

9

40

7,962

This piece from @psantacl explains the error in the degrowth agenda furthered by @PikettyWIL @stiglitzian and others who signed the @guardian article theguardian.com/commentisfre… @JonSteinsson @albertobisin It is well worth reading. If you teach undergraduates: make sure they read @psantacl’s arguments. The level of hubris demonstrated by the signers of the Guardian piece is extraordinary.

Jun 14

"The pie is fixed. The Earth is a closed system. You cannot have infinite growth on a finite planet."

I hear this constantly, and it's delivered like a law of physics — case closed, only a compromised economist could disagree.

It's wrong. And the mistake is revealing, because it isn't in the physics. It's in the economics smuggled inside the physics.

2

3

16

4,347

Roger E. A. Farmer retweeted

Jun 13

Barnaby Philip John Webber

11/01/2004-13/06/2023 💔

If you can, share these images of the beautiful soul stolen from us by the worst of humanity.

Let his face today burn bright.

Barney, I promise you there will be accountability 💛💚

For You. For Grace. For Ian.

740

7,457

24,546

882,732

Jun 13

💯

Jun 13

What would it require to enforce Piketty’s plan? About this matter, he is conveniently vague. Confiscating something on the order of 10% of world GDP and redirecting it through a newly created supranational body does not happen by asking nicely. You cannot restructure the global economy at that scale without a coercive apparatus that dwarfs anything in human history.

The mechanism must be authoritarian. It would require a world government with the power to tell billions of people which jobs they may and may not hold, what they may build, what they may eat and how many hours they are permitted to work.

And to what end? “Climate change” is an insufficient answer when Picketty’s entire edifice is built on a discredited foundation. The report relies on a baseline from the RCP8.5 climate scenario that projects Earth warming by as much as 4.8 degrees Celsius by 2100. But last month, the UN’s own climate panel officially retired RCP8.5 (always a high-end estimate) as “implausible.” A more central projection is about 2.7 C. Replies to Piketty’s X feed pointed this out immediately. His response, as far as anyone can tell, has been silence.

That leaves the inequality argument. Worldwide income inequality is nearing a 150-year low, but Piketty insists that radical redistribution of wealth is essential for the Global South. And where have billionaires and wealth been popping up fastest in recent decades? Embarrassingly, data from Piketty’s World Inequality Database confirms that it’s in South and Southeast Asia, as well as East Asia. These are the exact Global South regions that have spent recent decades rescuing hundreds of millions of people from poverty through market-directed economic growth.

latimes.com/opinion/story/20…

1

1

5

1,573

Roger E. A. Farmer retweeted

Jun 11

Another comment: all this is a sad sign of intellectual desperation of the left - reduced to massaging some of the data - and disregarding the rest - to fit fundamentally failed policies … one can be on the left in terms of values and objectives (as I consider myself) and still accept good economics and solid empirical evidence to design possibly successful (at least not yet failed) policies.

5

22

204

20,872

Jun 11

💯

Jun 11

This is crazy good and interesting. It shows how the sausage is made in Mazzucato and Piketty’s work.

I also think it is important to note - as it is done in the essay - that while Mazzucato is just pure and simple advocacy - no contribution to research - Piketty (and coauthors) have contributed great data (that many of us are using).

4

2,788

Roger E. A. Farmer retweeted

Jun 10

Last week I published "The Fatal Conceit, Renewed." Today I publish its companion: a catalogue of the methodological errors in the work of Thomas Piketty and Mariana Mazzucato.

The errors are not peripheral. They are devastating — and they all lean in the same direction. In econometrics, we have a name for an estimator whose errors all point one way: biased. In politics, we also use the same name.

Why spend the effort taking these two apart? Because they are dangerous. Piketty and Mazzucato are the intellectual darlings of today's left. They supply a veneer of scholarly respectability to what the left is forever seeking: a justification for higher taxes and more state intervention. The oldest idea in politics — that a few enlightened people know better than the rest of us what to do with our money.

The fame is real. The findings are not. Here is the audit.

10

69

292

55,409

Roger E. A. Farmer retweeted

Jun 11

I don't know what Piketty, Stiglitz, and co. are smoking. Global poverty rates have never been lower. Progress on basic global health and wellbeing measures has been amazing over the past few decades. "End of the road"?!? Come again!?!

theguardian.com/commentisfre…

119

458

2,536

810,305

Jun 10

💯

Jun 10

For the record.

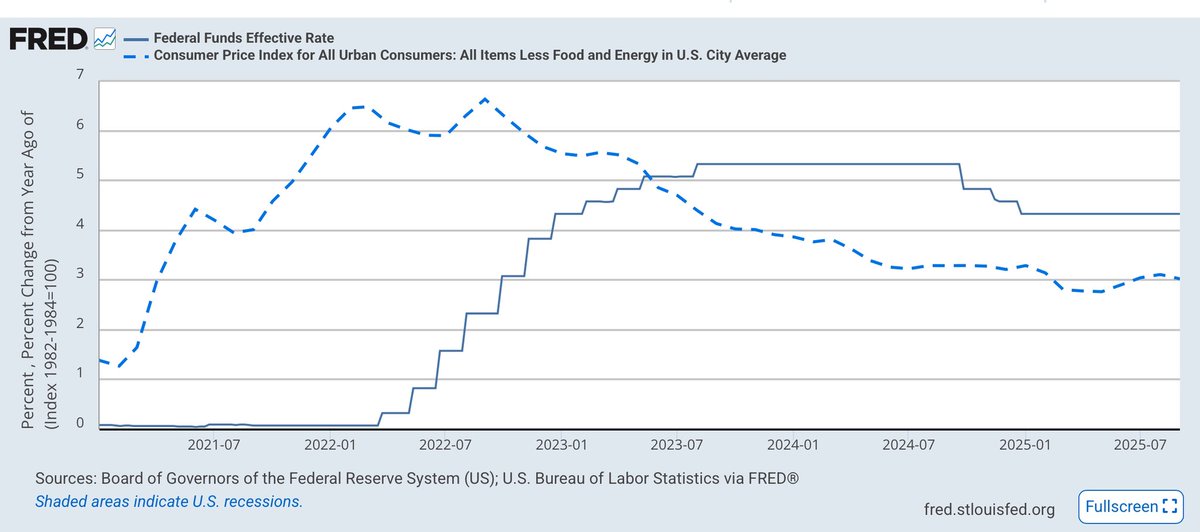

Keynesian brain rot is now hard‑wired into central banks and Wall Street: every supply shock is instantly rebranded as “inflation,” and the reflex is to demand rate hikes, as if tighter money could magically print oil, repeal tariffs, or reopen the Strait of Hormuz. This is not analysis; it is a category error with a policy rate attached.

Inflation, properly defined, is a monetary phenomenon: a sustained rise in the general price level, or a persistent fall in the value of money. It shows up when most prices trend higher together, not when one or two sectors reprice violently. A change in relative prices is about who gets squeezed within a largely fixed nominal envelope. When energy, freight or chips spike, some prices must rise and others, in real terms, must fall. That is redistribution and a hit to real income, not automatically an inflation regime.

Any visible price spike, from new tariffs to a shipping choke point in the Strait of Hormuz, is now lazily labelled “broad inflationary pressure,” and the default prescription is tighter money, even when the underlying impulse is clearly a relative‑price shock rather than excess nominal demand. The result is pro‑cyclical tightening into real‑side damage, on the comforting illusion that monetary punishment can “fix” a shortage of physical capacity or geopolitical constraints.

Meanwhile, housing, the most interest‑rate‑sensitive sector and in many economies already in a rolling recession – plainly did not cause the supply shock, yet is sacrificed first on the altar of this misdiagnosis.

There's a new version of this post

66

Roger E. A. Farmer retweeted

A tribute volume dedicated to Hoover scholar John B. Taylor discusses his life, his scholarly and government work, and the profound impact of his eponymous "Taylor rule." Learn more in a new Defining Ideas excerpt: hoover.org/research/celebrat…

1

9

20

9,122

Roger E. A. Farmer retweeted

Jun 5

An honor to co-author an article in this volume on John Taylor. Essentially every central bank around the world calculates the Taylor Rule as a reference. John Taylor will easily be one of the economists alive today whose work will still be studied one hundred years from now.

A tribute volume dedicated to Hoover scholar John B. Taylor discusses his life, his scholarly and government work, and the profound impact of his eponymous "Taylor rule." Learn more in a new Defining Ideas excerpt: hoover.org/research/celebrat…

2

9

78

6,781

Roger E. A. Farmer retweeted

This is a full radical degrowth agenda. Sad to see

Jun 4

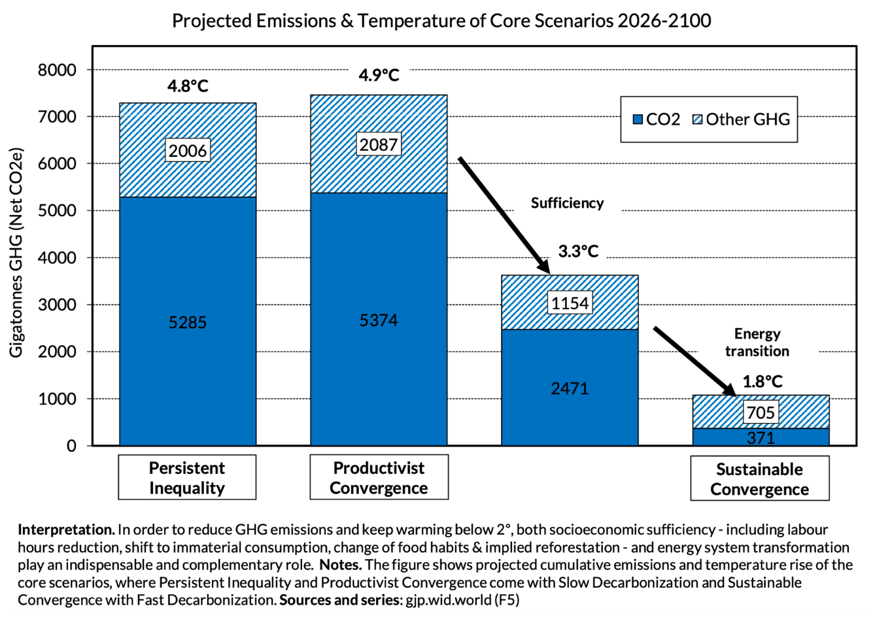

The key finding of the report is that energy transition alone will not suffice.

We need to combine it with "sufficiency" to stay within 2 degrees. This includes labour hour reductions, growth caps in rich countries, less material consumption, and changes in food habits.

Community note

This report uses a ~4.8°C baseline. In May 2026, the U.N. climate panel officially retired this scenario (RCP8.5) as "implausible." Updated projection: ~3.5°C. Sources: NYT & Washington Post, May 2026.

nytimes.com/2026/05/26/cli…

washingtonpost.com/climate-enviro…

lemonde.fr/en/environment…

35

124

1,058

98,457

Roger E. A. Farmer retweeted

Jun 5

C’est une opération marketing. Le débat honnête n’a pas de sens désormais. Vous avez fait, avec d’autres, votre possible pour challenger l’argumentaire branlant de GZ en espérant probablement une correction. Elle n’arrivera jamais. Ce n’est plus de la science mais de la vente.

2

7

104

4,777

Roger E. A. Farmer retweeted

Jun 4

Le terme "incompétent" est fort. Mais il faut admettre que "sloppy" et "bâclé" s'appliquent très bien.

J'ai quatre articles qui montrent exactement comment lui, Saez et Zucman ont coupé les coins ronds en mautadine.

Depuis je n'accepte aucune de leurs affirmations sans moi-même aller voir l'architecture des données.

Voir:

Jun 4

Je ne partage pas les usages politiques qu'il fait de son travail, mais dire Thomas Piketty est économiquement incompétent n'est pas sérieux. Le Capital au XXe siècle est un livre discutable mais important.

7

36

250

33,207

Roger E. A. Farmer retweeted

Jun 4

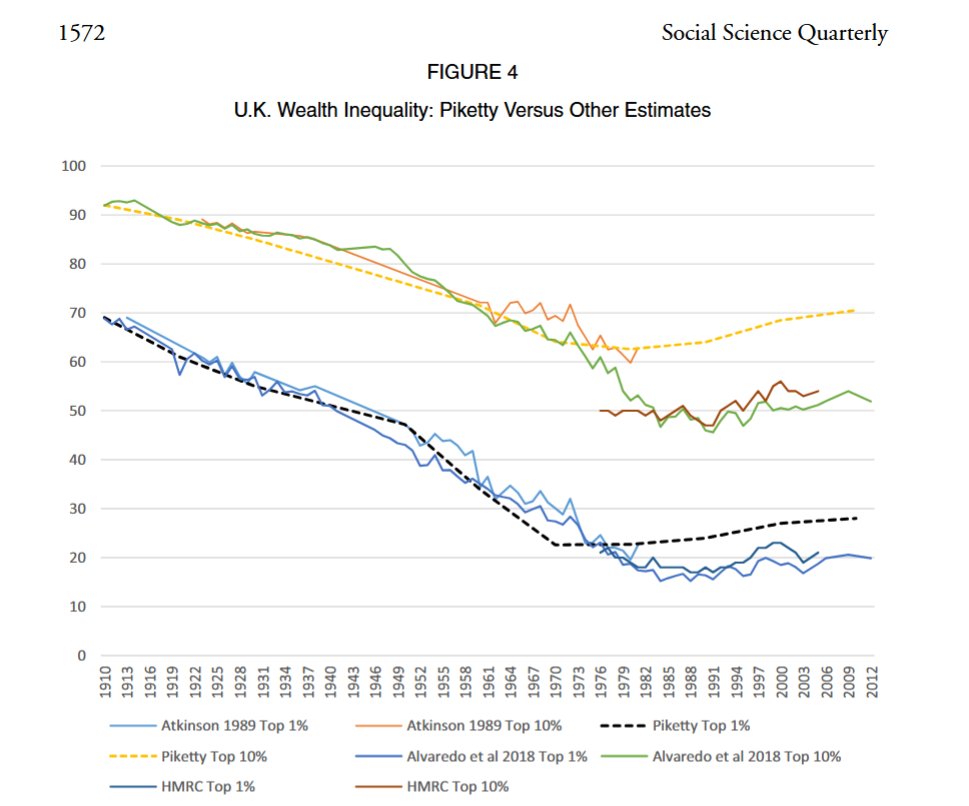

This is utter nonsense. Zucman's mentor Piketty manipulated the UK data to show rising wealth inequality, when it has been flat for decades.

Data duplicity is a clear and recurring pattern for these two Frenchmen.

Jun 4

The UK is in decline.

Billionaire wealth is rocketing.

It's time to tax the super rich.

My conversation with the brilliant @gabriel_zucman:

youtu.be/1cG4ULI1yCo?si=DJJ2…

5

46

275

11,186

Jun 3

I agree with this assessment from @DrJStrategy: To paraphrase Greenspan

“I guess I should warn you, if I turn out to be particularly clear, you’ve probably misunderstood what I said.”

Central bankers are acting in a world of uncertainty not of risk ; a distinction made by Frank Knight. Economic models are models of risk.

Basing policy on models that attribute an unwarranted degree of confidence to decisions is hubris and likely to lead to bad outcomes.

Central bankers would do well to follow Wittgenstein’s advice:

“Whereof one cannot speak, thereof one must be silent.”

Jun 3

Stanley Fischer Would Applaud This

Warsh can’t scrap the dot plots and forward guidance fast enough. In a world where Stanley Fischer prized humility about models and genuine data dependence, the current regime looks like the opposite: an illusion of precision that locks policy into yesterday’s forecast and invites the Street to trade “the path” rather than the data. The dots convert a committee’s uncertainty into a pseudo‑promise, then punish any attempt to change course as a credibility problem rather than a sign of learning.

Worse, the communications revolution has metastasized into a noise factory. There is no plausible world in which a dozen regional presidents and assorted governors doing a daily speaking tour improves policy or price discovery. It fragments the reaction function, encourages grandstanding, and turns every luncheon remark into a tradable headline. A central bank is not a content platform; it is, as Fischer would insist, a steward of stability, not a streaming service for half‑formed views.

If Warsh is serious about restoring the Fed’s authority, the fix is straightforward: scrap the dots, radically curtail forward guidance, and shut down most of the

speechmaking. Let the institution speak mainly through its decisions and a small number of tightly disciplined communications. Fewer words, clearer incentives, more genuine uncertainty, forcing markets back to the hard work of inference rather than quote‑mining Fedspeak.

6

1,312

Roger E. A. Farmer retweeted

Jun 3

I have worked with @BrianCAlbrecht on questions closely related to the issues of stability analysis that @IvanWerning and Lorenzoni have been wrestling with recently.

Some of our papers related to this topic:

link.springer.com/article/10…

link.springer.com/article/10…

onlinelibrary.wiley.com/doi/…

And some of my observations regarding this topic in general:

1. A perfectly competitive general equilibrium describes a situation where agents know everything they need to know and where the price system enables agents to execute all trades to reach a Pareto efficient allocation.

2. This mechanism of trade through the competitive price system is also very minimalistic in the sense that agents use a minimal amount of information.

3. This competitive general equilibrium can be understood as a steady-state of a learning process operating in a reasonably "fixed" or stable environment, which features imperfectly competitive markets that become more competitive as information "percolates" over the interested parties and profit margins tend to be reduced over time.

4. Macroeconomic issues such as inflation and business cycles that generate fluctuations in unemployment and output are intimately related to this concept of "agents learning towards general equilibrium."

5. That is, if the agents in the economy are very "flexible" and "smart," the resulting reaction of the economic system to unanticipated exogenous shocks will result in quick adjustment and therefore low levels of output and unemployment fluctuations.

6. Random/directed search theory is intimately related to these issues. Hence, why the new monetarist economists such as @1954swilliamson and Randy Wright are tackling money and macro topics using search, and why we have labor search literature to explain why unemployment occurs in "equilibrium." Although I think most of lacks an explicit approach to learning and "convergence process to GE over time," which I tried to bridge in my job market paper (link.springer.com/article/10…).

Overall, I think that this "convergence to GE studies" field is enormous and ultimately the field in economics that has an intimate relationship to the evolution of economic theory over the last 80 years, and that there is still a lot (perhaps most) of stuff to be done.

Jun 2

A great comment from @hidetomitanaka on the magisterial paper by @guido_lorenzoni and @IvanWerning and one I endorse. I hope their work leads others to return to questions that predate the rational expectations revolution.

My number one question is: How does an economy function when trades take place outside of a Walrasian equilibrium? I do not think that Calvo pricing is a satisfactory answer to that question because it is, in essence, an alternative equilibrium concept — as opposed to a disequilibrium trading mechanism.

A satisfactory resolution would contain, IMO, several elements.

1. Expectations matter and they do not always coincide with outcomes, even probabilistically.

2. The set of traders changes over time as a consequence of birth and death and some traders, in all markets, are more sophisticated than others.

3. The world is not fully ergodic over the lifetime of a typical agent: see our definition here, in work with J. P. Bouchaud, of quasi-non ergodicity: static1.squarespace.com/stat…

4. Point 4 implies that people will not generally be able to learn in finite time. The economy will NEVER attain an equilibrium in the Walrasian sense — or in the Lorenzoni-Werning sense which adds price setters.

5. Inventories act as a buffer against imperfect price discovery: they do not appear as an important element in our theories. They should! This, I believe, is one of the points of @hidetomitanaka’s point about early vs late Hicks.

None of these points should be taken as a negative assessment of the LW paper which is a tour de force and which I highly recommend.

5

25

6,100

Jun 3

Great thread from @drmtgr

Jun 3

Another interesting thing, since RF raises the issue of inventories, is in fact how one should think of production functions if seriously considering disequilibrium problems.

I think the issue is that the common "language" we use to frame things in econ is at heart a language

1

5

1,425

Roger E. A. Farmer retweeted

Jun 3

Il faut se frayer son chemin, c'est un pari mais moi je suis globalement très content de ma situation

1

1

3

1,600

Jun 2

Great post from @MZunigaP about the founder of the UCLA school ht @BrianCAlbrecht

Jun 2

‘Uncertainty, Evolution, and Economic Theory,’ by Armen Alchian

truthonthemarket.com/2026/05… (via @TOTMBLog).

1

1

7

2,244