Honest Analysis | In-depth Research (Article Session) | Narrative Trader | AI & Crypto Believer

Joined December 2014

- Tweets 9,108

- Following 1,289

- Followers 11,603

- Likes 10,099

990 Photos and videos

Foxi 🦊 retweeted

13 Mar 2025

There's been a lot of discussion on Hyperliquid's margin design. I’ll address some flaws in the common arguments and explain Hyperliquid's first-principles based approach to improving the system. To my knowledge, this is the first such design in margining systems.

Perhaps other teams will find it useful for their own logic. Like good theories in physics, the best margining design is simple, canonical, explainable, and works in a wide variety of pathological scenarios.

1. The conclusion of some people has been that there needs to be a centralized force that detects and limits malicious behavior. This completely violates the purpose of defi and everything Hyperliquid stands for. This forces users back to a web2 world where the platform has the final say. True decentralized finance is worth it, even if it is 10x harder to build. Just a few years ago, no one believed DEX/CEX volumes would reach its ratio today. Hyperliquid is leading the charge here and has no intention to stop.

2. Some assume that copying approaches from CEXs will work in defi. The most common suggestion I've seen is per-address margin requirement fraction scaling with position size, as CEXs only offer higher leverage for smaller positions. However, this doesn't work to prevent manipulation attempts on a DEX because a sophisticated attacker can easily open positions on many accounts. Nonetheless, this will help somewhat reduce the impact of "organic whale" positions and is on the list of features to implement.

3. Another suggestion is to implement some features that severely limit usability of the platform in exchange for safety. For example, if unrealized pnl is not withdrawable, many attacks are not possible. Indeed, Hyperliquid pioneered isolated-only perps for illiquid assets which feature this safety mechanism. However, this change would have a crippling effect on funding arbitrage strategies, where unrealized pnl from Hyperliquid needs to be withdrawn to offset the loss on other venues. Real user needs are a top priority in system design.

4. There were also suggestions to innovate on design by having margin settings based on global parameters. However, liquidation prices need to be deterministic functions of price and position size. If global parameters such as open interest were added as inputs to margin requirements, users would lose confidence in the ability to use leverage at all.

So what's the answer? We all want defi, but a permissionless system must be robust to manipulation at all scales.

The answer lies in understanding the true problem with large positions: they are difficult to mark. The first order approximation of mark price times size breaks down when market impact approaches maintenance margin. It's impossible to accurately simulate market impact because book liquidity is a path-dependent function of time and actions of other participants. Without simulating market impact, it can be possible for liquidation to be a low-slippage way to exit at a price that is unfavorable to the liquidator.

Therefore, Hyperliquid's margining system update has the following desirable property: any liquidated position is either a loss relative to entry price, or at least a (20% - 2 * maintenance_margin_ratio / 3) = 18.3% loss relative to the last margin transfer out (using an example of 20x leverage). An organic 20x user who makes 100% return on equity after a 5% move will still be able to withdraw the majority of the pnl without closing the position. However, by introducing separate margin requirements between transfers and opening new positions, profitable manipulation attempts require moving the mark price almost 20%. This kind of attack is infeasible from a capital perspective.

Finally, I'd like to point out that the mark price problem also solves itself as market makers continue scaling up on Hyperliquid. It's quite possible that the trader yesterday could have lost money in aggregate. $1.8M pnl longing on Hyperliquid could have been more than offset when pushing the price on other venues, or using other accounts on Hyperliquid. HLP took over an undesirable position, losing $4M. The only market participants who definitely made money in aggregate are the market makers. With millions of dollars of pnl to be made in the span of minutes, it's becoming clear to sophisticated participants that Hyperliquid is one of the venues with the best flow. As liquidity improves, it will become more and more expensive to dislodge prices. So while the margining system improvements will go a long way, the allure of easy pnl attracting market makers will provide an independent source of robustness over time.

The future is decentralized.

Hyperliquid.

319

634

2,677

483,955

Morgan Stanley’s price discovery happens on @tradexyz

38

127

1,647

219,986

The best innovation in this cycle is HYPE and tradexyz.

There is literally no second best. Many tradfi will use hyperliquid as a price discovery venue from now on. The non-KYC advantage gives hyperliquid the best edge in this financial market.

Before CFTC did anything, hyperliquid would still remain the best token to long in crypto.

May 14

price discovery for the largest AI tech IPO of the year happened on crypto rails through a decentralized perpetuals platform & gave retail an entry -50% lower than what it is going to open at on the Nasdaq

2

1

2

276

Foxi 🦊 retweeted

1/3 PropAMM liquidity is now fully operational on Ethereum mainnet!

Three makers are live in every Titan block, and quotes are already consistently beating Binance VIP9 taker fees for retail orders (trades <$1k).

6

14

187

66,388

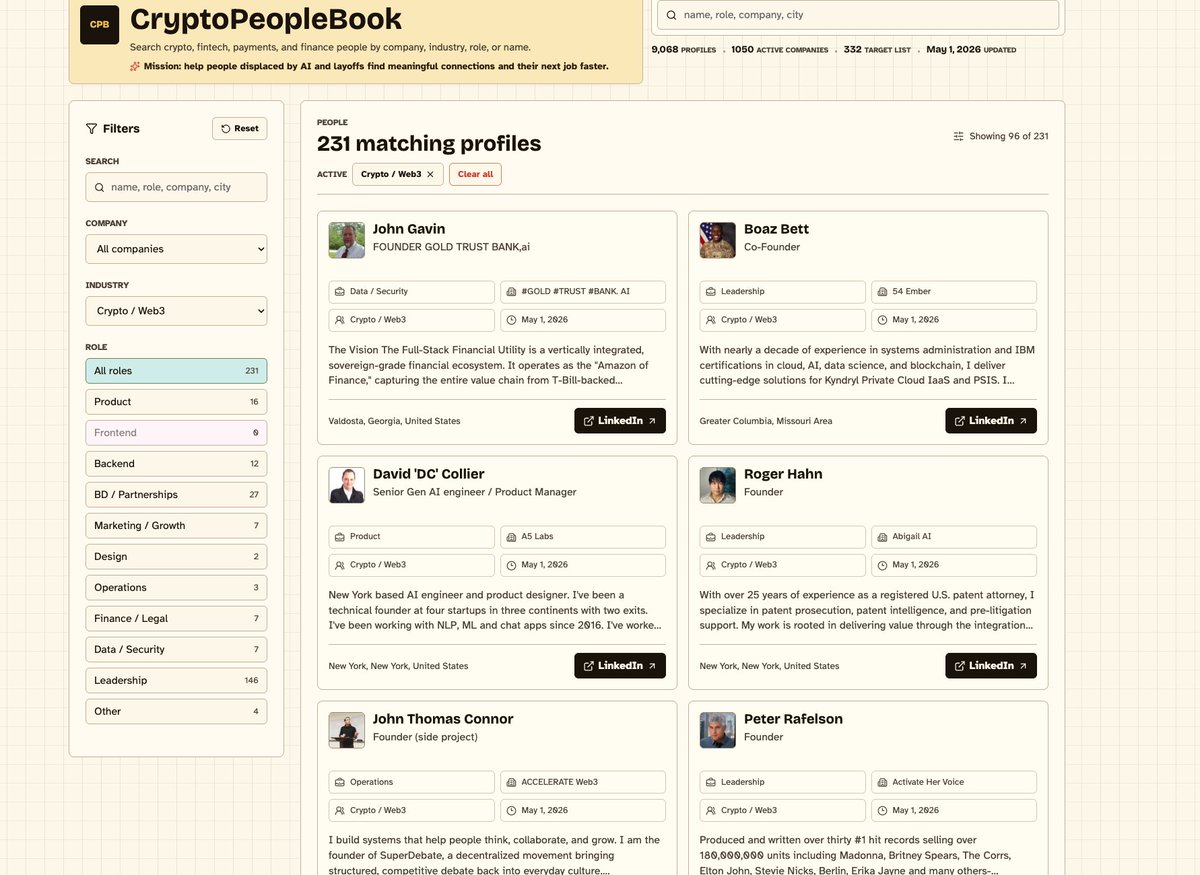

It's time to pull this web3 people contact book out and start dming people in LinkedIn

"ser, I know your time is valuable here's the 3 bullet points about me: ..."

This is an email I sent earlier today to all employees at Coinbase:

Team,

Today I’ve made the difficult decision to reduce the size of Coinbase by ~14%. I want to walk you through why we're doing this now, what it means for those affected, and how this positions us for the future.

Why now

Two forces are converging at the same time. We need to be front footed to respond to both.

First, the market. Coinbase is well-capitalized, has diversified revenue streams, and is well-positioned to weather any storm. Crypto is also on the verge of the next wave of adoption, with stablecoins, prediction markets, tokenization, and more taking off. However, our business is still volatile from quarter to quarter. While we've managed through that cyclicality many times before and come out stronger on the other side, we’re currently in a down market and need to adjust our cost structure now so that we emerge from this period leaner, faster, and more efficient for our next phase of growth.

Second, AI is changing how we work. Over the past year, I’ve watched engineers use AI to ship in days what used to take a team weeks. Non-technical teams are now shipping production code and many of our workflows are being automated. The pace of what's possible with a small, focused team has changed dramatically, and it's accelerating every day.

All of this has led us to an inflection point, not just for Coinbase, but for every company. The biggest risk now is not taking action. We are adjusting early and deliberately to rebuild Coinbase to be lean, fast, and AI-native. We need to return to the speed and focus of our startup founding, with AI at our core.

What this means

To get there, we are not just reducing headcount and cutting costs, we’re fundamentally changing how we operate: rebuilding Coinbase as an intelligence, with humans around the edge aligning it. What does this mean in practice?

- Fewer layers, faster decisions: We are flattening our org structure to 5 layers max below CEO/COO. Layers slow things down and create coordination tax. The future is small, high context teams that can move quickly. Leaders will own much more, with as many as 15 direct reports. Fewer layers also means a leaner cost structure that is built to perform through all market cycles.

- No pure managers: Every leader at Coinbase must also be a strong and active individual contributor. Managers should be like player-coaches, getting their hands dirty alongside their teams.

- AI-native pods: We’ll be concentrating around AI-native talent who can manage fleets of agents to drive outsized impact. We’ll also be experimenting with reduced pod sizes, including “one person teams” with engineers, designers, and product managers all in one role.

In short: AI is bringing a profound shift in how companies operate, and we’re reshaping Coinbase to lead in this new era. This is a new way of working, and we need to leverage AI across every facet of our jobs.

To those who are affected

I know there are real people behind these decisions — talented colleagues who have poured themselves into this company and our mission. To those of you who will be leaving: thank you. You’ve helped build Coinbase into what it is today, and I am sincerely grateful for everything you've done.

All impacted team members will receive an email to their personal account in the next hour with more information, and an invitation to meet with an HRBP and a senior leader in your organization. Coinbase system access has been removed today. I know this feels sudden and harsh, but it is the only responsible choice given our duty to protect customer information.

To those affected, we will be providing a comprehensive package to support you through this transition. US employees will receive a minimum of 16 weeks base pay (plus 2 weeks per year worked), their next equity vest, and 6 months of COBRA. Employees on a work visa will get extra transition support. Those outside of the US will receive similar support, based on local factors and subject to any consultation requirements.

Coinbase prides itself on talent density. Our employees are among the most talented people in the world, and I have no doubt that your skills and experience will be highly sought after as you pursue your next chapters.

How we move forward

To the team that is staying, I know this is a difficult day. We’re saying goodbye to colleagues and friends you've been in the trenches with. But here’s what I want you to know as we move forward together:

Over the past 13 years, we have weathered four crypto winters, gone public, and built the most trusted platform in our industry. We’ve made it this far by making hard decisions and by always staying focused on our mission. This time will be no different – nothing has changed about the long term outlook of our company or industry. And most importantly, our mission has never been more important for the world. Increasing economic freedom requires a new financial system, and we’re building it.

The Coinbase that emerges from this will be more capable than ever to achieve our mission.

Brian

2

224

Foxi 🦊 retweeted

Apr 30

JFYI MEGA MINDS - Kumbaya takes a 50% cut of all swap fees. if you want to trade / LP elsewhere there is also Prism which has normal fee rake.

Wish I knew this yesterday, I gave Kumbaya $5k

prismfi.cc?ref=NLCAQHUU

13

14

94

25,089

After almost a half year, this is the first time that I'm using the Dapps on a "new" chain.

This is absolute good work. @hotpot_dao

I thought I will be forever put my money in US stock market.

1

3

266

Foxi 🦊 retweeted

4 Mar 2023

1/ Controversial take: hard work is more important than smart work.

It's a myth that we only have a few hours of good creative work per day. Train yourself to grind long hours first. You will surprise yourself. The work naturally become higher quality, less distracted.

3 Mar 2023

You'll get more done in 4 hours of deep work than 7 days of distracted work.

High - Quality Work = (Time Spent) x (Intensity of Focus)

All you need is a Weekly Schedule System.

Find my free template in the YouTube video below:

51

344

2,540

352,304

Introducing GPT-5.5

A new class of intelligence for real work and powering agents, built to understand complex goals, use tools, check its work, and carry more tasks through to completion. It marks a new way of getting computer work done.

Now available in ChatGPT and Codex.

2,484

6,875

51,526

13,115,570

Wait, so you telling me $ZEC is not crime?

With all due respect to @zachxbt, a coin can be manipulated since the float is low and was manipulated were a different story.

There are many projects keep dumping their token since TGE and we are not punishing those?

One coin 100x = crime

Hundred coin 10x = bull market

🤣

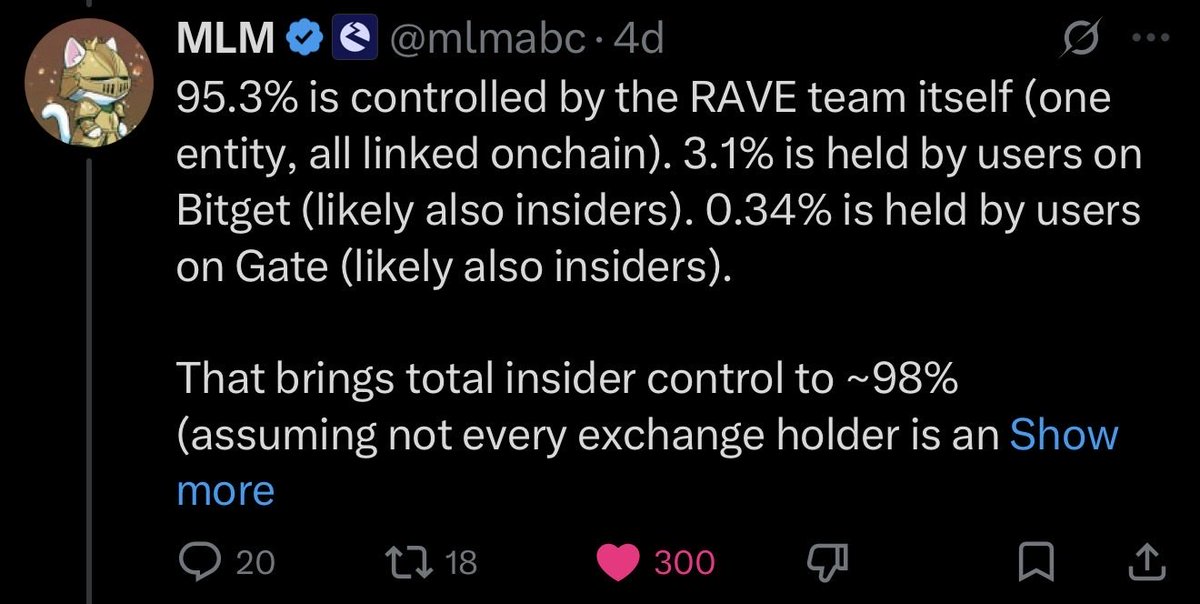

Pump and dump activity for $RAVE originated on @bitget @binance @Gate

Call to action for both @heyibinance @GracyBitget to do better and launch internal investigation offboarding the responsible actors.

Offering up to $10K bounty of my personal funds for whistleblowers to come forward privately to share evidence about parties involved

We cannot allow this blatant market manipulation by insiders controlling >90% RAVE support to further extract from retail investors.

523

Foxi 🦊 retweeted

Apr 17

📦New in · OKX Agent Trade Kit 上新!

-市场筛选×持仓分析:多维筛选 最长2年持仓历史,锁定资金异动

-情绪雷达:聚合3万 KOL与多家媒体 @BlockBeatsAsia @TechFlowPost @OdailyChina @wublockchain12 @PANews @bwenews 动态,量化多空,捕捉情绪反转

数据面 情绪面,从选币到验证,Agent 皆可为。

46

114

528

374,559

SEC - RWA assets, tokens

CFTC - derivatives, DCM & IB

SEC decision is not equal to CFTC

For your information

I love hyperliquid.

But whoever say this is a big win for hyperliquid should know that it’s not just DeFi front-ends.

Hyperliquid earn the biggest regulatory benefit from the current government and would still be safe for 2 years.

The next US government could do the same thing to hyperliquid like to @cz_binance.

Non-KYC exchange will have the best of time until then.

1

223

I love hyperliquid.

But whoever say this is a big win for hyperliquid should know that it’s not just DeFi front-ends.

Hyperliquid earn the biggest regulatory benefit from the current government and would still be safe for 2 years.

The next US government could do the same thing to hyperliquid like to @cz_binance.

Non-KYC exchange will have the best of time until then.

Apr 13

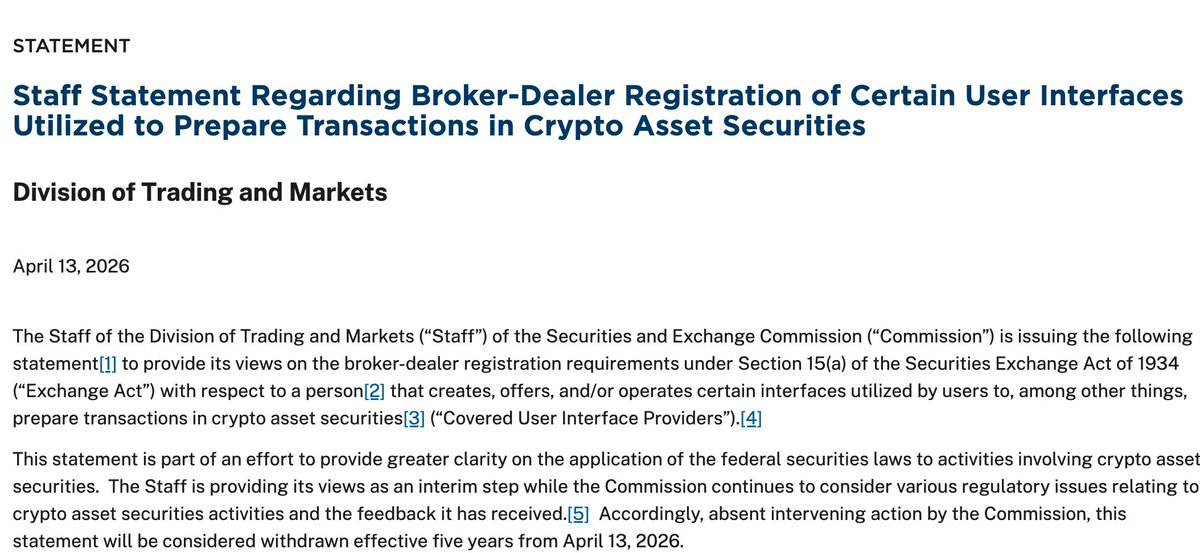

SEC Clarifies Certain DeFi UIs Can Operate Without Broker-Dealer Registration

The SEC’s Division of Trading and Markets said certain crypto trading interfaces, including DeFi front-ends, wallet extensions, and mobile apps, may operate without broker-dealer registration if specific conditions are met. These include no order routing, no investment advice, no custody of user assets, and only fixed, neutral fee structures. The guidance applies to self-custodial wallet interfaces and will remain effective for five years unless superseded by further SEC action.

2

556