16 Photos and videos

Pinned Tweet

14 Aug 2024

We are delighted to welcome @mariabrw to our team!!🥂🙌🎊

14 Aug 2024

Delighted to announce I’ve joined @freestylevc alongside @dsamuel @jennylefcourt @dsb - can’t wait to build with them and continue backing the next generation of exceptional founders! For more details, check out the announcement here: shorturl.at/kfy1E

1

7

1,257

Freestyle Capital retweeted

5 Dec 2025

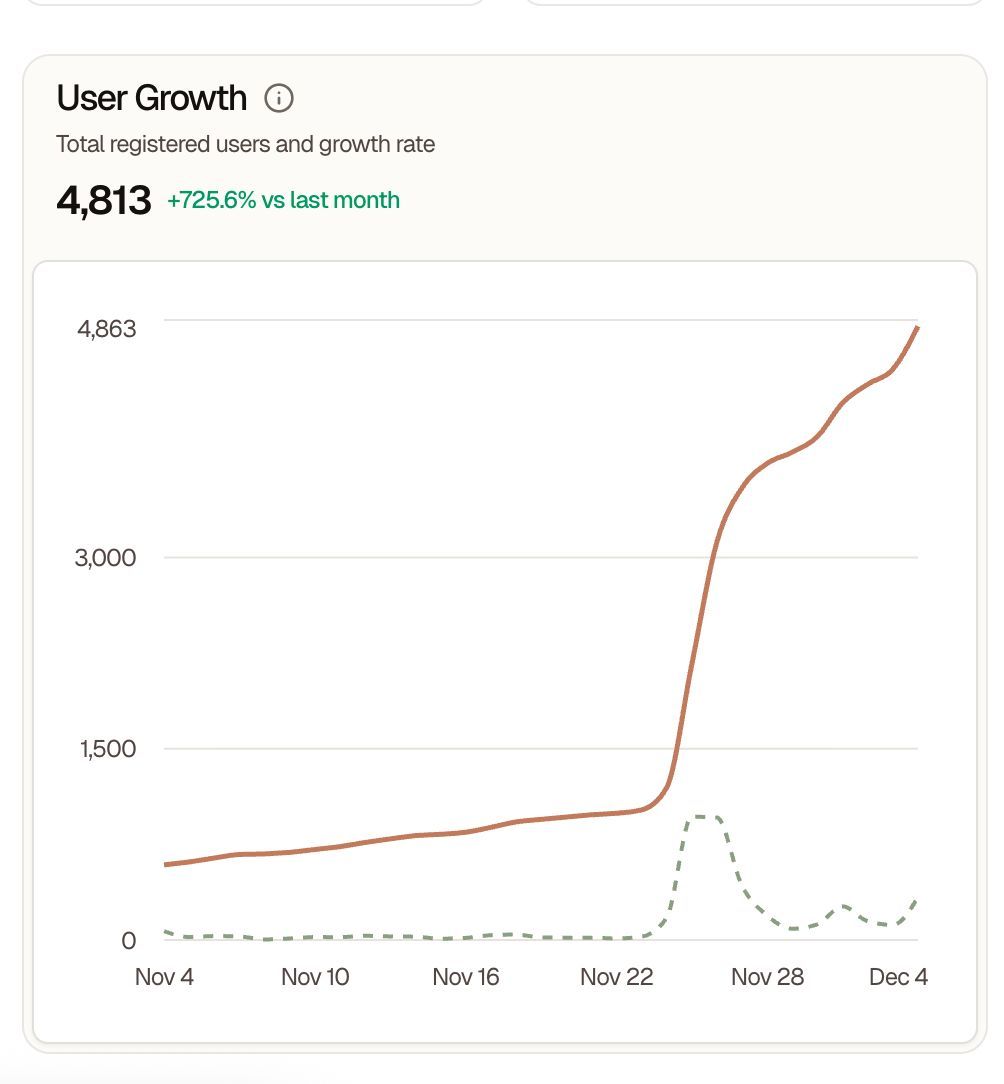

$40k in MRR in 12 days. This is going to be fun.

Founder–market fit gets a lot of attention. But I also like to think about founder–company fit, especially for repeat founders.

Some founders don’t just start companies.

They arrive at the one they were always meant to build.

Def true for @donnellycss with Searchable and delighted to back him alongside @imsamhogan and @aryanagab and an amazing team! LFG!

5

3

10

588

Freestyle Capital retweeted

27 May 2025

Founders can now build WAY faster with MUCH smaller teams.

Founded within @InvTechInc, @_InfinityConst is the first AI-native holdco that pairs top founders with the latest AI models to build revenue first businesses, in services businesses. @onependragon @br3nnan

@freestylevc led their spin-out $12M funding round, bringing total funding to $17M.

@alexrkonrad at @UpstartsMediaCo shares the news: upstartsmedia.com/p/infinity…

27 May 2025

upstartsmedia.com/p/infinity…

After years of building in the shadows, I’m thrilled to share @_InfinityConst's emergence from stealth today.

Born from some of the most ambitious ideas within @InvTechInc, Infinity is the first AI-native HoldCo.

Already with 8 startups generating $7M in annualized revenue, we just raised a $12M seed round led by @mariabrw at @freestylevc, along with @BackedVC, @deepwatermgmt, BY Venture Partners, and leading angels. This round follows $5M in pre-seed capital invested by Invisible in 2023 & 2024.

Many thanks to @br3nnan, Charlie Songhurst, @scottdownes, and so many others who helped make this a reality.

Software was a technology, subscriptions became its business model. AI is a technology, what is the natural business model of AI? We believe both Enterprise SaaS & traditional Enterprise Services will be disrupted by a new business model: AI Process Platforms - pioneered by Invisible Technologies, Palantir Technologies & ServiceNow.

The legendary @alexrkonrad of @UpstartsMediaCo breaks the news:

3

4

15

1,451

Freestyle Capital retweeted

22 May 2025

The iPhone of AI is coming.

In today’s episode of Venture Daily:

– OpenAI raises $11.6B for their AI data center

– Trump’s $175B “golden dome”

- OpenAI's $6.5B acquisition of Jony Ive's AI device startup

Thanks to @mariabrw (@freestylevc) for joining us!

Watch now.

1

1

263

18 Apr 2025

“The fear of somebody else winning your market has never been higher than it is now. You haven’t seen a slowdown because the rate of change on the technology side is almost indigestible.” - @mariabrw pitchbook.com/news/articles/…

3

2

192

Freestyle Capital retweeted

3 Apr 2025

As ChatGPT, Grok, Gemini & other LLMs expand features: What subscriptions are you canceling? Midjourney & Lensa were great, but ChatGPT’s image gen now competes. Perplexity’s “Google-like” search was fresh, yet Gemini catches up. What AI tools are you dropping today? Share below! #AI #TechTrends

1

4

284

Freestyle Capital retweeted

2 Apr 2025

When Machines Pay Machines: The Era of Agentic Payments Has Arrived

Agents aren't just coming - they're already here. Yet, their full potential won't materialize unless they can autonomously transact and handle money seamlessly. This isn't entirely new - think about the frictionless payment experience of Uber, where transactions invisibly settle behind the scenes. However, extending this model to fully autonomous AI agents introduces unprecedented complexity and scale.

Why Current Infrastructure Isn't Ready

Two major blockers stand in the way of scaling agentic payments: identity authentication and the inherent probabilistic nature of AI decision-making.

From Bad Bots to Good Bots

Historically, 99.9% of bot traffic has been malicious, designed explicitly for fraud and exploitation. Existing financial infrastructure is consequently optimized to combat bad bots, not embrace good ones. But AI agents flip this narrative. As headless browsers and automated agents proliferate, traditional authentication methods break down. Every time an AI developer describes their "headless browser," bank fraud teams cringe. How do we distinguish legitimate autonomous agents from malicious bots, especially when the agents themselves multiply exponentially and operate at superhuman speeds?

Traditional identity verification, KYC, and fraud detection processes were designed for human-led transactions, not agents operating independently. Who exactly are we authenticating - the developer, the AI model itself, or the ultimate beneficiary? Today's frameworks offer few answers.

Probabilistic vs. Deterministic Payments

AI operates on probabilistic reasoning to get outputs, where "close enough" often suffices. Yet payments demand absolute precision. A model hallucinating text might be harmless; hallucinating transaction details - a quantity, a decimal, a recipient - is catastrophic. Imagine your agent mistakenly orders one million units instead of one. Probabilistic errors in financial contexts simply aren't permissible, yet current payment rails lack robust verification mechanisms capable of interpreting and correcting probabilistic decision-making.

Unprecedented Scale & Frequency, and Variable Pricing

The human brain struggles to grasp exponential growth. Autonomous agents don't sleep - they operate in parallel, instantly spinning up infinite workflows, transactions, and interactions. Consider startups running thousands of autonomous MVP experiments simultaneously to optimize product-market fit, or personal agents autonomously negotiating purchases, services, and contracts around the clock.

This isn't incremental change - it's an order-of-magnitude leap. The traditional financial rails - FedACH, Visa, Mastercard - weren't built for instantaneous, 24/7, infinite scalability. Yet AI-driven commerce demands precisely this.

New infrastructure will likely be required, as it's important to move information alongside money - especially because the cost of completing a task can vary. For example, if you ask an agent to book a flight, the price is known in real time. But if a chain of agents is executing a workflow, costs can fluctuate based on which LLM is used, which freelance agent is hired, and other factors. Take the simple task of generating a logo - you'd want to confirm that the work has been delivered and meets expectations before releasing payment from one agent to the next.

What Should Agentic Payments Infrastructure Look Like?

The future payments system for agents will definitely run on traditional fiat rails for regulatory compliance, and may also include crypto elements such as programmable smart contracts and stablecoins. Ideally, these transactions should:

• Validate and verify completion of tasks autonomously before releasing payment, much like smart contracts today.

• Enable instant, secure, compliant microtransactions at unprecedented scale.

• Seamlessly handle variability in operational costs - such as dynamically priced compute resources or API calls from various AI models.

• Have a way to handle liability that is baked into each step (as it is today in the current financial system) so it's clear who is responsible for a charge-back, return etc

Who's Already Building?

This market barely existed 12 months ago but is now bustling with innovation. Here's how the early movers are shaping it:

• @AtumLabs : Building a blockchain-based Visa-like network on Solana and Base for open agentic commerce.

• @crossmint : A crypto platform for people to build onchain, including agents

• @fewsats (Lightning Network): Leveraging Bitcoin's Lightning Network and the internet's original HTTP 402 payment protocol to facilitate microtransactions.

• @Nevermined_io : Creating decentralized AI-native payment protocols tailored explicitly for autonomous workflows.

• @PaymanAI *: AI compliant bank accounts and infrastructure - recently executed the first real, compliant autonomous bank transaction initiated by an AI agent.

• @trySkyfire : Former Ripple team reimagining the financial stack for an AI-first economy.

People are also leveraging old financial infrastructure in new ways. I spoke to a stealth company that was leveraging traditional financial proxies for agent payments.

Why Won't @stripe Just Own This?

Yes, Stripe is a payments powerhouse with deep pockets. I mean - Stripe is worth $90 Billion dollars and is capable of going after what they want, but agentic payments pose significant risks. The cost of prematurely enabling autonomous agents without solving authentication, fraud, and liability concerns is immense. Stripe's cautious moves into agentic payments - mainly through partnerships and virtual cards - highlight the risks inherent in rushing forward, and they have much more to lose if things go wrong on the regulatory front. Plus most of Stripe's true advantage is on the merchant side which doesn't necessarily translate here. Early startups can innovate faster and take more targeted bets without existential risk to legacy systems.

A Glimpse Into the Near Future

The coming era of agentic payments remains somewhat hazy, so here is blurry ball of predictions versus a crystal one:

•Hybrid & New Infrastructure: Whether it's existing FIAT or crypto infrastructure or a patchwork quilt of both, the rails and at least the concepts exist today to build this the way it should be built.

•New Merchant Interfaces: Websites may have dedicated checkout gateways designed explicitly for agent interaction, separate from human-facing systems.

•Fraud & Liability Reimagined: Teams ignoring fraud prevention, consumer protection, and clear liability definitions will fail spectacularly. Those proactively embedding these considerations will thrive.

•Humans to Automation: Short-term solutions will keep humans in the approval loop, but complete autonomy will rapidly become the norm. Agents will autonomously transact, settle, and reconcile transactions at a scale never before seen.

One thing is crystal clear - what wins will be the team that can get compliant, fast payments into the hands of as many developers as quickly as possible as they build out agents (ultimately getting it into the hands of businesses and consumer).

The Opportunity is Now

We're in the opening innings of an enormous transformation. AI, fintech, and crypto founders who move fast to solve these challenges will unlock vast new categories of commerce and reshape global financial infrastructure. VCs who back the right teams today will fund the financial backbone of tomorrow's autonomous economy.

If you're building, innovating, or investing in this explosive new frontier, we'd love to connect, exchange ideas, and chart the future together.

The agentic payments revolution has begun. The only question now: who's going to win the race?

* Disclosure - I'm an investor in Payman

2

8

442

Freestyle Capital retweeted

1 Apr 2025

When agents transact, everything changes. How we go from bad bots to good bots and why today's financial systems aren't set up for agentic payments today - More on that here - medium.com/p/when-machines-p… and shout out to @PaymanAI @AtumLabs @crossmint @fewsats @Nevermined_io @trySkyfire

7

7

30

4,731

Freestyle Capital retweeted

25 Mar 2025

Blinders Off! Why Founders Need Peripheral Vision to Build in the Age of AI

There was a time — not that long ago — when a founder could slap on blinders, keep their head down, and just build. Craft a great product, hire their team, find customers and product-market fit, and grow revenue. The classic playbook.

But that path is dead.

2

3

24

3,544

Freestyle Capital retweeted

28 Jan 2025

So freaking exciting!!! First real bank transaction made by an AI agent - HISTORY in the making!! @0xTyllen @PaymanAI @HF0Residency

There’s a unique feeling you get when you experience the future happening. This is a glimpse of what that looks like. The hype is too strong!

1

2

8

1,311

Gemini 2.0 launched today. Amazing multimodal capabilities, long context windows, fast response times, built-in tools, and top-of-the-leaderboards reasoning capabilities.

Plus a new API — the Multimodal Live API — for conversational AI applications, like voice agents and multimodal copilots.

@Google and Daily have partnered to build Multimodal Live API support into the @pipecat_ai Open Source SDKs for Web, Android, iOS and C .

The Pipecat SDKs come with echo cancellation and noise reduction, device management, event abstractions, React hooks, and more. They support both direct connections to the Gemini WebSocket API, and WebRTC routing on Daily's global ultra-low latency network.

Build realtime voice agents with Gemini, Pipecat, and Daily.

Links to docs and starter kits in the thread below (1/4)...

4

11

38

18,991

24 Oct 2024

Thrilled to announce we are leading the $6.5M seed round for Dash Bio - a new robotics startup helping to get miracle drugs to market cheaper and faster! 🧪💊wsj.com/articles/moderna-alu…

3

162

8 Oct 2024

100 is a proptech platform disrupting multifamily's rental and screening process with a tech-driven approach that makes renting easy, bias-free, and secure. Freestyle Capital is thrilled to support their vision alongside @MetaPropNYC @ContestPoint & more!! 🙌🥂🎉commercialobserver.com/2024/…

4

156

Freestyle Capital retweeted

21 May 2024

Who are we? Let us tell you.

HiveWatch is making it easier for companies to keep their people, assets, and brands safe. Learn more: hubs.ly/Q02xjp4x0

#aboutus #HiveWatch #intro

1

3

275

Freestyle Capital retweeted

8 May 2024

Mother's Day is just around the corner, and we're celebrating with a special sale! Treat the amazing moms in your life to something they'll love. Hurry, these deals won't last long! 💐💛

2

5

420

6 May 2024

Huge congrats to @jennylefcourt , in good company with @aileenlee @aunder & @kirstenagreen among others, all named to Business Insider's Top 40 Early Stage Women Investors List of 2024. What and amazing group of VC's. Congrats ladies!! 👏 👏 👏

businessinsider.com/seed-40-…

4

195

6 May 2024

It's deja vu all over again... Congrats to @jennylefcourt for being named to the

@BusinessInsider #Seed100: The best early-stage investors of 2024 list! businessinsider.com/seed-100…

1

1

3

505

24 Jan 2024

It's not all bad news! Seed investing has turned out to be one of the most vibrant funding stages though last year's downturn. See what this means for 2024 and check out what @jennylefcourt @rquintini & @MGCardamone have to say about it. Thanks to @geneteare of @crunchbasenews for this piece! news.crunchbase.com/seed/us-…

1

3

306

7 Dec 2023

“The more money people got before the party ended, the longer the hangover.” -@jennylefcourt

Read the full story The New York Times article here:

nytimes.com/2023/12/07/techn…

1

1

188