85 Photos and videos

10h

Japan just made Bitcoin a financial instrument.

Metaplanet is now licensed (after acquisition closes) to distribute bitcoin-related financial instruments.

-bitcoin-backed bonds

-JPYC/BTC settlement layer

-bitcoin-backed preferred equities

-tokenized bitcoin-backed securities

In other words, Metaplanet is now a licensed manufacturer and distributor of bitcoin related financial instruments in the third largest economy on earth.

They just became the first regulated bitcoin securities platform in Japan.

It’s stunning work.

June 11: Japan’s lower house passes bill moving crypto from payments law to financial-product rules, effective within a year.

June 12: Metaplanet acquires 100% of Siiibo Securities, adding a regulated Type I securities platform to build and distribute BTC-linked yield products.

5

11

137

8,887

Jun 12

Distribution. For anyone scratching their head on this, study the history of Uridashi bonds in Japan.

Metaplanet is building an Uridashi-like distribution channel for bitcoin yield products.

This also provides Metaplanet with a Type 1 securities license - highest level available.

Nomura of Bitcoin.

Very Bullish.

Jun 12

We are pleased to announce that Metaplanet has entered into an agreement to acquire 100% of Siiibo Securities, a licensed Type I securities firm and a pioneer of Japan's online corporate bond market. Following closing, expected in July, the company will be renamed Metaplanet Securities. This is Metaplanet's first major acquisition and the first concrete step in Project Nova, our long-term strategy to build a Bitcoin-centric financial ecosystem in Japan.

The significance is hard to overstate. Japanese households hold roughly $7.4 trillion in cash, deposits and low-yield products, and as Japan shifts from deflation to inflation, that capital has begun searching for yield. By bringing Siiibo's Type I registration and online securities platform into the group, we will develop and distribute Bitcoin-related yield products directly to Japanese investors, supported by the 40,177 BTC on our balance sheet, the largest corporate Bitcoin treasury in Asia.

We have great respect for Kazuki Komura and the team at Siiibo Securities and what they have built. Together, as Metaplanet Securities, we will bring new yield opportunities to Japan.

6

12

158

29,554

Jun 9

It’s a good day to post this.

Conflict Theory was architected by Karl Marx.

When Marxism failed, the Germans picked it up & tried again.

They called it Critical Theory, but it was Marxism.

Working off Critical Theory and inspired by the Civil Rights Movement of the 1960s, Marxist legal scholars & professors invented Critical Legal Studies.

And Critical Legal Studies is the father of Critical Race Theory.

From there we get Intersectionality, which is another Marxist cancer.

It’s all Marxism. Which is to say, it’s all communism.

Anytime you hear or see the word “Critical” you should replace it with “Communist.”

spacrs.wordpress.com/what-is…

1

130

bitcoin retweeted

May 25

A lot of pieces are being put in place right now at Metaplanet. Individually, none of them tell the full story. Together, they will. We are working harder than at any point I can remember to get them right. I wish I could share more. Soon enough, the picture will speak for itself. We are building this company for the long term, and for every shareholder who is along for that journey.

いまメタプラネットでは、様々な取り組みが少しずつ形になりつつあります。個別に見ても、全体像は見えてきません。すべてが揃ったとき、初めて意味を持ちます。私たちは、これまでにないほど真剣に、その一つひとつに向き合っています。今はまだ多くを語れないのが歯がゆいですが、時が来れば、自ずと見えてくるはずです。私たちはこの会社を長期視点で築いています。そして、その歩みを共にしてくださるすべての株主の皆様と共に。

468

274

2,523

567,826

May 18

Spencer Pratt has leveraged the gaslit gibberish of the left impeccably - he's painted the left as the corrupt idiots they truly are with their own words.

He'll probably lose the election, which is the measure of CA itself. But what an impressively effective campaign.

May 18

Now this is a story all about how my life got flipped, turned upside down

2

185

May 16

Incredible

May 16

We're so back.

An entrepreneur is restoring Pizza Huts to their former glory.

2

230

May 15

Double the money supply. Good. Double it again. Get Kevin O’Leary to tell everyone they’re not liquid unless they have $5M in treasuries. Now send the 10 year to 4.5%.

1

113

bitcoin retweeted

May 15

He’s finally locked in on his sleep, diet, and exercise. Have his kids bring home a flu from school that’s going to wreck him for 10 days

35

237

6,723

201,703

May 13

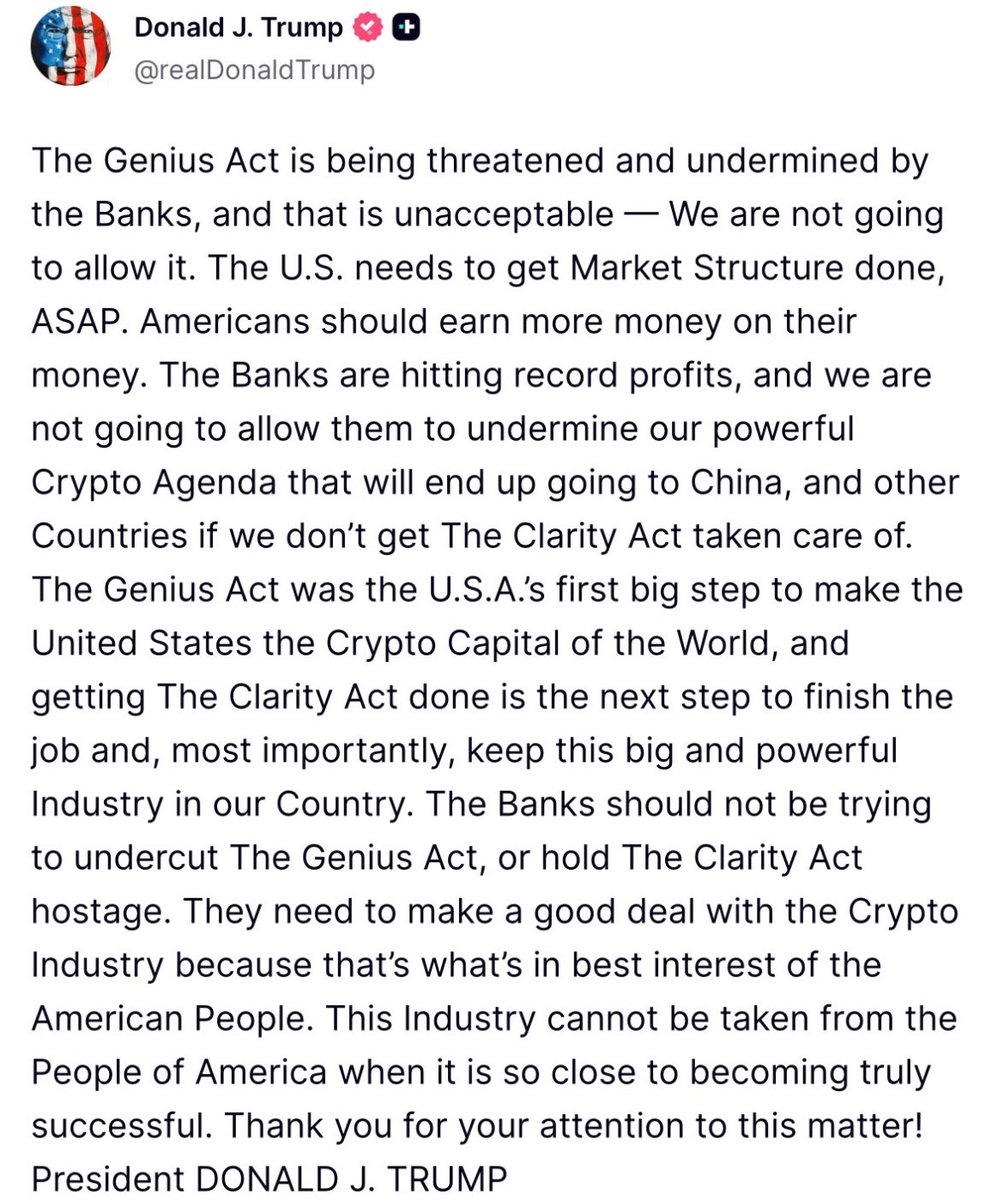

My take:

1) Gensler-like regulatory slow play on behalf of incumbent power (bankers mostly). Imagine what 5-6% does to legacy players. Of course there’s pushback.

2) Nobody can stop bitcoin or the instruments being formed around corporations that hold large amounts of bitcoin - global markets being global.

3) MTPLF/MPJPY remains the best - potential - asymmetric bet long-term.

4) Building a cash machine into a BTC treasury co. will be massively different than any other treasury co if you can see the long-term market structure.

5) Prefs will come. Japanese investors just might not be the first to benefit from MP’s prefs though.

May 13

There is a limited universe of listed preferred shares in Japan today. Upon listing, our preferred would be only the seventh in the market, and the first perpetual preferred. We view this as a meaningful contribution to the development of Japan's capital markets, but it is also why the path to listing is necessarily deliberate.

In the Japanese market, dividends on preferred shares are expected to be supported by sustainable cash flows generated from underlying operations. The listing review accordingly assesses dividend-paying capacity based on projected financial performance over a multi-year period, including scenarios across different market environments. Metaplanet already has a six-quarter track record in its Bitcoin Income Generation Business, and we believe it is important to continue demonstrating that the business can generate stable, recurring cash flows across both strong and weak Bitcoin market conditions. We are also continuing to articulate the scalability and long-term viability of our related operating businesses that support this cash flow profile.

A second consideration is dividend operations. Listed companies in Japan have historically paid dividends once or twice per year. The structure we are designing contemplates more frequent distributions, including monthly dividends. Implementing this requires careful work on record-date procedures, shareholder identification, dividend calculation, and recurring shareholder notice operations. We are working closely with our partners to build and modernize this infrastructure in a manner consistent with Japanese regulatory and market practice.

The process has taken longer than we initially anticipated, and we appreciate that this has created uncertainty. We are deliberate about this work because Japan today is one of the most yield-starved major capital markets in the world, and we believe a preferred equity product supported by credible operating cash flows, robust operational infrastructure, and a long-term growth strategy can meaningfully address that need. We are deeply committed to bringing this product to market, and to doing so in a form that earns the long-term trust of investors and market participants.

1

2

46

2,343

May 12

He still doesn’t get it.

While Bitcoin gets a lot of attention, it hasn’t played the safe-haven role many expected. In my view, there are a few reasons why.

First, Bitcoin lacks privacy. Transactions can be monitored and potentially controlled, which is why central banks aren’t looking to hold it.

Second, it also has a high correlation with tech stocks. When investors get squeezed in other areas of their portfolio, they sell their Bitcoin to cover it.

Third, it’s a relatively small and controllable market, whereas gold stands alone. There is only one gold.

Ultimately, gold is more widely held, deeply established, and still plays a central role in the global system.

2

229

bitcoin retweeted

The year is 2030. It’s Friday, May 10th, and Bitcoin is trading at $746K. This comes after a brutal five-month drawdown since it topped at $1,047,255 in December 2029. Skeptics on X are calling for $500K, and the WSJ just ran a piece on Michael Saylor titled “Michael Saylor’s Bitcoin Bet Just Lost $500 Billion. He’s Still Buying.”

Over in Japan, #Metaplanet’s share price corrected to 1.3x EV mNAV, and their market cap is trading 5% below the value of their Bitcoin holdings. Last month they closed with a stack of 451,200 BTC, worth $336.5B — 2.15% of every coin that will ever exist. Management expects to cross 500K BTC by the end of the year.

On the macro front, the yen had depreciated to ¥220 per dollar by late 2028, on the back of Takaichi winning her second LDP presidency that October — Abenomics 2.0, but this time with conviction and a mandate. The BOJ trilemma (pick two: stability, yield, or currency) resolved through the currency, which is the path her government had been walking deliberately since she came in.

For years now, Metaplanet has been running the largest and most sophisticated Bitcoin options desk in the world, monetizing volatility through their BIG business line. In FY2029, BIG brought in ¥1.3 trillion ($5.7 billion) in premiums, a ~1.7% return on their total Bitcoin holdings.

Project Nova — rebranded as Metaplanet Financial Services in 2027 ahead of the Bitcoin ETF launches — pulled in ¥420 billion ($1.9B at ¥220/USD) in recurring revenue in FY2029. Metaplanet stopped being a treasury company somewhere around 2028 and transformed into a financial conglomerate with the treasury at its core.

All that recurring income exists for one reason: to service the preferred stock book.

The math is simple. At a blended dividend rate ~5%, every $1 of recurring income covers dividends on $20 of preferred issuance. Income leverages 20x into preferred capacity, which is then used to buy more Bitcoin.

MARS, the Class A senior preferred Metaplanet announced in late 2025, was designed straight off Strategy’s $STRC playbook. Adjustable monthly dividend with no conversion/dilution to common. Built specifically for Japanese institutional capital that needed a yen-alternative short duration product, which the BOJ kept making more pressing every year.

MARS listed on the TSE late 2026 and has since scaled to ¥10 trillion ($45B) outstanding. MERCURY, the junior Class B convertible, converted into common in late 2027 during the post-halving rally — the instrument retired itself, exactly as designed.

Since then, Metaplanet has further built out the Bitcoin yield curve in Japan, launching JUPITER and SATURN with combined total assets of ¥4T ($18B). The company’s amplification ratio sits at 35% following the Bitcoin price drawdown, up from 25% at the cycle peak.

With operating income running at a ~70% margin, in FY2029 Metaplanet brought in ¥1.2T ($5.4B), covering preferred dividends at about 1.7x.

One structural decision in 2027 made all of this possible at scale. Metaplanet’s TSE listing graduated from Standard to Prime that fall, and TOPIX index inclusion followed shortly after.

Suddenly Metaplanet sat in every passive index fund tracking Japanese equities. And today, around 1.5 million Japanese retail shareholders hold the stock, up from 220,000 in 2026. Nippon Life, Dai-ichi Life, and Tokio Marine all anchor the MARS preferred book.

Meanwhile on X, @gerovich posted “Morning Planet!” at 6:47am Tokyo time. And @DylanLeClair retweeted a daily Bitcoin chart with the caption: still bullish.

Financial stats:

•Market cap: ~$320 billion (¥70T at ¥220/USD)

•FD share count: ~3.0 billion

•Sats per diluted share: ~15,000

•Metaplanet share price: $125 (¥27,500)

$MPJPY $MTPLF

16

26

210

16,151

May 8

Where Simon & Team's US roadshow fits in the $MTPLF timeline. My best guess.

Nov 20, 2025 - Board approves two-tier preferred structure: MARS and MERCURY. $150M MERCURY private placement announced. Keep in mind, they have 1 year to IPO MERCURY. Clock's ticking.

Dec 2025 (Bitcoin MENA) - Simon calls MERCURY "pre-IPO," targeting early 2026 listing. Confirms MARS is Metaplanet's answer to Strategy's STRC.

Dec 22, 2025 - EGM. All five proposals pass. Authorized Class A (MARS) and Class B (MERCURY) shares doubled to 555M each. Capital stock and reserves restructured into capital surplus, expanding the legal pool for preferred dividends and buybacks. ADR program (MPJPY) launched for US access.

All that sets the stage for this week.

Metaplanet's team is on a week-long US investor roadshow. Flexing in Boston, tweeting publicly...which is interesting.

A formal roadshow shuts all that down. This is a non-deal roadshow / pre-marketing tour, building the US institutional book potentially across all three instruments. No clue which one will come into focus as the next big capital raise vehicle.

Common: US demand feeds directly into that program, but I don't think this is viable at current mNAV. Need to get it to 1.01x on the 27th series.

MARS: fully authorized and ready to issue. Recent success of STRC makes this a LFG potential, but I'm hesitant to let STRC recency bias overtake me here. I'm rooting for it, but US investors I'd assume look more towards MERCURY.

MERCURY: pre-TSE listing, with a 1-year IPO clock embedded in the Q4 2025 placement. Targets the hybrid fixed-income equity-upside buyer. This is my bet for the current roadshow. Why? STRK never had a prayer at hitting the $1000/sh strike price IMO on any reasonable timeframe. Like so many things, Simon and team learn from MSTR errors and improve on them. MERCURY is the best bitcoin-backed call option in the world right now. I would buy this with both hands if I was an institutional investor with a mandate.

Formal roadshows are typically a grueling 7-10 business days before pricing. Not where we're at today. I worked for the COO of a fund during this exact timeline before the fund IPO'd, and I thought he was going to drop dead. There's no time to pose in front of Paul Revere.

(I do appreciate the symbolism of the MTPLF team posing in front of a statue that symbolizes revolution. Nice touch.)

NDRs like this are ballpark 2-12 weeks before a deal, and I'd guess more like 8-10. Happy if it happens sooner. Would be thrilled if it's MERCURY.

When Dylan stops tweeting sweet new headshots of himself, and the signal-sending-tourism photos disappear, I'll be paying attention.

3

2

10

321

May 6

The Tokyo Stock Exchange closed April 30th at 1am CST.

Bitcoin was at $76,305.

I know it's not much, but a bit of pain to $MTPLF short sellers is nice to contemplate.

6

195

May 5

Has anyone checked in on Willy Woo?

12 YR TREND BROKEN.

BTC should be a valued a LOT HIGHER relative to gold.

Should be. IT'S NOT.

The valuation trend broke down once QUANTUM came into awareness.

Don't read this post if you want to stay high on hopium instead of seeing things as they are.

3

160

bitcoin retweeted

May 4

$MTPLF “Bread crumbs”. MARS coming sooner than later. 🚀

May 4

The first wave of Bitcoin-backed fixed income has shown the demand is real. The global opportunity is many multiples larger. Japan is a particularly compelling case. Japanese households hold roughly $7 trillion in cash and deposits earning nothing. Decades of zero-yield conditioning, a generation of conservative savers, and a regulatory framework that increasingly accommodates digital assets. The fit is hard to ignore.

9

10

224

15,574

May 1

Liberals out-liberaling themselves here. Fantastic stuff.

May 1

KOMO reporter Chris Daniels asked the Seattle socialist mayor if she had changed her views on banning security cameras around the city, a demand of leftists, after experiencing a shooting near an event she was at. Her staff then shut down the interview.

72

bitcoin retweeted

Apr 29

Bank of Japan (BOJ) Policy Decision: The BOJ maintained its policy rate guideline at ~0.75% (as of April 28, 2026).

The decision passed by a 6–3 vote, the widest split under Governor Kazuo Ueda’s tenure. Three board members dissented, advocating an immediate interest rate hike to ~1.0%, a classic hawkish halt where policy remains unchanged, but the dissents signal more and longer restrictive measures.

The BOJ also revised its inflation projections higher: core CPI for FY2026 was raised significantly to 2.8% from ~1.9%, while the growth outlook was trimmed amid external uncertainties.

Key market implications:

- Upward pressure on short-end yields as markets pull forward, tightening. A steeper JGB curve is expected.

- Expect more yen volatility

- Reduced appeal of yen-funded carry trades with spillover into broader rate differentials.

1

4

20

5,419