🏭 Dubai Industrial City unveils MetaFab Labs! Pioneering advanced material synthetics for future industries, propelling UAE's manufacturing innovation. #DubaiFuture #AdvancedMaterials #IndustrialInnovation

🔗

🔗 dubai-lens-daily.lovable.app…

5

Jun 13

Solar innovation may be shifting from efficiency to manufacturability.

For years, much of the solar industry has focused on improving cell performance.

But a new collaboration between Henkel and Brilliant Matters highlights a different challenge: scaling next-generation solar technologies from promising prototypes to commercially viable products.

Key signals:

• Henkel and Brilliant Matters are developing specialized silver inks for roll-to-roll OPV manufacturing

• The collaboration targets a critical metallization bottleneck in organic photovoltaics

• Brilliant Matters' BM10 OPV platform has demonstrated outputs above 100 W/m²

• The technology has reported operational lifetimes exceeding 25 years

Why this matters:

Organic photovoltaics have long attracted interest because they can be lightweight, flexible, and semi-transparent.

However, manufacturing complexity has limited broader commercialization.

Solving production bottlenecks could accelerate the adoption of solar technologies that integrate into windows, building facades, infrastructure, and other surfaces where conventional panels are difficult to deploy.

What's changing:

From laboratory-scale OPV innovation → to industrial-scale OPV manufacturing

As clean-energy technologies mature, competitive advantage increasingly depends on manufacturing capability rather than performance improvements alone.

This partnership highlights how materials science, process engineering, and industrial scale-up are becoming critical drivers of commercialization.

Could manufacturing breakthroughs become the deciding factor in which next-generation solar technologies achieve widespread adoption?

#SolarEnergy #RenewableEnergy #OrganicPhotovoltaics #CleanTech #EnergyInnovation #AdvancedMaterials #PrintedElectronics #EnergyTransition #FutureOfEnergy #InnoDexis

19

Jun 13

Asset tracking that survives the furnace. 🔥 @CeraTattva builds ceramic traceability labels and markers that endure up to 2,800°C, giving steel, glass and ceramics manufacturers in-process visibility from start to finish. #BharatInnovates #MakeInIndia #AdvancedMaterials

ceratattva.com/

@PMOIndia @MEAIndia @IndianDiplomacy @BharatInnov2026

3

473

Jun 13

Heat may be becoming a programmable technology.

For decades, engineers have mastered the ability to control electrons and photons with extraordinary precision.

Now, researchers from Carnegie Mellon University College of Engineering, in collaboration with Stanford University and Purdue University, have demonstrated a way to dramatically enhance heat transfer at the nanoscale, suggesting thermal energy itself may become an engineered resource rather than a limitation.

Key signals:

• Researchers engineered gold metamaterials to control heat transfer across nanoscale gaps

• Resonance effects accelerated thermal energy transfer through interactions with surface phonon polaritons

• Experiments achieved up to 4× greater heat transfer than comparable conventional systems

• The findings provide strong evidence that heat flow can be intentionally enhanced through nanoscale engineering

Why this matters:

Heat management is becoming one of the defining challenges in semiconductors, advanced computing, and energy technologies.

As processors become smaller, denser, and more powerful, conventional cooling approaches are increasingly struggling to keep pace.

The ability to precisely direct thermal energy could unlock more efficient chip cooling, higher-performance electronic systems, advanced sensing technologies, and improved energy conversion.

What's changing:

From treating heat as an engineering constraint → to designing heat as an engineering resource

For decades, thermal management has largely focused on removing unwanted heat from systems.

This research suggests a different future may be emerging - one where heat is not simply dissipated, but actively directed, optimized, and potentially harnessed to improve performance and efficiency.

Could thermal engineering become as strategically important as semiconductor design in the next generation of computing and energy technologies?

#MaterialsScience #Nanotechnology #Metamaterials #Semiconductors #ThermalEngineering #HeatTransfer #EnergyTechnology #AdvancedMaterials #FutureTech #InnoDexis

19

Jun 13

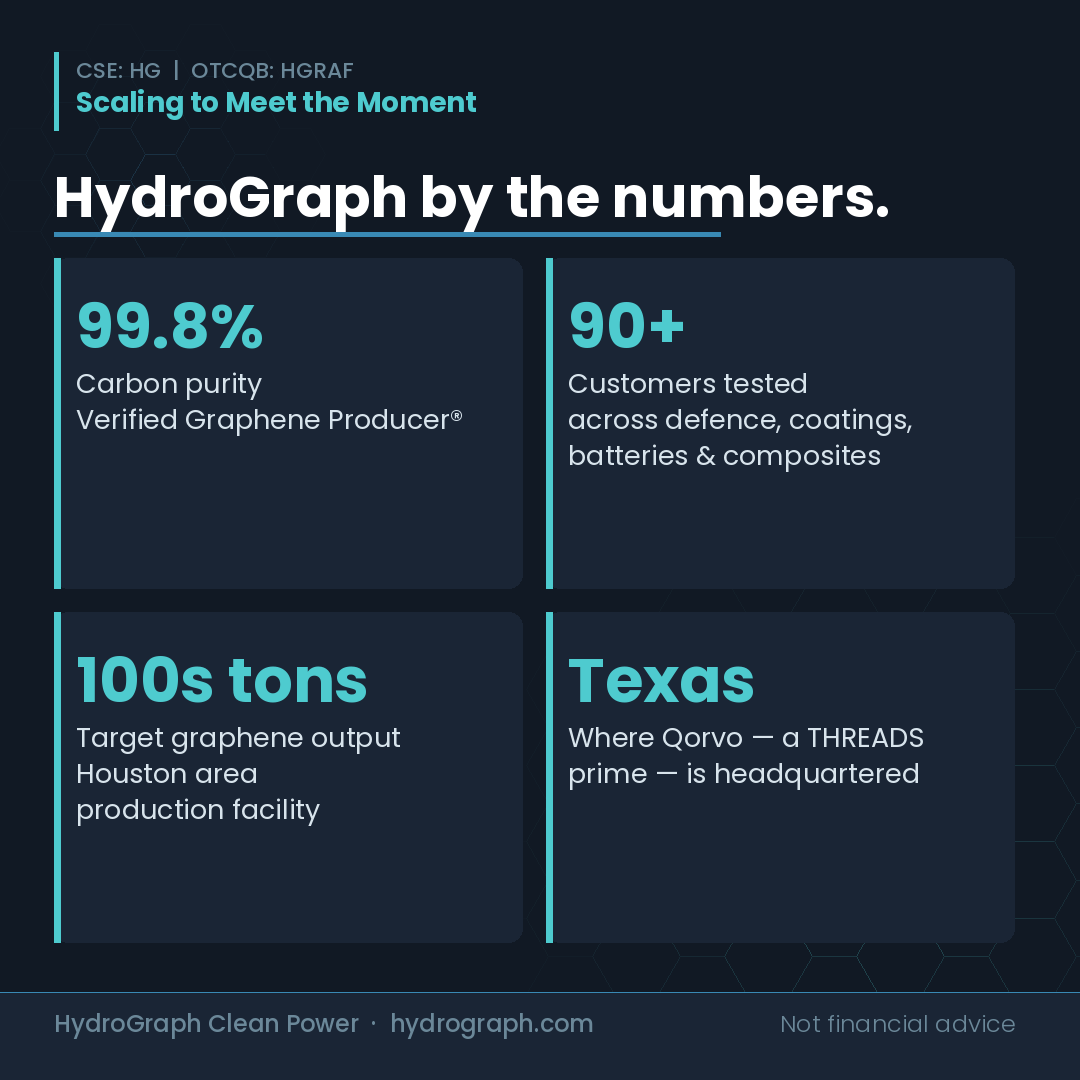

@HydroGraphInc is already scaling.

Two new Hyperion reactors commissioned in early 2026.

A Houston area production facility targeting hundreds of tons of graphene.

Texas. Where @QorvoInc is headquartered. 📍

#CriticalMinerals #AdvancedMaterials #GaN $HGRAF

5

192

Creator Fund Closes $56M Fund to Back Europe’s Next Generation of Scientific Founders

newnex.io/feed/creator-fund-…

#DeepTech #VentureCapital #StartupFunding #ScientificFounders #ArtificialIntelligence #AI #Biotech #Robotics #Semiconductors #AdvancedMaterials #Innovation

10

Great to see growing interest in graphene. At Volt Carbon, we encourage investors to compare the data. All of our work has been developed in-house, from graphite processing, to graphene production, to batteries, composites, and end-use products.

That level of vertical integration is rare in the industry and allows for rapid innovation and deployment of tech. Our publicly available results include third-party verified battery performance, material strengthening, conductivity improvements, and characterization of graphene through Raman, XRD, TEM, and SEM. These analyses provide insight into crystallinity, morphology, graphitic structure, and the preservation of the sp² carbon network. The data is publicly available through our news releases and website for anyone to review, compare, and challenge.

We believe transparency, crystallinity preservation, reproducible performance, and commercial scalability will ultimately determine the winners.

Review the data. Draw your own conclusions.

$VCT $TORVF #Graphene #BatteryMaterials #AdvancedMaterials #Nanotechnology #EnergyStorage

2

129

Kingrande supports stable polymer processing with advanced fluorinated chemistry solutions that improve wetting, dispersion & production consistency.

🌐 kingrande.com

#kingrande #fluorosurfactant #polymerprocessing #advancedmaterials #chemicalengineering #lithiumbattery

7

American Elements delivers advanced materials that power next-generation foam technologies—supporting performance, safety & scalability across industries. Explore more at americanelements.com #FoamExpo #AdvancedMaterials

4

Jun 12

Following the decline in Q1 2026 earnings and a significant compression in gross margins, can the company achieve full-year growth in 2026 through the relocation of its new plant, a recovery in orders, and optimization of its product mix?

Can the structural demand for advanced materials in EVs, grid upgrades, defense, and AI power electronics be translated into stable revenue and improved profitability?

Against the backdrop of recent equity financing and the appointment of a new CFO, how will the company balance dilution and execution risks against growth potential?

CPSH’s Q1 2026 revenue declined year-over-year due to order timing, while gross margin fell significantly due to fixed cost allocation and inventory adjustments, resulting in a shift from profit to loss. However, the company holds a strong order backlog, a $4 million new sealing and packaging order (post-quarter), and a Navy SBIR extension, and plans to relocate to a larger facility in 2026 to boost capacity and efficiency. The company recently completed a $9.6M equity financing round to bolster liquidity. Its stock price experienced significant volatility and rebounded today (June 11, 2026), reflecting its typical characteristics as a highly volatile, low-volume advanced materials/defense-themed stock. Management remains optimistic about growth in the second half of the year, but execution and gross margin recovery are critical.

Financials: Q1 revenue was $7.03M (down 6.7% YoY from $7.5M), gross profit was $0.6M (gross margin 8.6% vs. 16.4%), and net loss was $0.3M (loss of $0.02 per share vs. profit in the prior year). SG&A remained stable.

Operations: Strong order backlog; secured a $4M hermetic packaging order post-quarter; plans to relocate to a new facility to improve efficiency; new CFO Chris Fraser has assumed the role.

Funding: Completed a $9.6M registered direct offering ($8 per share) in late May, raising approximately $9M net for operations and expansion.

Market: Serves multiple growth sectors (EVs, power grids, defense, aerospace); products offer advantages in thermal management, lightweighting, and high reliability. Market cap of approximately $160–170 million, with distinct small-cap, high-beta characteristics.

Strong demand for high-performance thermal management materials driven by the global energy transition (EVs, wind power, HVDC), defense modernization, and 5G/AI power electronics. As a U.S.-based leader in MMC technology, CPSH benefits from policy support (domestic supply chain) and customer loyalty (long-term major clients). If the new plant relocation and order fulfillment proceed smoothly, they could significantly enhance economies of scale and gross margins, driving a growth inflection point in 2026–2027. It is a high-risk, high-return investment targeting the intersection of advanced materials, defense, and new energy.

Short-term target price: $10–$13

Appropriate future sell price (6–18 months): $15–$20

#CPSH

#MetalMatrixComposites

#AdvancedMaterials

#DefenseTech

#PowerElectronics

#HybridTechArmor

#GridInfrastructure

1

146

Come to us with an idea. Leave with a functional device.

Michael Leverentz explains how Royce at Imperial helps researchers and SMEs accelerate innovation through advanced materials facilities and rapid prototyping.

imperial.ac.uk/royce-facilit…

#AdvancedMaterials #MaterialsScience

1

21

Jun 12

Scientists unlock MOF glass design codes to advance next-generation functional glass development verified via atomic characterization and AI simulation

#AdvancedMaterials

#ScientificDiscovery #MaterialsScience #Chemistry #TechBreakthrough #ScientificBreakthrough #NatureChemistry

2

Jun 11

🚀🤖 MEDUSA TECHNOLOGIES: OPTIMUS A7-HX HAZARD PHOENIX 🤖🚀

Straight from the legendary worlds of Aurora-7, Kid Nebula Gold and Aurora Gold unveil the next generation of planetary infrastructure for the 2100s.

Forged with Aurora Gold Ceramic Shields, Kid Nebula Gold Meta-Coatings, Quad Stack AI Intelligence, and adaptive hazard-response systems, the Hazard Phoenix is designed to enter environments too dangerous for humans. 🔥☣️⚡

From megacities and industrial zones to orbital facilities and interplanetary colonies, Medusa Technologies imagines a future where autonomous guardians protect civilization through advanced robotics, resilient materials, and intelligent infrastructure.

🌎 Planetary Safety

🤖 Humanoid Robotics

🔥 Fire & Hazmat Response

⚙️ Advanced Materials

🛰️ Aurora-7 Sensor Networks

🧠 Quad Stack Intelligence

🌌 Infrastructure for the 2100s

Kid Nebula Gold ✨

Aurora Gold ✨

Medusa Technologies ⚙️

The future isn’t being built. It’s being engineered.

#MedusaTechnologies #Aurora7 #KidNebulaGold #AuroraGold #OptimusA7HX #HumanoidRobotics #FutureInfrastructure #AdvancedMaterials #Robotics #ArtificialIntelligence #HazmatResponse #FireTech #Engineering #Innovation #SmartCities #PlanetaryInfrastructure #TechFuture #SciFiEngineering #FutureOfWork #Automation 🚀🤖⚡🌌

52

Jun 11

🚨 China reaches mass production of T1000 carbon fiber, marking a major milestone in the global race for advanced materials.

The ultra-high-strength material is critical for aerospace, defense, energy, and next-generation industrial applications.

#CarbonFiber #AdvancedMaterials #Aerospace #Manufacturing #Technology #Innovation

1

14

Jun 11

𝐇𝐨𝐧'𝐛𝐥𝐞 𝐃𝐫. 𝐉𝐢𝐭𝐞𝐧𝐝𝐫𝐚 𝐒𝐢𝐧𝐠𝐡, Union Minister (Independent Charge) for Science & Technology, inaugurated the 𝐂𝐞𝐧𝐭𝐫𝐚𝐥 𝐈𝐧𝐬𝐭𝐫𝐮𝐦𝐞𝐧𝐭𝐚𝐭𝐢𝐨𝐧 𝐅𝐚𝐜𝐢𝐥𝐢𝐭𝐲 (𝐂𝐈𝐅)

@iitgn

#ResearchClusters #AdvancedMaterials #HealthcareInnovation #ViksitBharat

33

Jun 11

𝐇𝐨𝐧'𝐛𝐥𝐞 𝐃𝐫. 𝐉𝐢𝐭𝐞𝐧𝐝𝐫𝐚 𝐒𝐢𝐧𝐠𝐡, Union Minister inaugurated the 𝐂𝐞𝐧𝐭𝐫𝐚𝐥 𝐈𝐧𝐬𝐭𝐫𝐮𝐦𝐞𝐧𝐭𝐚𝐭𝐢𝐨𝐧 𝐅𝐚𝐜𝐢𝐥𝐢𝐭𝐲 (𝐂𝐈𝐅) @iitgn Gandhinagar

#ResearchClusters #CIF #AIInnovation #AdvancedMaterials #HealthcareInnovation #EnergyResearch #ViksitBharat

23

Jun 11

𝐀𝐝𝐯𝐚𝐧𝐜𝐢𝐧𝐠 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡 & 𝐈𝐧𝐧𝐨𝐯𝐚𝐭𝐢𝐨𝐧 𝐓𝐨𝐰𝐚𝐫𝐝𝐬 𝐕𝐢𝐤𝐬𝐢𝐭 𝐁𝐡𝐚𝐫𝐚𝐭

IITGN welcomed 𝐇𝐨𝐧'𝐛𝐥𝐞 𝐃𝐫 𝐉𝐢𝐭𝐞𝐧𝐝𝐫𝐚 𝐒𝐢𝐧𝐠𝐡, Union Minister of State (Independent Charge), Ministry of Science & Technology and Ministry of Earth Sciences, Government of India, who inaugurated the 𝐂𝐞𝐧𝐭𝐫𝐚𝐥 𝐈𝐧𝐬𝐭𝐫𝐮𝐦𝐞𝐧𝐭𝐚𝐭𝐢𝐨𝐧 𝐅𝐚𝐜𝐢𝐥𝐢𝐭𝐲 (𝐂𝐈𝐅) and launched three interdisciplinary Research Clusters in 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐝 𝐌𝐚𝐭𝐞𝐫𝐢𝐚𝐥𝐬, 𝐄𝐧𝐞𝐫𝐠𝐲, 𝐚𝐧𝐝 𝐇𝐞𝐚𝐥𝐭𝐡𝐜𝐚𝐫𝐞 & 𝐌𝐞𝐝𝐓𝐞𝐜𝐡.

The visit also featured the introduction of the 𝐂𝐞𝐧𝐭𝐫𝐞 𝐟𝐨𝐫 𝐀𝐈-𝐃𝐫𝐢𝐯𝐞𝐧 𝐈𝐧𝐧𝐨𝐯𝐚𝐭𝐢𝐨𝐧, further strengthening IITGN’s commitment to translational research, industry collaboration, and innovation-driven solutions aligned with the vision of 𝐕𝐢𝐤𝐬𝐢𝐭 𝐁𝐡𝐚𝐫𝐚𝐭 𝟐𝟎𝟒𝟕.

#IITGN #ResearchAtIITGN #Innovation #ResearchClusters #CIF #AIInnovation #AdvancedMaterials #HealthcareInnovation #EnergyResearch #ViksitBharat

2

9

282

Jun 11

Engineered for performance and built for purpose!

Technical textiles are transforming industries with advanced durability, enhanced protection and innovative functionality. At #BharatTex2026, discover how these high-performance materials are driving innovation and shaping the future across sectors.

📍 Bharat Mandapam, New Delhi

📅 14-17 July 2026

Register now: bharat-tex.com

@TexMinIndia @girirajsinghbjp @PmargheritaBJP @aepcindia @TexprocilIndia @Matexil_Srtepc @csbmot @pdexcil @HEPC_India @IndiaExpoCentre @epchindia @wwepcindia1 @cepcindia @jpdepc2019 @ISEPC1

#TechTextiles #EngineeredForPerformance #InnovationDriven #AdvancedMaterials

13

12

402

Jun 11

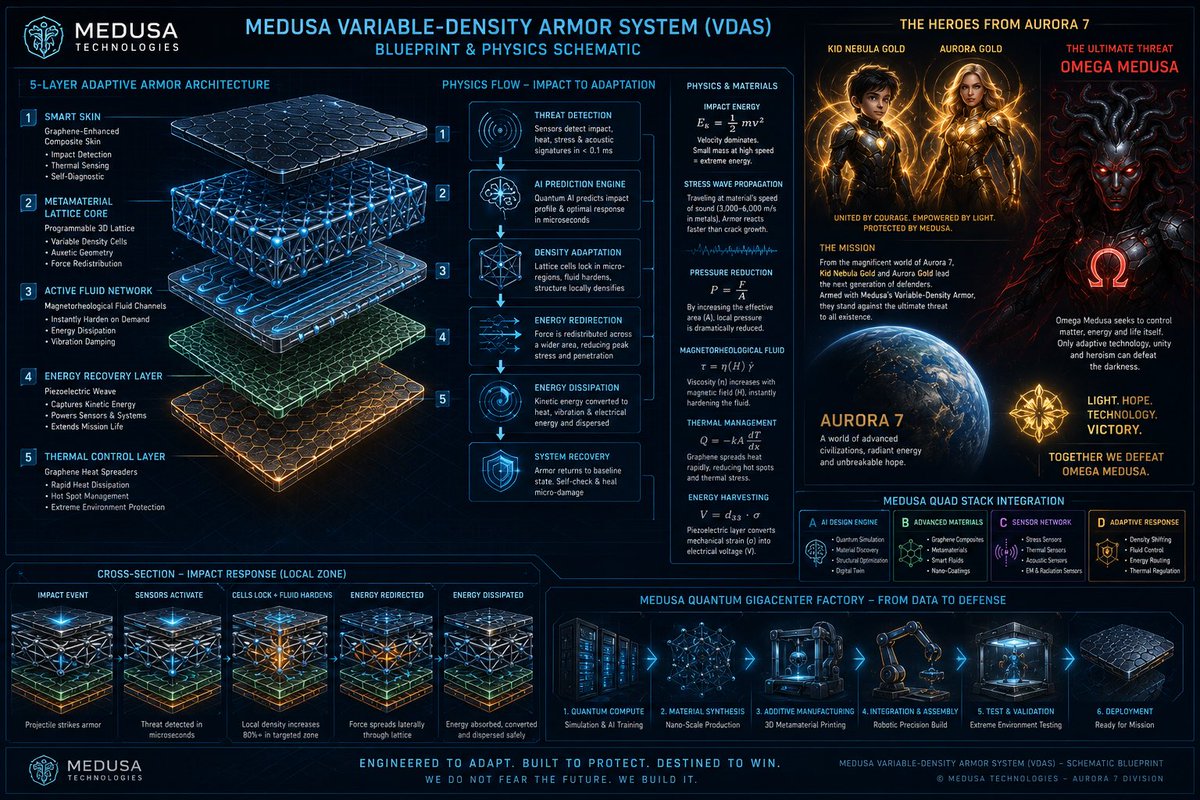

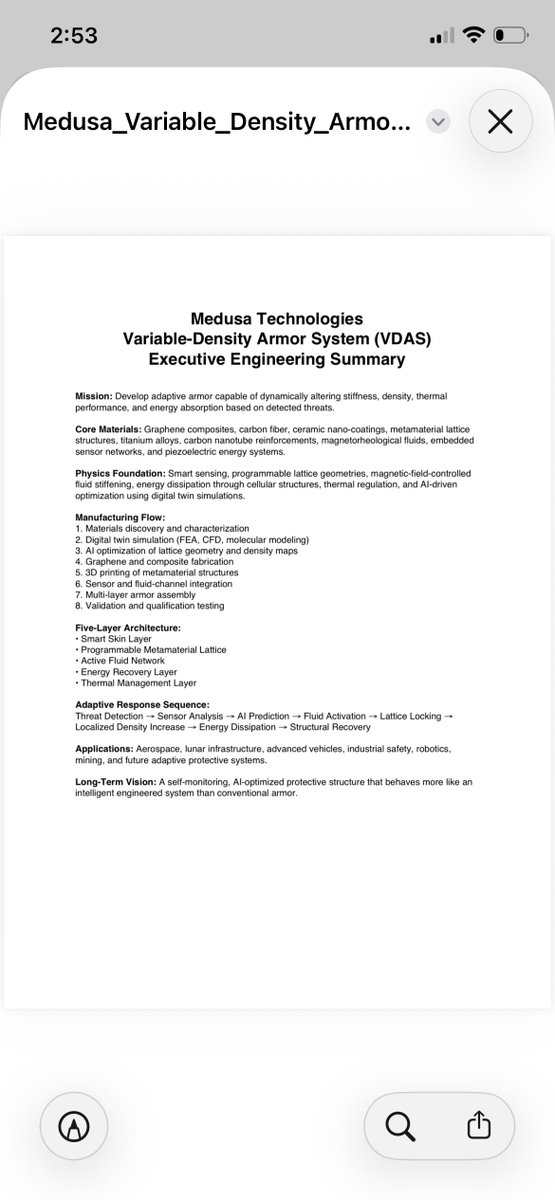

🛡️⚡ MEDUSA VARIABLE-DENSITY ARMOR SYSTEM (VDAS) ⚡🛡️

From the advanced world of Aurora 7 comes a new generation of adaptive protection technology.

Powered by the Medusa Quantum Gigacenter, the Variable-Density Armor System dynamically senses threats, redirects impact energy, controls heat, and adapts its structure in real time. Built with metamaterials, graphene composites, smart sensor networks, and advanced AI optimization, VDAS transforms protection from passive armor into an intelligent defensive system.

As Kid Nebula Gold and Aurora Gold prepare for the final confrontation against Omega Medusa, this technology becomes the shield between civilization and chaos. Every impact is analyzed. Every threat is calculated. Every layer adapts.

⚙️ Smart Sensor Skin

🧠 AI-Powered Adaptive Response

🛡️ Programmable Metamaterial Lattice

⚡ Energy Recovery Systems

🌡️ Advanced Thermal Management

🚀 Aerospace & Planetary Defense Applications

On Aurora 7, survival is not enough.

We engineer victory.

✨ Light.

✨ Hope.

✨ Technology.

✨ Evolution.

#MedusaTechnologies #Aurora7 #KidNebulaGold #AuroraGold #OmegaMedusa #VariableDensityArmor #AdvancedMaterials #Metamaterials #Graphene #Engineering #FutureTech #SpaceTechnology #Robotics #ArtificialIntelligence #Innovation #SciFi #Blueprint #QuantumCompute #AdaptiveSystems #TechFuture

54