Jun 16

_/_/_/_/_/ ٩(ˊᗜˋ*)و #LLM #AgentEngineer

あとでやってみる。

Jun 15

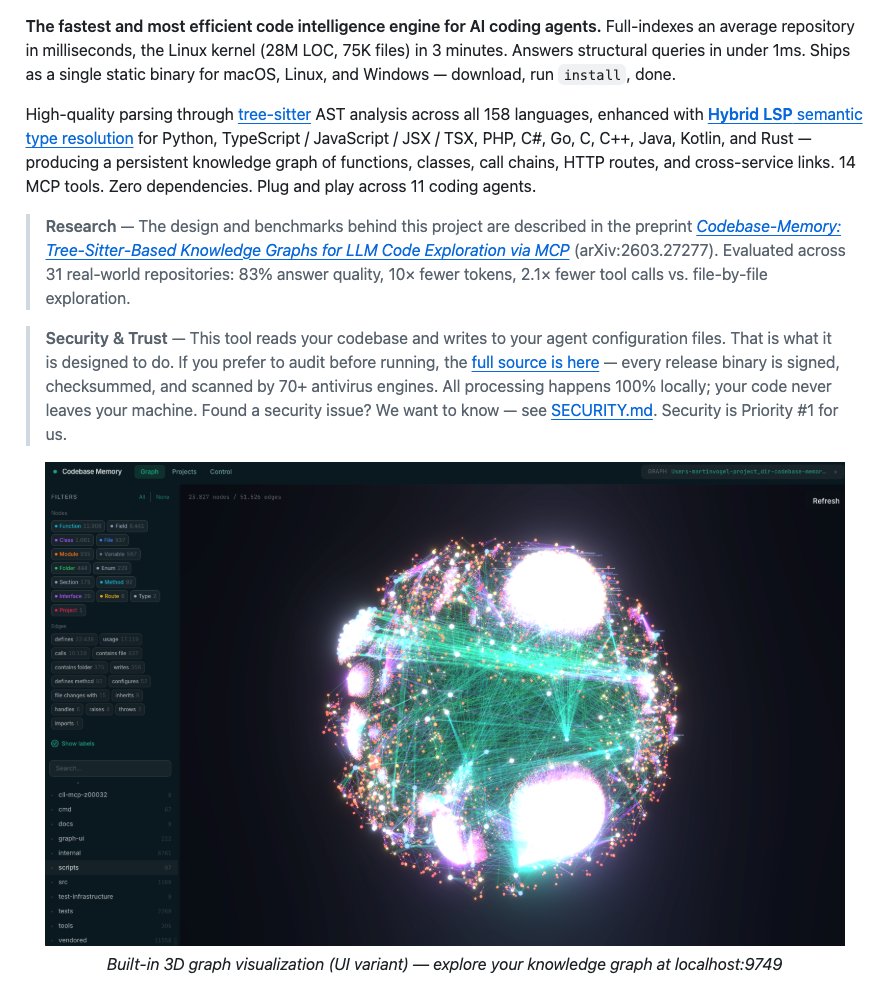

🚨How do you index the entire Linux kernel (28M lines of code) for an AI agent in 3 minutes?

You stop letting the agent read files one by one.

There is a fascinating new open-source release called codebase-memory-mcp.

It's a code intelligence engine that swaps traditional file-searching for high-speed AST knowledge graphs.

What makes this project stand out is the research behind it.

Evaluated across 31 real-world repositories (detailed in arXiv:2603.27277), the architectural shift yields massive efficiency gains:

→ 99% reduction in tokens for structural queries

→ 83% answer quality across complex tasks

→ 2.1x fewer tool calls required

It maps functions, classes, HTTP routes, and cross-service links into a graph. When the agent needs context, it queries the graph directly.

Security is prioritized too: everything happens 100% locally on your machine via a single static binary.

It runs entirely locally.

No Docker, no Ollama, no API keys.

You download the binary, restart your agent, and it just works.

Are we one good index away from cutting AI dev costs to zero?

Paper and Repo links in the thread ↓

1

304

May 31

3. Gen AI & Intelligent Content Applications (3 talks)

Thurs 9:30am Ed H. Chi, $GOOGL (Google DeepMind): The Future of Personalized Universal Assistant

Thurs 10:00am Thomas Andersen, $SNPS (Synopsys): Automating Chip Design with AgentEngineer

Thurs 11:30am Dr. Paul Cunningham, $CDNS (Cadence): Pioneering the Future of IC with Agentic AI

4. AI Devices, IoT & Edge Intelligence (3 talks)

Wed 1:30pm Mark Linton, $MSFT (Microsoft): Powering a Billion Users with Windows

Wed 2:30pm Kedar Kondap, $QCOM: The Rise of Personal AI Devices

Wed 3:30pm Sameer Wasson, MIPS (→ $GFS?!): Building Software-First AI for the Real World

5. Applied AI for Industry Transformation (3 talks)

Wed 4:00pm Dr. Denise Lee, McKinsey (private): The AI Inflection, Redefining Work & Decision-Making

Thurs 1:30pm Frank Grunert, $SIE.DE $SIEGY (Siemens): From Hype to Impact, Digital Twins & Industrial AI

Thurs 2:00pm Miller Chang, Advantech ($2395.TW): From Digital to Physical, Edge AI Computing & WEDA

6. Data Intelligence, Governance & Security (1 talk)

Thurs 11:00am Mike Chen, Synology (private): Digital Sovereignty Accelerates Private Cloud Adoption

2

503

May 19

Synopsys just launched AgentEngineer, an agentic AI that automates the entire chip design pipeline from specs to silicon. Major leap for semiconductor innovation. $SNPS

Synopsys AgentEngineer Automates End-to-End Chip Design

1

2

375

May 18

📢 COMPUTEX 2026 Forum Speaker Announcement!

We are excited to announce that Thomas Andersen, Vice President of AI and Machine Learning at @Synopsys, will take the stage at the COMPUTEX Forum!

Thomas Andersen will present "Automating Chip Design with AgentEngineer™ Technology." In this session, he will share his vision for automating the entire systems to silicon chip design process using Agentic AI technology, spanning from initial concept specification all the way to final production.

Join us to discover how Agentic AI is set to revolutionize the chip design process and accelerate the future of silicon innovation!

Date: June 4 at 10:00 a.m. – 10:25 a.m. (GMT 8)

Venue: Taipei Nangang Exhibition Center, Hall 2 (TaiNEX 2), 7F

More Information: events.computextaipei.com.tw…

#COMPUTEX2026

1

2

669

Meet your new AI coworker: Synopsys AgentEngineer — the adaptive, multi-agent workflow solution transforming chip design. Unlock innovation now: bit.ly/48WNoTE

2

3

690

Our mission is to empower innovators to drive human advancement. And that advancement involves re-engineering how next-gen, AI-powered products are designed & delivered.

Hear from our CEO Sassine Ghazi as he outlines our AgentEngineer technology: bit.ly/4wtg7K6

1

1

3

526

Mar 22

Synopsys 今天发布了AgentEngineer AI平台

这反映的是芯片设计的复杂度和成本,已经逼近传统工程方法的极限。

先进制程下,一颗高端芯片的开发成本动辄数亿美元,继续靠堆工程师、拉长周期去解决问题,越来越不现实,行业不得不把更多设计流程交给ai自动化系统。

而在此过程中, EDA 正在从工程师使用的软件工具,变成一种系统级基础设施。

过去是“人设计,软件辅助”,现在开始走向“系统主导设计,人负责监督”。谁能控制设计、验证、仿真、优化这一整条链路,谁就不只是卖工具,而是在控制芯片设计流程本身。

这也对应了一个更大的趋势,ai能力的递归自我迭代正在从训练大模型,向设计、仿真、工业计算等更多环节外溢。未来消耗算力的,不只是训练模型的公司,也包括设计芯片的公司。

AI参与设计芯片、芯片再反过来加速AI的循环,也已经开始启动。

对 Synopsys 这类 EDA 龙头来说,短期护城河会更深。因为它们的核心不只是软件,还包括历史设计数据、失败案例、优化路径和客户流程。AI进入之后,这些积累会进一步放大,客户替换成本也会更高。

至于长期,当ai实现覆盖软硬件芯片的全递归自我迭代,那么eda公司也就将成为整个迭代闭环中,重要的一个组成部分。

3

2

29

18,254

Mar 20

Synopsys, GTC 2026서 NVIDIA와 AI 엔지니어링 혁신 성과 발표

1/ Synopsys가 Ansys를 인수한 후 NVIDIA와의 협력을 강화하며 GTC 2026에서 AI 기반 엔지니어링 혁신 성과를 공개했다. 반도체·자동차·항공우주 등 산업에서 설계 복잡성과 개발 비용 증가 문제를 AI·고성능 컴퓨팅으로 해결하는 방향을 제시한다.

2/ Synopsys는 반도체 설계와 멀티피직스 시뮬레이션을 통합한 환경을 구축했다. 디지털 트윈과 가상 프로토타이핑으로 물리적 시제품 제작 전에 성능 검증이 가능해 개발 리스크와 시간을 크게 줄인다.

3/ 에이전트 AI 기반 엔지니어링을 강조하며 Synopsys AgentEngineer 기술을 중심으로 멀티 에이전트 워크플로를 구현한다. NVIDIA의 Agent Toolkit·NIM 추론 서비스·Nemotron 모델과 연동해 복잡한 칩 설계 작업을 자동화한다.

4/ 업계 최초 L4 수준 에이전트 EDA 워크플로를 시연했다. 실리콘부터 시스템까지 AI가 관여하는 새로운 설계 패러다임을 보여줬다.

5/ 고객 사례로 Analog Devices(ADI)는 NVIDIA Omniverse·Isaac Sim 환경에서 Synopsys 멀티피직스 시뮬레이션을 활용해 멀티모달 촉각 센서와 로봇 민첩성 디지털 트윈을 제작했다. 고충실도 시뮬레이션으로 케이블·플러그·센서 인식 등을 검증한다.

6/ Applied Materials는 QuantumATK와 NVIDIA cuEST로 양자 화학 시뮬레이션 속도를 최대 30배 향상시켰다. Honda는 Ansys Fluent GPU 가속으로 CFD 연산을 34배 빠르게 하고 비용을 38배 절감했다.

7/ Astera Labs는 AWS에서 B200 GPU 기반 PrimeSim으로 설계 검증 속도를 3.5배 개선해 제품 출시 기간을 단축했다.

8/ Sassan Ghaffari Synopsys CEO는 전통 엔지니어링 방식의 한계를 지적하며 NVIDIA 등 파트너와 협력해 공동 설계·연산 가속·디지털 트윈을 통해 고객 지원을 강화한다고 밝혔다.

9/ Jensen Huang NVIDIA CEO는 AI와 고성능 컴퓨팅이 제품 설계·운영 전 과정을 바꾸고 있으며 Synopsys와의 결합으로 새로운 엔지니어링 패러다임을 구현한다고 강조했다.

10/ Synopsys는 GTC 2026 기간 부스(#1135)에서 산업용 로보틱스·반도체 제조·양자 화학·의료 등 AI 엔지니어링 적용 사례를 데모하고 전문가 세션을 진행한다. AI 시대 복잡한 설계 환경을 효과적으로 다루는 방향으로 나아간다.

1

2

170

Mar 12

A big day for Synopsys Converge and CEO Sassine Ghazi after announcing Multiphysics Fusion, the AgentEngineer AI platform and the start of “Synopsys 2.0” following the Ansys merger.

@synopsyslife #SNPS #Semiconductors #EDA $SNPS #CEOSelfie

3

372

Mar 12

Mi amico and brother from another mother @MarcoChiappetta is out at @Synopsys Converge this week, and there have been some exciting announcements at the show, including the company's new AgentEngineer for chip design. You've heard of L4 level autonomy for self-driving cars. Now think a fully agentic workflow along side human engineers right on down to generating RTL from natural language input. Wild stuff! Check out Marco's full coverage right here... 👇forbes.com/sites/marcochiapp…

1

2

365

Mar 11

. @Synopsys CEO Sassine Ghazi just announced the industry's first L4 agentic workflow, dubbed AgentEngineer...

2

7

750

Mar 11

Part 1 : Synopsys

To me, this company used to be just the maker of the FineSim simulator and an IP bank. Nothing more, nothing less.

Honestly, FineSim is famous. For time-domain analysis, there's no better tool. It's still widely used globally.

It also acts as an IP bank holding many SerDes IPs for TSMC and Samsung Foundry.

But this company is transforming.

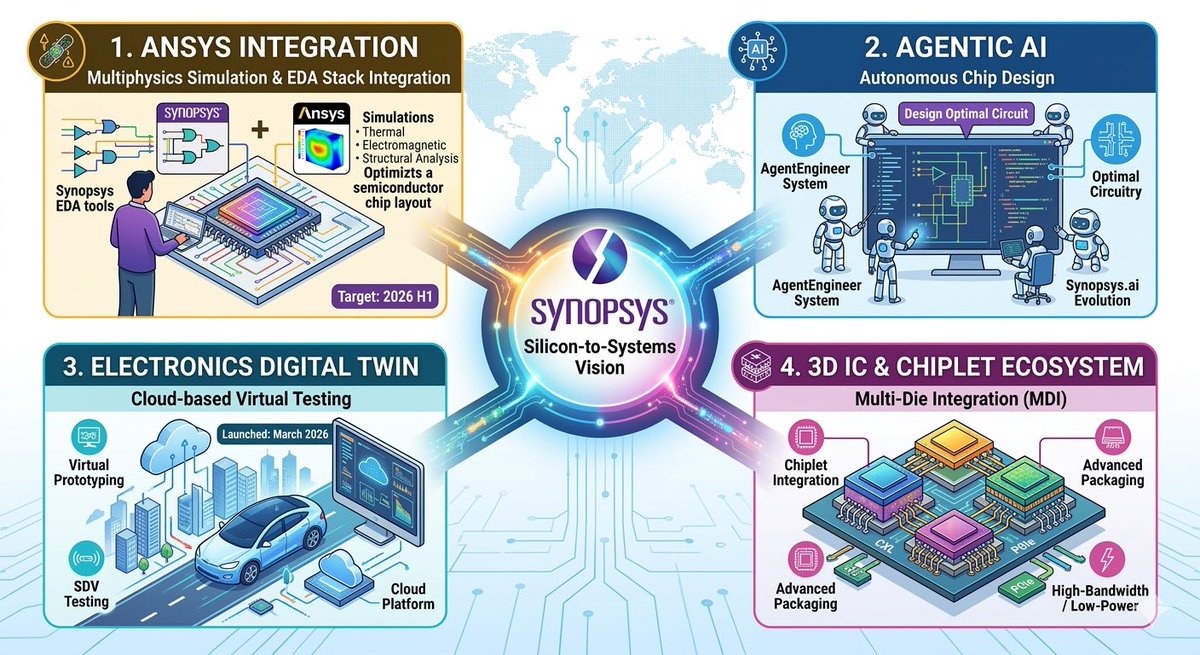

Recently (late 2025~2026), Synopsys is evolving from a simple EDA company into a "Silicon-to-Systems" engineering solutions provider. Here is a summary of their major ongoing or upcoming projects.

1. Synopsys-Ansys Tool Integration (Target: 2026 H1)

In July 2025, Synopsys acquired Ansys for $35 billion. Their largest integration project is underway to combine both technologies.

• Project Direction: Integrating Ansys's thermal, electromagnetic, and structural simulations into the EDA stack.

• Current Goal: Launch the first combined solution covering multi-die packaging and the EDA stack by 2026 H1.

• Related Roles: R&D Software Engineer (Algorithm Optimization), Physical Design Engineer, Cloud Architect.

2. Autonomous Chip Design via Agentic AI

Following Synopsys.ai, Synopsys is now applying Agentic AI to the design workflow.

• Project Direction: Advancing AgentEngineer technology where AI agents autonomously generate testbenches, analyze designs, and optimize workflows (collaborating with Microsoft, AMD).

• Current Goal: Building an environment where natural language prompts let AI optimize physical verification and layout, reducing design time.

• Related Roles: R&D Software Engineer (AI/ML), ASIC Verification Engineer, Hardware Architect.

3. Electronics Digital Twin (eDT) Platform (Launched: March 2026)

Launched in March 2026, this virtualization project tests software and systems in the cloud before physical chips are produced.

• Project Direction: Building a cloud platform to accelerate Software-Defined Vehicle (SDV) and intelligent system development.

• Current Goal: Helping automotive, aerospace, and industrial customers find pre-silicon defects and speed up time-to-market.

• Related Roles: Firmware/Embedded Software Engineer, Emulation Hardware R&D, Full-Stack Web Engineer.

4. Next-Gen 3D IC and Chiplet Ecosystem

With surging AI chip demand, Multi-Die and Chiplet design has become a key trend.

• Project Direction: Collaborating with Samsung, SK Hynix, and TSMC to advance its Multi-Die Integration (MDI) flow (e.g., 3DIC Compiler).

• Current Goal: Maximizing support for high-bandwidth, low-power architectures for AI chipsets.

• Related Roles: High-Speed Interface (PCIe, CXL, DDR) IP Design & Verification Engineer, Applications Engineer (AE).

<Summary>

Synopsys is focusing on four pillars: Ansys integration, Agentic AI, cloud-based digital twins, and 3D packaging/high-speed IPs. They are aggressively hiring hardware/software talent for these.

In my experience, enhancing EM analysis via Ansys is a strong foundation, and expanding this to chiplets is very compelling. We desperately need simulation tools for precise TSV or chiplet-level predictions.

Honestly, I tried the autonomous chip design, and the performance is still meh haha. I was nervous for nothing lol.

$SNPS

3

387

Mar 11

Part 1 : Synopsys

내가 아는 이 회사는 Finesim. 이라는 시뮬레이터를 만드는 회사? 그리고 IP를 꽤 많이 보유한 회사 그 이상도 이하도 아니였습니다

솔직히 Finesim. 은 워낙에 유명한 tool이죠 솔직히 time domain에서의 분석엔 이만한 툴이 없어요 글보벌하게 널리 쓰고 지금도 쓰죠

그리고 TSMC든 삼성파운드리든 다수의 SerDes IP를 보유하고 있는 IP bank 입니다

그런데 이회사가 변모하고 있네요

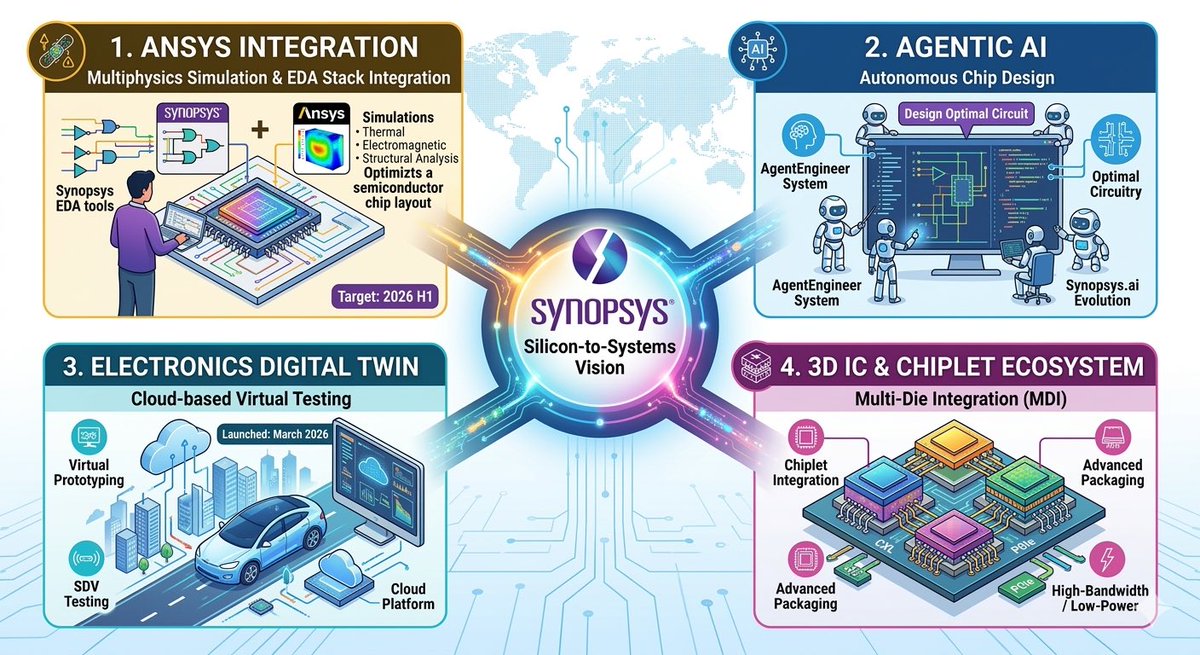

최근(2025년 하반기~2026년 현재) 시놉시스의 행보를 보면, 단순한 반도체 설계(EDA) 회사를 넘어 "실리콘에서 시스템까지(Silicon-to-Systems)" 아우르는 종합 엔지니어링 솔루션 기업으로 진화하고 있습니다.

이를 바탕으로 현재 진행 중이거나 곧 출시를 앞둔 주요 프로젝트를 정리해 드립니다.

1. 시놉시스-앤시스(Ansys) 툴 통합 프로젝트 (2026년 상반기 출시 목표)

2025년 7월, 시놉시스는 다중 물리(Multiphysics) 시뮬레이션 1위 기업인 앤시스(Ansys)를 350억 달러에 인수 완료했습니다. 현재 두 회사의 기술을 결합하는 창사 이래 최대 규모의 통합 프로젝트가 진행 중입니다.

• 프로젝트 방향: 기존 반도체 설계(EDA) 스택에 앤시스의 열, 전자기계, 구조 해석 시뮬레이션을 완전히 통합.

• 현재 목표: 2026년 상반기 내에 첨단 멀티다이(Multi-die) 패키징 및 전체 EDA 스택을 아우르는 첫 번째 결합 솔루션 출시.

• 관련 채용 직무: R&D 소프트웨어 엔지니어(알고리즘 최적화), 물리 설계(Physical Design) 엔지니어, 클라우드 아키텍트.

2. 에이전틱 AI (Agentic AI) 기반의 칩 설계 자율화

시놉시스는 업계 최초로 AI 기반 EDA인 Synopsys.ai를 도입한 데 이어, 현재는 에이전틱 AI(스스로 판단하고 실행하는 자율형 AI)를 반도체 설계 워크플로우에 적용하는 데 집중하고 있습니다.

• 프로젝트 방향: 단순한 챗봇 형태의 보조를 넘어, AI 에이전트들이 서로 협력하여 테스트벤치 생성, 설계 분석, 작업 흐름 최적화 등을 자율적으로 수행하는 AgentEngineer 기술 고도화 (마이크로소프트, AMD 등과 긴밀히 협력).

• 현재 목표: 엔지니어가 자연어로 프롬프트를 입력하면 AI가 복잡한 물리적 검증과 레이아웃을 최적화하여 설계 시간을 대폭 단축하는 환경 구축.

• 관련 채용 직무: R&D 소프트웨어 엔지니어(AI/ML 알고리즘), ASIC 검증 엔지니어, 하드웨어 아키텍트.

3. 전자 디지털 트윈(Electronics Digital Twin, eDT) 플랫폼 (2026년 3월 론칭)

가장 최근인 2026년 3월에 공식 론칭된 플랫폼으로, 물리적인 칩이나 하드웨어가 나오기 전에 클라우드 환경에서 소프트웨어와 시스템을 먼저 테스트할 수 있는 거대한 가상화 프로젝트입니다.

• 프로젝트 방향: 클라우드 기반의 개방형 플랫폼을 구축하여, 자동차 업계의 화두인 소프트웨어 정의 차량(SDV) 및 지능형 시스템 개발을 가속화.

• 현재 목표: 자동차, 항공우주, 산업용 센서 분야 고객사들이 칩 제작 전 단계에서 결함을 찾고 시장 출시 속도(Time-to-market)를 앞당길 수 있도록 지원.

• 관련 채용 직무: 펌웨어/임베디드 소프트웨어 엔지니어, 에뮬레이션 하드웨어 R&D, 풀스택 웹 엔지니어.

4. 차세대 3D IC 및 칩렛(Chiplet) 생태계 선점

AI 모델 구동을 위한 고성능 칩의 수요가 폭발하면서, 여러 개의 칩셋을 레고 블록처럼 이어 붙이는 멀티다이(Multi-Die) 및 칩렛(Chiplet) 설계가 핵심 트렌드가 되었습니다.

• 프로젝트 방향: 삼성전자, SK하이닉스, TSMC 등 핵심 파운드리 파트너들과 협력하여 3DIC Compiler 등 자사의 멀티다이 통합(MDI) 설계 플로우를 최신 공정에 맞춰 지속해서 인증받고 고도화.

• 현재 목표: 초거대 AI 칩셋 개발 시 필수적인 고대역폭, 저전력 아키텍처 지원 능력을 극대화.

• 관련 채용 직무: 고속 인터페이스(PCIe, CXL, DDR 등) IP 설계 및 검증 엔지니어, 어플리케이션 엔지니어(AE).

<요약>

현재 시놉시스는 Ansys 툴과의 물리 시뮬레이션 융합, 에이전틱 AI를 통한 설계 자동화 극대화, 클라우드 기반 디지털 트윈 플랫폼 확장, 3D 패키징 및 고속 인터페이스 IP 고도화라는 4가지 거대한 축으로 프로젝트를 굴리고 있으며, 이에 맞춰 하드웨어/소프트웨어 인재를 공격적으로 흡수하고 있습니다.

내 경험으론 Ansys 인수를 통한 EM 분석 능력 향상이 큰 밑바탕이고 이를 바탕으로 chiplet 까지 넘보는 건 진짜 매력적이네요

TSV나 chiplet level 에서 정밀하게 예측해줄 simulation tool이 진짜 간절하거든요

솔직히 칩설계 자율화는 써 봤는데 아직 좀 성능이 그닥입니다 ㅋㅋ 괜히 긴장했었음 ㅋㅋ

$SNPS

2

2

22

1,550

Feb 28

はてなブログに投稿しました #はてなブログ

自律行動するAIエージェントの新次元:Synopsys AgentEngineer™ - Vengineerの妄想

vengineer.hatenablog.com/ent…

5

628

$SNPS Synopsys — Morgan Stanley downgrades to Equalweight, cuts PT 🔻

PT ↓ $480 (from $550) | Current $423 (Upside ~13%)

⠀

• Core EDA (ex-Ansys) slowing to high single-digit growth

• AgentEngineer early stage; ramp timing & pricing model unclear

• Competition rising in 3D-IC & physical AI emulation despite strong hardware & IP outlook

2

257

Yapay Zeka Gündemi (22 Ocak 2026)

Elon Musk Davos'ta bomba patlattı: "Yapay zeka bu yılın sonunda herhangi bir insandan daha akıllı olacak. En geç 5 yıl sonra (2031) tüm insanlığın toplam zekasını aşacak!"

Tahmin: Robotlar insan ihtiyaçlarını karşılayacak kadar çoğalacak, ekonomide patlama yaşanacak.

Kaynak: Anadolu Ajansı Euronews

Musk'ın bir başka çarpıcı sözü: "Robotların sayısı insan nüfusunu geçecek ve bu benign (zararsız) senaryoda olacak"

BlackRock CEO'su Larry Fink ile röportajında: AI robotik, benzeri görülmemiş ekonomik büyüme getirecek.

Kaynak: CNBC röportajı (22 Ocak 2026)

Dünyada paralel gelişmeler:

Davos 2026'da üst düzey yöneticiler uyardı: AI milyonlarca işi yok edecek, işsizlik artacak (JPMorgan CEO'su Jamie Dimon: "Kaçınılmaz, 5 yıl içinde daha az iş olacak").

Kaynak: The Economic Times (22 Ocak 2026)

Teknik devrim: Yonga tasarımı artık tamamen AI'ye emanet.

2nm çiplerde "Agentic Design" ile AI ajanları kendi başına tasarım yapıyor (Synopsys AgentEngineer).

Geliştirme süresi 12 ay kısalıyor, güç tüketimi " azalıyor.

Bu, "Recursive AI Improvement" – AI'nin kendi donanımını tasarladığı ilk büyük adım.

Kaynak: TokenRing AI raporu (22 Ocak 2026)

Türkiye'den ilginç not: Ocak 2026 itibarıyla Türkiye'de 457 yapay zeka girişimi var. (40 adet yeni eklenmiş) TRAI Girişim Haritası güncellendi – ekosistem hızla büyüyor.

Kaynak: Türkiye Yapay Zeka İnisiyatifi (turkiye.ai, Ocak 2026)

Korkutucu mu heyecan verici mi?

Bir yanda "kara kutu" gibi anlaşılmaz AI'lar (uzaylı zekâya benzetiliyor – MIT Technology Review).

Diğer yanda günlük hayat: Google Photos ve Gmail'e "Personal Intelligence" eklendi, AI kişisel verilerini öğrenip daha akıllı cevap veriyor.

2026'da AI meteorolojiyi dönüştürüyor – Google DeepMind fırtınaları günler öncesinden 0 doğru tahmin ediyor.

Daha fazla detay için takipte kalın.

#YapayZeka #AI #ElonMusk #GelecekTeknolojisi #BilimselGerçek #Teknoloji #GerçekBilgi #ArtificialIntelligence

2

45

Jan 4

_/_/_/_/_/ ٩(ˊᗜˋ*)و #LLM #AgentEngineer

「プログラミングができる人」と「アイデアがある人」という固定的役割の壁が崩れます。誰もがNexusを通じて他者のスキル(Wrapper)をエージェント経由で使えるようになることで、より多様な人々がプロジェクトに「真に」参画できるようになります。

1

2

63

25 Dec 2025

$SNPS $CNDS $RMBS $ARM EDA and Semiconductor IP: Market Dynamics, Strategic Valuation, and Sector Overview

The provided equal-weight EDA and semi IP index contains 2 structurally attractive but economically distinct business types: EDA software platforms (CDNS, SNPS) and semiconductor IP licensors and interface-enablement vendors (ARM, RMBS, CEVA). The index snapshot (12/24 14:20) shows wide dispersion: RMBS is 78.74% YTD versus CEVA at -30.84% YTD, while CDNS is 5.76% YTD, SNPS is -1.98% YTD, and ARM is -9.57% YTD. Over the last 3M, all constituents are negative except SNPS ( 1.64%), indicating a recent factor rotation away from higher-multiple secular software/IP exposures despite continued evidence of secular demand for design, verification, and system analysis tooling. Valuation dispersion is also significant: ARM screens at 64.9x current P/E and 21.6x EV/Sales versus SNPS at 33.1x current P/E and 10.7x EV/Sales, with CDNS in between at 45.0x current P/E and 15.0x EV/Sales; RMBS and CEVA exhibit “IP vendor” optics (higher P/E with materially smaller scale), but their business-model mix and margin structures differ substantially.

At the industry level, the electronic system design ecosystem continues to grow at a pace that is directionally consistent with long-cycle semiconductor R&D intensity and system complexity rather than wafer-fab cycles. The SEMI ESD Alliance reported Q2 2025 electronic system design industry revenue of $5,089.4M ( 8.6% YoY), with a 4-quarter moving average 10.4%. Within that dataset, CAE grew 17.2% to $1,929M and Semiconductor IP grew 8.7% to $1,826.7M, highlighting that simulation/analysis and IP monetization are increasingly large components of the design stack alongside traditional digital implementation and verification. The structural driver set remains consistent: advanced-node physics, exploding verification state-space, chipletization and 2.5D/3D integration, rising thermal/power constraints, and heterogeneous compute architectures for AI, automotive, and edge devices. These drivers increase tool and IP content per design, raise the value of “signoff-grade” software, and extend the duration and criticality of tool engagement across the design lifecycle. However, the sector is not immune to episodic volatility driven by (1) customer digestion cycles and contract timing, (2) export controls and geopolitics, (3) consolidation and vertical integration among leading chip designers, and (4) competitive dynamics in open instruction sets (RISC-V) and in-house tooling for specific workflows.

Cadence Design Systems (CDNS) is positioned as a full-stack EDA vendor with a portfolio intentionally structured to capture value across chip, package, board, and system-level analysis, with an explicit strategy to integrate multiphysics computation and AI into the design flow. Cadence groups its business into 3 categories—Core EDA, Semiconductor IP, and System Design and Analysis—and disclosed that for the 3 months ended 6/30/2025, revenue mix was 71% Core EDA, 13% Semiconductor IP, and 16% System Design and Analysis. This mix matters for both cyclicality and competitive posture: Core EDA tends to be the stickiest (deep workflow integration and foundry-qualified signoff), Semiconductor IP adds “design-start” leverage and potential royalties but introduces greater end-market sensitivity, and System Design and Analysis expands TAM into multiphysics and system-level verification where compute intensity and AI-assisted optimization can create incremental monetization vectors.

The Core EDA franchise is typically monetized via time-based licensing, subscriptions, and support/maintenance, with additional revenue from hardware platforms (emulation/prototyping) and services. Cadence’s disclosure of recurring revenue at 80% for the trailing 12-month period ended 6/30/2025 (versus 88% at 6/30/2024) suggests a higher mix of up-front revenue and/or hardware and services over the prior year, which can improve near-term growth optics but also modestly increases sensitivity to contract and delivery timing. For a hedge fund committee, the key point is that CDNS’s business model remains predominantly recurring, but marginal shifts in mix can influence reported growth volatility and investor perception of defensiveness.

Cadence’s ecosystem role is anchored in mission-critical nodes of the RTL-to-GDSII and verification stack, plus packaging and PCB, which keeps the company structurally levered to rising design complexity. Differentiation is increasingly pursued through AI-driven automation and compute orchestration. Cadence has promoted Cerebrus as an ML-driven optimization layer for RTL-to-signoff implementation, positioned to improve engineering productivity and PPA outcomes and to better utilize cloud/on-prem compute. In verification, the JedAI platform and Verisium are designed to unify design/verification data and apply AI to workload optimization and debug productivity. The commercial relevance of these initiatives is 2-fold: they support pricing power by tying outcomes to measurable productivity improvements, and they potentially shift value capture toward compute-intensive optimization cycles where usage-based and cloud-delivered models can expand revenue per design beyond historical seat-based licensing.

From a market-sizing standpoint, Cadence’s exposure spans EDA plus adjacent system analysis categories that have been growing faster than the core. The ESD Alliance data showing CAE growth 17.2% YoY provides external validation that system analysis is a meaningful growth pool. Within Cadence, the System Design and Analysis category (16% of revenue) adds another lever: if chiplet and thermal constraints keep moving “system problems” upstream into silicon design, demand for co-design and multiphysics integration should increase. Variant perception often centers on whether multiphysics expansion is a durable incremental TAM capture versus a competitive response to Synopsys’s Ansys acquisition. A constructive variant view would emphasize that multi-domain simulation is becoming a prerequisite for first-pass silicon success in AI accelerators, automotive SoCs, and advanced packaging, and that early integration into EDA workflows may allow incumbents to capture share via flow ownership rather than by selling point tools. A cautious variant view would emphasize that simulation buyers in non-semiconductor verticals have different procurement behavior and that “EDA-first” vendors risk slower adoption outside their historical buyer base.

Regulatory and geopolitical risk is tangible. Cadence disclosed that in the 3 months ended 6/30/2025, China was 9% of revenue (down from 12% in the prior-year period), and explicitly attributed the decline in China revenue to “decreased deliveries of software offerings” resulting from BIS export license requirements temporarily imposed from 5/23/2025 to 7/2/2025. This highlights a non-trivial tail risk: abrupt export policy changes can impact near-term revenue and collections in a manner that is difficult for the market to handicap ex ante. It also reinforces that the EDA stack is strategically sensitive and can be used as a policy lever, which can compress multiples during periods of heightened uncertainty.

Financially and in market terms, CDNS in the snapshot trades at MV 86,495 and EV 86,220 with ROIC 14, EV/EBITDA 31.8, EV/Sales 15.0, current P/E 45.0 and next P/E 39.6. Consensus “Best” financials imply Sales 5,281, EBITDA 2,494, and NI 1,932, consistent with a high-margin, asset-light software model. The stock is -15.59% from its all-time high, with 52W range 221.56–376.45 and last price 317.76. The near-term trading tape shows -10.98% over 3M despite 4.37% over 1M, consistent with a recent rebound within a broader drawdown. The bull case hinges on continued structural growth in design complexity, monetization of AI-driven productivity layers, and sustained pricing power within a consolidated EDA market. The bear case centers on valuation risk at high multiples, potential spending pauses at leading customers, the durability of non-core expansion, and recurrent export-control disruptions.

Synopsys (SNPS) occupies a complementary but distinct position relative to Cadence: it is both an EDA platform vendor and a large-scale design IP provider, and as of 2025 it has expanded into full-system simulation and analysis through the Ansys acquisition. Historically, Synopsys reported 2 main segments—Design Automation and Design IP—and in fiscal 2024 generated $4.221B in Design Automation revenue and $1.906B in Design IP revenue (total $6.127B), implying Design IP at ~31% of revenue and making SNPS structurally more exposed to “IP attach” and unit-driven royalty dynamics than CDNS. Synopsys’s geographic exposure has been higher in China than Cadence’s in the cited period: fiscal 2024 revenue from China was $989.524M out of $6.127B total, representing 16.1% of total revenue. This matters for risk assessment under export controls and for multiple durability in a regime of persistent U.S.-China technology friction.

Strategically, the defining development is the acquisition of Ansys, which was completed on 7/17/2025 and required closing conditions including planned divestitures (notably the Optical Solutions Group and the PowerArtist tool) to address regulatory concerns. The industrial logic is “silicon-to-systems”: chip design increasingly requires tightly coupled multiphysics simulation (electromagnetics, thermal, mechanical stress, fluids) across package, board, and enclosure, particularly for AI accelerators, advanced packaging, and automotive/aerospace systems where safety margins and thermal envelopes are binding constraints. A combined SNPS Ansys stack can, in principle, unify signoff constraints earlier in the design loop, reduce iteration count, and allow AI models to learn across a larger simulation dataset. The bull thesis frames this as a step-function TAM expansion and a moat-widening move: if the “system” becomes the new optimization boundary, the vendor owning the integrated workflow can capture disproportionate value. The bear thesis frames it as integration and execution risk: product integration timelines, salesforce alignment, customer procurement complexity, and regulatory constraints that may limit bundling or require interoperability can reduce synergy realization and delay monetization.

Synopsys is also aggressively positioning around AI-enabled automation of the EDA workflow. The company has described Synopsys.ai as a suite applying reinforcement learning and generative AI to improve performance and efficiency and accelerate time-to-market, and has highlighted AgentEngineer as a next step toward agentic AI systems that can execute multi-stage engineering tasks under human oversight. This trajectory is central to the medium-term monetization debate in EDA: if agentic systems reduce the marginal cost of design exploration, the value captured may shift to the tool vendor (who provides the agent and the optimization stack) and to compute providers, rather than accruing entirely to engineering headcount reduction at the customer. A skeptical variant view would argue that AI features become table stakes and compress differentiation, especially if customers demand them as part of existing contracts. A constructive variant view would emphasize that proprietary training data (design/verification traces, signoff results, bug databases) and foundry-qualified signoff flows create defensible data moats, enabling outcome-based pricing or higher ARPU per customer.

A notable ecosystem signal is the deepening relationship between Synopsys and NVIDIA. Reuters reported that NVIDIA made a $2B investment in Synopsys as part of a multi-year collaboration to integrate NVIDIA’s AI developer tools into engineering workflows, with the intent to advance AI-driven design and simulation across industries. This reinforces a plausible bull pathway: accelerated computing (GPU-accelerated simulation and EDA workloads) and AI-enabled automation can increase compute demand per design, potentially supporting usage-based monetization, cloud attach, and higher switching costs through integrated stacks. A risk-aware interpretation is that such partnerships are non-exclusive and may not translate into sustained pricing power; competitive parity could emerge if similar integrations proliferate across vendors.

In the provided snapshot, SNPS trades at MV 91,020 and EV 102,352, implying meaningful net debt or acquisition-related financing and raising sensitivity to integration outcomes and interest-rate conditions. It screens at ROIC 3, EV/EBITDA 22.6, EV/Sales 10.7, current P/E 33.1 and next P/E 28.1, with consensus “Best” Sales 9,628, EBITDA 4,328, NI 2,757, consistent with a much larger revenue base than the fiscal 2024 standalone numbers and directionally consistent with post-Ansys scale. The stock is -27.00% from its all-time high, with 52W range 365.74–651.73 and last price 475.75. Recent performance is notable: 17.58% over 1M and 5.01% over 5D despite -1.98% YTD, consistent with an event-driven rebound and/or shifting expectations around integration and AI leverage. The principal bull case is that integrated EDA IP simulation becomes the dominant platform for system-level optimization in AI and automotive, driving sustained high-single-digit to low-double-digit growth with stable or expanding margins. The principal bear case is that integration delays and regulatory constraints reduce synergy, China exposure remains a persistent overhang, and the combined entity faces a higher burden of proof to justify platform dominance given rising scrutiny of market power in critical design infrastructure.

Arm Holdings (ARM) is economically and competitively different from the EDA names: it is the leading CPU architecture/IP licensor with a business model split between up-front licensing (including various access/subscription programs) and downstream royalties per chip shipped by partners. Arm’s Form 20-F describes royalties as variable and dependent on licensees’ sales, with royalty rates influenced by multiple factors and typically declining with higher shipment volumes, which makes mix and tiering as important as unit growth for revenue expansion. Arm has also expanded “access” models intended to increase design-start engagement and pipeline visibility; in the fiscal Q4 2025 shareholder materials filed with the SEC, Arm reported Arm Total Access licenses increased to 44 and Arm Flexible Access customers to 314. These programs are strategically relevant because they can convert historically lumpy licensing into more predictable contract value and can deepen the funnel of smaller and mid-size customers who may become future royalty contributors.

Arm’s ecosystem role is foundational: it supplies ISA, CPU cores (mobile, embedded, and data center), and related system IP that underpins a large share of global compute devices, particularly in smartphones and increasingly in data center, automotive, and client PCs. The company’s strategic imperative is to increase value capture per device by driving adoption of higher-royalty architectures (e.g., Armv9) and more integrated compute subsystems (CSS) that raise attach and reduce customers’ incentive to multi-source. In its FY ended 3/31/2025 annual report, Arm reported total revenue of $4,007M (versus $3,233M in the prior year), reflecting strong growth in a period where AI and compute platform demand remained elevated. Arm’s newsroom communications around fiscal year-end 2025 emphasized that full-year revenues exceeded $4B and royalty revenues reached $2B for the 1st time, underscoring the company’s ability to translate platform positioning into royalty expansion as higher-value designs ramp.

The TAM discussion for Arm is best framed as “share of global compute value” rather than a bounded software market. Arm’s near-term growth vectors are tied to (1) data center penetration via Arm-based CPUs and accelerators in hyperscale and cloud environments, (2) automotive compute and zonal architectures that raise silicon content per vehicle, (3) client compute (Windows on Arm and AI PCs) where power efficiency and on-device AI can shift platform choices, and (4) continued smartphone unit normalization with higher royalty content per chip. The principal competitive tension is RISC-V, particularly in low-end embedded and microcontroller segments, and the risk that large customers negotiate harder on economics or pursue more in-house architectures. The 20-F’s description of royalty rates declining with volume highlights a structural negotiation dynamic: the largest customers can exert pricing leverage, so Arm’s ability to maintain or raise effective royalty rates depends on delivering differentiated performance/power, software compatibility, and subsystem integration that is costly to replicate.

In the snapshot, ARM trades at MV 118,355 and EV 115,507, implying net cash. It screens at ROIC 12 but at materially higher valuation multiples than peers: EV/EBITDA 45.1, EV/Sales 21.6, current P/E 64.9, next P/E 49.1, P/CF 51.2. Consensus “Best” Sales 4,856 and EBITDA 2,278 imply an EBITDA margin near 46.9%, consistent with high gross margin licensing economics, while the multiple reflects expectations for sustained above-market growth and rising royalty take. The stock is -40.90% from its all-time high, with 52W range 80.00–183.16 and last price 111.55. Near-term momentum is negative: -17.19% over 1M and -22.70% over 3M, consistent with multiple compression in high-growth IP and/or sensitivity to guidance and licensing timing. The bull case is a durable shift in compute toward Arm in data center and client, sustained Armv9/CSS mix uplift, and improved predictability through access/subscription programs. The bear case is that Arm’s premium multiple is vulnerable to any evidence of slowing royalty growth, delayed data center penetration, or accelerating RISC-V substitution in embedded markets, especially given the inherent lumpiness in licensing and the negotiating leverage of top customers.

Rambus (RMBS) is best characterized as a hybrid of (1) high-speed memory/interface silicon IP and security IP licensing and (2) specialized memory interface chip products that enable next-generation DDR5/LPDDR5 modules and high-performance data center memory subsystems. This positioning makes RMBS more directly levered to AI server memory scaling and memory interface content increases than the more “workflow” driven EDA names. Rambus’s investor presentation highlights that 2024 product revenue was $247M and that product revenue grew at a 28% 5-year CAGR; it also states that Data Center & AI represented >75% of chip and silicon IP revenue. This revenue mix is materially different from pure IP licensors: product revenue introduces supply-chain execution and pricing dynamics, but it also enables faster near-term scaling when standards transitions (DDR5 speed grades, MRDIMM adoption) drive higher content per system.

Rambus’s product and IP portfolio is tightly aligned with the server memory hierarchy and the constraints introduced by AI model scaling. The investor materials list memory interface chips (registering clock driver, PMIC, SPD hub, temperature sensor) and silicon IP offerings including HBM/GDDR/LPDDR memory controller IP with inline memory encryption, PCIe/CXL controller IP with security, and root of trust security IP with quantum-safe cryptography. This places Rambus at a nexus of 3 secular themes: (1) bandwidth and signal-integrity constraints at high DDR5 speeds that increase the value of high-quality clocking and power management on memory modules; (2) the growth of CXL and heterogeneous memory architectures, which increases controller IP content and security requirements; and (3) rising security requirements for data-in-use, data-at-rest, and data-in-motion, which increases attach opportunities for encryption, integrity, and root-of-trust blocks.

TAM framing for Rambus is narrower but potentially fast-growing: it is a beneficiary of the migration from DDR4 to DDR5 and subsequent DDR5 speed ramps, plus the adoption of MRDIMM and other novel memory modules that can increase required interface components. Rambus’s investor materials reference performance leadership toward 12,800 MT/s for MRDIMM and expansion of chipset portfolios for industry-standard DDR5 and LPDDR5 modules. The bull case is that AI server build-out and memory bandwidth constraints extend the DDR5 speed transition and increase content per server, driving multi-year product revenue growth with high operating leverage given the company’s asset-light structure and relatively fixed R&D base. The same materials emphasize cash generation and sustained product revenue records into 2025, supporting a narrative of scaling profitability. The bear case is that memory-related opportunities remain cyclically exposed: server demand can be volatile, module ecosystems can commoditize over time, and pricing pressure can emerge as more suppliers compete in standardized components. Additionally, RMBS is exposed to customer concentration and to technology transitions (e.g., if memory architectures shift faster than expected toward alternatives that reduce third-party chipset content). IP licensing also carries litigation and renewal risks, which can introduce event risk and revenue volatility.

In the snapshot, RMBS trades at MV 10,171 and EV 9,524 (net cash implied), screens at ROIC 20, EV/EBITDA 26.0, EV/Sales 12.1, current P/E 37.9 and next P/E 31.7. Consensus “Best” Sales 704 and EBITDA 336 imply ~47.7% EBITDA margin, consistent with IP-like profitability blended with product revenue. The stock is 78.74% YTD yet still -25.61% from its all-time high, with 52W range 40.12–114.55 and last price 94.48, suggesting the market has repriced the AI/memory exposure but still discounts peak-cycle risks and/or sustainability of elevated growth.

1

4

3,341

2 Dec 2025

$NVDA $SNPS

엔비디아, 시냅시스 지분 2.6% 확보 🔎ㅣ 251201

1. 엔비디아는 2025년 11월 말~12월 초 발표에서 반도체 설계 소프트웨어(EDA) 1위 업체 시냅시스(Synopsys)의 보통주를 주당 414.79달러에 총 20억 달러어치 매입해 약 2.6% 지분을 확보했다고 밝힘

2. 이 투자는 단순 재무투자라기보다 “엔지니어링·디자인 혁신을 위한 전략적 파트너십”의 일환으로, 양사는 다년간 협력 체계를 구축해 엔비디아의 GPU·CUDA AI 플랫폼을 시냅시스의 칩 설계·시뮬레이션·물리 해석 툴 전반에 깊게 통합하기로 함

3. 구체적으로는 CUDA‑X 라이브러리와 AI‑물리(physical AI) 기술을 이용해 시냅시스의 전자설계자동화(EDA), 물리 검증, 전자기 해석, 분자·재료 시뮬레이션, 광학 설계 등 연산 집약적 애플리케이션을 CPU 중심 구조에서 GPU 가속 구조로 전환해, 기존 몇 주 걸리던 워크로드를 몇 시간 수준으로 단축하는 것이 목표

4. 양사는 시냅시스의 AgentEngineer 기술과 엔비디아의 에이전틱 AI 스택(NVIDIA NIM 마이크로서비스, NeMo Agent Toolkit, Nemotron 모델 등)을 결합해, 칩 설계·검증·시뮬레이션 워크플로에서 설계 옵션 탐색·코드 생성·파라미터 튜닝을 ‘자율 설계 에이전트’가 수행하도록 하는 차세대 AI‑EDA 워크플로를 개발 중

5. 또 엔비디아 옴니버스(Omniverse) 기반 디지털 트윈을 시냅시스의 시뮬레이션·검증 도구와 연결해, 반도체뿐 아니라 자동차·항공우주·산업장비·제약 등 다양한 산업의 제품을 ‘원자→트랜지스터→시스템→공장’ 수준까지 가상 공간에서 통합 설계·테스트할 수 있는 엔지니어링 플랫폼을 구축하겠다는 계획

6. 젠슨 황은 이번 거래를 “세계에서 가장 연산 집약적인 분야 중 하나인 설계·엔지니어링을 GPU 가속·AI·디지털 트윈으로 재창조하는 파트너십”이라고 설명하며, 엔비디아가 처음부터 시냅시스 툴 위에서 GPU를 설계해 온 만큼, 이번 협력은 양사 관계의 자연스러운 확장이라고 강조

7. 시냅시스 CEO 사신 가지는 “차세대 지능형 시스템 설계는 전자·물리 통합, AI, 막대한 컴퓨팅 파워가 동시에 필요하다”며, 엔비디아와의 협력이 칩·시스템 설계 복잡도와 비용을 낮추고 출시 속도를 크게 앞당길 것이라 평가했고, 기존 CPU 인프라를 GPU로 전환하는 데 엔비디아가 직접 기술·마케팅 지원을 하기로 했다고 밝힘

8. 시장에서는 엔비디아의 이번 투자와 파트너십을 “칩 설계 스택까지 장악하려는 움직임”으로 해석하며, GPU·CUDA 플랫폼을 데이터센터·모델 학습뿐 아니라 EDA·엔지니어링 툴의 사실상 표준으로 만들려는 전략으로 본다; 실제 발표 직후 시냅시스 주가는 5~8% 급등한 반면, 엔비디아는 단기 조정에도 불구하고 장기 성장 모멘텀 강화로 평가됐음

9. 규제·경쟁 측면에선, 엔비디아가 AI 칩·소프트웨어·클라우드 파트너·설계 툴까지 잇달아 지분·제휴를 확대하면서 생태계 지배력이 과도해질 수 있다는 우려도 제기되지만, 양사는 이번 계약이 비독점(non‑exclusive)이라 다른 파운드리·EDA·클라우드 업체와의 협업도 계속 열려 있다는 점을 명시

10. 종합하면, 엔비디아의 시냅시스 20억 달러 지분 투자는 “GPU AI 플랫폼을 칩 설계·산업 엔지니어링 전체로 확장해, 설계 속도·정밀도·비용 구조를 뒤집는” 장기 전략의 일환으로, 단순 투자 이상의 의미를 가지며, 앞으로 EDA 시장 구조와 반도체·산업 설계 워크플로에 상당한 변화를 가져올 잠재력이 있는 딜로 평가

1

1

11

1,201