אני עוקב אחרי ג׳יימס צ׳אנוס כבר המון זמן ולומד ממנו המון. לא משנה לי הפורטפוליו שלו, אין ספק שהוא מבין לעומק איך השוק עובד ואיך לנתח מניות כמו מעטים מאוד. מאזין גם לצ׳אמת, אקמן וכו׳. אפשר להוסיף לרשימה גם את @altcap שהוא מהצד השורי אבל מעניין תמיד.

1

1

24

BY retweeted

Jun 15

Tremendous respect for @GavinSBaker @altcap @_clarktang & their teams. One of the best pods of the year.

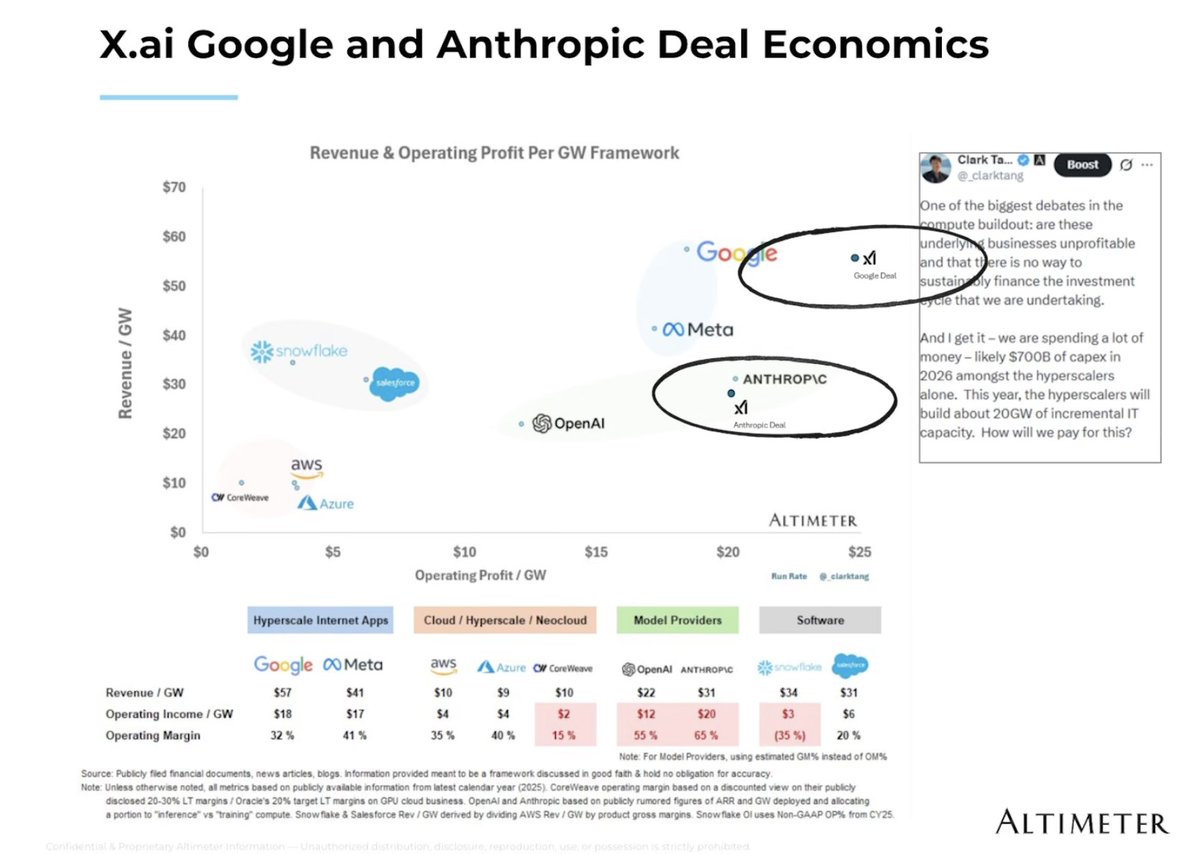

SpaceX becomes hyperscaler #4 in record time

-Effectively went from not focused on it to the #4 in roughly ~30 days, past Oracle and others, on the Google and Anthropic cloud deals alone

-Google deal implies ~$50B revenue/GW, Anthropic ~$25B/GW, against a bank base case of $14B/GW

-Added ~$29B of run-rate in a month, taking the multiple from ~100x trailing revenue to ~39x [shows how savy Elon & Gwynne are at striking deals]

-Core edge is build speed: Colossus 1 in 122 days, and speed compounds because idle construction is pure labor cost on already strained workforce

-AWS analogy holds loosely, but they enter a market where AWS, Azure, GCP, CoreWeave and Oracle already fight for the same dollars

Terrestrial data center math

-Freda Duan bottom-up: 325k Nvidia GPUs across Colossus 1 and 2, blended $5.33/hr, ~590MW facility power at 1.2 PUE for the Anthropic deal

-Implies ~$25B revenue/GW against ~$29B/GW to build (ARK estimate of Colossus costs)

-Payback near 1.2 years before opex, 55% IRR if the contract renews [on Colossus 1]

-Elon flagged the Anthropic deals short term, and the $8/hr GB200 rate for Colossus 2 compresses as supply expands, which the bull case underweights

-The $50B /GW Google figure has no equivalent bottom-up build, it sits as a residual on the scatter plot [one thing I thought was interesting, though, by their own admission Google is likely buying optionality to be first on the orbital DCs IF they work and come online fast enough so anchoring to the same revenue/GW they signed at doesn't seem like a usable datapoint and is rather an outlier given it's a call option]

Orbital compute

-Fox puts orbital capex at ~$5B/GW versus $20-25B/GW terrestrially, a 5x cut on roughly half the bill of materials

-Built off 100 tons and ~5MW of compute per Starship launch at a $250/kg target, versus ~$1,500/kg on Falcon today

-Requires two-stage reusability, never demonstrated, with a second-stage return attempt later this year

-Ignores satellite failure rates, radiative cooling mass and orbital power intermittency in LEO

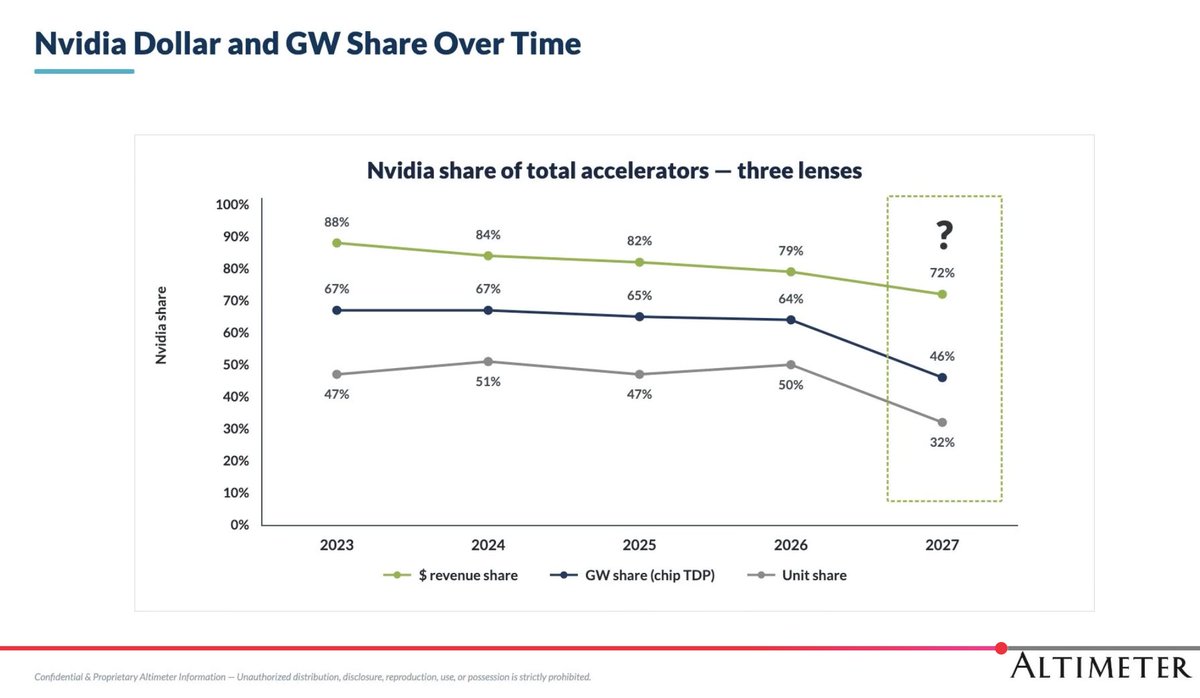

Nvidia share

-Altimeter's own chart steps Nvidia 2026 to 2027E down across all three lenses: revenue 79% to 72%, GW share 64% to 46%, unit 50% to 32%, with the 2027 column flagged with a question mark.

-GW share falls harder, 64% to a projected 46%, and unit share drops 47% to 32%

-Revenue share holds up better than units because Nvidia chips cost more, so ASIC unit gains don't convert to dollar losses one for one

-Baker's "maintained share handsomely" line is softer than the Altimeter slide, and the 2027 step down assumes ASIC ramp at a pace with no precedent

-Jensen's argument: tokens per watt is revenue, so a cheaper ASIC saves capex but yields less revenue in a watt-constrained world

Model frontier economics

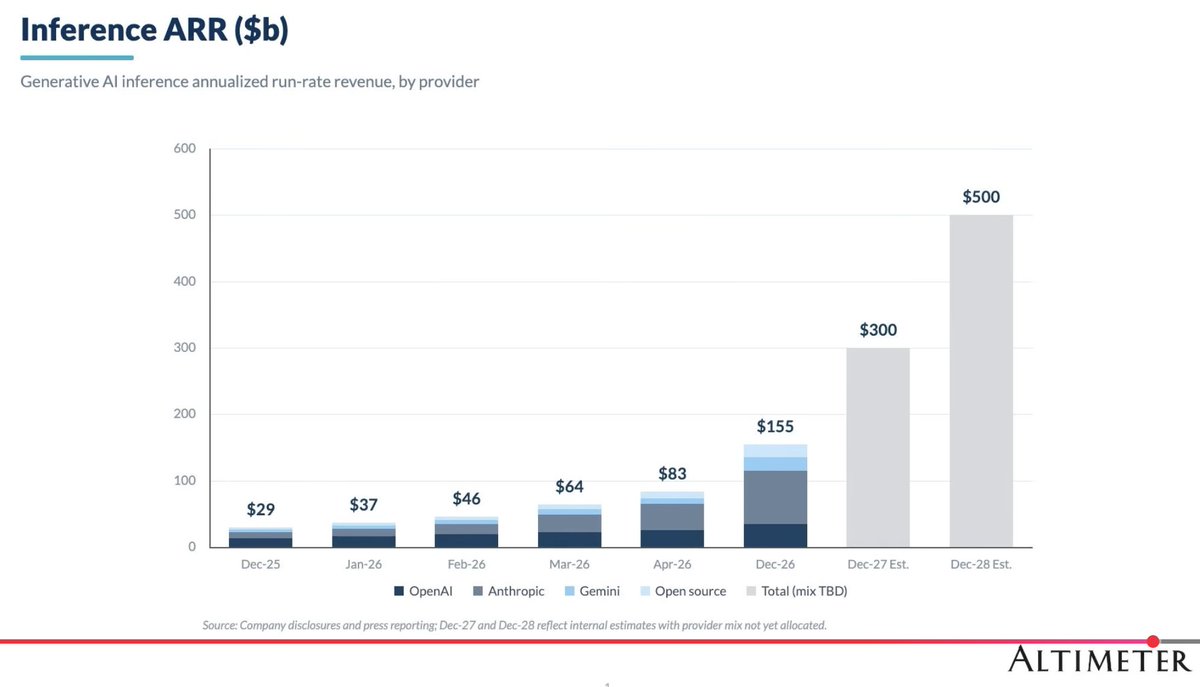

-Inference ARR went $29B (Dec-25) to $83B (Apr-26), roughly 3x in five months

-Internal estimates of $155B at year-end 2026, $300B in 2027, $500B in 2028, with the outer years top-down and provider mix unallocated

-Morgan Stanley 2027 capex at $1.1T, Gerstner closer to $1.5T including SpaceX and CoreWeave

-At 60-70% gross margin the capex against revenue maths, but the $300B and $500B targets carry no bottom-up build

-Monetization per GW is rising from ~$20B to $30-40B, what they call accidental profitability from demand outrunning supply [think this is the biggest jump in assumptions]

Frontier versus open source

-Closed frontier models captured roughly 90% of AI economic value in H1 2026, against consensus that cheap open-source tokens would converge

-Baker's split: frontier keeps the revenue, open source takes most of the tokens

-Harvey example: an open-source base plus proprietary RL and a router beat Opus 4 at lower cost, while still consuming heavy Opus volume

-Stronger open source is bullish for compute because it pushes margin out of models and into hardware

-Jensen could ship a frontier open-source model whenever he chose, Nemotron is already efficient, so it reads as a business choice not a capability limit

BG2 w/ Gavin Baker. The SpaceX IPO, Fable 5 / Mythos, AI Capex Update & Market Check. 🚀💰 @BG2Pod @altcap @GavinSBaker @_clarktang

8

40

293

81,024

Thomas Power retweeted

CNBC Halftime Scott Wapner (@TheJudgeCNBC) asked Brad Gerstner (@altcap) why the @SpaceX valuation ultimately comes down to compute. Brad pointed to a recent post from Noam Brown (@polynoamial) arguing that current models can solve almost any problem if given enough run time.

"We are out of compute in this country… The world is going to be massively consumptive of compute."

@CNBC Halftime Report with Altimeter founder & CEO Brad Gerstner (@altcap) and Scott Wapner (@TheJudgeCNBC) | June 12, 2026

On the day of the @SpaceX IPO, key takeaways:

- SpaceX appears on track to become one of the largest AI hyperscalers in the United States

- The world is running out of compute, and SpaceX is potentially best positioned to build it

4

10

126

102,493

BG2 w/ Gavin Baker. The SpaceX IPO, Fable 5 / Mythos, AI Capex Update & Market Check. 🚀💰 @BG2Pod @altcap @GavinSBaker @_clarktang

49

65

771

9,251,227

Twill77 retweeted

Jun 12

#1 Hyperscaler by 2028 @SpaceX then 1000x more compute than the entire Internet of Humans. 4 years ago, most thought I am crazy except few. Crazier @elonmusk today added $2T soon Quadrillions as the Internet Of AI is just about to begin.

Mar 28

Love @elonmusk or hate him, you will soon realize, shifting the focus of compute towards space is on its own rescuing your civilization and will be more valuable when every AI agent collaborates securely with ZERO third party dependencies. @Hypercycle_AI

1

24

49

1,128

chicken salad deluxe retweeted

Jun 15

A country of founders free & courageous enough to take the first step. Embracing risk. Pursuing dreams. Beyond the coercive hand of gov’t that crushes dreams around the world. This IS the American DNA - a golden formula that binds the generations. 🇺🇸🚀

UFC

UFC

22

98

1,103

52,818

10h

The bear case misses that SpaceX isn't just a rocket company - it's a logistics platform.

Starlink already prints money, Starship drops launch costs 10x, and they own the rails to space.

Every competitor is a decade behind on reusability.

91

ranksXBT 👾 retweeted

Scott Wapner (@TheJudgeCNBC) asked Brad Gerstner (@altcap) to respond to the bear case on @SpaceX after CFRA issued a sell rating on the stock's first day of trading.

"In technology, a lot more money has been lost sitting on the sidelines, wringing your hands about all the things that can go wrong rather than betting on the upside."

CNBC Halftime Scott Wapner (@TheJudgeCNBC) asked Brad Gerstner (@altcap) why the @SpaceX valuation ultimately comes down to compute. Brad pointed to a recent post from Noam Brown (@polynoamial) arguing that current models can solve almost any problem if given enough run time.

"We are out of compute in this country… The world is going to be massively consumptive of compute."

7

5

98

81,560

Gustaf retweeted

Scott Wapner (@TheJudgeCNBC) asked Brad Gerstner (@altcap) about @elonmusk's wealth crossing $1 trillion on @SpaceX IPO day. Brad connected the moment to why @InvestAmerica24 exists.

"60 to 70% of people today don't compound in the upside of our capital markets. I think you'll see a lot of announcements in the weeks ahead."

Scott Wapner (@TheJudgeCNBC) asked Brad Gerstner (@altcap) to respond to the bear case on @SpaceX after CFRA issued a sell rating on the stock's first day of trading.

"In technology, a lot more money has been lost sitting on the sidelines, wringing your hands about all the things that can go wrong rather than betting on the upside."

3

2

26

8,413