Jun 12

Proud to see Atul Greentech featured in The Telegraph UK's story on India's electric tuk-tuk revolution.

A recognition of India's growing impact in sustainable mobility and electric three-wheeler innovation.

Read More:

telegraph.co.uk/global-healt…

#AtulGreentech #AtulAuto

1

68

Vijay Kedia:

😊 SMILE [Small Size Extra Large TAM] isn't just a framework. It's a time machine.

📌 Atul Auto → 5,600% (held through years of zero action)

📌 Cera Sanitaryware → ~16,000x (since 2004!)

📌 TAC Infosec → ongoing SaaS bet before the narrative

🎯 He doesn't buy what's big. He buys what will be big.

🚪 Exits only when the TAM [Total Available Market] shrinks.

Otherwise:

Sits still.

Small size.

Large ambition.

Extra-large patience. 💡

#VijayKedia #SMILEInvesting #AtulAuto #CeraSanitaryware #TACInfosec #TACINFOSEC #KediaPortfolio #MultibaggerStocks

1

1

470

Jun 11

#VijayKedia

Top holdings

#AtulAuto ₹258 Cr,

#NeulandLaboratories ₹220 Cr, #EleconEngineering ₹118 Cr, #SudarshanChemical ₹87 Cr,

#Yatharthhopital ₹81 Cr,

#Vaibhavglobal ₹75 Cr,

#Mahendraholiday ₹46 Cr,

#websolenergy ₹41 Cr,

Showcasing his diversified long-term investment strategy across pharma, chemicals, engineering, healthcare and niche businesses.

Do you holding any stocks in this list

1

1

152

Jun 11

New swing entry in Atul Auto

Slowly building position, I may average it down. Holding period: 2-4 weeks.

#Atulauto

1

298

Jun 9

#atulauto - !𝐀𝐭𝐮𝐥 𝐀𝐮𝐭𝐨 𝐋𝐢𝐦𝐢𝐭𝐞𝐝!

🔔 Order Type: New Order | 💰 Event Value: ₹490.5 Cr

🏗️ Market Cap: ₹1280 Cr | 🏷️ Stock PE: 30.30

🧾 Revenue (Qtr|Last Year): ₹240 Cr | ₹824 Cr

💡 Atul Auto secured a ₹490.50 Crore contract from Exponent Energy to supply 15,000 electric three-wheelers over three years. This partnership significantly expands its EV manufacturing footprint.

#bse #nifty #nse #stockmarket

1

249

Jun 1

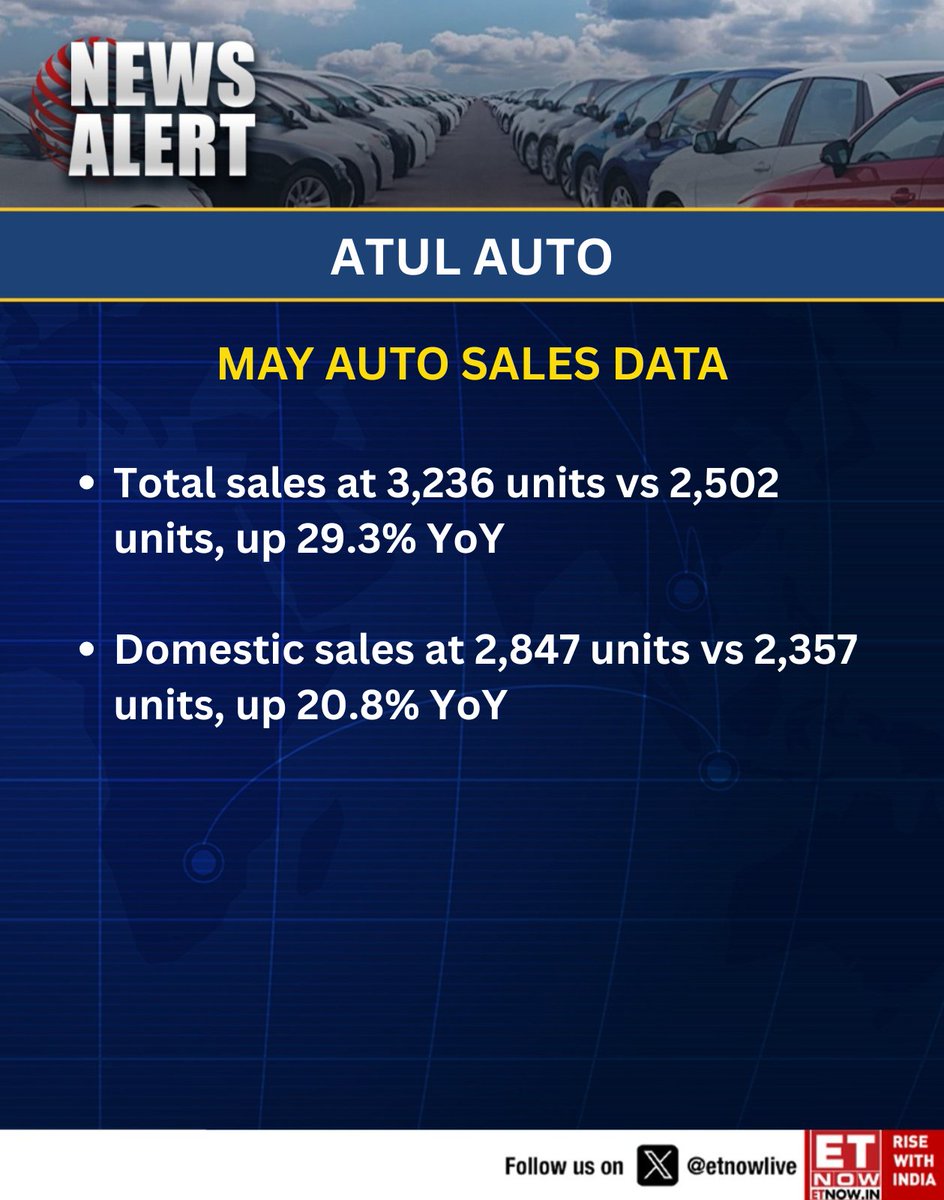

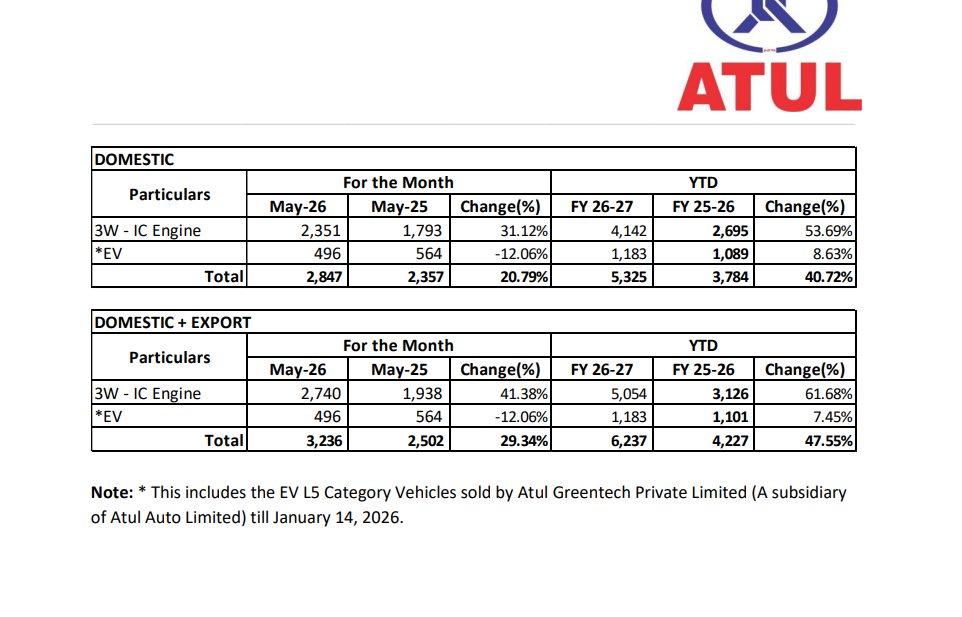

#NewsAlert | May Auto Sales: Atul Auto

Total sales at 3,236 units vs 2,502 units, up 29.3% YoY

#Auto #Autosales #StockMarket #ATULAUTO

1

6

1,193

Jun 1

#MayAutoSales | #AtulAuto;

Total Sales Up 29.3% At 3,236 Units Vs 2,502 Units (YoY)

1

15

4,479

May 29

Nifty 23750-23700

making bull hedges as on 9 june in nifty decline

its not blind buy, its hedge if you dont understand, then avoid

#nifty50 #options #call #put #breakoutstocks #parasdefence #apollo #grse #premierexplosive #jayantorganics #parasdefence #geshipping #refex #chalet #atulauto #jindalworld #jamnaauto #ricoauto #atgl

2

499

May 27

Rly for tom, track all by 3.28 n then decide

#nifty50 #options #call #put #breakoutstocks #parasdefence #apollo #grse #premierexplosive #jayantorganics #parasdefence #geshipping #refex #chalet #atulauto #jindalworld #jamnaauto #ricoauto #atgl

2

637

May 19

3

601

May 19

#VIEW

holding since 1-2 months now

hardly 20 Rs up from cost 😂😂

but atleast up, yahi bahut hai

#nifty50 #options #call #put #breakoutstocks #parasdefence #apollo #grse #premierexplosive #jayantorganics #parasdefence #geshipping #refex #chalet #atulauto

2

792

May 19

#GESHIP

1500 to 1760 in one session

#nifty50 #options #call #put #breakoutstocks #parasdefence #apollo #grse #premierexplosive #jayantorganics #parasdefence #geshipping #refex #chalet #atulauto

May 18

#GESHIP

dhoond lo PF mai

kis kis ke pas 😅😅 indicated just yesterday

#twl #jupiterwagons #nifty50 #options #call #put #breakoutstocks #parasdefence #apollo #grse #cochinshipyard #fsl #premierexplosive #jayantorganics #parasdefence #geshipping #refex #chalet #atulauto

2

663

May 19

#GNFC

excellent results with great dividend

#nifty50 #options #call #put #breakoutstocks #parasdefence #apollo #grse #premierexplosive #jayantorganics #parasdefence #geshipping #refex #chalet #atulauto

2

440

May 18

May 18

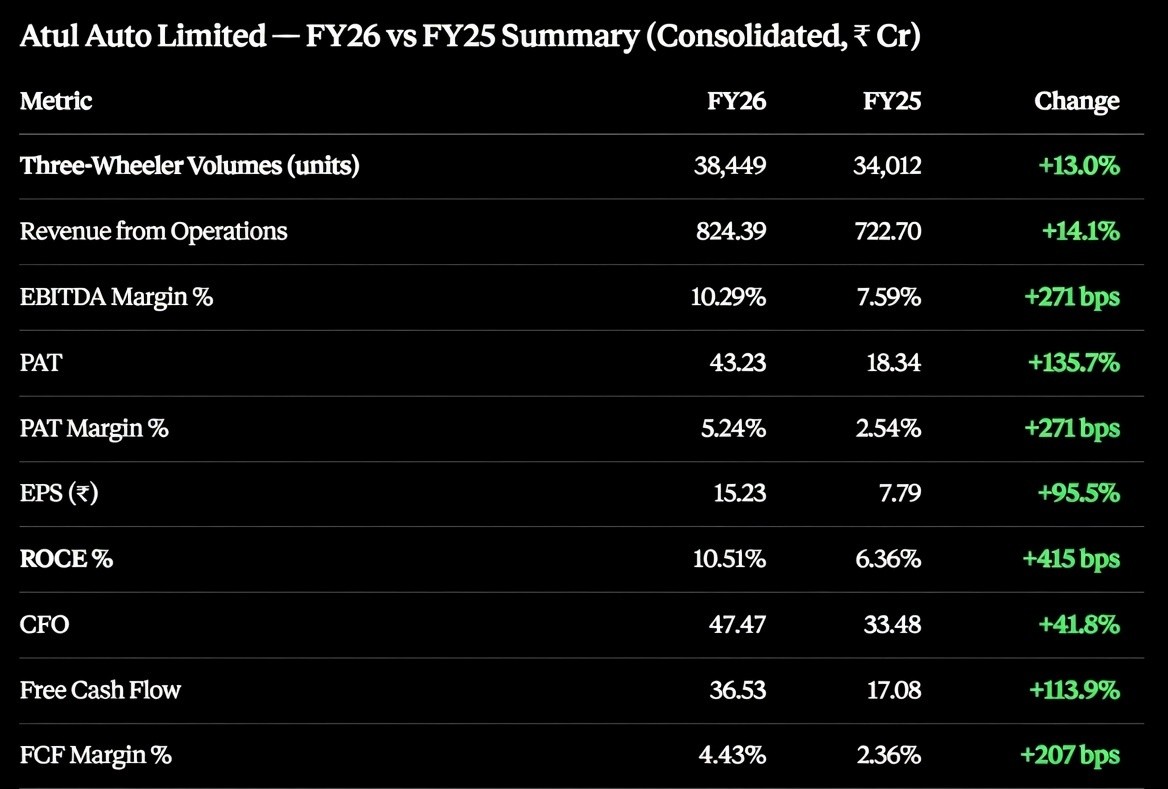

#ATULAUTO: PAT 136%. ROCE Doubled. FCF Positive. Why Atul Auto Has My Attention.

What Company does? Atul Auto makes three-wheelers -passenger and cargo auto rickshaws

The FY26 results just dropped. And they're loud 👇

✅ Volumes: 38,449 units, up 13%. Real demand, not pricing tricks.

✅ PAT more than doubled: ₹18 Cr → ₹43 Cr

✅ EBITDA Margin: 10.29% vs 7.59% ( 271 bps)

✅ ROCE jumped from 6.4% → 10.5%

✅ Free Cash Flow doubled - cash generation doubled, not just paper profits.

✅ Debt/Equity at just 0.29x - virtually debt-free balance sheet

A clean balance sheet doubling profits expanding margins improving cash generation.

My take 📈

A company growing PAT over 100%, with margins expanding, D/E of just 0.29x, and trading at a PE of ~33?

That's not expensive. That's mispriced. It's a BUY.

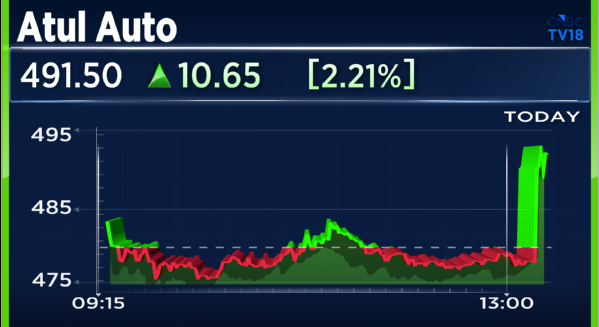

🟢 Entry: Added at ₹495 for long term

🛑 Stoploss: ₹470

🎯 View: Long term hold

Disclaimer: This is my personal view, not investment advice. Markets are risky. Do your own research before investing.

3

1,307

May 18

NIFTY23500

recovered 200 points, koi shaq

But people beleives only on fake astrologers and experts

#twl #jupiterwagons #nifty50 #options #call #put #breakoutstocks #parasdefence #apollo #grse #cochinshipyard #fsl #premierexplosive #jayantorganics #parasdefence #geshipping #refex #chalet #atulauto

May 18

NIFTY23300

support 23000-22800, making few bull hedges 26 May expiry n 2 June.

2

419