Jun 13

Before they took fable away, I had it create a OG Blockstack inspired p2p network for terminal apps. UUIDs and profiles handled by STX, optional payments w/ stx, but the rest libp2p

Anyone in the STX world interested in playing with it?

Fable walked so Opus can run.

1

4

346

Jun 13

I actually had it build a stx thing that has nothing to do with defi.

Not sure how to explain it well, but it’s a p2p network that lets you host/run terminal apps. Think og blockstack, but term not web (at least for now), and p2p

It’s neat.

1

1

43

Jun 11

Lol, you might be very new to STX.

Check when algorithm.btc started in Stacks.

I’m from blockstack era.

Since you didn't lose money on STX, curious why you are taking an interest in talking bad about it?

3

23

May 26

O endereço 1111111111111111111114oLvT2 é da blockstack, ele serve justamente para proof of burn, ou seja, para queimar BTC, esse saldo nunca mais poderá ser movimentado.

2

141

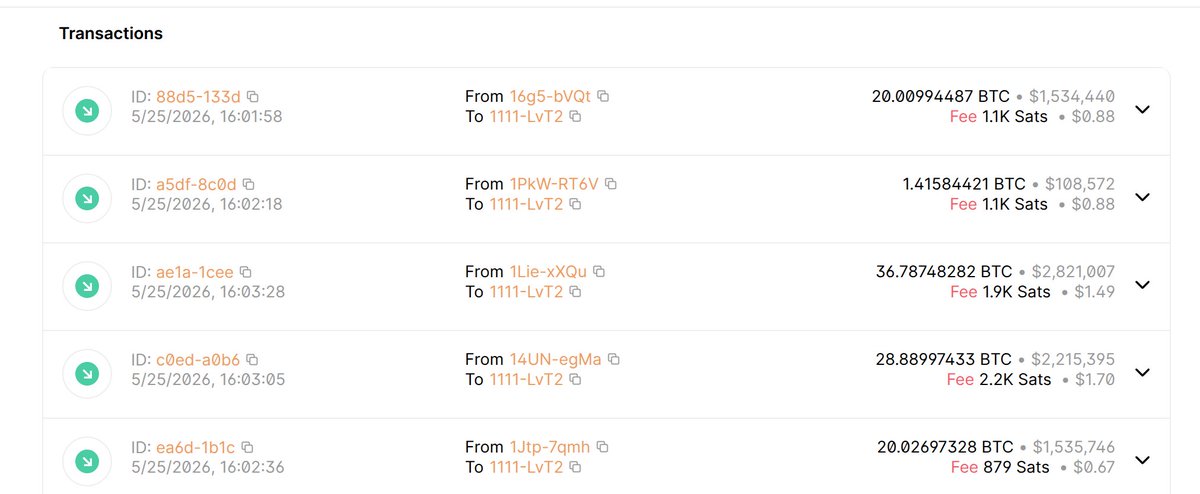

May 26

107 BTC (~$8.2M) just got permanently deleted from Bitcoin.

Someone sent 107 Bitcoin across five separate transactions to the address:

1111111111111111111114oLvT2

This isn’t just any address.

It’s one of Bitcoin’s oldest and most famous burn addresses. Its Hash160 is literally all zeros (0000000000000000000000000000000000000000).

Finding a private key for it is considered computationally impossible. Once BTC lands here — it’s gone.

Forever.

This address has been used since at least 2015 as a proof-of-burn address (originally by Blockstack/Stacks). Over the years it has already “eaten” hundreds of BTC.

But today’s move stands out:

107 BTC in just a few transactions

No obvious reason

No public explanation

Was it:

-A massive accidental send?

-An intentional sacrifice / protest?

-Someone cleaning up dirty coins?

-A very expensive way to make a statement?

We’ll probably never know.

What we do know: in a world where people fight over every satoshi, someone just decided that $8.2 million should disappear from circulation permanently.

This is Bitcoin’s brutal honesty in action — absolute scarcity, absolute finality.

The question is… why now?

4

175

May 26

Yep, that actually happened today 👀

What went down:

• An anonymous wallet sent 107.13 BTC (∼$8.2M - $8.3M) to the famous Bitcoin burn address 1111111111111111111114oLvT2

• It happened across 5 separate transactions confirmed in block 950962 on May 26, 2026

• That burn address is a vanity address with no known private key - so anything sent there is provably unspendable and permanently removed from circulation

Context:

1. How much supply is that? Bitcoin has ∼19.6M coins circulating. 107 BTC = 0.0005% of supply, so the market impact is tiny. But it’s still $8M gone forever.

2. Not the first time: That burn address now holds 807 BTC total from years of similar sends. People often send dust there to timestamp messages on-chain.

3. Why would someone do it? Nobody knows yet. Theories floating around:

○ Statement/protest - burning BTC increases scarcity for everyone else

○ Proof-of-burn mechanism - some projects like early Blockstack used it

○ Mistake - though 5 separate txs makes that unlikely

○ Quantum bounty - Adam Back joked it could be an "accidental quantum bounty"

○ Mt. Gox links - AMLBot claimed some wallets were tied to historical Mt. Gox addresses, but nothing confirmed

Trezor even replied to the news with an Elmo-in-fire meme 🔥

Burning BTC is like mailing cash into a black hole. The coins exist on-chain, but no one can ever spend them again.

3

371

May 14

no offchain value would be like Blockstack revenues being used to buyback and burn BTC and that being the primary reason people buy BTC

2

109

May 1

$STX

Stacks : Bitcoin Üzerinde Programlanabilir Finans ve BTCFi Uygulama Katmanı

Marketcap: 402m$, FDV: 402m$

Stacks, Bitcoin’in güvenliğini temel alan ve Bitcoin üzerinde akıllı kontratlar, merkeziyetsiz uygulamalar ve DeFi kullanım alanları oluşturmayı hedefleyen bir Bitcoin Layer-2 / Bitcoin execution layer altyapısıdır.

Akademik konumu:

Bitcoin-secured smart contract and application execution layer

Problem Tanımı

Temel araştırma sorusu:

Bitcoin’in güvenlik modeli korunurken, BTC üzerinde programlanabilir finansal uygulamalar geliştirilebilir mi?

Çözüm Yaklaşımı: Stacks Modeli

Stacks bu problemi üç temel mekanizma ile ele alır.

1. Proof of Transfer (PoX)

Stacks’in en özgün mekanizması Proof of Transfer modelidir. PoX’ta miner’lar STX kazanmak için BTC harcar; bu BTC, STX kilitleyen stacker’lara ödül olarak aktarılır. Böylece Stacks ekonomisi doğrudan Bitcoin ile bağlantılı hale gelir. Stacking, STX sahiplerinin tokenlarını non-custodial biçimde kilitleyerek BTC ödülü kazandığı yerleşik mekanizmadır; STX cüzdandan çıkmaz, yalnızca protokol seviyesinde kilitlenir.

2.Nakamoto Upgrade

Nakamoto upgrade, Stacks’in teknik tarihinde en önemli kırılmalardan biridir. Q4 2024’te gerçekleşen bu güncelleme ile Stacks, Bitcoin bloklarına bağımlı yavaş blok üretim modelinden ayrılarak saniyeler seviyesinde blok üretimine geçti. Aynı zamanda Stacks işlemleri için 0 Bitcoin finality hedefi getirildi; yani onaylanmış bir Stacks işlemini geri almak Bitcoin işlemini geri almak kadar zor hale getirildi.

Bu upgrade üç şeyi güçlendirdi:

Daha hızlı işlem onayı

Bitcoin finality

Bitcoin miner MEV riskinin azaltılması

Bu nedenle Nakamoto, Stacks’i yalnızca Bitcoin’e bağlı bir yan ağ olmaktan çıkarıp, BTCFi için daha ciddi bir execution layer konumuna taşır.

3. sBTC

sBTC, Stacks’in BTCFi anlatısındaki en kritik üründür. Stacks Foundation’a göre sBTC, BTC’nin DeFi uygulamalarında kullanılabilmesini sağlayan 1:1 Bitcoin temsili varlık modelidir. Amaç, BTC’yi merkezi saklayıcıya veya tek bir aracıya bağımlı olmadan lending, trading, ödeme ve yield uygulamalarına taşımaktır.

sBTC’nin stratejik anlamı:

Bitcoin likiditesini satmadan veya merkezi saklayıcıya bırakmadan uygulama katmanına taşımak.

Teknik Mimari

1. Execution Layer

Uygulamalar Stacks üzerinde çalışır

Settlement Bitcoin’e bağlıdır

2. Clarity Smart Contract Language

Deterministik

Hüvenlik odaklı

Analiz edilebilir

3. Stacking Mekanizması

STX kilitlenir

Karşılığında BTC ödülü alınır

Önemli fark:

Staking ödülü STX değil, BTC’dir.

Ekosistem ve Kullanım Alanları

Stacks’in kullanım alanları BTCFi ekseninde yoğunlaşır:

BTC lending

BTC collateralized stablecoin loans

DEX ve swap işlemleri

Bitcoin tabanlı DAO treasury yönetimi

BTC ile yield üretimi

NFT ve creator uygulamaları

sBTC sayfası, BTC sahiplerinin lending, DEX ve yield gibi zincir üstü uygulamalara erişmesini hedeflediğini açıkça vurgular.

Ekip, Geçmiş ve Kurumsal Konum

Stacks’in kökeni Blockstack dönemine dayanır. Proje 2019’da ABD SEC tarafından Regulation A kapsamında nitelendirilmiş ilk token offering örneklerinden biri olarak dikkat çekmiştir. Blockstack’in Reg A satışı yaklaşık 40m$ token offering olarak kamuya sunulmuş ve dijital varlıkların düzenleyici uyum içinde dağıtımı açısından sektör için önemli bir örnek oluşturmuştur.

Token Ekonomisi

STX’in Fonksiyonları:

STX tokeni üç ana işlev görür:

İşlem ücretleri

Stacking yoluyla ağ katılımı

Bitcoin ödül mekanizmasına katılım

Rekabet Analizi

Stacks’in rekabet ettiği alan BTCFi execution layer segmentidir.

Başlıca rakipler:

Rootstock

Merlin Chain

Fark: Stacks, BTCFi’nin execution ve application layerı

Benim yorumum

Teknik olarak → Bitcoin’e bağlı smart contract execution layer

Ekonomik olarak → PoX ile BTC-STX teşvik döngüsü

Stratejik olarak → BTCFi uygulama katmanı

Kurumsal olarak → regülasyon geçmişi olan olgun Bitcoin altyapısı

Stacks, Bitcoin’i değiştirmeden Bitcoin’in ekonomik kapasitesini genişletmeye çalışan en önemli BTCFi altyapılarından biridir.

8

12

387

Apr 18

equity securities are great (esp if tokenized!), utility/meme tokens are great, but the one thing you can do with securities that you can't do with utility/meme tokens is give holders real, direct economic rights

if you give such rights to tokenholders, then the utility/meme tokens are themselves securities or every sale/purchase of them will be a securities transaction

this is a red line that imo will never be legally crossed, because crossing it would be the same thing as abrogating the securities laws wholecloth (or making them "opt-in"...same thing, since no one would opt in)

many of us have worked very hard to at least help Congress and regulators understand that tokens having governance rights within a system that includes entities shouldn't cross that red line--that's something! you can see it spelled out clearly in most of the CLARITY Act drafts

it hopefully means, for example, that tokenholders via voting could have influence over who comprises the board of a grants BORG funded by a DAO, or a BORG that holds critical DAO-related IP and what it does with that IP, etc., without rendering the tokens or most transactions in the tokens securities...

but those are governance rights/powers...not directly economic!

in contrast, a business entity will never legally be allowed to give tokenholders dividend or M&A payment rights, for example...the moment it does, they would become securities, with all the illiquidity etc. burdens of securities

and no, I don't believe the complicated schemes from projects I won't name, claiming "oh yes the tokens give you economic rights, but only if one person holds at least 30% of them", are going to be permitted/legal...in the U.S., imo, they are clear wink-wink/nudge-nudge securities law evasion schemes and run afoul of all the anti-evasion rules, at minimum, and probably a lot more than that (tender offer rules, swaps rules, etc.)

and people who think these projects have some genius loophole figured out should ask themselves: why doesn't the launchpad entity pushing the model use it first and foremost for its own token? supposedly it gives holders almost all the economic benefits of equity with none of the securities law burdens...that should be a total no-brainer for any company...they should be dogfooding it, raising their own rounds structured this way, proving it's legally sound by taking the risk themselves first...but they don't, and won't, because they (or their lawyers) know better...which tells you everything...

in the U.S. we have the most pro-crypto SEC, regulators, and politicians we are ever going to get, and they are not saying anything different...they are not proposing to make the securities laws opt-in by letting tokens have dividend rights etc....read their last statement, it does not say this or anything like this, it actually says the opposite, and every time it mentions non-securities tokens, it stresses that they "do not have any rights or interest in or with respect to a business enterprise or other entity, promisor, or obligor" or "intrinsic economic properties or rights, such as generating a passive yield or conveying rights to future income, profits, or assets of a business enterprise or other entity, promisor, or obligor", but rather at most have "a limited license or other intellectual property rights" for collectibles or "governance rights with respect to the associated functional crypto system", etc.

you can hate it, you can wish it were different, you can build complicated financial rube goldberg evasion schemes with offshore entities that won't stand the test of time...but imo the red line of 'no economic rights in a business enterprise for tokenholders' is real and here to stay

we have pushed things as far as they are going to go short of simply canceling the securities laws entirely, and should be amazed we got as far as we did without a lot more people ending up fined or in prison

conversely though, I'm not sure people *should* hate this status quo...because the other side of the coin [sic.] is that securities are not very good at accruing value from trustless systems, being pure bearer assets, being used in remittances, powering cypherpunk apps, etc....they have too many offchain dependencies and are too bound up with the legal system...they cannot be predicates of "autonomousness" in the DAO sense of "autonomous"

so imo, both securities (tokenized or not) and non-securities tokens have important and distinctive mechanisms of value accrual, and we need both in general, and many projects need or should want both...

I totally understand people may not want the brain damage of trying to navigate both, or figure out how to hold both, and I also super appreciate teams that push the envelope to make their token as valuable and trustworthy as possible, but disregarding every dual equity/token project as a scam or as bad means:

--> you would've missed out on BTC because it's also possible to own Blockstack equity & they could theoretically pvp

--> you would've missed out on ETH because it's also possible to own Consensys equity & they could theoretically pvp

--> you would've missed out on BNB because it's also possible to own Binance equity & they could theoretically pvp

--> you would've missed out on UNI, AAVE & others because it's also possible to own equity in their Labs companies

moreover, even most projects that don't have an equity issuing labs company could form one at any time, and that could pvp the token...we saw this, for example, with SushiSwap and other notorious 'DAO takeovers'....

you can see this exact debate playing out live right now with @pumpcade...@PopPunkOnChain raised ~$6M of equity across two rounds while the $PUMPCADE token was live and trading, and the discourse around it basically is the debate this post is about...I don't have a strong take on that specific cap table and I think the team deserves credit for building a real product in public, but the fact that the whole space is arguing about it proves the point: dual equity/token is here, it's structural, and the answer is better tools--not pretending the question away...

the only exception to that risk I know of is @MetaDAOProject, which requires projects that launch on it to prohibit equity issuance via a @MetaLeX_Labs integration...so if you're bullish on that model, great, you have an awesome option with a top-tier elite team and community trying to make it as scalable and trustworthy as the law allows...

but there is not one size fits all...and, most importantly, there is a lot more we can do to make sure as many people as possible have access to actual securities--for example, last week at MetaLeX we launched ACE so more people can hold both securities and tokens like VCs do....it also adds more covenants and transparency for how teams manage token treasuries, and there are even more ways projects and communities could keep improving that aspect...@AragonProject's and @DefiLlama's recent token ratings schemes are another push in the right direction...

....overall, we're talking about corporate finance and project finance....having lots of options is good, is not ideological, and certainly is not zero-sum, as projects that make sense for a dual equity/token structure are likely not the ones that could go token-only...and vice versa, many projects (eg a new blockchain) do not make sense to accrue value to securities...

17

8

65

10,403

Mar 26

@zeroauthdao がStacks年表をポストしていたので紹介させて頂きます。

これはテストに出るのでメモしておきましょう🧐📝

ty!

---

Stacksの歴史、年ごとの歩み👇

2013年 — Bitcoin上でスマートコントラクトを稼働させる構想が始まる

2014年 — Y Combinator(Yコンビネータ)に参加

2015年 — 初期のプロトコル研究と開発

2016年 — Bitcoin開発者コミュニティで機運が高まる

2017年 — SEC(米国証券取引委員会)初認可のICOを実施(当時の名称:Blockstack)

2018年 — ホワイトペーパーの公開とテストネットの進化

2019年 — SEC認可に関する重要なマイルストーンを完了

2020年 — Stacks 2.0テストネット稼働 + PoXの設計

2021年 — メインネットローンチ(Stacks 2.0)

2022年 — エコシステムの成長(dApps、NFT、DeFiの拡大)

2023年 — sBTCの導入発表 → Bitcoin DeFi時代の幕開け

2024年 — sBTCの進展 + ロードマップの拡大

2025年 — Bitcoinアプリのスケーリング(拡張)と普及

2026年 — Stacksを通じて参加者に分配されたBitcoinが累計4,000 BTCを突破

Mar 26

Stacks history, year by year 👇

2013 — smart contracts on Bitcoin thesis begins

2014 — joins Y Combinator

2015 — early protocol research development

2016 — builds momentum in Bitcoin dev circles

2017 — first SEC-qualified ICO (Blockstack)

2018 — whitepaper testnets evolve

2019 — SEC qualification milestone finalized

2020 — Stacks 2.0 testnet PoX design

2021 — mainnet goes live (Stacks 2.0)

2022 — ecosystem growth: apps, NFTs, DeFi

2023 — sBTC introduced → Bitcoin DeFi era

2024 — sBTC progress roadmap expansion

2025 — scaling Bitcoin apps adoption

2026 — 4,000 Bitcoin distributed to participants via Stacks

A decade of building on Bitcoin and we’re still early⚡️⚡️

1

2

114

Mar 26

Stacks history, year by year 👇

2013 — smart contracts on Bitcoin thesis begins

2014 — joins Y Combinator

2015 — early protocol research development

2016 — builds momentum in Bitcoin dev circles

2017 — first SEC-qualified ICO (Blockstack)

2018 — whitepaper testnets evolve

2019 — SEC qualification milestone finalized

2020 — Stacks 2.0 testnet PoX design

2021 — mainnet goes live (Stacks 2.0)

2022 — ecosystem growth: apps, NFTs, DeFi

2023 — sBTC introduced → Bitcoin DeFi era

2024 — sBTC progress roadmap expansion

2025 — scaling Bitcoin apps adoption

2026 — 4,000 Bitcoin distributed to participants via Stacks

A decade of building on Bitcoin and we’re still early⚡️⚡️

6

11

41

1,523

✅筋トレ

✅Shopifyアプリ開発:40m

・商品リストにリアルタイム検索機能を追加(filterメソッド活用)

・BlockStackによるコンポーネント間の余白調整

#デイトラコミュニティ

16

353

Mar 15

This is very good and may prove to be the post mortem when it's all said and done.

Once "crypto" is dead and buried, maybe there can be a return to Gaia and other decentralization efforts that attracted many of us to "blockstack" in the first place.

It's never been more needed

Mar 8

I joined Blockstack in 2018 for the developer tools. Seven years later I left with a clear picture of what happens when token dynamics replace product feedback loops. Not a failure of people. A failure of incentive structure.

markmhendrickson.com/posts/w…

1

6

311

Mar 12

Throwback Thursday

Found this old Blockstack token voucher from the early days.

Fast forward to today and we’re now settling transactions on @Stacks for the @dataing_io data marketplace.

1,000,000 TX is light work, we're shooting for trillions. @toony1908 @MarkKilaghbian

3

5

144

Took some time to read through. As an original investor in Blockstack, I had high hopes for a new and better way for people to identify and transact. So much has been achieved but the incentive structure is perhaps the biggest learning for those building today. We’re still early

2

104

Mar 8

I joined Blockstack in 2018 for the developer tools. Seven years later I left with a clear picture of what happens when token dynamics replace product feedback loops. Not a failure of people. A failure of incentive structure.

markmhendrickson.com/posts/w…

15

7

50

4,243