Mar 10

What is Aehr Test Systems? $aehr is a company that builds special tough-testing machines for computer chips — the kind that go into phones, electric cars, huge AI supercomputers, and data centers that power things like ChatGPT.

Think of chip factories cranking out thousands of super-tiny chips all together on one big, thin, round disc called a wafer (like a giant pizza with tons of mini pepperonis that are actually the chips).

Before those chips get sliced up, packaged, and shipped to make your gadgets work, they have to pass a really strict “final exam.” Aehr’s machines run this exam by:

• Testing them to see if they do what they’re supposed to (like running programs, handling power, or sending light signals).

• Burning them in — stressing them out with high heat, high voltage, and full-speed operation for hours or days. This forces any weak or faulty chips to fail right now in the factory (instead of failing later when someone’s using them in a car or AI server, which would be way more expensive and dangerous to fix).

Their coolest machines are in the FOX family:

• FOX-XP — the powerhouse one. It can test and stress up to 18 full wafers at once (or 9 in some high-power setups for the newest tough chips). That’s like checking thousands or tens of thousands of chips all together super efficiently. It’s perfect for the hardest jobs, like powerful chips for electric cars (silicon carbide or gallium nitride ones that handle tons of electricity without wasting energy), light-based chips (photonics for super-fast data), and the advanced processors that run massive AI training in data centers.

• FOX-NP — a smaller, cheaper starter version that’s fully compatible with the big one. Great for testing smaller batches or new chip designs before going full speed.

• FOX-CP — even simpler and lower-cost for basic chips like memory, phone sensors, or logic parts — it handles one wafer at a time but still does the full test-and-stress routine.

They also make special contact tools called WaferPak (like a giant precise touch-screen that gently presses thousands of tiny probes onto every spot on the wafer at once without damaging anything) and auto-loaders to make the whole process hands-free in big factories.

Why is this a big deal?

AI companies and electric car makers need chips that are rock-solid reliable — one bad chip in a giant AI cluster or a car’s power system could cause huge problems or cost millions. Aehr’s machines catch the duds early, save factories tons of money (cheaper to fix before packaging), help chips last longer in real life, and make production faster/cheaper overall.

So basically: Aehr doesn’t make the chips themselves — it makes the super-strict quality-control gym that every important chip has to survive before it gets to power your future tech. Without machines like these, the world of fast AI, self-driving cars, and efficient EVs would be a lot slower and less trustworthy. Pretty essential behind-the-scenes hero stuff! ⚡🚗🤖 #POETTechnologies #AehrTest #Photonics #OpticalInterposer #Semiconductors #AIInfrastructure #DataCenter #SiliconPhotonics #ChipTesting #BurnInTesting #FOXSystem #WaferLevelTesting #5G #LIDAR #EdgeComputing #PowerSemiconductors #SiliconCarbide #GalliumNitride #AIchips #NextGenChips #TechStocks #SemiconductorIndustry #Optics #PhotonicsIntegration

2

171

The Reliability Guard: Why $AEHR is the Invisible Gatekeeper of the AI Supercycle

In the high-stakes race for AI dominance, the industry has hit a physical wall: Thermal Infantile Mortality.

As chip power consumption moves toward the kilowatt range, the risk of "dead on arrival" hardware has become a multi-billion dollar liability.

Aehr Test Systems $AEHR has positioned itself as the only scalable solution to this bottleneck, transitioning from a niche Silicon Carbide player into a fundamental pillar of the 1.6T networking and AI ASIC supply chain.

1⃣The Core Edge: Torturing Silicon at 3,500 Watts

Modern AI processors and 1.6T optical chips are power-hungry monsters. Traditional "single-die" testing is now too slow and costly. Aehr has changed the rules with its FOX-XP Ultra-High Power system:

Extreme Power Density: These systems deliver and dissipate 3,500 Watts per wafer across nine 300mm wafers simultaneously an industry record.

Multi-Zone Thermal Control: Each wafer is divided into independent thermal zones, allowing the system to catch "infant mortality" defects without melting the delicate silicon structures.

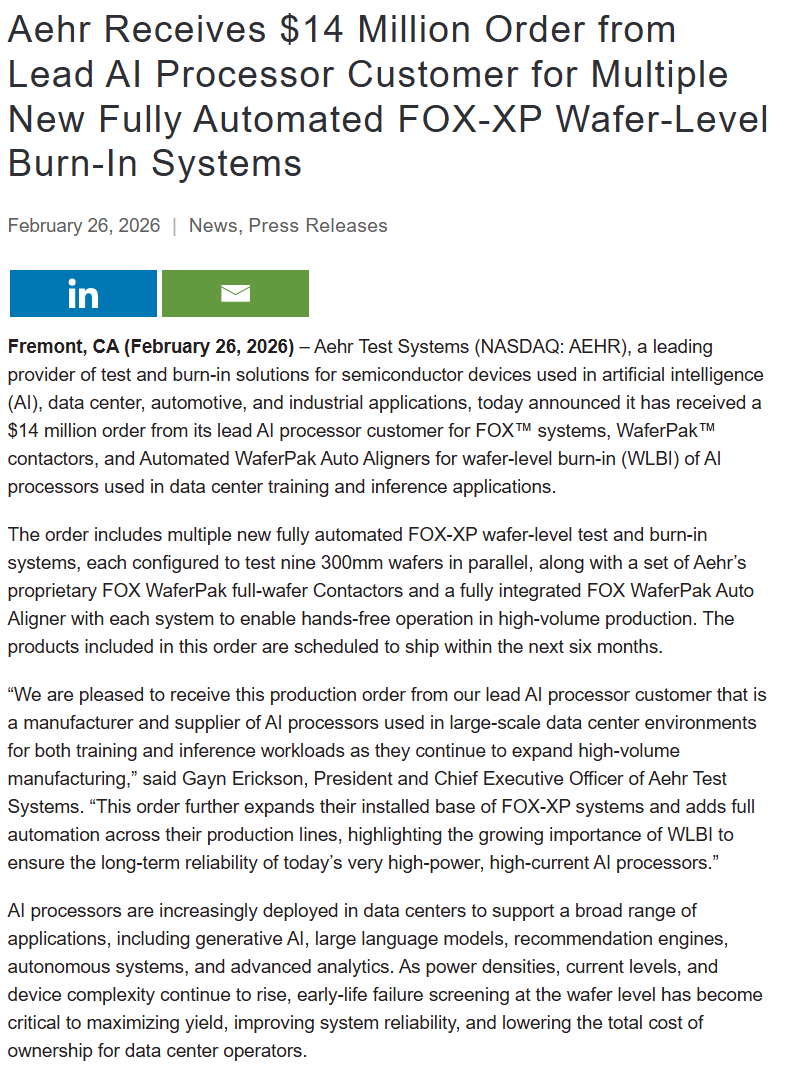

1.6T Synergy: New March 2026 orders for Silicon Photonics configurations ensure that even the smallest crystal defects are caught before packaging, saving giants like Broadcom and Intel billions in potential losses.

2⃣The "Razor & Blade" Revenue Engine: More Than Just Machines

Investors often misjudge AEHR by looking only at large system contracts. Its true strength lies in its high-margin, recurring revenue model:

The Razor (FOX-XP/Sonoma): Selling the system is the "entry ticket" to the customer’s fab.

The Blade (WaferPak™ & DiePak®): Every new chip architecture (e.g., the transition from Nvidia Blackwell to Rubin) requires a new, proprietary set of WaferPaks.

Recurring Alpha: During production ramps, these consumables generate gross margins exceeding 60%, providing a financial cushion against the cyclical nature of hardware sales.

Strategic Expansion: With the integration of Incal Technology, Aehr now earns twice: first by testing the wafer, and then the packaged module.

3⃣Financial Deep-Dive: The Great Inflection

March 2026 marks the moment Aehr shifted from "promise" to "execution":

The Guidance Pivot: In January 2026, the company reinstated guidance, targeting $25M–$30M in H2 FY26. A recent $14M order from a lead AI customer proves these targets are within reach.

Backlog Visibility: While the current backlog is $18.3M, management expects bookings of $60M–$80M in the coming months, setting the stage for a record-breaking FY2027.

Ironclad Balance Sheet: With $31.3M in cash and zero debt, Aehr has the liquidity to scale production rapidly for the 1.6T era.

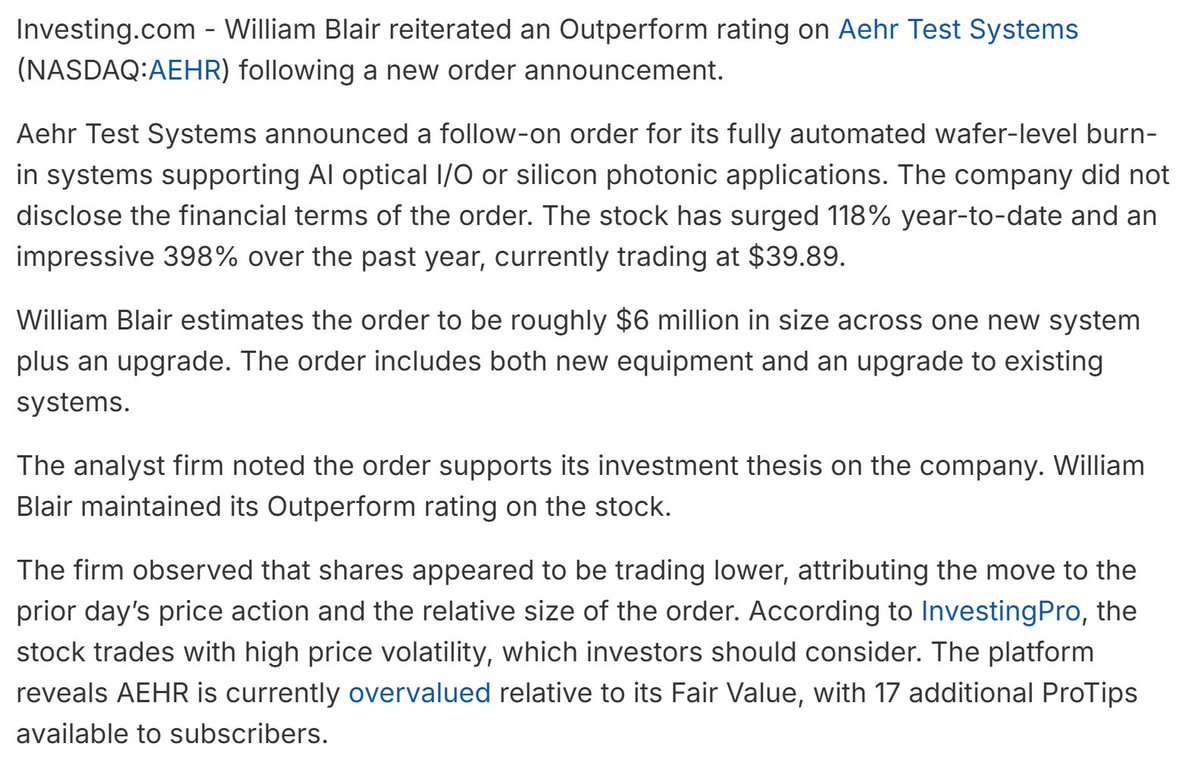

Institutional Momentum: A double upgrade from William Blair and increased stakes from firms like Wellington Management confirm that "smart money" has identified the bottom.

4⃣ The Specialist vs. The Giants: Can $AEHR Scale?

The ultimate question for $AEHR is how it survives in a market dominated by Advantest and Teradyne.

Specialization vs. Scale: Advantest and Teradyne control ~95% of the general ATE (Automated Test Equipment) market. However, they lack Aehr’s hyper-specific expertise in ultra-high-power wafer-level burn-in. For AI chips pulling 1000W , generalist tools are insufficient.

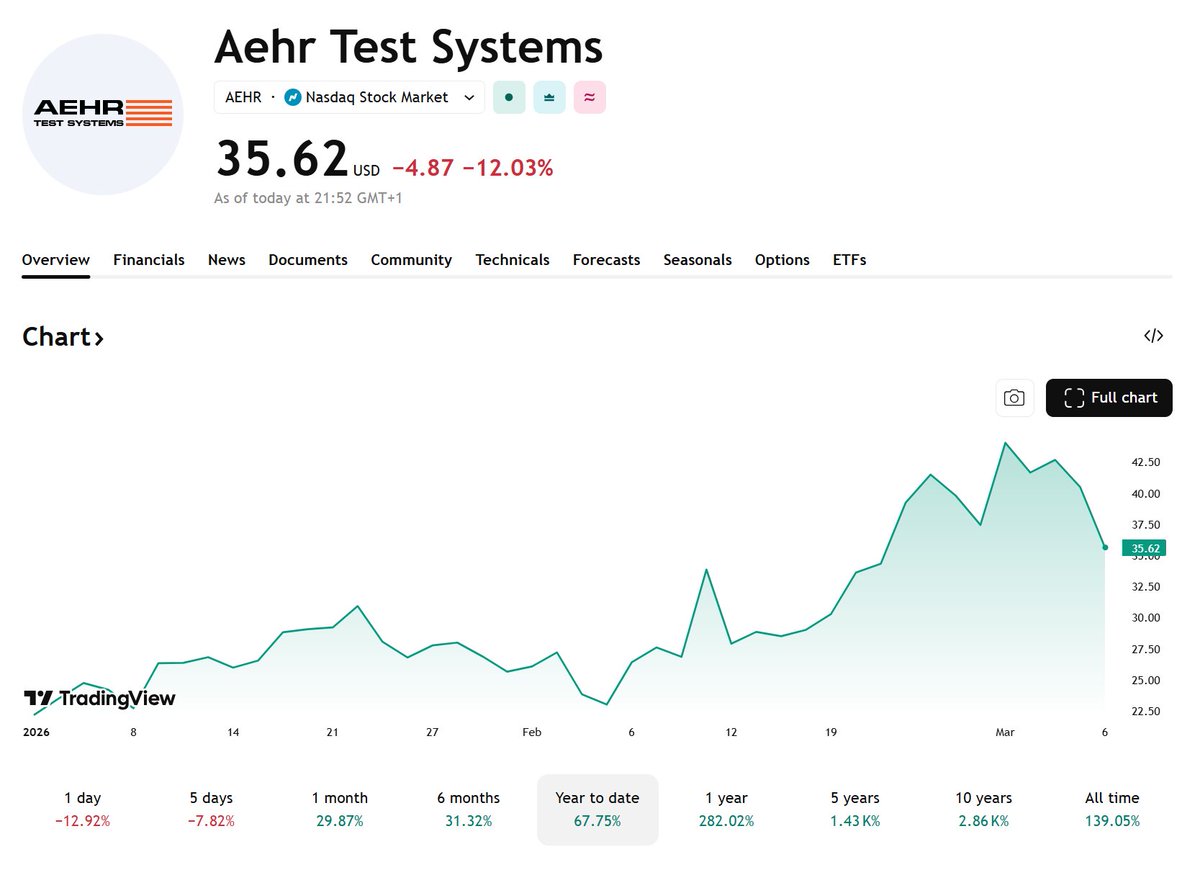

The Acquisition Narrative: With a market cap around $1.3B and a year-to-date gain of 118% (as of March 6, 2026), Aehr is increasingly viewed as an acquisition target. Its proprietary Sonoma and FOX-XP platforms would be a perfect "bolt-on" for Advantest to complete its AI testing suite.

Market Potential: While today’s revenue is small, William Blair estimates a $1.5B–$2.3B Total Addressable Market (TAM) for AI burn-in tools by 2030. If Aehr captures even 30% of this niche, its fair value could reach $50–$70 per share.

Final Verdict: The Strategic Inflection Point

Aehr Test Systems is no longer a speculative play on electric vehicles; it is a fundamental tax on AI reliability.

The Bull Case: Aehr owns the only high-volume platform for 3,500W wafer-level testing. As hyperscalers like Alphabet and Amazon commit hundreds of billions to AI infrastructure in 2026, the demand for "guaranteed uptime" makes Aehr’s technology an operational necessity.

The Bear Case: Customer concentration remains high. A delay in the Silicon Photonics ramp would hurt. However, with the launch of the Sonoma system, Aehr is successfully diversifying into the broader AI ASIC and memory markets.

Conclusion: Aehr is the gatekeeper. As AI power envelopes push toward the physical limits of silicon, Aehr’s ability to "torture-test" at scale makes it an indispensable component of the 1.6T stack. For investors, the play is no longer about "testing".

It is about Yield Assurance in a world where failure is not an option.

#AEHR #AIInfrastructure #Semiconductors #Investing #BurnInTesting #Advantest #Teradyne #MarketAnalysis

The Glass Gatekeeper: Why $SCHMD is the High-Stakes Interconnect Play of 2026

I spent yesterday deep-diving into the infrastructure of the 1.6T era. While the technical analysis was ready, the market moved faster than the ink could dry.

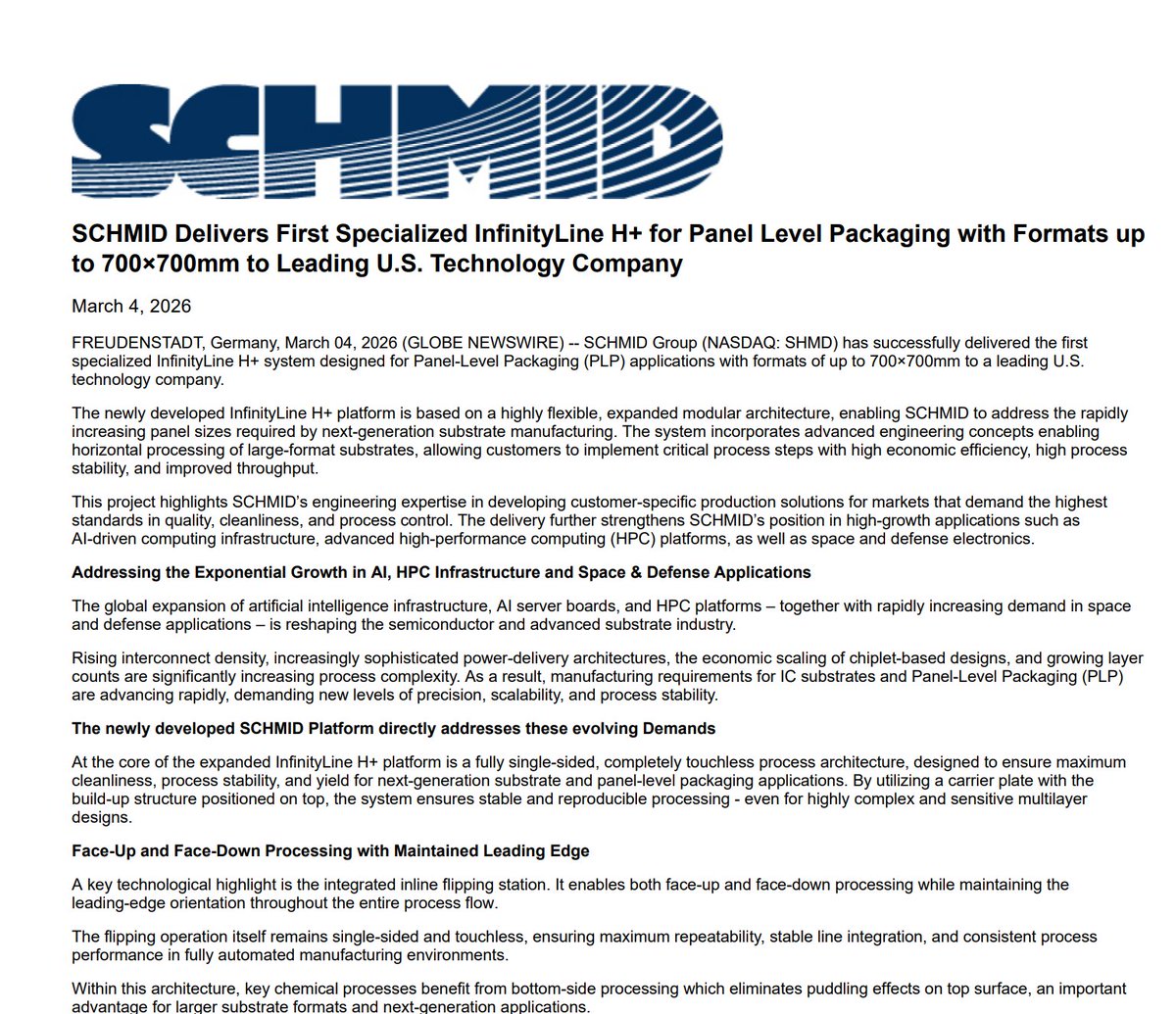

Today, the narrative shifted from "theoretical potential" to "operational reality." SCHMID Group ($SHMD) erupted with a 30.73% surge following a catalyst that redefines the advanced packaging landscape.

1⃣The Core Business: What is SCHMID?

SCHMID is a German engineering powerhouse providing wet process equipment (etching, cleaning, metallization) for the world’s most advanced electronics manufacturers.

In March 2026, the company became a pivotal link in the production of AI Server Boards and Glass Substrates. Their advantage lies in breaking the physical barriers that even industry giants struggle to overcome:

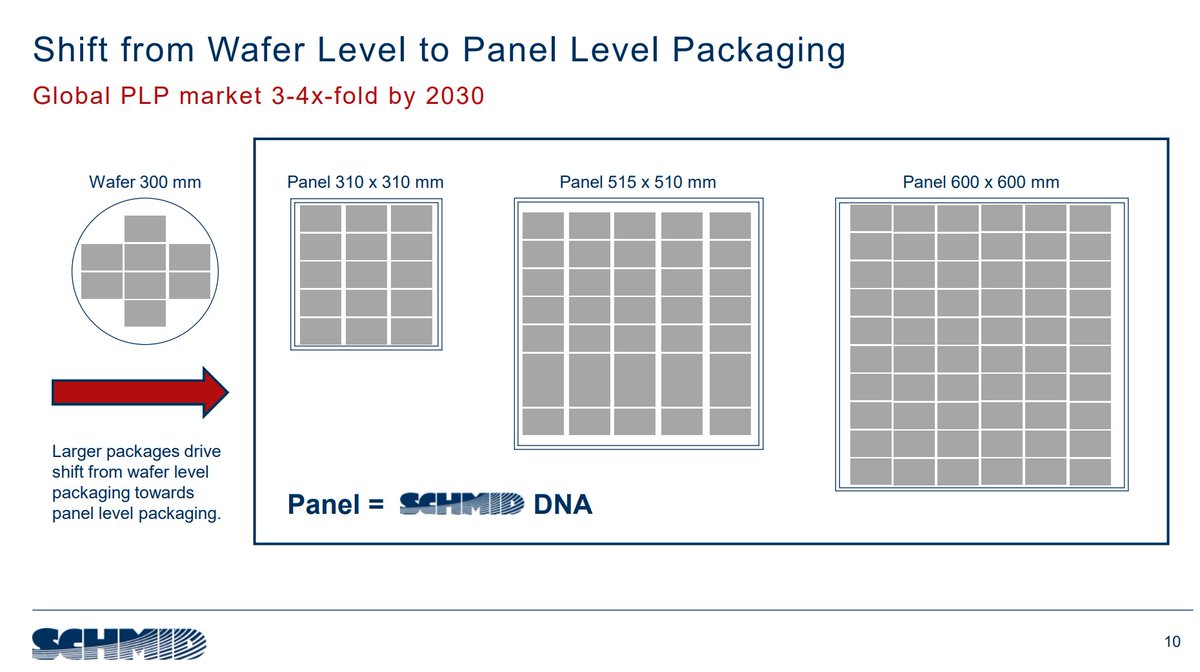

InfinityLine H (The catalyst for today's rally): This is a platform for Panel-Level Packaging (PLP). It is one of the few systems globally capable of handling massive 700x700mm panels. Larger panels mean lower unit costs and the ability to package more powerful AI clusters.

Touchless Technology: In the 1.6T standard, where interconnects are microscopic, any contact with the substrate risks fractures or contamination. SCHMID developed non-contact transport systems that drastically boost yield - the most critical metric in Intel and TSMC fabs today.

Vertical Processing: Traditional horizontal processing leads to the "puddling effect" (chemical residue), which ruins fine-line circuits. SCHMID’s vertical systems ensure chemical uniformity, essential for the high-density traces required by SAP and mSAP technologies.

2⃣ Why SCHMID is Indispensable

The company has become the gateway to new AI server architecture. Their machinery is mandatory where copper and plastic (traditional PCBs) hit a physical wall:

AI & HPC Infrastructure: Building motherboards for "Rubin" or "Blackwell Ultra" processors requires a level of precision that only SCHMID's vertical etching can provide.

Space & Defense: Today’s news of the U.S. delivery confirmed that H systems are entering the defense and aerospace sectors, where the reliability of large-scale integrated circuits is mission-critical.

The Glass Core Ecosystem: SCHMID provides the "wet" technology that, paired with $LPKF lasers, creates the complete production chain for glass substrates - the future of 1.6T connectivity.

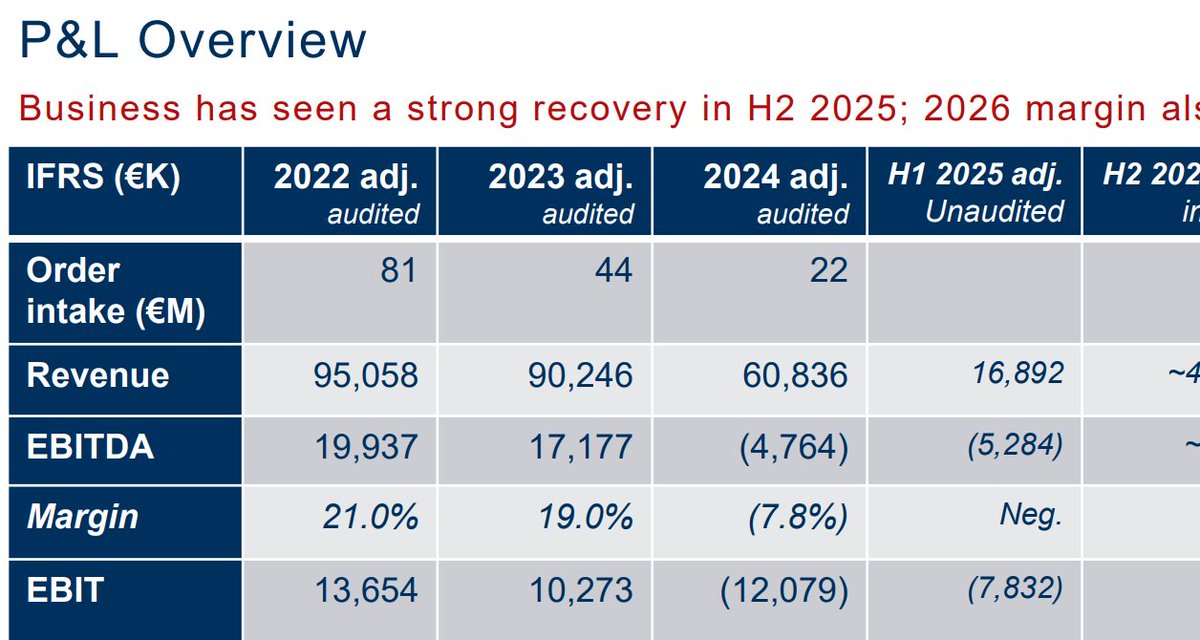

3⃣Financial Deep-Dive: Margins, Revenue, and Debt

This is where the investment thriller begins. The stock jumped 30% because investors finally believe SCHMID is successfully leaping across the "valuation chasm."

➡️Revenue & Growth Forecast

2024–2025: These were transformation years. Revenue was under pressure (approx. €72-77M for 2025) as the company "purged" old tech to pivot toward AI.

2026 Guidance: The company officially forecasts a revenue surge to over €100 million. This represents a 30-40% YoY growth driven by a record order backlog (approx. €95M in new orders secured in 2025 alone).

➡️Profitability (Margins)

Gross Margin: After a difficult 2025, gross margins are returning to healthy levels thanks to high-margin systems like the InfinityLine H .

EBITDA: The target for 2026 is an Adjusted EBITDA margin >12%. This is a key signal—the market sees a company that is no longer just dreaming of growth but is actually generating cash from it.

➡️Debt Management (The "Risk" Factor)

This was the primary weight on the stock for months:

In January 2026, the company executed a massive debt-to-equity swap, converting approx. $27 million of debt (owed to XJ Harbour) into shares. While this caused dilution, it drastically deleveraged the balance sheet.

They secured $30 million in Convertible Notes. The first $15M hit the accounts in January; the second $15M is tied to operational milestones. Today’s U.S. delivery is a loud signal to creditors that this money is already working.

➡️Investor’s Verdict⬅️

Today’s 30.73% move marks the moment the market stopped viewing SCHMID as a "debt-ridden German engineer" and started seeing it as a strategic U.S. supplier.

With a market cap still hovering around $400M–$450M and a backlog nearly matching that value, $SHMD remains one of the most asymmetric bets on AI infrastructure. Debt risk still exists, but today’s H delivery proved that SCHMID’s technology isn't just a "PowerPoint" - it’s a physical machine building the future in the U.S. right now.

7

35

14,507

22 Dec 2025

BREAKING: Trio-Tech (NYSE: $TRT) Explodes to $12.65 for a 22.3% Move Today – Now Up 21.87% Since Our Alert at $10.38 Per Share and Charging Toward New Highs!

📱Download our Mobile App (iOS / Android)

🔗 link-to.app/dexwirenews

Trio-Tech International (NYSE: #TRT) is on absolute fire in this red-hot semiconductor resurgence. Founded in 1958 and headquartered in California, this underrated gem provides critical back-end semiconductor testing services, burn-in and reliability equipment, and distribution across the US, Singapore, Malaysia, Thailand, and China. With surging demand for AI-driven chips, advanced SiC/GaN testing, and industrial electronics, TRT just reported explosive Q1 FY2026 revenue growth of 58% YoY, swinging back to profitability amid recovering Asian semi demand. Fresh off completing a key Malaysian subsidiary acquisition and announcing a confidence-boosting 2-for-1 forward stock split (effective early January 2026 to boost liquidity), this small-cap powerhouse (market cap ~$50M) is perfectly positioned as a pure-play beneficiary in the ongoing chip boom – often flying under the radar while giants grab headlines!

Disclaimer: We were not compensated in any way for this alert, nor do we own any shares of TRT or plan to purchase any in the future. **THIS IS NOT FINANCIAL ADVICE.** Always do your own due diligence and consult a professional advisor. Trading stocks involves significant risk of loss.

#TRT #TrioTech #SemiconductorStocks #StockSplit #NYSE #SmallCapStocks #ChipBoom #AITesting #Semis #BurnInTesting #GaN #SiC #TechStocks #StockAlert #PennyStocks #MomentumStocks #Breakout #StockMarket #Investing #DayTrading #SwingTrading #WallStreet #Finance #HotStocks #StockPicker #GrowthStocks #UndervaluedStocks #MarketMovers #Trading

1

3

10

415

19 Dec 2025

Discover the breakout potential in Trio-Tech International (NYSE: $TRT), a global leader in semiconductor manufacturing, testing, and distribution services.

📱Download our Mobile App (iOS / Android)

🔗 link-to.app/dexwirenews

Trio-Tech International operates across the United States, Singapore, Malaysia, Thailand, and China, #TRT delivers cutting-edge solutions for front-end and back-end semiconductor processes, including advanced test equipment, environmental and burn-in testing services.

Featuring a diverse portfolio of specialized products such as autoclaves, leak detectors, HAST testers, and temperature-controlled chucks, $TRT is strategically positioned to capitalize on surging demand in the semiconductor industry.

With strong technical momentum on the charts, an alert price around $10.38 per share, and a compact market cap of approximately $45M, analysts see significant upside potential toward the $20 mark, making this a compelling short-term trade opportunity in the thriving chip sector.

Instagram (Full Carousel): instagram.com/p/DScnbKqkV6K/…

*We have NOT been compensated for this particular stock profile, NOR do we own any shares. This is NOT financial advice. Everything we do is for informational & educational purposes only.

#NYSETRT #TRTStock #SemiconductorStocks #Semiconductors #ChipStocks #StockPick #BreakoutStock #PennyStocks #SmallCapStocks #Investing #StockMarket #Trading #TechStocks #Semicon #BurnInTesting #TestEquipment #Autoclaves #LeakDetectors #HASTTesters #StockAlert #MomentumTrading #ChartAnalysis #UpsidePotential #StockToWatch #Finance #WallStreet #DayTrading #SwingTrading #GrowthStocks

1

2

9

315

28 Jun 2018

See that red light right there? It ain’t supposed to blink. #hardwareproblems #burnintesting #gamedev @ Full Sail University instagram.com/p/BkliklDgMq7/…

2