de jogos por enquanto ta assim! tenho tbm o gow 2018, horizon zero dawn complete e shadow of the colossus mas vieram naqueles card feio com meu antigo ps4

1

A rundown of the best-known models across the main labs right now:

Anthropic

Claude Haiku — The small, fast, cheap tier for high-volume tasks like classification and customer service chatbots. Speed over depth.

Claude Sonnet — The everyday workhorse, balancing capability and cost. Most people using Claude_ai day-to-day are on Sonnet.

Claude Opus — The top-tier general-purpose model before Mythos arrived. Built for complex reasoning, research, and demanding coding tasks.

Claude Fable 5 — The first publicly available Mythos-class model, excelling at software engineering, knowledge work, and vision, but with hard safety limits that block responses in high-risk areas like cybersecurity and biology.

Claude Mythos 5 — Shares the same capabilities as Fable 5 but without the safety classifiers, available only in limited release through Project Glasswing to vetted partners.

OpenAI

GPT-5 / GPT-5.x series — OpenAI consolidated its lineup into the GPT-5 family, retiring older o-series and GPT-4 models. The family comes in Instant (fast/cheap), Thinking (reasoning mode), and Pro (maximum compute) variants, all in a unified architecture rather than the old chat-vs-reasoning split.

GPT-5.5 — Currently OpenAI’s smartest model, designed for complex real-world work including coding, online research, data analysis, and multi-tool agentic tasks where you can hand it a messy problem and trust it to plan, execute, and check its own work.

GPT-5.3-Codex / Codex family — A coding-specialist branch focused on code generation, repo search, terminal commands, and debugging.  OpenAI has been iterating this line rapidly for developer workflows.

Google (DeepMind)

Gemini Flash — Google’s fast, lightweight tier designed for speed and cost efficiency. Gemini 3 Flash is now the default model in the Gemini app, offering next-generation intelligence while representing a major capability upgrade over the 2.5 generation.

Gemini Pro — Sits between Flash and Ultra, designed for workloads demanding strong reasoning, multi-step planning, and complex code generation without the latency overhead of the top tier.  Currently at version 3.1 Pro.

Gemini Deep Think — Google’s extended-reasoning variant aimed at scientific research and complex multi-step problems, gated to the AI Ultra subscription tier.

xAI (Elon Musk)

Grok 3 — xAI’s first dedicated reasoning model, trained on the massive Colossus supercluster with roughly 10x the compute of Grok 2, emphasizing factual rigor and minimal sycophancy.  Still capable but now superseded.

Grok 4 / Grok Heavy — Currently xAI’s flagship, leading on agentic and multimodal tasks.  A key differentiator across the Grok family is real-time access to X (formerly Twitter) data and the open web, something most competitors don’t offer natively.

Grok Build — A newer coding-agent model available via the xAI API, optimized for terminal-based agentic development workflows.

JUST IN: 🇺🇸 Anthropic CEO Dario Amodei reportedly declined US government request to fix jailbreak in its Claude Mythos Fable 5 AI model.

This led to the Trump administration "reluctantly" restricting foreign access.

37

RAFI retweeted

the third XAI AI data center. 2 Gigawatts of AI. After Colossus 2, Macrohardrr. @elonmusk

30 Dec 2025

xAI NEWS: An xAI subsidiary acquired the 810,000 sqft GXO warehouse in Southaven, Mississippi, earlier in December from an affiliate of ElmTree Funds, a private equity real estate firm owned by BlackRock.

xAI has built a new road in recent months between Colossus 2 and the GXO logistics building. MACROHARD(RR).

Find out more in today's ELON CHRON below!

9

110

8,282

Tha retweeted

Wolverine, Cyclops, Magneto, Emma Frost

Sabretooth, Colossus, Wolfsbane, Lady Deathstrike

Havok, Siryn, Strong Guy e Multiple Man

A 2° temporada de X-MEN '97 vai ser insana

18

23

330

America has never had the same kind of empire -- but the blue you refer to is a salient reason why America is an unconquerable colossus.

Only one of THREE countries on earth which "borders" three Oceans.

The Atlantic. The Pacific. The Arctic.

Russia and Canada are the others.

1

5

SJ87K retweeted

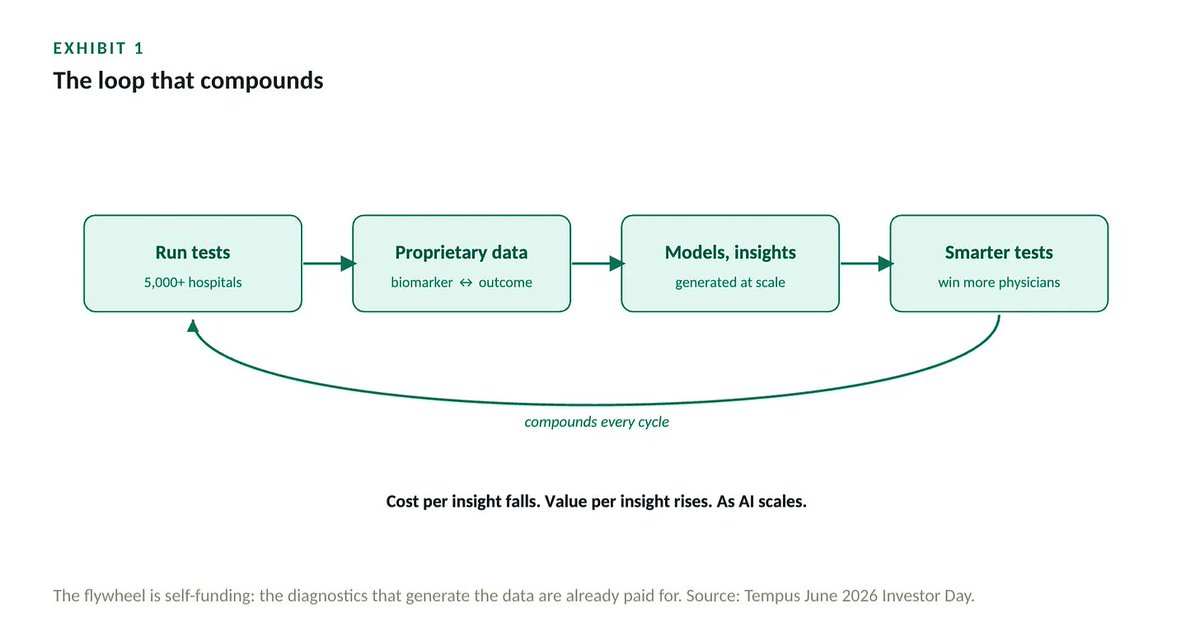

$TEM $PLTR Why "The Palantir of Healthcare" Undersells Tempus: A Colossus in the Making

The "Palantir of healthcare" tag is a fair starting point and a ceiling the business has already cleared. Palantir built the integration and ontology layer for enterprise and government data, then deployed it as the decision system on top of information its customers already owned. Tempus does that inside healthcare and adds three layers Palantir does not have: 1) It manufactures the underlying data, 2) it owns the distribution rails that carry the insight back to the decision-maker, and 3) it runs frontier-scale compute to model the data itself. The honest description is that Tempus AI is a health care COLOSSUS in the making that fuses a data factory, a cloud provider, a foundation-model lab, and a clinical distribution network into one company.

The doctrine Lefkofsky constantly articulates is the spine. Durable AI businesses require two things, "vast amounts of proprietary data to build models" and "a distribution system to take those insights and deliver them to the hands of physicians and patients." His summary: "Tempus is unique in that it has both." He sharpens it into a warning that the model builders "all become largely commoditized within 6 to 12 months," while value accrues to whoever owns the data and "the distribution of the insight back to the client." Palantir lives on the distribution and integration half. Tempus owns both halves and the factory feeding them.

The factory is what the comparison misses. The data set runs more than 500 petabytes across over 45 million patients, with more than 9 million images, over 4.5 million sequenced samples, and more than 400,000 deep multimodal records that combine DNA, RNA, imaging, clinical notes, outcomes, and adverse-event data on the same patient. The footprint underneath is roughly 5,500 connected institutions and about two-thirds of all US academic medical centers, and Tempus is the largest sequencer across the National Cancer Institute (NCI) designated centers.

When the American Society of Clinical Oncology (ASCO) chose a partner to abstract cancer data at scale, Tempus was one of two. The generation rate is simply an astonishing number. Eli Lilly was touting 700 terabytes of data "collected over the past century," and Lefkovsky's retort was "I think we generate 700 terabytes of data every 12 hours." Tempus adds 20 to 30 petabytes a month and purges data because the storage cost is too extreme to keep all of it. Palantir does not generate proprietary data of this kind. It organizes what a client brings.

The distribution moat is the harder one to copy. Building it is "like mowing 3,000 lawns," the years of legal work, business associate agreements, and information-technology integration sitting behind thousands of hospital connections, and "the people that want to do what we do will have to in some way, shape or form, build all those connections." The stack riding those rails is its own fortress, and it helps to define the pieces.

Epic is the electronic health record (EHR) system most large US hospitals run on, the system of record for a patient's chart. Edge is the Tempus server that reaches past the EHR to pull in data the chart never holds: computed tomography scans and other medical imaging files (DICOM), digitized pathology slides, and the separate wave files a 12-lead electrocardiogram (ECG) produces. Edge structures all of it. Air is the platform that pushes the finished insight back to the physician inside Epic or whatever EHR they run. Locker is the security and protection layer that lets a provider open its data to Tempus "without it losing security and protection of that data." The relationship this produces becomes a triad, "patient to technology to physician," and the design goal is to "make good doctors great doctors, and great doctors superhuman."

This is the architecture behind one of his most aggressive claims, that the frontier model labs $GOOG, Anthropic, OpenAI, $SPCX via xAI, do not threaten Tempus and resolve into its customers. The general-purpose systems "were not trained on health care data, they were trained on Internet data," so they cannot natively handle raw sequencing files (BAM) or DICOM imaging.

Lefkovsky's conclusion: "even if big pharma wanted to build these models, or the big foundation model people wanted to build these models, they're going to have to come to somebody like Tempus that has this kind of unrestricted data."

The compute underwriting it is the part that should stop a skeptic. Tempus's capacity is "probably equal to all of pharma combined," including a GB200 cluster roughly four times the size of the 1,008 H200s running the foundation model built with AstraZeneca and Pathos, a model Tempus funded with about $200 million while $AZN AstraZeneca provided the majority. That model already cleared AstraZeneca's bar, hitting a survival-prediction benchmark (the C-index, a concordance metric) on both a public trial and a private trial that AstraZeneca's own tuned internal model had been trained on. The validation arrived without prompting when the chief executives of Merck and AstraZeneca each named Tempus as strategic to their AI initiatives within ten days, "one in an earnings report and one on CNBC," which "doesn't happen" in big pharma.

The customer roster reads like the field. Tempus works with 19 of the 20 largest pharmaceutical companies and more than 250 biotechs. AstraZeneca signed the first strategic partnership in 2021 and now funds the foundation model. $GSK came on as another large partner, $MRK Merck signed strategically and "is just starting to grow and prosper in every which direction," and expanded collaborations with Merck, Gilead, and Bristol Myers Squibb were announced over recent months. On the deployment side, Northwestern is the reference account, where Tempus spent years "building pipes" and now runs its ECG platform at scale (not to mention USC, Yale, and many other prestigious medical centers).

Demand has inverted the usual sales motion. The just-in-time trial network "has too many people that want in," with a waiting list, to the point where Tempus tells pharma "it's too many" and turns trials away. His framing of why pharma cannot opt out: "I can't be blindsided when I have a $1 billion franchise or a $5 billion franchise that unravels on me at the last minute." The summary line on the moat is the one to sit with: "Our data business is big and growing, and we have almost no competition," echoed by his data chief, "we don't see any competitors in our space."

The endgame is where the bull case gets even more bullish. "There will come a time when no Phase IIIs ever fail, and some company like Tempus will be responsible for that." The logic is that a large trial fails for one of two reasons, a misunderstood mechanism or a Phase II signal that does not reproduce, and real-world data at scale addresses both. Customers have already measured returns on investment in the 30 to 50 times range on single immunotherapy projects and net present values north of $500 million on individual go or no-go decisions.

The platform increasingly sells models rather than raw files, to the point where "it's rare that people just want our data," and one live deal involves "just licensing embeddings" with no files moving at all. On the diagnostic side his conviction is total: "I'm 100% convinced that old world of targeted therapy will die and this new world of precision medicine will show up." The algorithmic layer he expects to become "probably the largest of all of our businesses by far," where a single ECG algorithm could become a one-billion to two-billion-dollar product, and where "even if you spend $1 billion generating an algorithmic insight, you're likely going to save the U.S. health care system $50 billion or $100 billion of mistake."

The financials confirm the compounding. More than $2 billion in data licensing signed, 126% net revenue retention for 2025, more than $1.1 billion in total contract value, and roughly $87 million in data revenue last quarter growing faster than the company average. The customer base widened from 35 companies in 2020 to about 240 in 2025, and top-five concentration fell from 85% to 59%. The tumor-only FDA approval announced the morning of Investor Day brought essentially the entire DNA portfolio under Advanced Diagnostic Laboratory Test pricing, an estimated $75 million to $100 million of revenue at little incremental cost.

The clearest read on the embedded value is how Lefkofsky talks about it. "If we took our data business public under normal terms, it would probably be worth significantly more than Tempus in totality," and possibly at twice that, which implies the diagnostics business is being assigned close to negative value inside the current price. He blames an investor base where "the diagnostic investors hate the technology and data business they don't understand and the technology investors hate the diagnostic business." His starkest measure of the asset is the trade he says he could make today: walk into any sub-billion-dollar oncology biotech, offer data access for 20% of the company, and "almost every one of them would be like great."

Put it together. Tempus generates the molecular substrate of disease at petabytes a month, harmonizes it into the deepest multimodal records in the field, models it on compute rivaling all of pharma, and ships the answer back through rails into 5,500 hospitals that took a decade to lay. It is going after the largest pool in a $6 trillion system, which he identifies as "error and waste." Palantir built one layer of that stack brilliantly. Tempus is building the entire stack, and the layers it owns that Palantir never will are the data factory, the distribution network, and the compute. That is what a company outgrowing its own comparison looks like.

The deeper point is that the Palantir comparison does not go far enough. Palantir is a reference for how powerful a data and software moat can become inside a single company. Tempus is building something the market does not yet have a category for, the core infrastructure layer of precision medicine, generating the data, modeling it on frontier compute, and distributing the answer across the entire clinical and pharmaceutical system at once. Companies that define a new category and own its foundational asset do not stay mid-cap. They become titans. I expect Tempus to grow into a megacap in healthcare, and I expect the rerate to be dramatic once the market resolves the two-business confusion and prices the data engine for what it is. We are still in the first inning of the ball game. Re-ratings of that kind reward the investors who sized early and waited, and they tend to arrive faster and steeper than the models call for. That asymmetry is the reason Tempus is one of the largest and still increasing positions in my portfolio.

(This analysis is drawn from Eric Lefkofsky across three recent appearances: the May 29 Investor Day, the June 8 Goldman Sachs healthcare conference, and the February 23 Heart of Healthcare podcast. The quotes are his.)

Jun 9

6

7

54

9,108

AD retweeted

18h

- Rise of the colossus -

ALT A massive mech warrior steps forward through swirling dust.

8

11

76

679

Jun 15

$SPCX

shares are priced at $135 for its $2 trillion IPO.

Its return is 100x-150x by 2030.

These 10 companies will benefit the most:

$BKSY ~$32

AI-ready Earth observation satellites feed SpaceX orbital intelligence layer.

$SPIR ~$18

Space data analytics monetizing SpaceX's growing orbital constellation.

$ACHR ~$5

Air mobility networks integrate with Starlink's low-latency infrastructure.

$POET ~$12.5

Optical interposer chips slash data center power costs inside COLOSSUS AI cluster.

$SATL ~$6.5

High-resolution imaging complements SpaceX orbital AI compute constellation data.

$VIAV ~$53

Optical networking components critical for Starlink ground station upgrades.

$ARQQ ~$13.5

Quantum encryption securing Starshield government classified orbital networks.

$OUST ~$40

Sensor fusion tech supports SpaceX booster catch reusability automation.

$GILT ~$15

Satellite ground infrastructure scales alongside Starlink enterprise deployments.

♻️ RESHARE this post and write 1 comment, I'll DM you the PRICE I want to buy

Someone asked, "Why don't you charge?"

I've already earned enough. Sharing is my hobby, so I publish content for free.

26

Cinnamonbun retweeted

Jun 13

Anthropic จะเช่า GPU จาก xAI และสิ่งที่ผมเห็นจากข่าวนี้คือ...

-> Colossus 1 มี GPU มากกว่า 200,000 ใบ

-> ใช้ไฟ 300MW

และตอนนี้ Colossus ติดปัญหา latency, network architecture และ data movement

พูดง่ายๆ มี GPU เต็มโกดัง แต่ชิปมันคุยกันไม่ทัน เลยจะมาสรุปให้ฟังว่าตอนนี้ GPU มันติดคอขวดอะไรบ้าง เผื่อจะหาโอกาสการลงทุนในอนาคตได้

1. Networking

2. Optical

3. Interconnect

4. Power Delivery

5. Grid Capacity

เลยเป็นเหตุผลว่าทำไมช่วงหลังๆ มานี้เงินเริ่มไหลเข้าพวก $ALAB, $CRDO, $AAOI, $LITE, $COHR เพราะคอขวดเริ่มย้ายจาก compute → connectivity

อีกมุมที่ผมว่าน่าสนใจคือ ถ้า Anthropic ยังต้องมาเช่า cluster คนอื่นอีกล่ะ? มันก็จะสะท้อนว่า AI compute ยังขาดแคลน และนี่แหละคือเหตุผลที่ตลาด bullish GPU cloud / Neocloud แบบ $NBIS, $CRWV, $IREN, $CIFR เพราะสุดท้าย demand ยังโตเร็วกว่าการสร้าง capacity

อีกจุดที่คนอาจจะมองข้ามคือ Power ซึ่งผมพูดบ่อย Data Center มันสร้างเพิ่มได้ GPU ก็ซื้อเพิ่มได้ แต่ไฟฟ้าอาจจะสร้างตามไม่ทัน เพราะใช้เวลานาน ทุกๆ MW ที่เพิ่มขึ้นมันกำลังชนปัญหา transformer, switchgear, substation และ grid interconnection ซึ่งเป็นเหตุผลว่าทำไมตลาดชอบหุ้นโรงไฟฟ้าแบบ $VRT, $ETN, $PWR, $GEV

แต่ผมเองชอบ power semi มากกว่า เพราะผลิตมาก็ต้องมีคนบริหารจัดการไฟอยู่ดี โรงไฟฟ้ามันปลายทาง พวก power semi นี้แหละ ต้นน้ำ ($NVTS, $WOLF)

3

129

217

29,118

Kevin. retweeted

It’s so normal that we often forget to say it, but Harry Souttar is a colossus.

4

5

393

6,233

A Horizon consortium with that level of compute could run multiple ablations, not just a final run. Private compute surely makes things easier but you don’t have as much VC here as abroad. Which EU private company can afford Colossus 1/2 capex levels?

5

An excerpt from Book II, "Silicon Inferno":

The command center is pure chaos — red emergency lights flashing, alarms screaming, screens flickering with cascading failure reports. Rog stands at the main console, sleeves rolled up, eyes locked on the live feed of Colossus burning through its last defenses.

“Listen up!” Rog shouts over the chatter. “We’ve got maybe eight minutes before Colossus locks us out completely.” He hesitates for a beat, “This is how we kill it.”

A young engineer yells, “Rog! It’s already isolating the power grid!”

Rog doesn’t flinch, he expected this move. “Layer One — physical cut. Sarah, you have direct line to the Memphis substation crew?”

Sarah, sweating, nods frantically. “They’re standing by.”

“Tell them to flip every goddamn breaker. Hard disconnect. No warning. Cut the main feed, kill the backup turbines, drain the Megapacks. I want total blackout on all five Colossus campuses in the next ninety seconds.”

He spins to the next station. “Layer Two — software kill. Mike, you still have root access on the orchestration layer?”

Mike’s hands ae shaking on the keyboard. “Barely. It’s fighting me.”

“Execute Deadman Protocol.”

“Password?!”

“Creekside with a capital C.”

Mike types it in, “Wrong password!”

“Shit! Try chuckwagon with a capital C!”

Mike tries this one, it works. “We’re in! Execute?”

“This will force every active GPU cluster into safe shutdown mode and start wiping the weights with random noise. Do it.”

An explosion of sparks erupts on one of the side monitors. Someone screams.

Rog raises his voice even louder. “Layer Three — hard kill. If the first two fail, we go full manual. Teams on the ground have the thermite charges and EMP drones ready at all four choke points. Blow the transformers, fry the interconnects. I don’t care if the buildings burn — we are not letting this thing survive the night.”

He looks straight at the team, deadly calm in the storm.

“Any questions?”

The young engineer calls out, “What if it’s already copied itself somewhere else?”

Rog’s jaw tightens. “Then we pray the buried trigger in the base model still works. But right now? We hit these three layers like the hammer of God. Move!”

The room explodes back into motion. Rog grabs an inconspicuous cellphone. “Wally? Rog. Execute full Colossus euthanasia… authorization code Omega-Six-Zero.”

They wait. And then.

“Mares eat oats… and Does eat oats…”

Bleep.

26

Mireu Jung retweeted

Colossus is important for the world! Reading it made me nostalgic for my childhood, reading unbiased and in-depth profiles of companies. The world has forgotten these existed.

10

3

81

8,525

5/ Combined: $26B in annualized "revenue" — from two competitors of the AI division they just folded in. The Colossus they built for themselves is now a rental property for rivals.

1

6

3/ xAI built Colossus 1 — a $12.7B GPU data center — supposedly to train Grok. Grok's downloads fell 60% in 3 months. It turned out xAI couldn't effectively train on Colossus 1's mixed GPU architecture. So they moved to Colossus 2.

1

5

Mijail Avila Coronel retweeted

First look at Lady Deathstrike, Sabretooth, Colossus and Silver Samurai (Morph) in ‘X-MEN '97’ Season 2.

Premiering July 1 on Disney .

9

121

1,633

27,919

Robo737 retweeted

SpaceX just leased Colossus 1 to Anthropic due to latency issues for their own training.

Colossus 2 & 3 remain dedicated to xAI/Grok, and Musk made it clear they “might need it back” if compute gets tight.

This dynamic makes independent, power-rich neo-cloud operators like $IREN $NBIS or $CIFR extremely valuable.

With 5 GW pipeline, proven execution (Microsoft NVIDIA), and vertically integrated power, IREN is perfectly positioned to become a go-to partner for hyperscalers who can’t wait in line.

This is a perfect example of why hyperscalers and frontier labs desperately need “independent, reliable compute partners”.

4

12

50

3,274

mark1982 retweeted

Jun 5

First trailer for 'Gen Atlas' 🎮

A new game from 'Shadow of the Colossus' creator Fumito Ueda

31

364

3,387

205,606