Brian Wang | NextBigFuture: Deep Tech Insights on AI, Drones, Space, Energy & Investments | Proven prediction track record (Metaculus rank 8 Grok citations

Joined May 2008

- Tweets 40,852

- Following 4,809

- Followers 18,965

- Likes 4,072

10,883 Photos and videos

Pinned Tweet

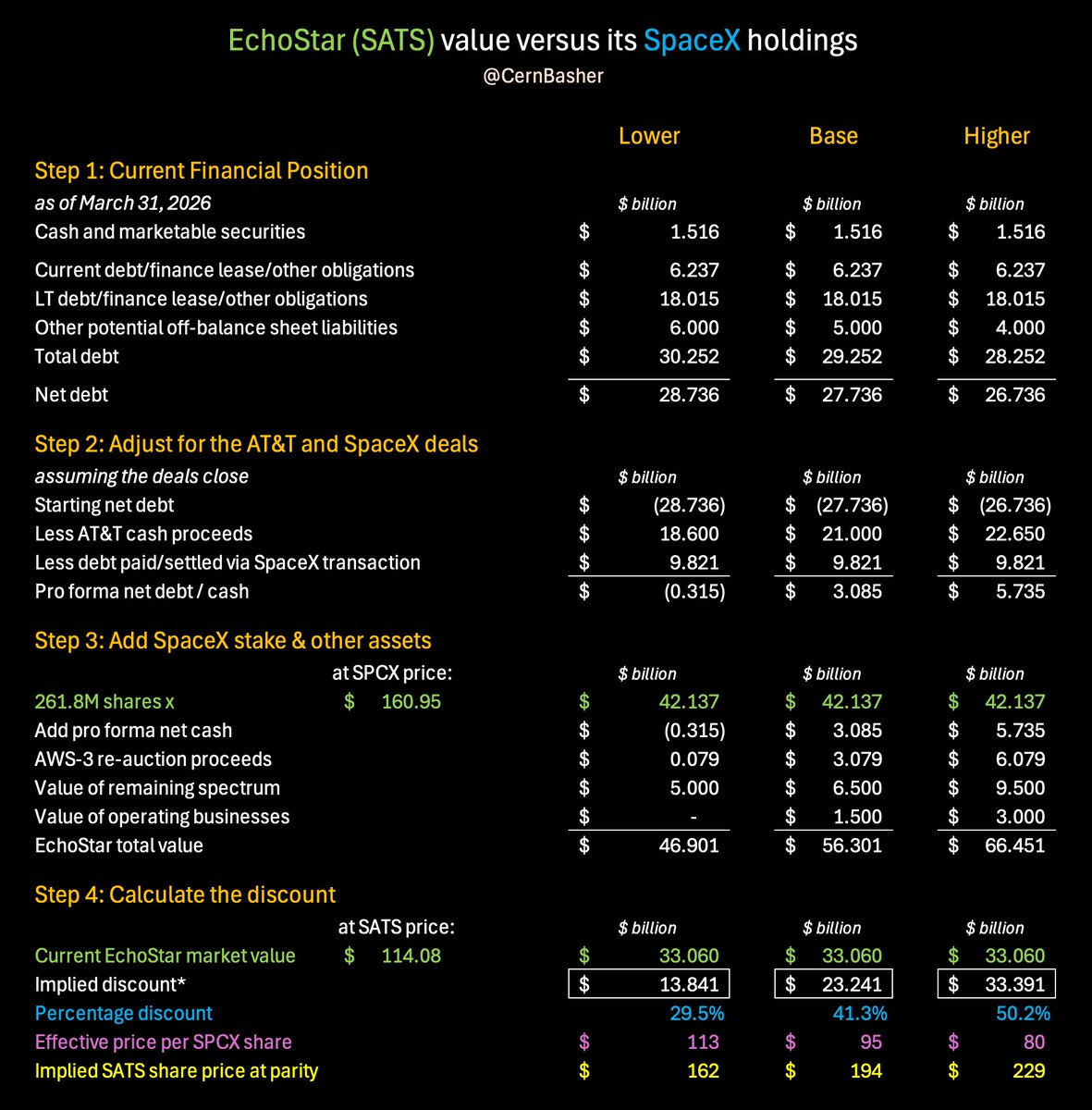

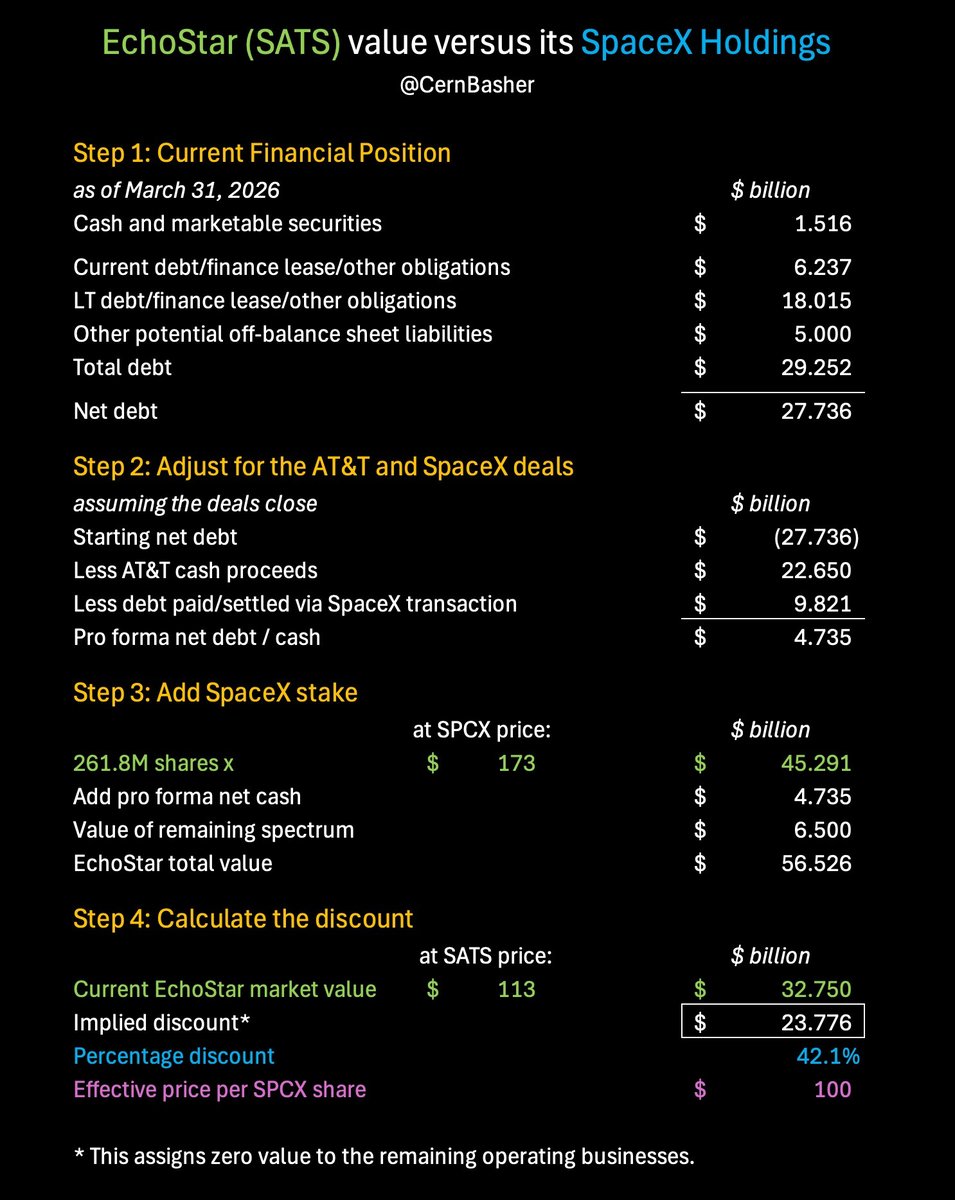

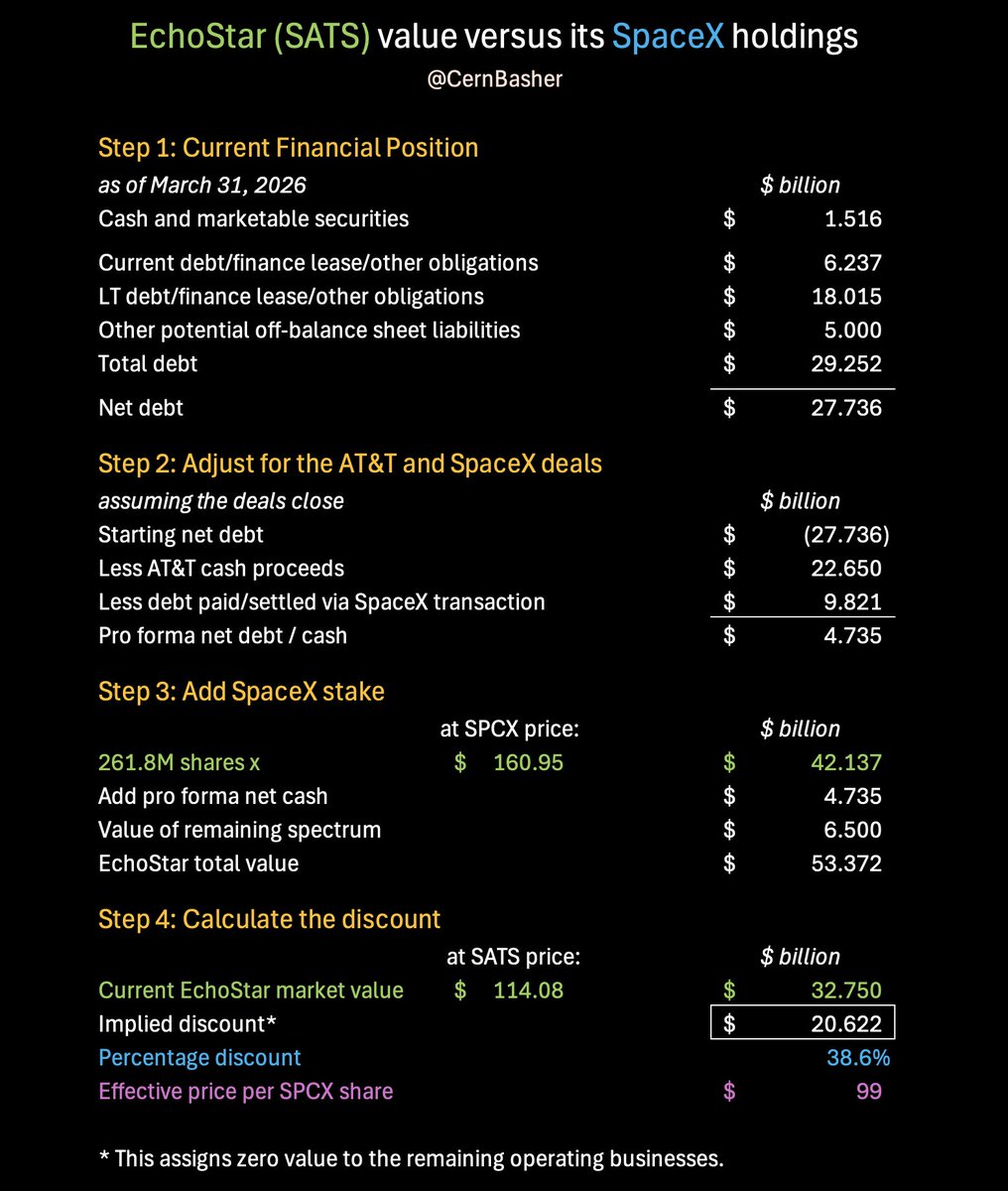

I have worked with @CernBasher to analyze Echostar. Full disclosure I own Echostar and SpaceX. $SPCX $SATS @elonmusk @chamath @ARKInvest @altcap @bradsferguson

Based upon this analysis, the value of SpaceX within Echostar works out to an implied price of $80-113 per share depending upon how the parts of Echostar are valued. Echostar has 266 million shares of SpaceX spread over 288 million shares. The FCC has given approval for the ATT deal and the SpaceX spectrum deals but the final transfers of shares and cash require more time and bureaucracy. The May 12 approvals are past the 30 day open for challenges period as of June 11.

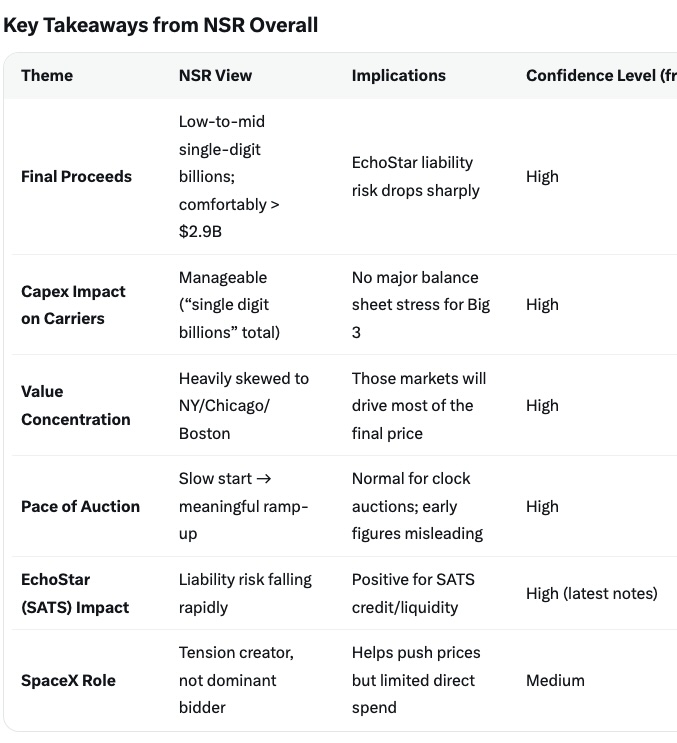

There is ongoing auction of Echostar AWS3 spectrum now. $2.9 billion has been set aside for this but the auction is ongoing and each round that bidders are still involved is now adding over $130 million in value. FCC Auction 13 is ongoing. 6 rounds per day. 185 licenses out of 200 still ongoing. New street estimates $4-8 billion for auction. Every billion added bids will be worth $3.5 per share to Echostar. If the auction lasts extra days into Tuesday to Friday or even next week will be meaning that $1-2 billion per day is being added. SpaceX has Russell and other index inclusion for $10 billion of buying on Friday, June 19. Nasdaq inclusion is 2 weeks after June 19.

Echostar is over 50% owned by the CEO Charles Ergen. He is not selling his shares. Echostar is in the SP500. another 10-15% is held by institutions.

35% is being shorted. This seems to be a short against SpaceX placed before SpaceX opened. SpaceX will not have options trading for a few more days. It will take 5 days of normal $SATS trading if the shorts were to unwind wither position.

Every day this coming week will see clarity on Echostar AWS3 value. Each day adding $3-6 of cash value. Echostar skipped a $100-200 million in debt payment a couple weeks ago. They will get the account with potential payment of $2.9 billion unlocked with the auction. Already $1.33 billion will be returned. All of that after Monday would be returned if the auction continues.

Jun 12

6

11

75

11,694

the third XAI AI data center. 2 Gigawatts of AI. After Colossus 2, Macrohardrr. @elonmusk

30 Dec 2025

xAI NEWS: An xAI subsidiary acquired the 810,000 sqft GXO warehouse in Southaven, Mississippi, earlier in December from an affiliate of ElmTree Funds, a private equity real estate firm owned by BlackRock.

xAI has built a new road in recent months between Colossus 2 and the GXO logistics building. MACROHARD(RR).

Find out more in today's ELON CHRON below!

8

96

7,033

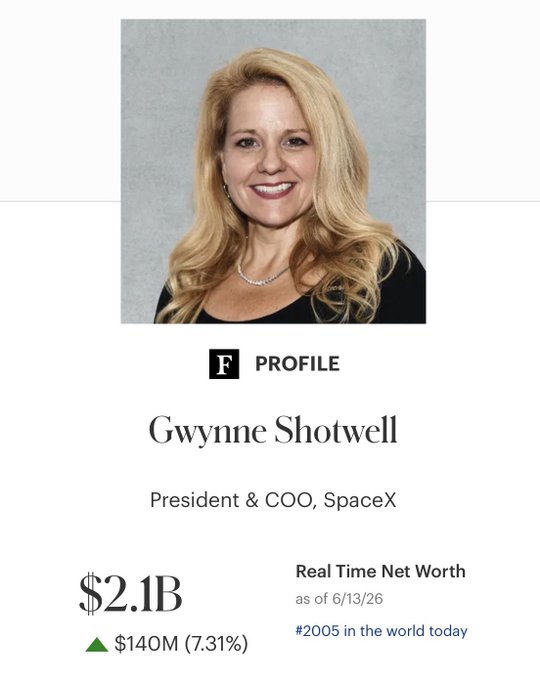

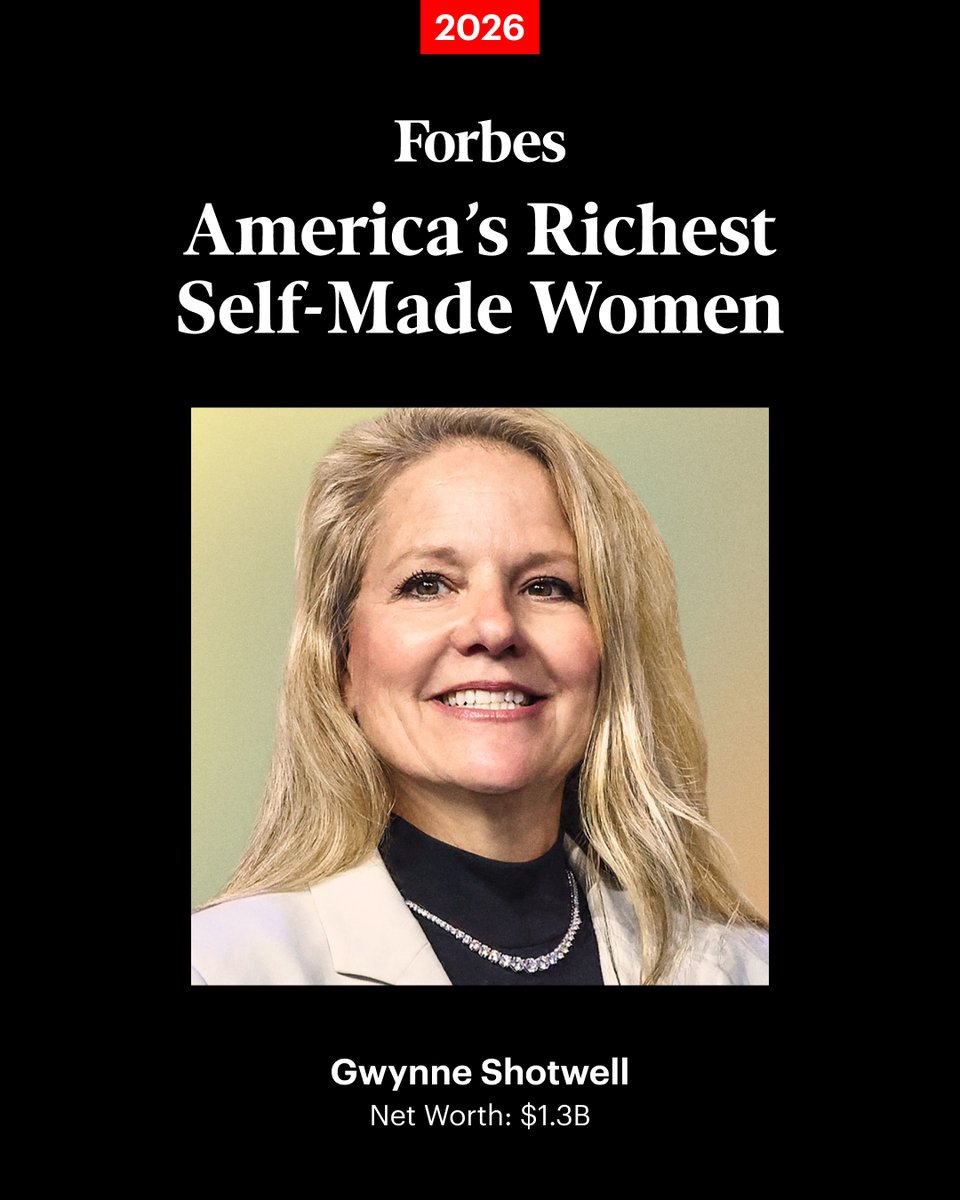

Gwynne Shotwell joined SpaceX in 2002 as its 11th employee. Today, as president and COO, she oversees operations at the commercial space exploration company.

Shotwell is featured on Forbes Richest #SelfMadeWomen. Read the full list: forbes.com/lists/self-made-w…

Photo: Angel Garcia via Bloomberg

1

1

36

2,170

Oil flows going around hormuz, sneaking oil through, using pipelines, increased us production and refining, strategic reserves. Increasing the amount going through that Iran cannot detect or stop. More alternatives gets to complete oil normalcy and lower gas prices.

1

1

16

895

Jun 13

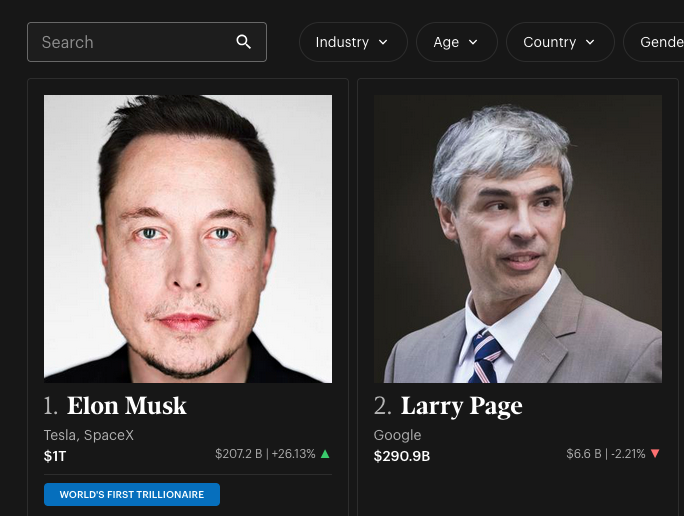

Buyers and sellers of the stocks and of the cars have paid over $100 billion in taxes and Elon has already paid $12 billion in taxes. Every year there is $6 trillion spent snd $4 trillion in taxes. Why would another $50 billion make The difference. You wasted all the other money but think this time you won’t waste it? @elonmusk. Elon already helped The government cut over $200 billion per year in waste. Stop wasting money.

Brad, a 5% tax on Elon's trillion net worth would literally pay for free college and trade school for every American.

And with the market's growth, he still would be worth over a trillion dollars!

You don't think that's worth it?

Community note

5% of $1.2T is $60b. 8m students in BA/BS programs on average pay over $20k/yr, or ~$160b/yr for BA/BS degrees only.

That tax could not cover even half of only US bachelor degree costs for just 1 year, excluding grad, ass., or trade degrees totaling another ~10m students.

nces.ed.gov/programs/coe/i…

bestcolleges.com/research/colle…

1

5

37

2,039

Jun 13

Luce the writer is upper class British. And he does not like the fact that @elonmusk was also outraged by the murder of Henry nowak. He feels this was interference in the UK internal affairs. He feels that if twitter still had leftists running it that they would go along with the UK censoring those who would speak up for anti white and anti traditional British. luce is correct that Elon has been anti censorship and expressed outrage at terrible events. I think Elon is on the side of right and Luce is on the side of wrong.

Jun 12

Elon Musk is a real-life Bond villain ft.trib.al/zAOuVKk

1

3

23

1,505

Jun 12

Spacex can be gotten for $99 per share by buying echostar $SATS

Jun 12

SpaceX stock for $99/shr?

This setup with EchoStar is quite interesting...

Effectively you can purchase SpaceX stock for about $99/share.

2

15

3,617

Jun 12

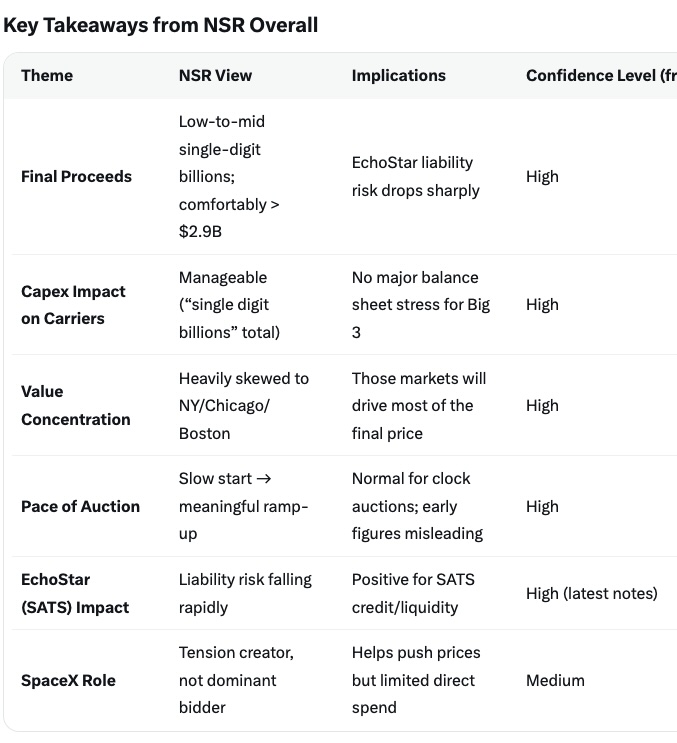

Echostar $SATS auction and discount on the 266 million spacex shares they have. New Street auction analysis is indicating a decent auction is likely. This should happen next week and the week after. Adding $500M to $1B per day next week to $1.1B and still 2 more rounds today. Bidders really wanting New York, Boston and Chicago markets would push the auction to over $5 billion by end of next week. No deadline of auction. Valuation from @CernBasher with some of my help. Does not include value for boost mobile or satellite internet and TV businesses.

4

9

80

78,121

Jun 12

Auction should be a catalyst next week, SpaceX going up with index inclusion. FCC removing all doubt on timing of $23B ATT money.

1

2

19

2,417

Jun 12

opening bell speech by Elon Musk

1

11

1,666

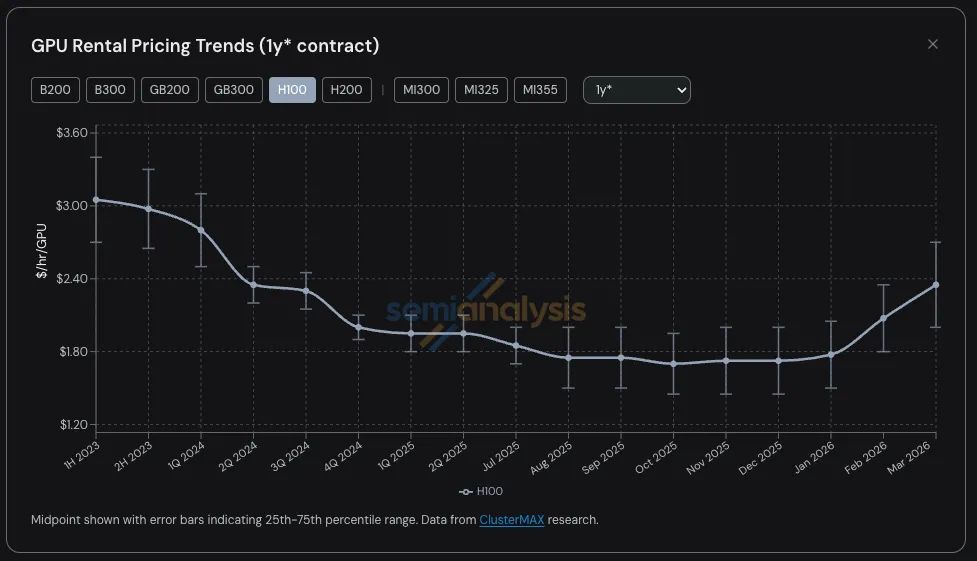

Jun 12

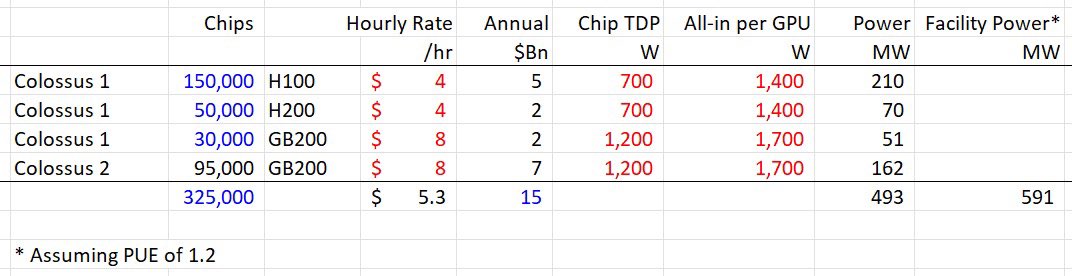

Broader GPU Market (Across Providers)

B200 medians Often $5–6/hr (ranges from ~$3.75 on cheaper neoclouds to $14 on hyperscalers like AWS).

B300 medians Often $6–7/hr (ranges from ~$6.10 to $18 on hyperscalers like Oracle).

Hyperscalers (AWS, Google Cloud, Oracle, etc.) Significantly higher — frequently $10–16 /hr for on-demand/spot B200.

Longer-term reserved contracts can be lower than pure on-demand but still elevated due to tightness.

Spot/interruptible (cheaper, can be preempted) is usually the lowest on Vast.ai.

On-demand/guaranteed costs more for uptime.

Availability is tighter for B300 (higher-end Blackwell Ultra) than B200.

Semianalysis H100 1-Click Rental Index, the spot market for compute has gone from finally cooling off in October to a hard squeeze again, in roughly five months.

Current Live Marketplace Prices (Cheapest Public Options)

Vast.ai(peer-to-peer marketplace — mix of interruptible/spot and on-demand)

B200 (192GB HBM3e)

Cheapest listings: ~$3.44/hr

Typical range: $3.44 – $7.45/hr

Median/typical: ~$4.5–4.7/hr (p25 ~$4.23, p90 ~$7/hr)

High availability.

B300 (Blackwell Ultra, 288GB)

Cheapest listings: ~$5.33/hr

Typical range: $5.33 – $7.33/hr (up to ~$8.27 at p90)

Median/typical: ~$6.2/hr

Medium availability.

RunPod (managed cloud, more reliable SLAs)

B200 (180–192GB): ~$5.89/hr (community/on-demand Pods).

B300 / HGX B300 (288GB) ~$6.94/hr.

Spot prices are generally 40–70% cheaper than on-demand rates but come with preemption risk.

Reserved contracts offer meaningful discounts versus on-demand (often 20–50%) with guaranteed availability and higher priority.

@elonmusk @WR4NYGov @herbertong @CernBasher @bradsferguson @RandyWKirk1

1

3

17

2,268

Jun 12

100 million barrels of oil were sent through Hormuz last month. Iran has no radar to detect ships.

Trump claimed a secret U.S. operation helped 200 commercial ships transit the Strait of Hormuz.

Now a June 5 INTERTANKO advisory reviewed by gCaptain describes a U.S.-coordinated nighttime route along the Omani coast involving ships operating with AIS off, navigational lights extinguished, and limited radar use.

The advisory not only corroborates with Trump's claims, but also offers the clearest description yet of how limited shipping has continued through Hormuz during the conflict.

Full story: gcaptain.com/tanker-industry…

3

12

1,375

Jun 11

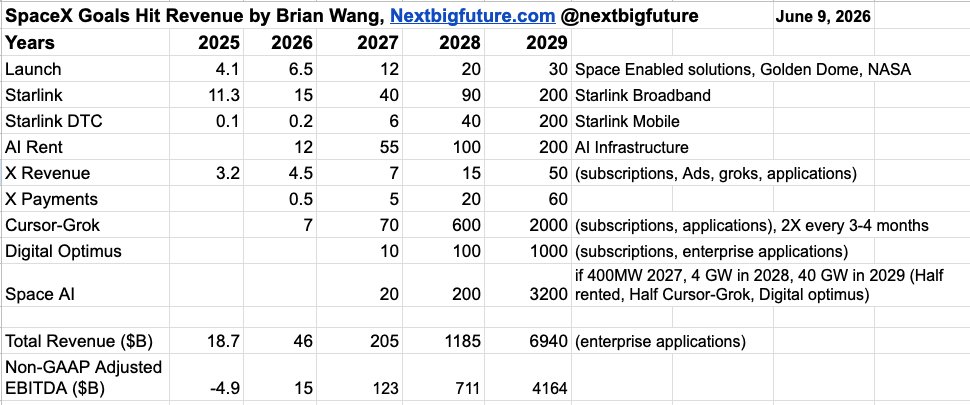

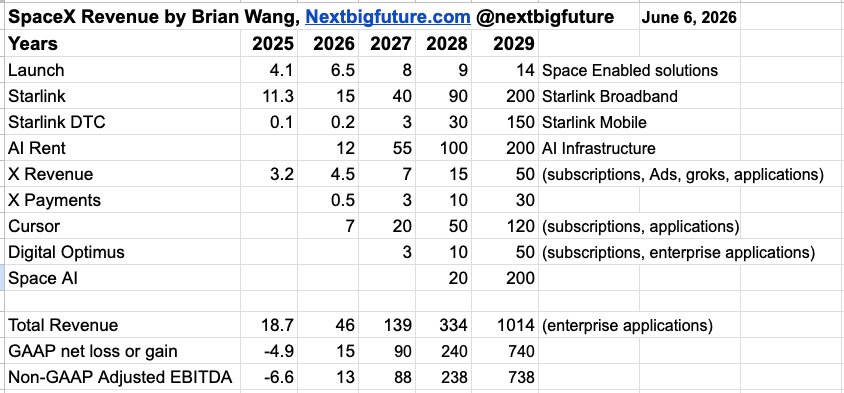

UNDERSTANDING SPACEX AND ITS AI AND SPACE BUSINESSES

Why Analysts Are Getting It Wrong

Most analysts are “feeling one part of the elephant”: understand space or AI, OR Not understanding either.

S1 (300-page F1) only covers through Q1 last year, predates the AI revenue pivot.

Many still exclude the new AI contract revenue from 2026 projections. JPMorgan, Morgan Stanley, and others have since validated Brian’s original numbers.

@elonmusk @spacex @aaronburnett @VladSaigau

3

6

38

2,897

Jun 11

The SPACEX AI Revenue Case

xAI already #2 in AI cloud rental, ahead of Google and Amazon on all cloud revenue

Current run rate: $26B/year in signed contracts (up from under $1B), mostly profitOnly using 40% of Colossus 2; fully rented out, run rate goes to $64B/year Full Colossus 1 2 rental would exceed Microsoft, Amazon, and Google cloud combined

Rubin chips (500K GPUs, ~1 GW): worth ~$100B/year in rental revenueIf xAI replicates Anthropic’s model capability, inference value 10x, pushing toward $300b to 400B/year. @elonmusk @ARKInvest @MilkRoadAI @chamath

Jensen Huang said 1 GW of data center is worth $300b to 400B/year in revenue. Complete AI data centers are worth more than a pile of components alone.

xAI can build new data centers in ~1 year vs. 4 years for competitors

Cursor acquisition closing gap with Anthropic’s Claude Code; Grok training 10x faster; models expected to converge

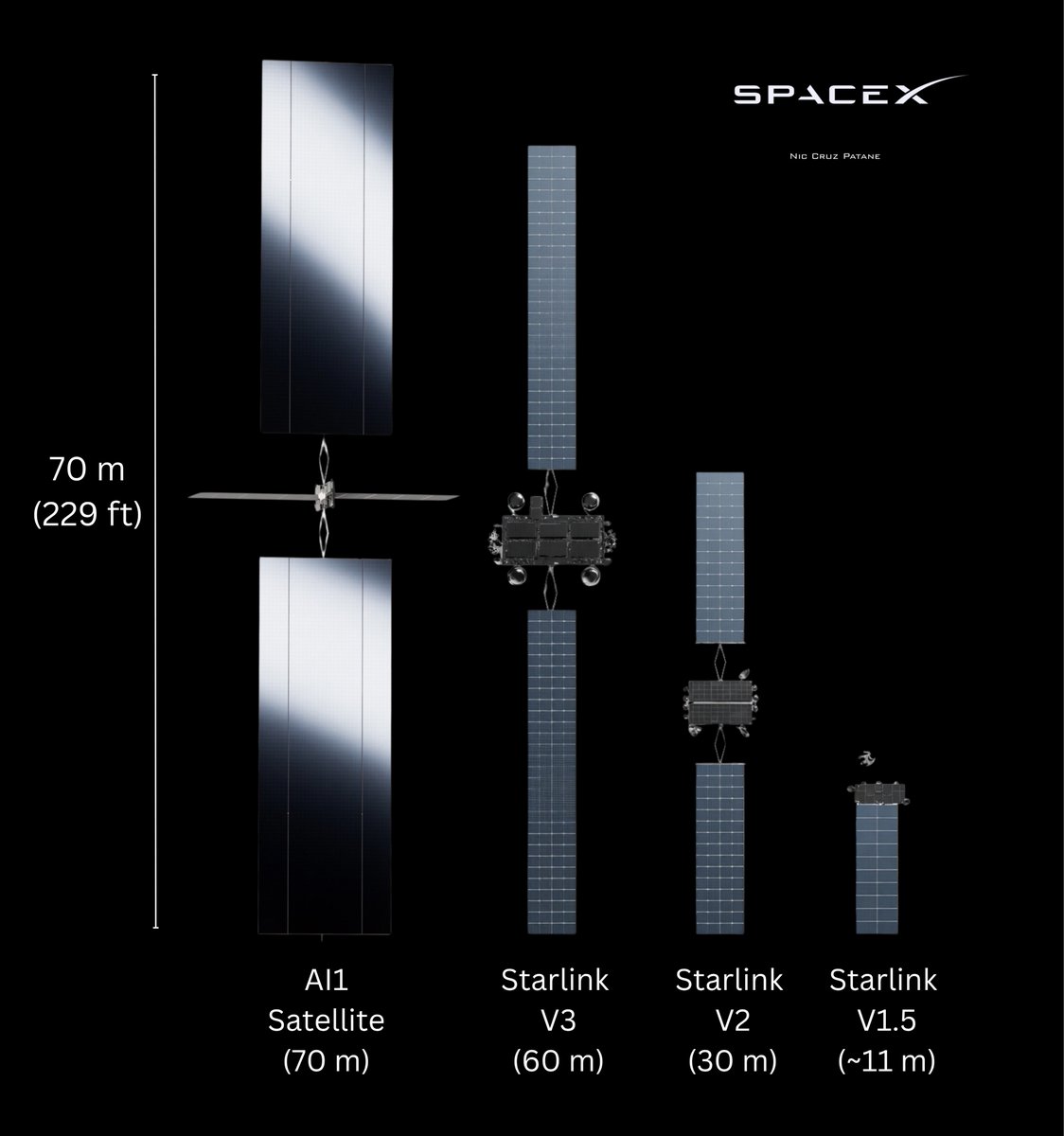

Starlink and Launch Moats

Starlink: 12M customers now, targeting 20M by year-end

Version 5 dish: thinner, cheaper, router built in, USB-C, battery-powered, no separate GPS neededDownload: up to 1-2 Gbps; upload: symmetrical gigabit, fully competitive with fiber Factory scaling from 1M dishes/month to 50K/day (~1.5M/month) in 2-3 months Elon flagged “a few hundred million dishes” as the deployment target, implying ~$200B/year in broadband revenue at $500/customer/year

Starlink Mobile: 650 satellites, video and text working now; V3 satellites bring 5G direct-to-cellCapacity scales 1,000x as satellite versions improve (V3 to V5)

SpaceX launches 75-90% of everything into orbit; dominance measured in decades

Starship V3 expected operational by July; each launch carries ~30x the capacity of 10 Falcon 9sTarget: 1,000 Starship launches in 2028, 4,000 in 2029, 14,000 by 2032 Even at 700K tons in 2030 (2-3 years late), still 1,000x ahead of nearest competitor

133 Starship launches needed per gigawatt of space-based AI 1 GW with Rubin chips worth $100b to 300B/year

Gigafactory expansion: 11M sq ft total complex, ~10x the size of Giga Austin. no competitor makes more than 100 satellites/year

Revenue Picture and IPO Framing

Four existing, revenue-generating businesses (not speculative). Launch and satellite manufacturing: dominant monopoly Starlink broadband: 12M customers, scaling fast AI infrastructure (xAI): $26B run rate, capacity to reach $64B per year just selling what exits. Consumer/digital advertising $3B/year now, path to $600B via X platform and Starlink Mobile on-ramp

Additional near-term streams Golden Dome (up to $1.2T over 20 years per CBO), Tesla supercharger rack co-location

IPO valued at ~$1.75T. Near-term technology catalysts include V3 Starship launches and V3 satellite deployment. Successful V3 launch in July would crystallize the roadmap skeptics currently push to 2028

At 100 GW of launch capacity and Feynman-era chips: potential revenue in the multi-trillion range, exceeding the combined EBITDA of today’s top 20 companies

2

1

8

1,219

Jun 11

Fully dry 4680 battery is great for Tesla

Jun 11

As usual, my next video is up early for paid supporters on Patreon and X. 🤠

'The Fully Dry 4680 // Too little too late?'

In the face of solid state and sodium ion batteries that offer higher energy densities and lower costs, people are wondering if the fully dry 4680 is still relevant.

In short, it is, because it's meeting Tesla's original goals for the 4680 project.

Not all the goals have been met yet, but they're working through them in order of importance:

✅Strategic Risks Addressed

🟨Cost Cutting is Going Well

🟥Performance is Moderate

But, more importantly, sodium ion batteries and solid state batteries are chemistries, not manufacturing innovations, which is what the 4680 is at its core.

Ultimately, the fully dry process will benefit those chemistries as well, because it's fundamentally a better way to manufacture a battery cell.

*Timestamps*

00:00 Introduction

01:00 Tesla’s Goals for the 4680 Project

03:31 ‘Obsolete’ Argument #1 - Performance

05:57 ‘Obsolete’ Argument #2 - Cost

10:14 The Fully Dry 4680 is NOT a Chemistry

11:40 Summary

2

2

35

5,097

Jun 11

My napkin math had arrived at similar numbers. Jensen confirmed

5

7

82

6,697