Jun 12

Hidden Growth Engine: Astra Rafael Comsys (ARC)

• FY26 Revenue: ₹360 Cr

• FY27 Revenue Target: ₹600 Cr

• Driven by Software Defined Radios, Tactical Communication Systems and EW Solutions.

1

1

261

🇯🇵 日本株、次の主役はアクティビストか。

“変われない会社”が狙われる時代に入った。

msn.com/en-us/money/news/202…

1/3

OasisのSeth Fischerが挙げた、日本のアクティビスト候補は7社。

KADOKAWA (9468 JP)

京セラ (6971 JP)

東京製鐵 (5423 JP)

SMS (2175 JP)

COMSYS (1721 JP)

EXEO (1951 JP)

ミライト・ワン (1417 JP)

共通点は明確。

“事業は悪くない。でも経営と資本配分が弱い。”

1

1

2

342

Jun 1

𝗔𝘀𝘁𝗿𝗮 𝗠𝗶𝗰𝗿𝗼𝘄𝗮𝘃𝗲 𝗣𝗿𝗼𝗱𝘂𝗰𝘁𝘀 𝗟𝘁𝗱: 𝗤4 𝗙𝗬26 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗖𝗮𝗹𝗹 𝗦𝘂𝗺𝗺𝗮𝗿𝘆:

𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝘆 𝗢𝘂𝘁𝗹𝗼𝗼𝗸 & 𝗖𝗼𝗺𝗽𝗮𝗻𝘆 𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻

- The defence industry outlook remains highly supportive, driven by government's focus on indigenization, with ~75% of India's defence capital acquisition budget allocated to domestic companies.

- Long-term defence manufacturing cycle is robust, supported by accelerating government procurement & increasing localization.

- Defence exports exceeded ₹38,000 Cr in FY26. Global supply chain diversification & rising defence spending create additional opportunities.

- Astra Microwave Products Ltd is well-positioned to benefit from these trends, with FY27 & FY28 expected to witness stronger execution & improved revenue conversion. The company sees itself transitioning from a subsystem supplier to a deeply integrated, IP-driven systems manufacturer & development-cum-production partner.

𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 (𝗙𝗬26)

- 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹1,157 Cr, meeting guidance.

- 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄: ₹370 Cr (significant improvement from -₹99 Cr last year).

- 𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸: ₹2,141 Cr as of March 31, 2026.

- 𝗗𝗶𝘃𝗶𝗱𝗲𝗻𝗱: Board recommended ₹2.40 per equity share (120% of face value) for FY25-'26, subject to shareholder approval.

- 𝗠𝗮𝗿𝗴𝗶𝗻 𝗧𝗿𝗮𝗷𝗲𝗰𝘁𝗼𝗿𝘆: Margins are expected to strengthen or remain at current levels due to increased value addition in exports & the JV (ARC), with gross margins on certain exports close to 40%. The company is moving away from low-margin build-to-print business.

𝗞𝗲𝘆 𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀 𝗗𝗲𝘃𝗲𝗹𝗼𝗽𝗺𝗲𝗻𝘁𝘀 & 𝗦𝗲𝗴𝗺𝗲𝗻𝘁𝘀

- 𝗥𝗮𝗱𝗮𝗿 𝗦𝗲𝗴𝗺𝗲𝗻𝘁: Primary growth driver, contributing ~60% of revenue. Expects to contribute ~45% in FY27.

- 𝗦𝗽𝗮𝗰𝗲 & 𝗠𝗲𝘁𝗲𝗼𝗿𝗼𝗹𝗼𝗴𝘆 𝗦𝗲𝗴𝗺𝗲𝗻𝘁: Contributed ~16% of revenue. Key orders include subsystems for the Gaganyaan mission & defence satellite programs. Expects continued contributions from ISRO & defence side.

- 𝗔𝘀𝘁𝗿𝗮 𝗥𝗮𝗳𝗮𝗲𝗹 𝗖𝗼𝗺𝘀𝘆𝘀 (𝗝𝗩): Closed FY26 with an order book of ~₹625 Cr. Expected to deliver a top line of over ₹600 Cr in FY27, with projected EBITDA margins of 18-20%. Share of profit from JV for FY26 was ~₹8 Cr (after tax).

- 𝗗𝗲𝗺𝗲𝗿𝗴𝗲𝗿 𝗣𝗹𝗮𝗻: Board approved in-principle demerger of space, meteorology, & hydrology business to create sharper focus & unlock value.

- 𝗣𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗣𝗿𝗼𝗱𝘂𝗰𝘁𝘀: Proactive investment in R&D, particularly in MMIC technologies, to develop Astra-owned IP & branded products for Indian & global markets. Multiple such products expected before Diwali.

𝗙𝘂𝘁𝘂𝗿𝗲 𝗢𝘂𝘁𝗹𝗼𝗼𝗸 & 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

- 𝗙𝗬27 𝗥𝗲𝘃𝗲𝗻𝘂𝗲 𝗚𝗿𝗼𝘄𝘁𝗵: Reaffirmed at 15% to 20% (₹1,300 Cr to ₹1,400 Cr).

- 𝗟𝗼𝗻𝗴-𝘁𝗲𝗿𝗺 𝗚𝗿𝗼𝘄𝘁𝗵: Company aims to triple turnover in 4.5 to 5.5 years, potentially reaching over $0.5 billion revenue enterprise in the next decade, driven by programs like QRSAM, Uttam radars, Su-30 upgrades, & BEL programs. Proprietary IP-led opportunities are not factored into this near-term growth aspiration.

- 𝗖𝗮𝗽𝗲𝘅: Ongoing capex of ~₹40-50 Cr annually is sufficient; no additional major capex planned.

- 𝗪𝗼𝗿𝗸𝗶𝗻𝗴 𝗖𝗮𝗽𝗶𝘁𝗮𝗹: Improvement expected to continue, managing within sanctioned limits.

𝗡𝗼𝘁𝗮𝗯𝗹𝗲 𝗤&𝗔 𝗣𝗼𝗶𝗻𝘁𝘀

- 𝗘𝘅𝗽𝗼𝗿𝘁𝘀: Exports are now more IP-driven & have higher value addition (~40% gross margin), unlike previous offset-based exports.

- 𝗦𝘂𝗸𝗵𝗼𝗶 𝗨𝗽𝗴𝗿𝗮𝗱𝗲 (𝗦𝘂-30): Development of AAAU for Virupaksha radar & Angad EW program (pod jammer) is ongoing. Production orders are expected possibly in FY28-FY29 after qualification.

- 𝗤𝗥𝗦𝗔𝗠 & 𝗨𝘁𝘁𝗮𝗺 𝗔𝗘𝗦𝗔 𝗥𝗮𝗱𝗮𝗿: Negotiations for Uttam radar with HAL are nearing completion, with orders expected in Q2/Q3. Small quantity orders for the FOPM version of QRSAM have started, with main contract orders expected in 3-4 months post BEL's contract.

- 𝗠𝗠𝗜𝗖: No issues encountered; in-house MMIC division supplies active devices, & the company is promoting MMICs to domestic & international players.

- 𝗚𝗿𝗼𝘂𝗻𝗱 𝗣𝗲𝗻𝗲𝘁𝗿𝗮𝘁𝗶𝗻𝗴 𝗥𝗮𝗱𝗮𝗿𝘀: Trials completed, addressing observations, & product launch expected soon.

- 𝗠𝗮𝗿𝗴𝗶𝗻 𝗦𝘂𝘀𝘁𝗮𝗶𝗻𝗮𝗯𝗶𝗹𝗶𝘁𝘆: Management indicated that current margins are strong & the company aims to sustain them, with potential for improvement based on product mix & value addition.

📊 ASTRA MICROWAVE PRODUCTS LTD | 🏷️ Earnings Call Transcript

🌐 Details: wegro.app/pbFlWx

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

3

152

May 28

📊 Astra Microwave Products Ltd | Broker Report | 𝘉𝘜𝘠 𝘊𝘢𝘭𝘭 🟢

🏢 𝘉𝘶𝘺 𝘈𝘴𝘵𝘳𝘢 𝘔𝘪𝘤𝘳𝘰𝘸𝘢𝘷𝘦 𝘗𝘳𝘰𝘥𝘶𝘤𝘵𝘴; 𝘵𝘢𝘳𝘨𝘦𝘵 𝘰𝘧 𝘙𝘴 1580: 𝘔𝘰𝘵𝘪𝘭𝘢𝘭 𝘖𝘴𝘸𝘢𝘭

📈 𝘙𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯: BUY

🏛️ 𝘉𝘳𝘰𝘬𝘦𝘳𝘢𝘨𝘦: Motilal Oswal

Astra Microwave Products' FY26 results exceeded expectations, driven by robust margin resilience and profitability beats. The company reported a 29% YoY increase in FY26 order inflows, reaching ₹16.6 billion. Notably, export inflows showed strong momentum in 4QFY26, propelled by higher-value RF systems and Software-Defined Radio (SDR) opportunities. 🚀

𝗞𝗲𝘆 𝗚𝗿𝗼𝘄𝘁𝗵 𝗗𝗿𝗶𝘃𝗲𝗿𝘀:

Looking ahead, Astra Microwave Products anticipates significant growth from projects like Uttam radar, QRSAM, Su-30 upgrades, Electronic Warfare (EW) systems, weather radars, and strategic space programs. The company's strategic focus remains on developing IP-led and proprietary defense solutions for both domestic and global markets. 🛰️

𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 & 𝗢𝘂𝘁𝗹𝗼𝗼𝗸:

Motilal Oswal has revised its FY27/FY28 earnings estimates upwards by 7% and 15% respectively, factoring in improved margins and higher other income. They anticipate execution ramp-up beyond FY27 as large-ticket orders are finalized. The brokerage reiterates its 'BUY' rating with a raised target price (TP) of ₹1,580 (up from ₹1,150), representing a 13% upside.

𝗙𝗬26 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

- Revenue grew 20% YoY to ₹4.8 billion, exceeding estimates by 7%.

- Gross margin expanded 420 basis points YoY to 50.3%.

- EBITDA surged 36% YoY to ₹1.6 billion, beating estimates by 39% with a margin expansion of 400 basis points to 33.3%.

- Adjusted PAT increased 44% YoY to ₹1.1 billion, driven by better margins, other income, and lower interest costs.

- Consolidated FY26 revenue, EBITDA, and PAT grew 11%, 24%, and 26% YoY respectively, with EBITDA margin expanding 310 basis points to 28.7%.

- Order book stood at ₹26.1 billion.

- Operating Cash Flow (OCF) and Free Cash Flow (FCF) were ₹4 billion and ₹3 billion respectively in FY26.

𝗦𝗲𝗴𝗺𝗲𝗻𝘁𝗮𝗹 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

- 𝗗𝗲𝗳𝗲𝗻𝘀𝗲: Revenue remained flat YoY, while inflows increased 4% YoY. The segment continues to scale across radar, EW, missile, and strategic electronics programs. 🛡️

- 𝗠𝗲𝘁𝗲𝗼𝗿𝗼𝗹𝗼𝗴𝘆: Revenue grew 40% YoY, with inflows up 43% YoY, driven by weather radar projects and expansion into specialized applications.

- 𝗦𝗽𝗮𝗰𝗲: Revenue increased 90% YoY, driven by participation in strategic satellite and ISRO-linked programs. 🌌

- 𝗘𝘅𝗽𝗼𝗿𝘁𝘀: Revenue grew 48% YoY, with a sharp ramp-up in 4QFY26. The business is transitioning towards co-developed and proprietary solutions, enhancing margins and value addition. 🌍

𝗝𝗼𝗶𝗻𝘁 𝗩𝗲𝗻𝘁𝘂𝗿𝗲 (𝗝𝗩) 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

Astra Rafael Comsys (ARC) secured ~₹5.5 billion in fresh orders, ending FY26 with an order book of ~₹6.3 billion. The JV targets revenues over ₹6 billion in FY27 with an expected EBITDA margin improvement to ~18-20%.

𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲:

For FY27, the company targets revenue of ₹13-14 billion (~15-20% YoY growth). Over the medium term, it aims to nearly triple revenue by FY30-31, supported by large strategic programs and improving operating leverage. Capex is expected to be manageable at ~₹400-500 million annually. 📈

𝗗𝗲𝗺𝗲𝗿𝗴𝗲𝗿 𝗣𝗹𝗮𝗻:

Astra Microwave Products is proposing to demerge its Space and Metrology businesses to enhance strategic focus, operational efficiency, and corporate governance across segments.

𝗩𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻:

The stock is trading at ~40.5x FY28E EPS. The 'BUY' rating and revised TP of ₹1,580 reflect the improved order visibility and strong growth prospects.

🔗 𝘙𝘦𝘢𝘥 𝘍𝘶𝘭𝘭 𝘙𝘦𝘱𝘰𝘳𝘵: wegro.app/pXvkUo

⚡️AI-driven watchlist alerts on WhatsApp - Try FREE 👉 wegro.app/go #BrokerageReport

4

127

May 27

🛰️ Astra Microwave Products Q4FY26 concall insights - Margin Expansion & Defense Scale-Up

🚀 FY26 Ended With Record Numbers

• Revenue reached ₹1,157 Cr with Q4 billing up 16% YoY to ₹490 Cr

• Operating cash flow jumped sharply to ₹370 Cr from negative last year

• Q4 EBITDA margin expanded strongly to 33.3% on exports and space mix

📈 Order Book Continues To Build

• Standalone order book remained healthy at ₹2,141 Cr

• ₹530 Cr fresh Q4 wins secured with ₹300 Cr negotiations concluded

• Radar business contributed nearly 60% of total revenue

🎯 Management Sees Strong FY27 Momentum

• FY27 revenue guidance set at ₹1,300-1,400 Cr with 15-20% growth target

• Company expects over ₹1,600 Cr order inflow during FY27

• Management aims to nearly triple revenue over next 5 years

🛡️ Large Defense Programs Nearing Execution

• Uttam AESA radar negotiations entered final stages

• QRSAM and Su-30 upgrade opportunities expected to drive future growth

• Transition underway from subsystem supplier to IP-led systems player

🌌 Strategic Restructuring Taking Shape

• Board approved demerger of Space Meteorology and Hydrology businesses

• Multiple Astra-branded products planned before Diwali launch window

🤝 JV Growth Could Surprise Positively

• Astra Rafael Comsys targets ₹600 Cr FY27 sales

• JV order book guidance stands at ₹1,200 Cr for FY27

• JV profit contribution expected above ₹20 Cr next year

🚫 No Recommendation

Source: Concall.in

5 Oct 2025

🛡️ Astra Microwave Products – Dual Engines of Growth | Rerating ahead 📈

📌 Astra Microwave isn’t just a radar company anymore. They are quietly transforming into a multi-tech defense innovator with Rerating triggers.

📊 Rerating - Valuation Triggers

FY27–28 optionality → Anti-drone, Tank, Space and Uttam

▪️Anti-Drone Systems – In 30 tenders, Astra has long-range multi-band jamming edge. Early mover in a high-growth niche.

▪️Tank Protection Radar (Army APS) – Prototype delivered; orders from FY27/28 → sticky Army adoption cycle.

▪️Uttam Radar (LCA Mk1A) – 97 jets in Phase 2; Astra embedded in HAL’s fighter jet production ramp.

▪️Space Business – ₹239 Cr OB today → tomorrow’s satellite integration & data monetisation play. Global comps show rerating potential.

▪️MMIC Chips Scale-up – GaAs/GaN → CMOS/BiCMOS; global sales optionality = tech rerating story.

💡 Rerating triggers = Astra’s transition from subsystem supplier → system-level deep-tech innovator.

🚫 No Recommendation. Shared for educational purposes only. DYODD.

#AMP #AstraMicroWave #Defence #MakeInIndia #ViksitBharat #StocksInFocus @deepak4748 @Chart_Wallah108

2

4

27

4,361

May 27

Astra Microwave Products Q4 FY26 concall insights - Margin Expansion & Defense Scale-Up

🚀 FY26 Ended With Record Numbers

• Revenue reached ₹1,157 Cr with Q4 billing up 16% YoY to ₹490 Cr

• Operating cash flow jumped sharply to ₹370 Cr from negative last year

• Q4 EBITDA margin expanded strongly to 33.3% on exports and space mix

📈 Order Book Continues To Build

• Standalone order book remained healthy at ₹2,141 Cr

• ₹530 Cr fresh Q4 wins secured with ₹300 Cr negotiations concluded

• Radar business contributed nearly 60% of total revenue

🎯 Management Sees Strong FY27 Momentum

• FY27 revenue guidance set at ₹1,300-1,400 Cr with 15-20% growth target

• Company expects over ₹1,600 Cr order inflow during FY27

• Management aims to nearly triple revenue over next 5 years

🛡️ Large Defense Programs Nearing Execution

• Uttam AESA radar negotiations entered final stages

• QRSAM and Su-30 upgrade opportunities expected to drive future growth

• Transition underway from subsystem supplier to IP-led systems player

🌌 Strategic Restructuring Taking Shape

• Board approved demerger of Space Meteorology and Hydrology businesses

• Multiple Astra-branded products planned before Diwali launch window

🤝 JV Growth Could Surprise Positively

• Astra Rafael Comsys targets ₹600 Cr FY27 sales

• JV order book guidance stands at ₹1,200 Cr for FY27

• JV profit contribution expected above ₹20 Cr next year

#ASTRAMICRO #Q4FY26 #Concall

1

3

721

May 17

يا شباب حد يعرف حد يعرف حد يعرف حد يعرف حد فيه شركة Comsys

بنبعتلهم ايميلات ومحدش بيرد ومحتاجين نعمل integration معاهم

1

8

872

May 14

What a day!

Buying ↗️↗️ :

The Shiga Bank, Ltd. (TSE:8366) — Ariake from 5.31% → 6.48%

Iwabuchi Corporation (TSE:5983) — Senjin Capital from 5.54% → 6.63%

Synchro Food Co., Ltd. (TSE:3963) — AVI from 26.68% → 27.68%

SENKO Group Holdings Co., Ltd. (TSE:9069) — NAVF from 10.88% → 11.91%

The Hyakugo Bank, Ltd. (TSE:8368) — Ariake from 5.06% → 5.94%

SMS Co., Ltd. (TSE:2175) — Oasis from 17.58% → 18.30%

COMSYS Holdings Corporation (TSE:1721) — Oasis from 5.61% → 6.32%

Wacom Co., Ltd. (TSE:6727) — AVI from 13.17% → 13.74%

eGuarantee, Inc. (TSE:8771) — Ariake from 9.75% → 10.31%

The Ogaki Kyoritsu Bank, Ltd. (TSE:8361) — Ariake from 8.00% → 8.57%

FUJIKURA COMPOSITES Inc. (TSE:5121) — Hibiki Path from 8.63% → 9.23%

Internet Initiative Japan Inc. (TSE:3774) — Oasis from 7.48% → 8.04%

Kokuyo Co., Ltd. (TSE:7984) — Oasis from 9.91% → 10.50%

Aichi Financial Group, Inc. (TSE:7389) — Ariake from 10.49% → 10.93%

Buffalo Inc. (TSE:6676) — Hiroyuki Maki from 17.75% → 18.19%

Lifenet Insurance Company (TSE:7157) — Ariake from 7.12% → 7.39%

Senshu Ikeda Holdings, Inc. (TSE:8714) — Ariake from 10.70% → 10.80%

Kobayashi Pharmaceutical Co., Ltd. (TSE:4967) — Oasis from 13.06% → 13.37%

Selling ↘️↘️ :

Shimadaya Corporation (TSE:250A) — Hiroyuki Maki from 14.87% → 13.93%

Calbee, Inc. (TSE:2229) — Oasis from 7.33% → 7.12%

1

17

2,591

Apr 6

Check that book, i found that Garret SatComm from Dalton, in the FWL, actually make those products. A ComSys called the Garret T11-b, and a T&TS called the Garret T11b. Only one "-" of diference between the two. >

1

1

13

414

Apr 6

When i was entering the data of both TRO:3025 and TRO:3039 i found a discrepancy. While the TRO3025 gives the mech a ComSys called the Tek BattleCom, TRO3039 gives it the Garret T11-b. So far, somethign that have happened bettwen the two books.>

1

14

358

Apr 3

#AstraMicrowave – Orders & Strategic Updates 👇

(🔔 Real-time Order alerts on WhatsApp → finq.in)

✅ ₹275.27 Cr – SDR/NCO order (IAF: MiG-29 24 LCA Mk-1A) via JV

🕒 Date: Jan’26

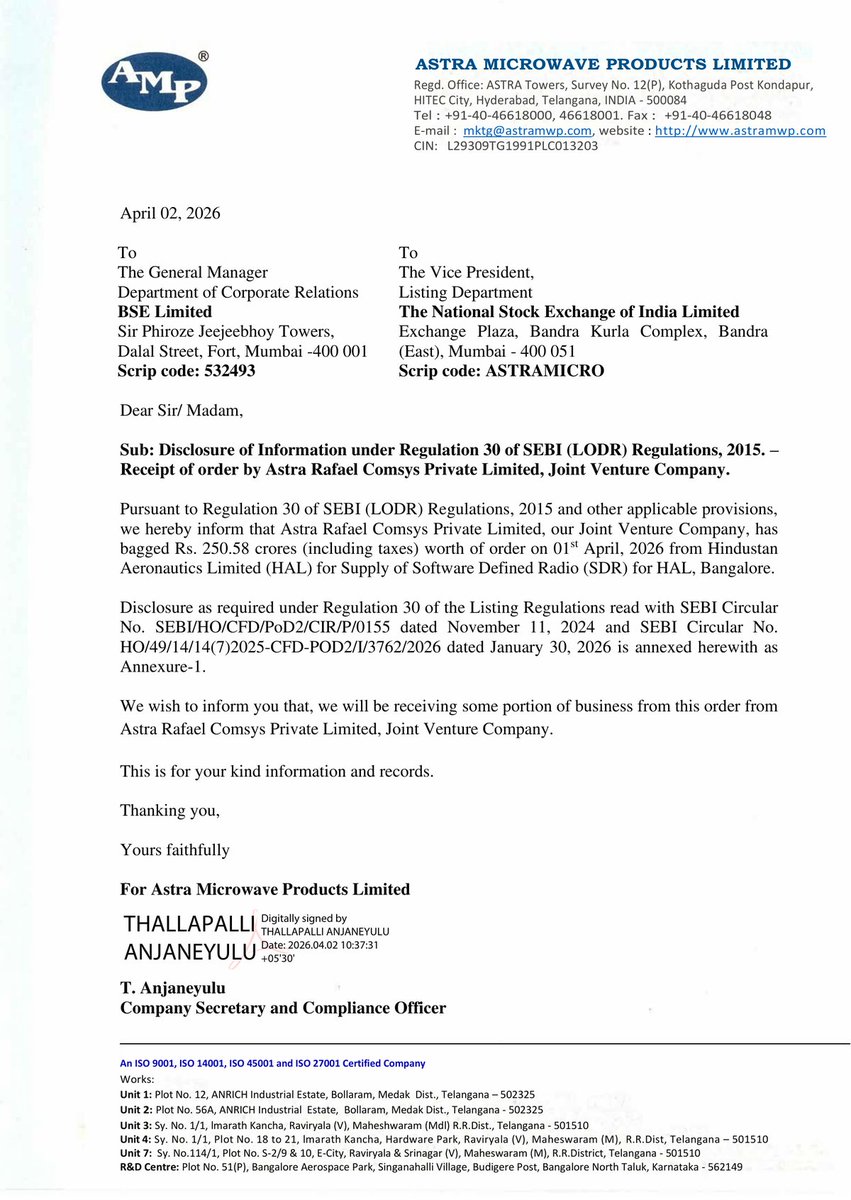

✅ ₹250.58 Cr – HAL order for SDR supply via JV Astra Rafael Comsys

🕒 Duration: 18 months

✅ ₹171.38 Cr – IMD order for 6 Doppler Weather Radars

🕒 Duration: 18 months 7-year CAMC

✅ ₹135 Cr – DRDO radar system upgrade

🕒 Duration: 18 months

✅ ₹124 Cr – SDR modules, cable assemblies & antennas

🕒 Duration: 9–12 months

⸻

🤝 Strategic Moves

• MoU with BEL for EW, radar & satellite defence systems

• Demerger approved: Space, Meteorology & Hydrology → Astra Space Technologies

🕒 Target listing: Q1 FY28

⸻

📊 Key Updates

• Order book: ₹1,916 Cr (as of Nov’25)

• ₹174 Cr raised via preferential warrants

5

330

Astra Microwave

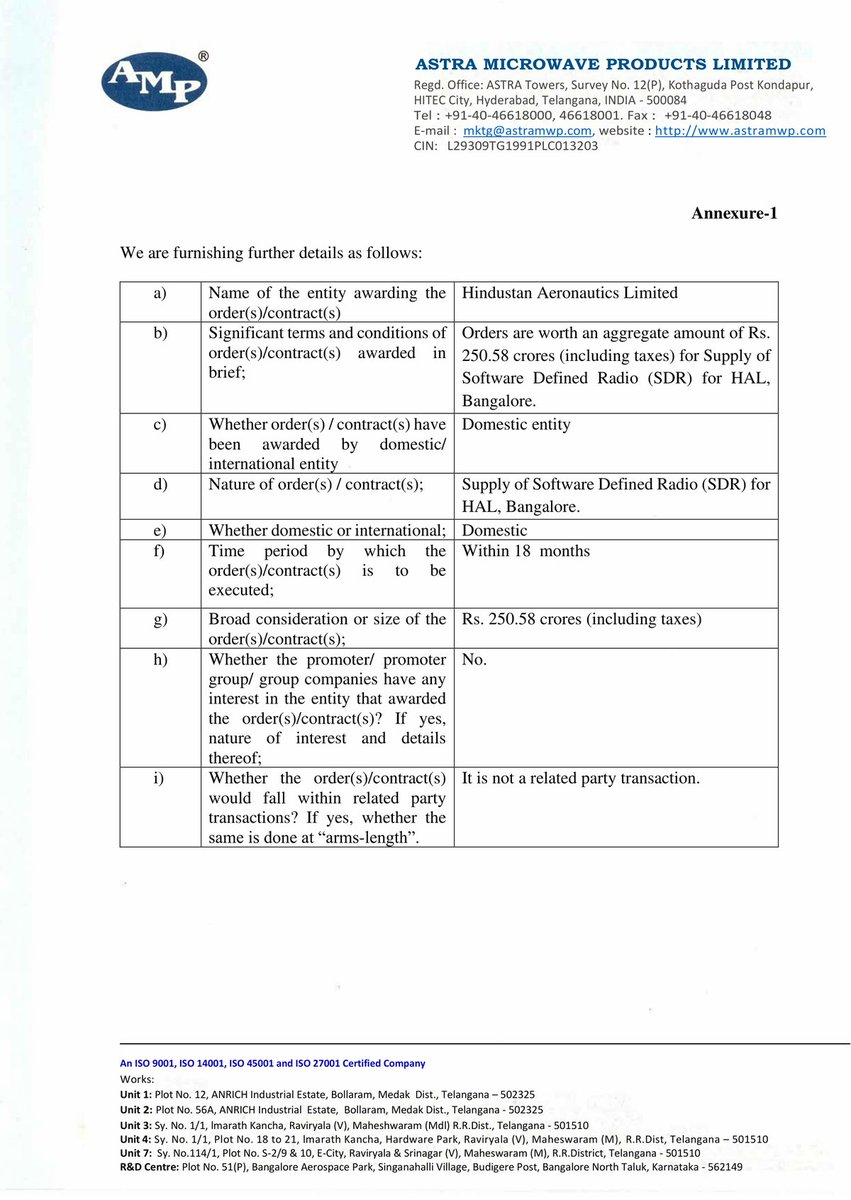

Receipt Of Order By Astra Rafael Comsys Private Limited, Joint Venture Company.

JV Astra Rafael Comsys won Rs. 250.58 crore HAL order for SDR supply within 18 months.

1

16

1,012

📡 Astra Microwave JV Secures ₹250.58 Crore Order from HAL | MCap 9,447.03 Cr

• Astra Rafael Comsys JV received ₹250.58 crore order from Hindustan Aeronautics Limited

• Order is for supply of Software Defined Radio (SDR) systems

• Execution timeline: 18 months

• Astra Microwave Products Limited will receive a portion of the business

Complete Source: bseindia.com/xml-data/corpfi…

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

2

4

293

ASTRA MICROWAVE PRODUCTS – JV ORDER WIN 🚀

• 📦 Order Value: ₹250.58 Cr (incl. taxes)

• 🤝 JV: Astra Rafael Comsys Pvt Ltd

• 🏢 Client: Hindustan Aeronautics Limited (HAL), Bangalore

• 📡 Scope: Software Defined Radio (SDR) supply

• ⏳ Timeline: 18 months

• 💼 Upside: Astra Microwave to receive share from JV

#AstraMicrowave #DefenceStocks #HAL #OrderWin #MakeInIndia #StockMarketIndia #Aerospace #DefenceSector

3

197

ASTRA MICROWAVE: JV ASTRRA RAFAEL COMSYS RECEIVES ORDER WORTH ₹250.58 CRORES FROM HINDUSTAN AERONAUTICS LIMITED FOR SUPPLY OF SOFTWARE DEFINED RADIO

2

9

76

13,734

🚨 High : ASTRAMICRO

⭐ 250 cr | rs. 250.58 crores | Company Received New Order⭐

astra rafael comsys, a joint venture, bagged a rs. 250.58 crores order from hal for supply of software defined radio.

#ASTRAMICRO #StockMarket #StockAlertsIndia

2

46

Quality Power operates in a highly specialized segment of power quality and high-voltage equipment, where the number of true competitors is limited.

Among the closest comparable global players are Schaffner Holding AG, Comsys AB, MTE Corporation, Arteche Group, and CIRCUTOR.

Within this group, Arteche Group stands out as significantly larger, with revenues of over €500 million, making it several times bigger than

Quality Power, whose revenue is in the ₹300–800 crore range. The remaining players largely fall into a similar mid-sized category or are even smaller, often operating as niche or component-focused companies rather than full-system solution providers.

The nature of this industry further shapes the competitive landscape. Products are highly customized, engineering and design capabilities are critical, and approval cycles especially with utilities and industrial clients are long and stringent. These factors naturally limit the number of credible participants. As a result, the market remains fragmented, with no single company dominating globally.

Quality Power competes in a niche where large multinational players are present but not deeply focused, smaller players lack the capability to deliver complex solutions, and only a handful of specialized firms operate at a comparable level.

1

9

668