54m

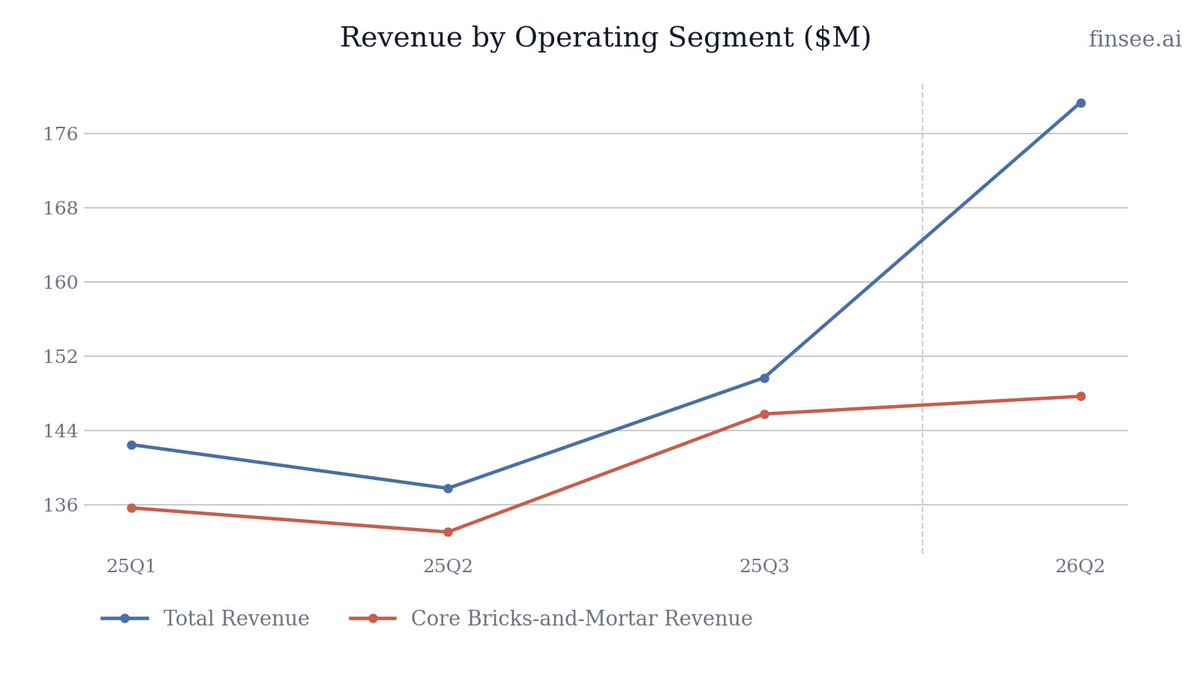

$HITI Q2 2026 earnings: Acquisition Masks Decelerating Core Growth as E-Commerce is Swept Under the Rug

High Tide posted a massive 30% YoY revenue jump to $179.3M and reached near-breakeven Net Income ($24k). However, the headline growth is a mirage. Almost all the incremental revenue came from the newly acquired German distributor, Remexian ($31.6M), which contributed just $372k in operating profit (1.2% margin). Meanwhile, the legacy Bricks-and-Mortar business decelerated to 7% YoY growth. Management also quietly merged the rapidly shrinking e-commerce division into the retail segment, obscuring its continued collapse. High Tide is trading quality for volume, and the core Canadian retail engine is no longer growing at historical rates, though its profitability is recovering.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐂𝐨𝐫𝐞 𝐑𝐞𝐭𝐚𝐢𝐥 𝐏𝐫𝐨𝐟𝐢𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 — Despite slower top-line growth, the Bricks-and-Mortar segment expanded operating income from $0.9M in 25Q2 to $5.7M in 26Q2. The company is extracting massive operating leverage from its established Canadian footprint.

• 𝐏𝐨𝐬𝐢𝐭𝐢𝐯𝐞 𝐍𝐞𝐭 𝐈𝐧𝐜𝐨𝐦𝐞 𝐌𝐢𝐥𝐞𝐬𝐭𝐨𝐧𝐞 — High Tide successfully reversed its multi-year trend of net losses, achieving $24k in consolidated Net Income this quarter (up from a $2.8M loss a year ago).

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐋𝐨𝐰-𝐌𝐚𝐫𝐠𝐢𝐧 𝐃𝐢𝐥𝐮𝐭𝐢𝐨𝐧 — The new Medical Cannabis Distribution segment operates on a razor-thin 1.2% operating margin, drastically altering the company's profitability profile and dragging down consolidated returns on capital.

• 𝐄-𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐎𝐛𝐟𝐮𝐬𝐜𝐚𝐭𝐢𝐨𝐧 — By merging the failing e-commerce business into the Bricks-and-Mortar segment, management has reduced transparency. U. S. revenues (a proxy for e-commerce) plunged another 30% YoY.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The core Canadian retail business is highly profitable and cash-generative, but the pivot toward low-margin European wholesale and the obfuscation of the failing e-commerce segment raise serious concerns about capital allocation and long-term margin trajectory.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴 𝐄-𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐂𝐨𝐥𝐥𝐚𝐩𝐬𝐞 𝐇𝐢𝐝𝐝𝐞𝐧 𝐛𝐲 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐌𝐞𝐫𝐠𝐞𝐫 [NEW]

Effective February 1, 2026, High Tide combined its struggling e-commerce segment into its Bricks-and-Mortar segment. This is a classic tactic to hide a declining business. Looking at the geographic breakdown, U. S. revenue (which is entirely e-commerce) is decelerating sharply, falling 30% YoY to $3.2M. While management previously claimed e-commerce was 'strategic' for future U. S. entry, the data suggests it is simply dying.

🔴 𝐑𝐞𝐦𝐞𝐱𝐢𝐚𝐧 𝐃𝐫𝐢𝐯𝐞𝐬 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞, 𝐃𝐢𝐥𝐮𝐭𝐞𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 [NEW]

The acquisition of Remexian artificially inflated High Tide's growth metrics. While it added $31.6M in quarterly revenue, it generated a paltry $372k in operating income. This 1.2% operating margin severely dilutes the consolidated margin profile and highlights the risk of aggressively buying low-quality wholesale revenue to maintain the illusion of high growth.

🟢 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 𝐢𝐧 𝐂𝐚𝐧𝐚𝐝𝐢𝐚𝐧 𝐑𝐞𝐭𝐚𝐢𝐥

The standout positive is the organic retail business. Bricks-and-Mortar operating income accelerated by over 500% YoY, reaching $5.7M. The company has successfully absorbed the SSSg slowdown by controlling costs and pushing higher-margin White Label products (Queen of Bud, Cabana Cannabis Co.) through its 221-store network.

🟢 𝐃𝐢𝐬𝐜𝐢𝐩𝐥𝐢𝐧𝐞𝐝 𝐒𝐭𝐨𝐫𝐞 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐂𝐨𝐧𝐭𝐢𝐧𝐮𝐞𝐬

High Tide grew its Canadian retail footprint to 221 locations, maintaining its status as Canada's largest cannabis retail chain. The strategic pace of self-funded, organic store growth limits the need for expensive M&A in the saturated Canadian market. They expect to hit 228 stores shortly after closing pending acquisitions.

🟢 𝐂𝐚𝐛𝐚𝐧𝐚 𝐂𝐥𝐮𝐛 𝐄𝐜𝐨𝐬𝐲𝐬𝐭𝐞𝐦 𝐚𝐧𝐝 𝐃𝐚𝐭𝐚 𝐀𝐧𝐚𝐥𝐲𝐭𝐢𝐜𝐬

The discount club model continues to be the primary engine for SSSg outperformance versus peers. High Tide effectively uses its scale to extract high-margin data analytics and advertising revenue from licensed producers, offsetting the intense price compression seen in physical retail.

⚪ 𝐁𝐚𝐥𝐥𝐨𝐨𝐧𝐢𝐧𝐠 𝐃𝐞𝐫𝐢𝐯𝐚𝐭𝐢𝐯𝐞 𝐋𝐢𝐚𝐛𝐢𝐥𝐢𝐭𝐲 [NEW]

The structure of the Remexian acquisition has created a massive balance sheet risk. High Tide issued a put option for the remaining 49% of Remexian tied to a 3.64x EBITDA multiple. The liability for this option climbed to $57.9M this quarter, forcing the company to record a $1.67M non-cash fair value loss. This creates unpredictable earnings volatility going forward.

⚪ 𝐆𝐞𝐫𝐦𝐚𝐧 𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐑𝐢𝐬𝐤 𝐁𝐮𝐢𝐥𝐭 𝐈𝐧𝐭𝐨 𝐃𝐞𝐚𝐥 𝐒𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞

Management explicitly acknowledges the regulatory risk in the German 'MedCanG' laws. High Tide holds a $1.3M contingent contract asset that protects them if German regulations change and Remexian's EBITDA drops by more than 30%. This highlights the precarious nature of the European regulatory environment.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 (𝟔 𝐌𝐨𝐧𝐭𝐡𝐬): $10.3 million

Accelerating from $8.9M in the prior year. High Tide's ability to generate structural cash flow from operations allows it to self-fund its ambitious 20-30 store annual expansion target without diluting shareholders heavily.

𝐈𝐧𝐭𝐞𝐫𝐞𝐬𝐭-𝐁𝐞𝐚𝐫𝐢𝐧𝐠 𝐃𝐞𝐛𝐭 𝐯𝐬 𝐂𝐚𝐬𝐡: Debt: $38.6M | Cash: $36.5M

Stable. The company maintains a healthy liquidity position. Following the quarter's end, they secured a $40M credit facility with BMO at standard commercial rates, which will replace the expensive ConnectFirst credit union loan and free up $7.5M in restricted cash.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐂𝐚𝐥𝐞𝐧𝐝𝐚𝐫 𝟐𝟎𝟐𝟔 𝐒𝐭𝐨𝐫𝐞 𝐎𝐩𝐞𝐧𝐢𝐧𝐠𝐬: 20 - 30 new locations

Stable. The company reiterated its target to open 20-30 locations this calendar year, focusing primarily on organic growth rather than M&A.

𝐋𝐨𝐧𝐠-𝐓𝐞𝐫𝐦 𝐒𝐭𝐨𝐫𝐞 𝐓𝐚𝐫𝐠𝐞𝐭: 350 locations

Stable. High Tide aims to expand significantly from its current 221-store footprint, indicating confidence in capturing further market share as weaker independent operators exit the Canadian market.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐄-𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐌𝐞𝐫𝐠𝐞𝐫 𝐓𝐫𝐚𝐧𝐬𝐩𝐚𝐫𝐞𝐧𝐜𝐲

You merged the e-commerce segment into Bricks-and-Mortar this quarter, citing resource allocation. Given the 30% drop in U. S. revenues, isn't this masking the structural failure of your e-commerce roll-out strategy?

𝐑𝐞𝐦𝐞𝐱𝐢𝐚𝐧 𝐌𝐚𝐫𝐠𝐢𝐧 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲

Remexian added nearly $32M in revenue but only $372k in operating profit. Is a 1.2% operating margin the normalized expectation for the Medical Cannabis Distribution segment, or are there specific synergies that will expand this margin over the next 12 months?

𝐏𝐮𝐭 𝐎𝐩𝐭𝐢𝐨𝐧 𝐋𝐢𝐚𝐛𝐢𝐥𝐢𝐭𝐲

The put option liability for the remaining 49% of Remexian has ballooned to $57.9M. At 3.64x trailing EBITDA, how are you preparing the balance sheet to absorb this potential cash outlay when the option becomes exercisable in September 2027?

1

630

$hiti $msos High Tide CG note is out!

• This morning, High Tide reported distributing 7.6 tonnes of medical cannabis through Remexian Pharma GmbH in Q2/F26, marking growth of 21% QoQ and 49% YoY. This performance reinforces HITI’s thesis for Remexian, which is to leverage its European distribution platform alongside established relationships with Canadian licensed producers to facilitate exports into Germany’s rapidly expanding medical cannabis market. In 2025, Germany imported 201.1 tonnes of medical Cannabis, more than doubling from 72.9 tonnes in the prior year, with Canada accounting for nearly half of total imports at over 93 tonnes. Against this backdrop, HITI’s growing distribution volumes suggest it is gaining traction within a structurally expanding and import-dependent market, in our view.

• Also of note, yesterday High Tide announced it has signed a term sheet for $40 million of new credit facilities, structured in two tranches: 1) a $25 million committed revolving facility intended to refinance the company’s existing connectFirst facility (at Prime 2.5%), which currently has just over $6 million drawn, implying approximately $19 million of incremental liquidity; 2) a $15 million committed delayed-draw term loan to refinance HITI’s existing $15 million second-lien

debentures (at 12% coupon rate), with a seven-year amortization period upon draw. Closing is expected within the next 60 days, subject to customary conditions precedent.

• The new facilities carry an interest rate of Prime 2% to Prime 3%, which we view as attractive given the improved capital structure and reduced reliance on higher-cost subordinated debt. According to our rough estimate, HITI can save ~$1 million of cash interest expense per year upon retiring the second-lien debentures.

3

19

1,174

#NowStreaming 🖥️🎧🎙️

America's First Corps CSM Shawn Carns talks readiness and resilience with R2's Callie Webster on the newest episode of #ConnectFirst "With The People" podcast.

Find the full episode on your favorite streaming service 👉 linktr.ee/icorps

ALT America's First Corps CSM Shawn Carns talks readiness and resilience with R2's Callie Webster on the newest episode of #ConnectFirst "With The People" podcast.

5

8

37

1,271

13 Jun 2024

12% interest bearing and 10% discount on debentures (5 year maturity) is ~14% cost of debt per annum.

Compared to ConnectFirst 9.7% (prime 2.5%) before rate hikes.

These are fine terms given that the bank rate is up 4.25% since we locked that in.

Good job team $HITI

13 Jun 2024

High Tide Executes Binding Subscription Agreements for $15 Million in Subordinated Debt $HITI prnewswire.com/news-releases…

1

2

11

640

30 May 2024

GIVEAWAY ALERT! Our presenting sponsor connectFirst Credit Union is giving away a pair of Discovery Passes to two lucky winners!

To enter, follow @ConnectFirstCU and @sledisland, and tag a friend! (Unlimited tags allowed).

Contest closes on Wednesday, June 5 at midnight. 18 .

ALT A connectFirst staff member is posing for the camera in front of a dart board at the #1 Royal Canadian Legion. There is a table in front of her that reads "DeLorean Lounge by connectFirst Credit Union"

2

299

13 May 2024

We are pleased to announce the new Executive Leadership Team that will lead our newly merged organization. Comprised of executives from both connectFirst and Servus, this powerhouse team is well suited to shape the credit union of tomorrow for Albertans. ow.ly/BxcH50REHJ6

1

2

733

8 May 2024

(1/6)

Hi @zcectsn. We’re sincerely sorry for the less than satisfactory experience you’ve had with Hong Leong ConnectFirst. We’re constantly learning & making improvements.

2

200

7 May 2024

Hong Leong customers cannot have access to their accounts online! @BNM_official: You had been informed about the complaints re: the failed ConnectFirst and BNM chose not to do anything about it!! The little napoleons are sleeping on the job in BNM! All is not well in BNM!

7 May 2024

Unseen before, online banking apps down is the norm. Its none other than @MYHongLeong’s ConnectFirst. How could @BNM_official allow a failed online banking apps to be launched and caused great inconveniences to its customers. When will Bank Negara take a serious action against Hong Leong to stop its Hong Leong’s substandard ConnectFirst! @MOFmalaysia #ConnectFirst #CoonectLast

2

5

4

1,872

7 May 2024

Hi @mrkenneth811. Thank you for reaching out to us, and we sincerely apologize for the inconveniences you experienced with Hong Leong ConnectFirst.

1

201

5 May 2024

"Servus and connectFirst credit unions merged on May 1 making it the largest merger in Canadian credit union history."

#ableg #abpoli

reddeeradvocate.com/local-ne…

2

137

1 May 2024

connectFirst is thrilled to announce that our merger with @servuscu is now closed!

Thank you for helping us reach this truly historic milestone which will create one of the largest and strongest credit unions in the country! Stay tuned for updates!

greatertogether.info/

2

2

707

10 Apr 2024

Huge congrats to MRU HPED and adapted physical activity student Emma Ghiultu, founder of 'Adapted' (adapted fishing rods), who took home the $10,000 connectFirst Credit Union Social Impact Award at the 2024 JMH LaunchPad Pitch Competition last week!

3

176

14 Mar 2024

Just had a workshop led be @melaniekatzman with #ObamaLeadershipNetwork members. Main takeawys : learn names of your colleague, see them and call their name ... #ConnectFirst

1

51

31 Jan 2024

@MYHongLeong ConnectFirst online is having its very periodical down time since 2 pm until now. No transaction can be done for so many hours. How could @BNM_official allow such sub-standard online app to be launched?

3

2

4

405

REMINDER: Parenting can be both a joy and a challenge. As an expectant mother, learn how you can navigate postpartum wellness. Join us, @TulsaHealthDept and ConnectFirst, for this FREE event on Jan. 26. RSVP: bit.ly/3NWYH3T #parenting #fcsok #mentalhealthandmore #classes

2

36

#NowStreaming 🎙️

I Corps CSM Shawn Carns talks about the importance of holistic health & how to implement it into every day life on the newest episode of #ConnectFirst podcast

🎧Listen at our link in bio or wherever you get your podcasts

4

18

644

7 Dec 2023

Leading with Heart: The Key to Inspiring Others

#LeadershipHeart #ConnectFirst #InspireWithEmpathy #AbundanceOfInspiration #SelfEsteemInLeadership

2

26

#NowStreaming 🖥️🎧🎙️

Our CSM Shawn Carns talks with the members of I Corps #BestSquad, about what being a part of a cohesive team means to them & how to remain resilient on the newest episode of #ConnectFirst podcast

linktr.ee/icorps

@USArmy @USARPAC @JBLM_PAO @7thID

2

4

470

⬛️ Building Trust

🔸Trust is fragile and can easily be undermined by a wrong word, sentence or action. It is a product of expressed intent and is built over time on a basis of repeated interactions.

👉"Before people decide what they think of your message, they decide what they think of you."

#leadership #trust #empathy #people #connectfirst

🔸Thanks @tnvora for your always great infographics and food for thought 💛

3

2

14

929