Jun 10

$MO Altria continues to have a good 2026 up 26% and remember they still own 8% of $BUD which also doing better. When this whole #AI pops #tobacco is what you want to own It was when dot-com crashed in 2000 and a good divi. #consumerdefensive #consumerstaples

1

251

Jun 9

$SJM leads the gains with a 10.1% rise, $HD surges 3.93%, $COST sees a significant increase, and $PAYO benefits as well.

Bullish rationale: With inflation expectations easing and consumer confidence rebounding, demand for consumer staples remains stable, and major retailers and food giants are demonstrating strong earnings resilience.

Conclusion Market Sentiment (Highlight): Defense is the best offense! $SJM and $HD have demonstrated their dominance amid market volatility, with substantial capital flowing back into the consumer defensive sector.

#SJM #HD #ConsumerDefensive #RetailStocks #JMSmucker #HomeDepot #DefensivePlay

113

Feb 4

Chart of the Day – $KR 🛒📈

Grocery stores could be in position for a catch-up move as we continue to see strength across consumer defensives. $XLP is having a monster year, and I’m now looking for industries within the sector that haven’t fully participated yet.

From a technical standpoint:

$KR has been trading under a 6-month descending trend

Price is now pressing into a key decision zone

The near-term setup favors watching for red-to-green action out of the gate

Ideal price action:

Pullbacks that hold prior day’s range

Reclaims of the Feb 2 resistance area

A daily close above $65 would confirm the breakout and signal trend change

This isn’t about chasing strength. It’s about rotation and confirmation as money continues to flow into defensives.

Watching closely for follow-through. 👀📈

@TradeThePool

#KR #ConsumerDefensive #Grocery #ChartOfTheDay

1

1

4

543

Feb 2

Chart of the Day – $PEP 🥤📈 by @TradeThePool

An over 2.5-year descending trendline is now coming into play for PepsiCo. Price has spent an extended period consolidating, and the chart is approaching a technical inflection point that deserves attention.

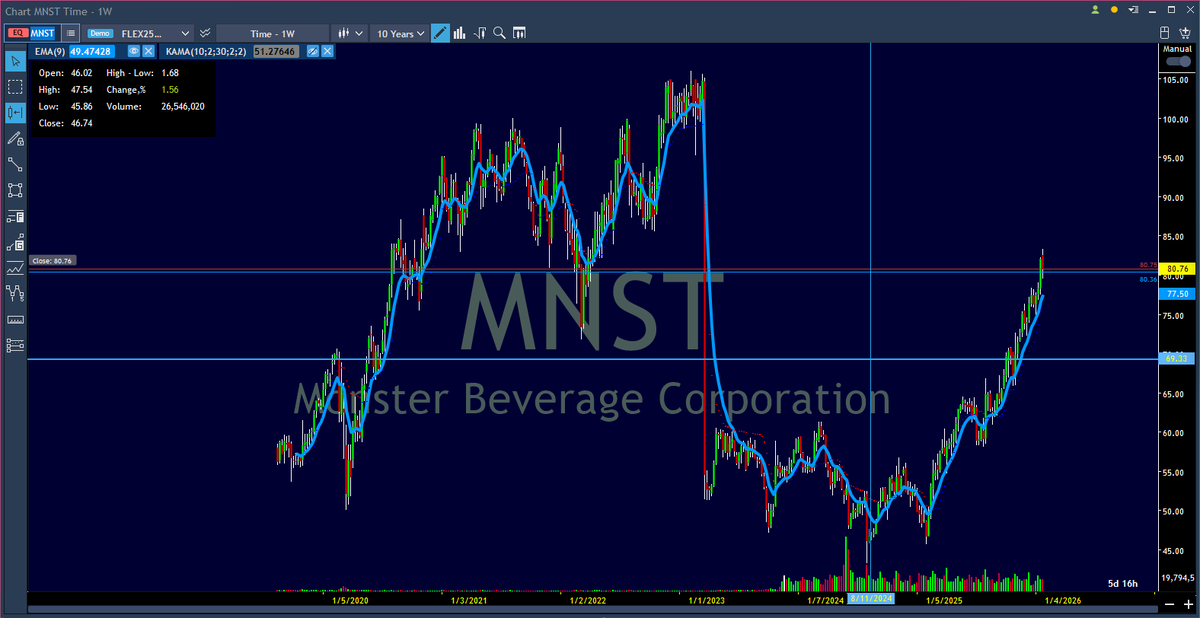

We’re starting to see strength in consumer defensive names, with the soft drink space already catching a bid in $MNST and $KO. If the broader market continues to rotate from growth toward value and defensives, this group could remain in favor.

From a positioning standpoint, I’m watching for lower-PE, steady cash-flow names to benefit from that shift. A resolution through this trendline would open the door for continuation, while support remains well-defined below.

Not a momentum chase. A rotation setup. 👀📉➡️📈

#PEP #ConsumerDefensive #ValueRotation #ChartOfTheDay

1

1

8

1,342

Entender el contexto global de los mercados a través de los ciclos, te ayuda a focalizar la búsqueda de oportunidades en inversión en compañías en sectores líderes. #energy #basicmaterials #consumerdefensive

4

561

6 Dec 2025

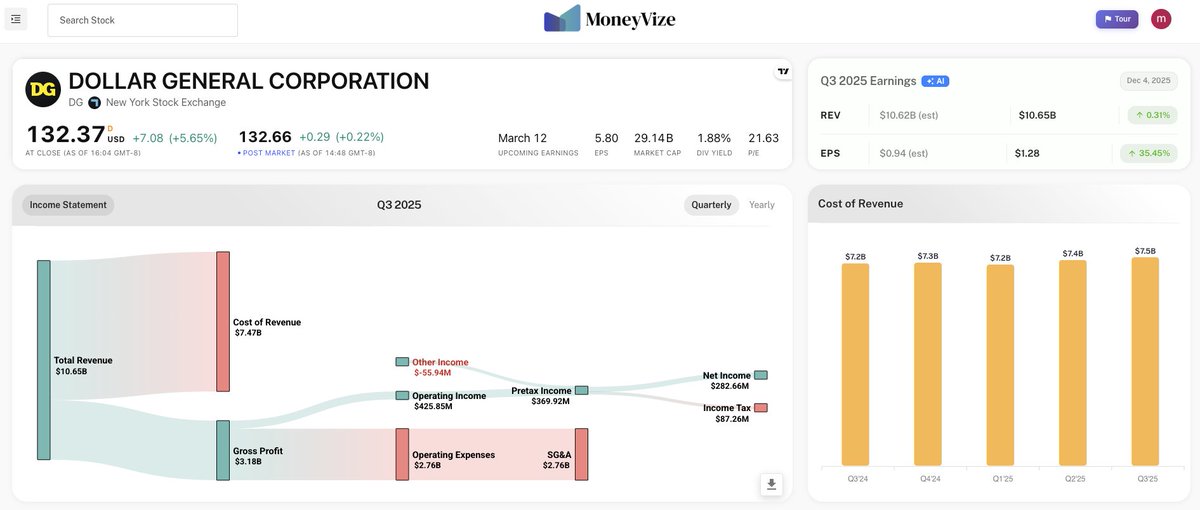

$DG Q3'25 Earnings Report from Moneyvize.com.

Dollar General reported strong Q3 results with increases in net sales, same-store sales, and earnings per share, driven by a focus on value and convenience.

The company is expanding its store footprint and investing in digital initiatives.

While facing some cost pressures, the company provided positive guidance for the year, including strong performance during the holiday season.

The company is confident about its long-term financial framework.

Stock is up 75% YTD.

Login to Moneyvize.com — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#DG #DollarGeneral #DiscountStores #DiscountRetailer #ConsumerDefensive #ConsumerEconomy #AIPowered #Moneyvize #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Earnings #earningswithmoneyvize

Not investment advice.

1

4

38

3 Dec 2025

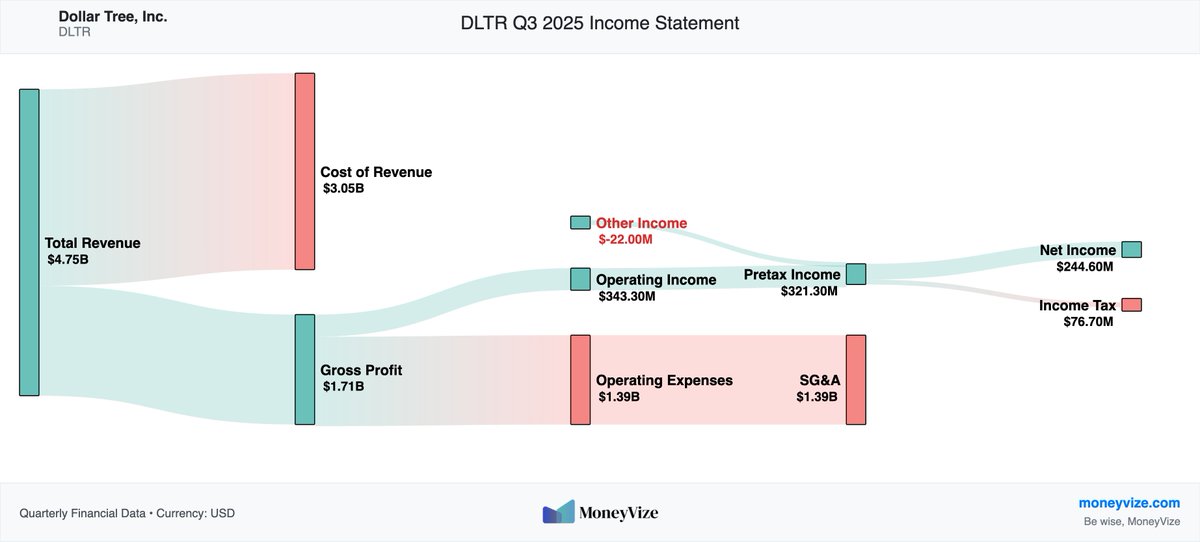

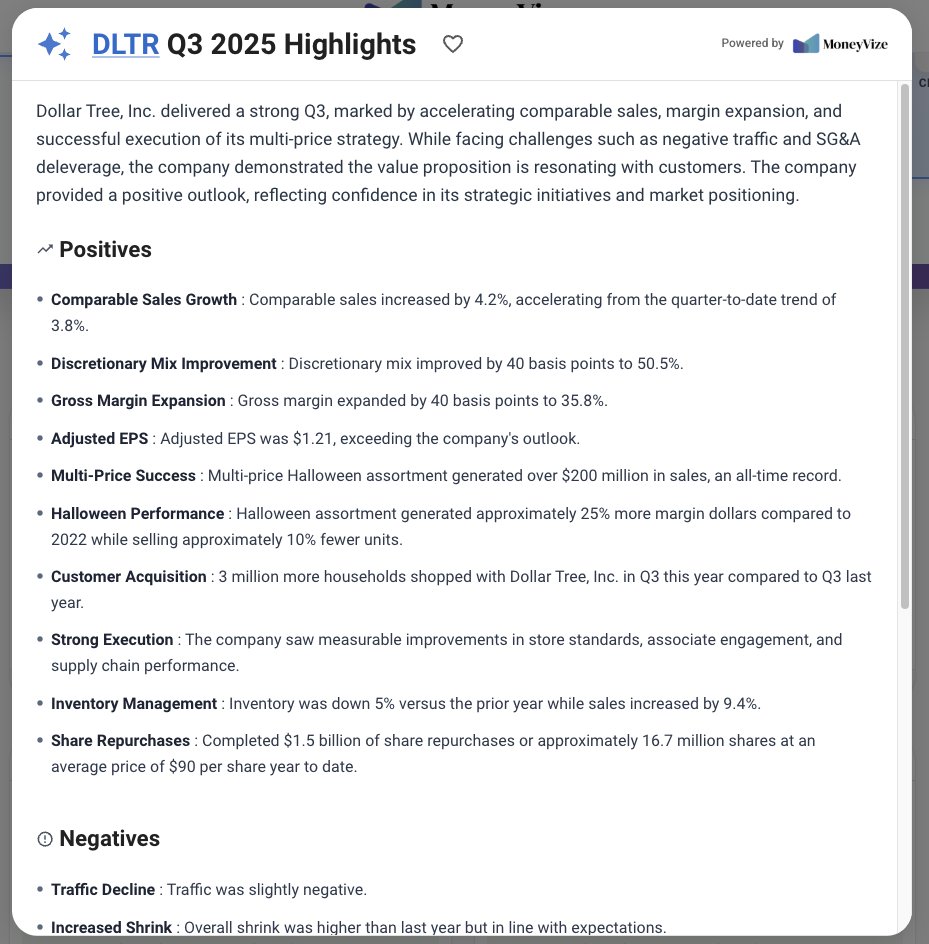

$DLTR Q3'25 Earnings Report from Moneyvize.com.

#Dollar Tree, Inc. delivered a strong Q3, marked by accelerating comparable sales, margin expansion, and successful execution of its multi-price strategy.

While facing challenges such as negative traffic and SG&A deleverage, the company demonstrated the value proposition is resonating with customers.

The company provided a positive outlook, reflecting confidence in its strategic initiatives and market positioning.

Login to Moneyvize.com — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#DLTR #DollarTree #DiscountStores #ConsumerDefensive #Household #PersonalCare #AIPowered #Moneyvize #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Earnings #earningswithmoneyvize

Not investment advice.

1

4

40

30 Nov 2025

Kraft Heinz: A Classic Value Trap Disguised as a Dividend Play $KHC #stocks #investing #valueinvesting #Value #ConsumerDefensive #US #Bear #WarrenBuffett gurufocus.com/news/3226493

2

720

20 Nov 2025

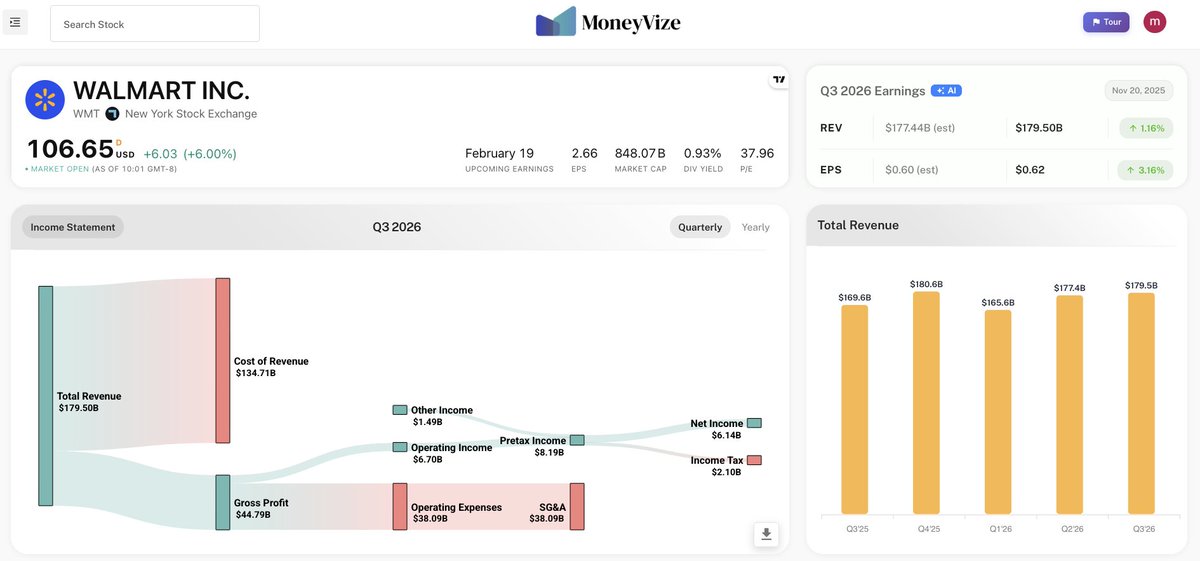

$WMT Walmart Q3'26 Earnings Report from Moneyvize.com.

Walmart #WMT dropped in pre-market, but investors quickly reversed course — the stock is now up ~6% on one of the ugliest macro days of the month.

That alone tells you how strong this Q3’26 report was. Revenue came in at $179.5B, beating expectations, with EPS at $0.62, also ahead of estimates. Growth was broad and clean: e-commerce surged 27%,

Walmart U.S. comps 4.5%, International 11.4%, and global advertising revenue jumped 53%. Management boosted full-year sales and operating income guidance, signaling confidence heading into holiday. Consumer behavior continues tilting toward essentials, value, and omnichannel convenience — exactly the categories where Walmart is gaining share.

What makes today notable is that Walmart is green while the broader market is getting rug-pulled after a hotter jobs report sparked fear of delayed Fed cuts.

Most retailers sank, but WMT broke away from the pack — a classic “flight to safety reward good earnings” move.

Yes, there were a few pressure points like inventory up 3%, some general merchandise softness and a $700M PhonePe charge, but none of it fazed investors. The market is clearly rewarding Walmart’s operating leverage story, its e-commerce momentum, and the long-term margin tailwind from advertising and AI-driven operational efficiencies.

Today’s reaction reinforces a clear takeaway: Walmart is becoming the market’s preferred consumer staple tech-enabled retailer hybrid. Strong results on a bad macro day show elevated investor conviction.

Heading into the holidays, watch merchandise mix normalization, traffic vs. basket trends, and how efficiently Walmart manages elevated inventory levels — but for now, the Street is giving this print a big thumbs up.

Login to Moneyvize.com — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#WMT #Walmart #Retail #eCommerce #consumerdefensive #SamsClub #PhonePe #Flipkart #AIPowered #Moneyvize #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Earnings #earningswithmoneyvize #ConsumerSpending #HolidaySeason

Not investment advice.

2

4

53

7 Nov 2025

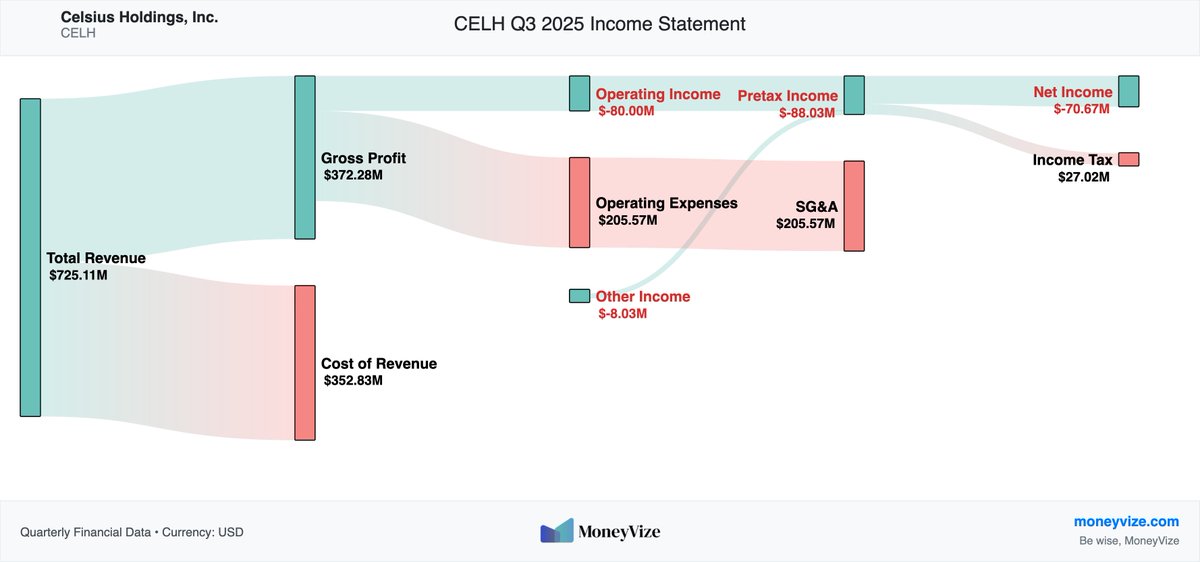

$CELH Q3'25 Earnings Report from Moneyvize.com

#Celsius Holdings posted a monster topline: $725.1M in revenue (up ~173% YoY) driven largely by the rapid scale-up from acquisitions (Alani Nu, Rockstar) and the expanded PepsiCo distribution partnership — plus strong underlying Celsius and Alani Nu retail growth, which together pushed U.S. market share and shelf penetration materially higher.

The quarter also showed better gross margins (51.3%) and impressive operating cash metrics that reflect the company’s rapid consolidation of acquired brands.

So why the ~25% plunge?

A few big reasons:

1. Huge one-time/transition costs tied to moving Alani Nu into the Pepsi system and distributor terminations were disclosed (reported distributor termination/transfer costs were very large even if PepsiCo agreed to fund much of the cash impact), which made Q4 visibility messy and produced a headline net loss and EPS softness versus what momentum investors wanted to see.

2. Management warned of a “noisy Q4” — promotions, integration freight/tariff pressure and timing effects that could compress margins near term and push incremental costs into the fourth quarter and early 2026.

3. The stock had already run a long way (big multiple expansion) into the print, so the combination of one-offs guidance noise triggered sell-the-news profit-taking and re-rating by traders and some analysts. Analysts and writeups also flagged heightened risk from heavy reliance on M&A to drive revenue (acquisition dependence = execution risk).

Valuation context (important for understanding the reaction): CELH’s forward P/E trades roughly in the ~$40 - $45 range and forward P/S in the ~$7.5 – $8.6 range (differences reflect varying model horizons and consensus estimates) v/s. Industry Avg. of ~$16 forward P/E and ~2.4 forward P/S — meaning the market has already priced in high growth into the stock, so a hint of short-term margin or integration risk prompted a sharp pullback.

The quarter validates Celsius’s scale strategy — massive revenue acceleration, PepsiCo distribution upside, and improved margins — but the market punished the stock because the quarter also exposed material short-term execution and timing risks (big distributor transition costs, Q4 noise) and left forward visibility lumpier than growth investors wanted. If management can execute the Pepsi / Alani / Rockstar integrations and deliver the expected synergies in 1H-2026, the long-term thesis still stands — but the near term will likely be volatile.

Login to Moneyvize.com — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#CELH #AlaniNu #Rockstar #PepsiCo #Beverages #ConsumerDefensive #AIPowered #Moneyvize #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Shutdown #Earnings #earningswithmoneyvize #jobmarket

Not investment advice.

1

5

436

4 Nov 2025

Currently, $LAUR is demonstrating solid momentum with a score of 78, suggesting positive price action in recent trading. Coupled with a high valuation score of 90, it's clear that the market perceives the stock as undervalued relative to its earnings, which stand at a PE of 21.50.

The 52-week range indicates that $LAUR is trading in a consolidated manner, reflecting stability in the consumer defensive sector. With a low beta of 0.7, it remains less volatile compared to the broader market, making it an interesting watch for those seeking stability.

Investors may find $LAUR's current standing as a solid hold amid shifting sentiment.

#ConsumerDefensive #Equities #InvestingInsights #LAUR

2

70

27 Oct 2025

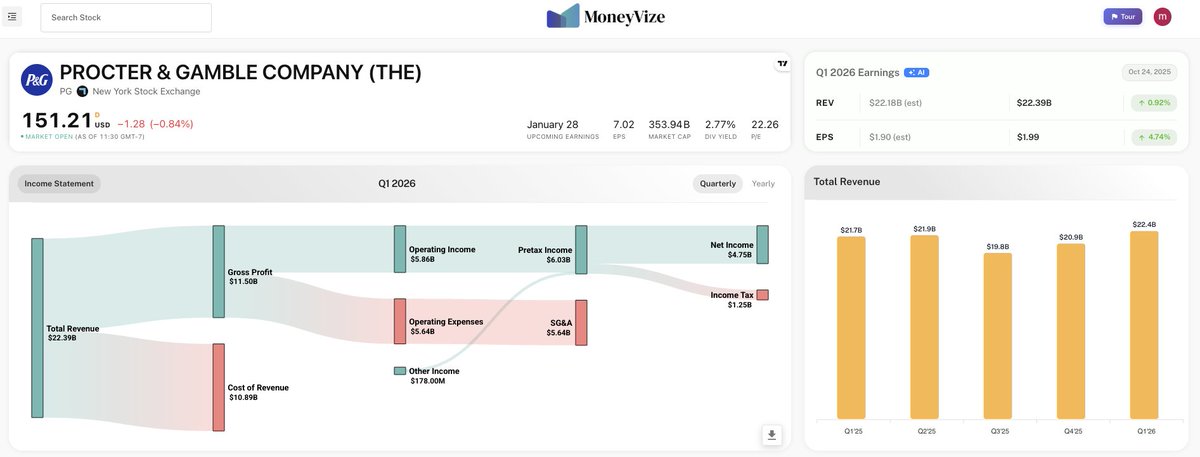

$PG Procter & Gamble Q1'26 Earnings Report from Moneyvize.com.

P&G delivered a solid start to fiscal 2026, with organic sales and core EPS growth, despite facing a challenging geopolitical, competitive and consumer environment. The company is actively managing its portfolio, investing in innovation, and executing a restructuring program to drive future growth.

While market share declined slightly and competitive pressures exist, especially in North America and Europe, the company's focus on integrated superiority, productivity improvements and strategic initiatives in key regions like China and Latin America positions it for sustained value creation.

Guidance for the year remains positive, with a focus on delivering balanced top and bottom line growth and returning value to shareholders, although the company is seeing a deceleration in North American consumption.

Login to Moneyvize.com — where you can compare key financials, evaluate forward guidance, spot emerging trends and understand overall business performance in one intuitive dashboard. Make sense of earnings — and invest smarter.

#PG #ConsumerDefensive #ConsumerGoods #HomeCare #Beauty #PersonalCareProducts #AIPowered #StocksinFocus #tariffs #inflation #ratecut #EarningsReport #EarningsSeason #Shutdown

Not investment advice.

1

2

99

25 Sep 2025

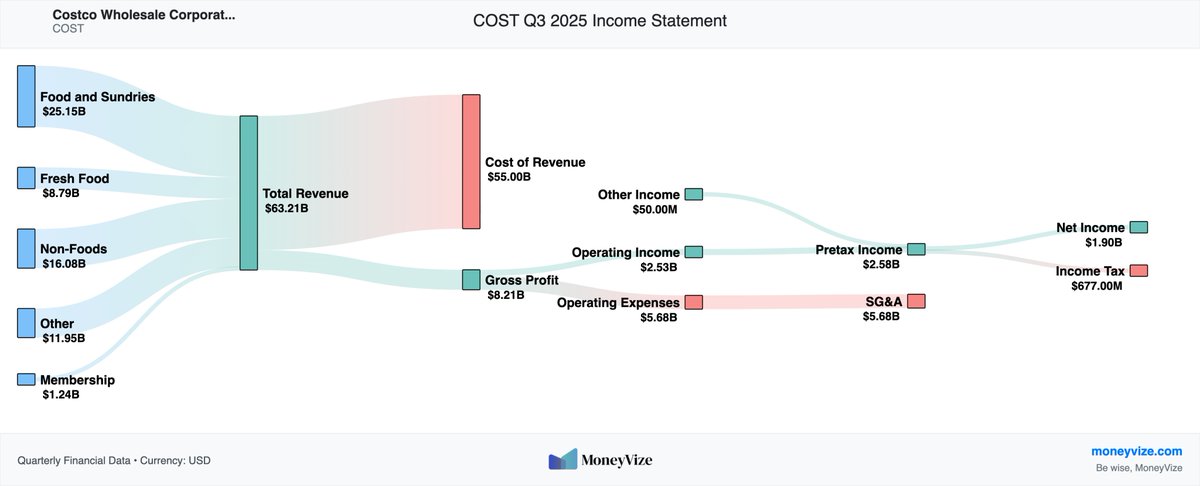

$COST Q4 & FY'25 Pre-Earnings Analysis from Moneyvize.com.

#Costco is set to report fiscal Q4 and FY 2025 results after the close today. Wall Street is expecting earnings of about $5.80–$5.82 per share on $86.0–86.3 billion in revenue, which would mark roughly 8% year-over-year growth.

The backdrop is interesting: the Fed just cut rates by 25 bps last week (to 4.00–4.25%), inflation has cooled but is still running around 2.9% YoY, and consumers remain cautious but resilient. Costco has been navigating tariffs, LIFO charges and FX headwinds while still growing comps, memberships, and e-commerce.

Last quarter, they posted strong comp sales ( 5.7% headline, 8% adjusted) and solid membership fee growth, but management warned of an additional $40–$50M LIFO charge hitting Q4 if inflation trends held.

Key things to watch this time:

1. Same-store sales momentum,

2. Renewal rates - now including members who first joined through Costco’s Groupon promotion in fall 2023 and those sign-ups tend to renew at lower levels than typical members.

3. Gross margin pressure from tariffs/LIFO, and

4. Updates on digital growth, Capex, and the rollout of new Executive-member perks (like early access hours).

Given Costco’s premium valuation, even small misses on comps or margin commentary could move the stock sharply, while a clean beat and signs of margin stabilization would likely be rewarded.

Will #COST meet or exceed the guidance? Stay tuned for more! Analyze the business, Login Now!

#Costco #Consumerdefensive #AI #Moneyvize #Aipowered #Earnings #EarningsReport #StocksinFocus #Inflation #Investing #StockMarket #RateCut

Not investment advice.

1

4

412

29 Aug 2025

Sector Performance - End of Day

#Data #Stocks #economy #USA #ConsumerDefensive #HealthCare #Energy #RealEstate #Financials #Materials #CommunicationServices #InformationTechnology #Industrials #ConsumerCyclical #Utilities

2

27

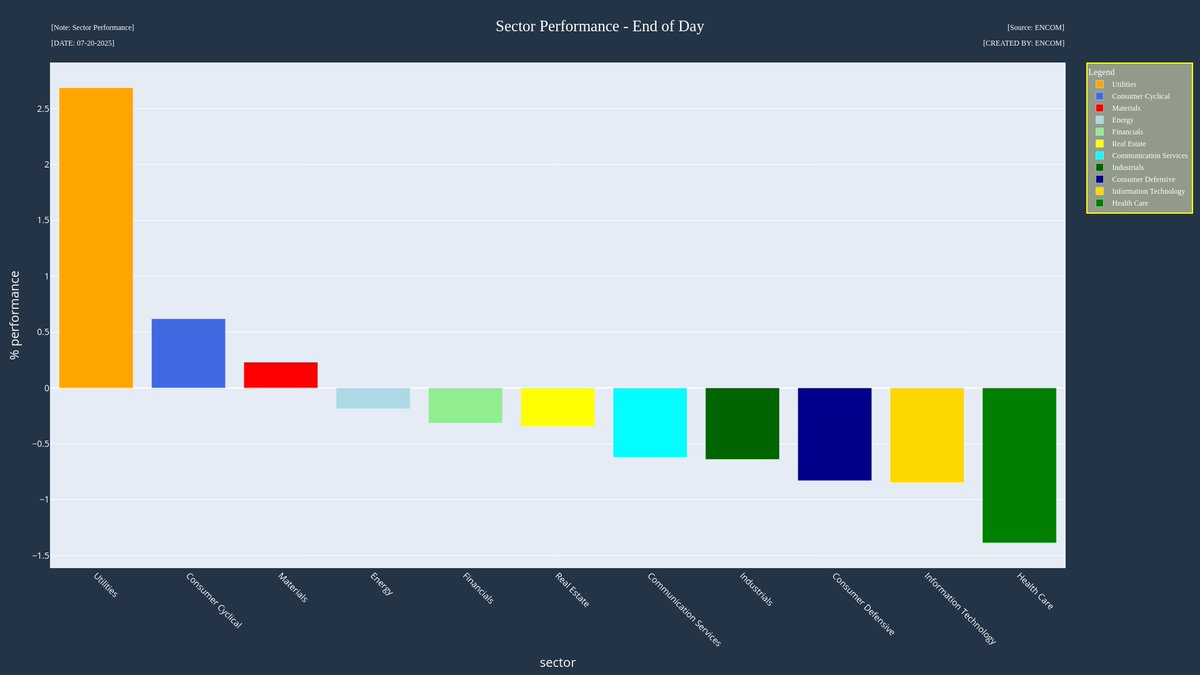

20 Jul 2025

Sector Performance - End of Day

#Data #Stocks #economy #USA #Utilities #ConsumerCyclical #Materials #Energy #Financials #RealEstate #CommunicationServices #Industrials #ConsumerDefensive #InformationTechnology #HealthCare

1

27

2 Jul 2025

Please Check Out 👀 the New #BeachBumTrading #YouTube #Video 🎥 "CELH | Celsius | Quick Take" 👉 youtu.be/5yzei2uUOXw

$CELH #Celsius #Stock #CELH #Trader #Trading #Traders #DueDiligence #ConsumerDefensive #Beverages #Drinks #Beverage #Drink #Consumer #Defensive #Stocks #DD

3

4

190

30 Jun 2025

$DG is a classic defensive play in uncertain times. Pricing power rural dominance = stable bullish case.

#Retail #ConsumerDefensive #DG

2

59

10 Jun 2025

Please Check Out 👀 the New #BeachBumTrading #YouTube #Video 🎥 "Selling Puts on LW | Lamb Weston | Quick Take" 👉 youtu.be/6FHjW53cS88

$LW #LambWeston #Stock #LW #Trader #Trading #Traders #DueDiligence #ConsumerDefensive #PackagedFoods #Consumer #Defensive #Food #Stocks #DD

3

4

153

8 Jun 2025

PepsiCo Inc: A Quiet Giant with More Firepower Than the Market Thinks $PEP ko ul #stocks #investing #valueinvesting #Value #ConsumerDefensive #inflation #US #Growth gurufocus.com/news/2906673

1

7

1,277

23 May 2025

Please Check Out 👀 the New #BeachBumTrading #YouTube #Video 🎥 "LWAY | Lifeway Foods, Inc. | Quick Take" 👉 youtu.be/dGNA3QB4sBY

$LWAY #LifewayFoods #Stock #LWAY #Trader #Trading #Traders #DueDiligence #ConsumerDefensive #PackagedFoods #Consumer #Defensive #Food #Stocks #DD

3

7

143