Jun 11

Gracias Novo Nordisk Mexico 🇲🇽

A great pleasure being the opening speaker at your “Bossa Novo” Leadership in Action offsite, with the more than 200 NN MX leaders reunited.

We opened with my keynote “The Consumer-centric Leader” and moderated an amazing panel discussion where we covered best practices and use cases in consumer-centricity with:

- Caio Brabo da Silva, LATAM Injectables Marketing Manager at Galderma

- Victor Vendramini, Head of Digital, Ecommerce, Omnichannel, and Marketing LATAM at Nestlé Health Science

- Arturo Gutiérrez, Cardiometabolic Marketing Director at Novo Nordisk

A special thanks goes to the amazing team that made this happen: Ximena Resendiz, Gloria Behrens, Adriana Orozco Mejía, Fernando Pulido, Alberto Retana, Patricia Field!

Keep pushing NN’s consumerization efforts!

#novonordisk #keynote #ai

44

Jun 9

The whole point is that what is happening to glp1 pricing is unprecedented in medicine. Net and realized prices are falling 50-70pct without any generic pressure. Purely due to commoditisation and consumerization of incremental demand. Ur missing the point

1

27

the consumerization and pornographization of Lestat mpreg.

og goth was, like, marilyn manson and 80s proto-niner runoff. I don't think we're being serious here

3

159

May 27

Consumerization of GLP-1 class at full throttle

May 27

5

1,016

AI ADOPTION DOESN’T SCALE THROUGH MODELS ALONE — IT SCALES THROUGH ACCESSIBILITY

One of the biggest hidden barriers in AI today is not capability.

It is usability.

Payment friction.

Regional restrictions.

Fragmented platforms.

Complicated onboarding.

Most users do not stop using AI because the models are weak.

They stop because access still feels unnecessarily difficult.

That is why the latest update from AINFT matters.

📢 AINFT now supports WeChat Pay & Alipay.

This is a much bigger step than simply adding new payment methods.

It is about reducing friction between users and AI itself.

1️⃣ PAYMENT ACCESSIBILITY IS PART OF AI INFRASTRUCTURE

As AI ecosystems expand globally, payment flexibility becomes increasingly important.

Because infrastructure adoption accelerates when users can:

➜ onboard instantly

➜ pay through familiar systems

➜ avoid complicated setup

➜ access models without technical barriers

By integrating:

➜ WeChat Pay

➜ Alipay

AINFT significantly lowers the accessibility threshold for mainstream AI usage.

This is especially important across regions where mobile-first payment systems dominate daily digital behavior.

2️⃣ THE REAL VALUE IS THE UNIFIED AI ACCESS LAYER

AINFT is not just offering individual models.

It is building a unified AI gateway.

Users can now seamlessly access:

➜ GPT

➜ Claude

➜ Gemini

➜ leading Chinese frontier models

➜ AI Agent services

…through a single platform experience.

This matters because the future AI economy may not revolve around:

“which single model wins.”

Instead, it may revolve around:

➜ orchestration

➜ routing

➜ unified access

➜ workflow coordination

➜ seamless execution infrastructure

The aggregation layer itself becomes strategically valuable.

3️⃣ AI IS ENTERING ITS “CONSUMERIZATION” PHASE

Early AI adoption focused heavily on:

➜ developers

➜ APIs

➜ technical users

➜ enterprise experimentation

The next phase increasingly focuses on:

➜ mainstream accessibility

➜ frictionless onboarding

➜ consumer usability

➜ payment convenience

➜ unified experiences

This is how technologies move from:

“specialized tools”

→ into

“mass-market infrastructure.”

And payment simplicity plays a much larger role in adoption than many people realize.

4️⃣ THE AI CRYPTO INFRASTRUCTURE CONVERGENCE IS BECOMING CLEARER

Platforms like AINFT also reveal a larger industry trend:

AI infrastructure and financial infrastructure are starting to converge.

Future AI ecosystems will likely require:

➜ unified identity

➜ intelligent routing

➜ seamless payments

➜ autonomous execution

➜ multi-model orchestration

➜ low-friction settlement systems

The future user experience may feel simple on the surface.

But underneath, it will operate on increasingly sophisticated coordination layers.

5️⃣ THE BIGGER STORY: THE WINNING AI PLATFORMS MAY BE THE ONES THAT REMOVE THE MOST FRICTION

The next AI competition may not simply be about:

➜ parameter count

➜ benchmark scores

➜ raw reasoning capability

It may increasingly revolve around:

➜ accessibility

➜ ecosystem integration

➜ payment simplicity

➜ workflow coordination

➜ user retention

Because the easier AI becomes to access, the faster adoption compounds.

And AINFT’s latest integration is another signal that AI infrastructure is steadily moving toward a more seamless, consumer-ready future.

@justinsuntron #TRONEcoStar

@AINFTcom

12

11

8,049

Ye banda chahta toh isko aise bhi frame kar sakta tha ki it's about civil rights, nutrition and things but he chose to call it praxis(a more serious word)

Proving once again that american leftists, streamers nd some anarchists r the victims of consumerization of protest/activism

1

1

11

238

May 12

The future is the consumerization of advertising

May 12

Proud to announce we are the official sponsor of Carson's parents' garage. Garage-based advertising is the future and we are excited to play a small part in it.

7

441

May 9

DeFi was never too complicated because people lacked intelligence.

It was too complicated because the experience was broken.

Most users don’t want to jump across multiple dApps, approve endless wallet permissions, calculate gas fees, or study validator mechanics just to stake ETH.

They just want a simple outcome:

“Put my ETH to work.”

That’s why the integration between @LidoFinance and @Ask_ORO feels like a major turning point for Ethereum staking.

For the first time, staking is becoming conversational.

Instead of navigating a complicated multi-step process, users can simply tell ORO:

“Stake my ETH.”

ORO handles the execution through Lido’s infrastructure while the user maintains ownership of their assets.

Simple. Fast. Accessible.

This changes the entire onboarding experience for DeFi.

Because the biggest barrier to adoption was never yield.

It was friction.

And ORO removes that friction completely.

What makes this integration even more powerful is that users receive stETH after staking through Lido.

That means your ETH stays liquid while still earning staking rewards.

You’re no longer forced to choose between staking and participating in DeFi.

You can do both.

And this isn’t built on untested infrastructure.

Lido Finance currently secures over $21.3B in TVL, making it one of the most trusted liquid staking protocols in the Ethereum ecosystem.

The real story here isn’t just staking.

It’s what this represents for the future of crypto products.

For years, DeFi platforms were designed for people who already understood crypto.

ORO changes that model by turning complex blockchain actions into natural conversations.

That shift matters more than most people realize.

Because once DeFi feels as simple as sending a message, adoption no longer depends on technical expertise.

It becomes accessible to everyone.

This is what the consumerization of DeFi looks like.

Not more dashboards. Not more complexity.

Just intent → execution.

And honestly, that may be the unlock that finally pushes DeFi into mainstream adoption.

@ZIGChain $ZIG

💧 @LidoFinance is now integrated on ORO.

You no longer need to know where to go, what to click, or how defi works.

Just tell ORO “Stake my ETH”.

Join the $21.3B already staked.

38

406

Apr 30

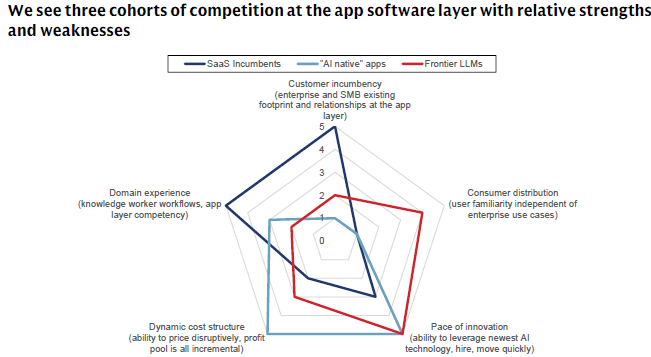

👀 Competitive framing of SaaS v AI Natives v Frontier Models

TBD right weighting of *consumer* familiarity

i.e. consumerization of enterprise IT would need to be remarkably strong... but ~plausible in a true epoch shift like AI

- via Goldman Sachs

1

4

655

Apr 26

This interview with $LLY CEO Dave Ricks gave great insights on capital allocation, drug development, and market dominance.

The obesity TAM is still misunderstood. Wall Street models price erosion as a direct hit to free cash flow. Ricks explicitly states this is wrong. Traditional drugs have zero volume elasticity. Obesity drugs act like a consumer product. Dropping the price from $1,000 to $350 doesn't kill margins. It triggers massive volume expansion in the cash channel. Plus, that lower price was basically the net price they were getting on diabetes drugs anyway after gross-to-net discounts. Price cuts does not necessarily mean margin compression. Price cuts can very well translate to TAM expansion. They are at roughly 20 million patients globally today and are pacing to 30 million this year. Ricks thinks peak penetration hits 20% to 40%, comparable to statins.

The competitive landscape is shifting and competitors are making a massive mistake. Ricks dropped critical info on why Lilly is not chasing a monthly dose if it ruins the pharmacokinetic curve. The secret to GLP-1s is a flat PK curve. If you inject a monthly drug, by day 30 you only have 20% of the active dose left. When you re-dose on day 1 of the next month, the patient gets hit with a massive spike. This forces the patient to restart the tolerability curve, sacrificing efficacy and causing gastrointestinal side effects every single month. Lilly refuses to do this. This is a direct shot at competitors like $NVO pushing monthly shots that sacrifice tolerability for convenience.

The pipeline is also incredible. The market is focused on Zepbound. Butt it is really just the start. Retatrutide, which is the triple G agonist, is causing patients to drop out of trials because they lose too much weight. It specifically targets and strips visceral fat out of the gut and liver. And then there is Amylin inhibitor, eloralintide. Ricks noted this pure asset drives nearly 20% weight loss with almost zero GI side effects. No titration into side effects needed. Meanwhile, Orforglipron, which is the daily oral, is their highly scalable, global distribution play. They cover every single square of the board.

The compounding threat is ending. Ricks noted that their $50 federal access pricing, part of their MFN deal with the administration, will completely obliterate the compounding market. Compounders have been skirting rules by mixing in Vitamin B12, creating completely untested, new complex molecules. The FDA loophole is closing, but Lilly is focused on pricing them out of existence.

And the consumerization of healthcare is here. LillyDirect now accounts for one-third of all obesity sales in the US and over 50% of new Zepbound prescriptions. They bypassed the PBMs. They bypassed the pharmacies. They are building a direct, 1P data relationship with the consumer. This creates price discipline.

Lilly is evolving from a pharmaceutical company to a consumer staples juggernaut with tech R&D speed. They sped up clinical timelines from 11 years to 6 years. They are doing 40 deals a year and are sizing up their M&A targets. They objectively view incretins as the modern equivalent of antibiotics, which is a foundational baseline to prevent chronic disease and fundamentally alter human longevity. Feels like early innings here still...

4

1

35

11,329

Apr 24

romanticize the glorifications the normalization the influenzation the fetishismism and enablizationisms of the consumerization o

4

52

1,216

Apr 22

even people in the lower income brackets in the UK are paying for GLP-1s out of pocket. incredible and more to come as consumerization hits full throttle in the UK market

2

1

7

1,571

My personal email inbox is scary!

Bullish on the consumerization of email. This team seems to be taking an interesting approach.

1

3

20

7,237

The consumerization of healthcare is prioritizing accessibility over evidence-based medicine.

The contrast between having access to things with limited evidence versus having limited access to evidence-based treatments is interesting. I'm unsure which world I prefer.

1

1

9

1,166

Apr 14

The consumerization of healthcare continues

Apr 14

WHOOP 🤝 MEDICARE

This week marks a defining moment for @whoop - and a major leap forward for Medicare with eligible individuals now able to receive Whoop as part of their care.

Our affiliated healthcare provider, Whoop Physician Services, PC, has been selected for the CMS Innovation Center’s ACCESS program, a first-of-its-kind initiative to bring technology-enabled, longitudinal care to Medicare beneficiaries to prevent chronic disease.

2

14

4,134

Apr 12

The gentrification of consumerization really highlights the contradiction of masterbation in retrospection

3

167

Apr 12

you just HATE mentally ill people and the consumerization of the justification of the masturbation of the dehumanization

3

14

216

2,324

Apr 12

How dare ya buddy, thats literally so anti art and the normalization of fandomization and consumerization and and

49

2,066

Apr 9

New @ThePeelPod with @nikillinit

100 minutes learning how the US healthcare system actually works, how a change to the tax code during World War II broke it forever, and how AI can fix it.

Thanks to @numeral @FlexSuperApp and @Amplitude_HQ for sponsoring!

Timestamps:

1:23 How the US healthcare system works

4:26 Why US healthcare is different from the rest of the world

12:01 Why healthcare costs keep going up

15:58 Core problem: is healthcare a marketplace or not?

21:04 How money flows Two-way price negotiation

27:34 Why payments are seeing early AI adoption

30:08 How AI could change healthcare delivery

35:40 Doctor’s are trapped on a productivity hamster wheel

39:28 How incentives shape healthcare delivery

43:53 Healthcare is an implicit jobs program in the US

48:45 Areas AI is overhyped, worst healthcare startups

55:30 Consumerization of healthcare

1:01:58 Rise of Peptides, understanding risks and downsides

1:09:35 Why all medical software is so bad

1:11:58 How to do enterprise sales in healthcare

1:14:51 The battle forming between Scribes, Search, and EMRs

1:18:33 Why we need more physician independence

1:26:51 Starting Out of Pocket in February of 2020

1:29:12 Write to meet your audience

1:37:54 Using AI as a content creator

1:42:13 How to get started writing on the internet

Stream here or below!

YouTube: youtu.be/b-e8QhvW8_A

Spotify: open.spotify.com/episode/5qR…

Apple: podcasts.apple.com/us/podcas…

Read the Transcript: thespl.it/p/how-us-healthcar…

5

2

13

4,483

Apr 8

The consumerization of healthcare feels less like disruption and more like a correction. Every other industry moved toward convenience, transparency, and user control decades ago. Healthcare was always going to follow. #health #healthcare

linkedin.com/posts/joncwarne…

2

3

83