May 21

#SME #CreativeGraphics #CGRAPHICS

Creative Graphics Solutions India H2FY26 Concall Highlights

👉 FY27 & Future Outlook

▫️Better optimism for FY27 with normalization of supply chains expected within 1-2 months

💠Q1-Q2 may see residual volatility but later on poised for sharp acceleration as new capacities (Alu-Alu, PVDC, Tandem, Bangalore Flexo) fully commercialize and contribute meaningfully

💠Installed capacity across businesses already supports 1000 Cr annual turnover

💠Management’s long-term ambition remains doubling top-line every year (non-linear journey) — (reiterated as realistic given current order traction and capacity headroom)

▫️Warren (pharma packaging) to drive ~80% of target (Alu-Alu PVDC Tandem blister); Flexo ~20%.

💠At optimal utilization: Warren gross margins targeted at 17-18%, EBITDA mid-teens (13-14%) — higher in exports and value-added products (holography, anti-counterfeit)

💠Margins bottomed in H2 FY26; sequential improvement expected from FY27 onward as front-loaded expansion costs are absorbed, supply volatility eases, and price hikes (already 30% on Alu-Alu, ~25% on PVDC) fully flow through

💠Exports (first order Feb 2026) to be key margin driver with better realizations; 20% export share targeted for Alu-Alu/PVDC business

💠Overall: FY27 viewed as “year of major action” as per management; to deliver meaningful step-up vs FY26’s consolidated revenue

👉 Current Order Book / Projects and Future Pipeline

▫️Domestic order book “full” and spilling over month-on-month

💠Unable to fulfill all orders due to raw material supply constraints (not demand)

💠Export order book: First order received Feb 2026; 100 MT in hand (pipeline significantly higher); long-gestation but high-realization focus; targeting 20% of pharma packaging revenue from exports

💠Existing 8,000 MT Alu-Alu plant utilization ~80% in H2 FY26 despite March-May disruptions

▫️New capacities update:

💠12,000 MT Alu-Alu foil factory (Wahren): Machine installed, trial runs complete, on cusp of commercialization (well before original H1 FY27 guidance); expected to add significant volume in FY27

💠 PVC/PVDC line: Commercialized end-H2 FY26; small revenue in H2 (~₹0.5-0.6 Cr); targeting ~25% utilization in FY27; orders in hand but raw material shortages impacted ramp

💠Tandem extrusion machine: Commercialized April 2026; currently sampling stage; new product line for pharma

💠Bangalore Flexo factory: Already running; client acquisition & testing stage; strategic location for South India growth

💠Oman Flexo factory: Installation complete but delayed due to war-related supply/manpower issues; expected commercialization in next quarter

▫️Pipeline drivers:

💠Latent demand in PVDC/Tandem (import substitution export potential); unmet demand in specialty products

💠Blister foil line newly started (machine acquired); consistent client export demand

💠Pharma packaging market tailwinds: Alu-Alu ~5,000 tons/month (~₹500/kg avg.); blister market ~double; PVDC 3,000-4,000 tons/month

▫️Current India Alu-Alu market share ~8-10%; well-distributed across 400 clients (no 80-20 concentration; top clients like Intas, Zydus, Cadilla, Torrent buying progressively higher volumes)

▫️Competitive edge vs incumbents: Broader product portfolio (Foil, blister, PVC/PVDC, tandem 3/4-layer)

💠Printing value-add from Creative legacy, faster capacity/capability build in 3.5 years

👉 Other Notable Points

▫️FY26 performance recap:

💠 Consolidated revenue ₹348 Cr (vs ₹256 Cr FY25)

💠PAT ₹18.76 Cr (vs ₹20.77 Cr FY25) — slight decline due to :

(1) Front-loaded expansion costs (employee 25%, finance 42%)

(2) ~₹5 Cr gross margin hit in H2 from Alu price/FX volatility war-related supply disruptions

💠 H2 sales ₹172 Cr (vs H1 ₹177 Cr) impacted by pharma supply issues (esp. March) and softer Flexo macro

💠Standalone boosted by ~₹27 Cr internal Creative-to-Wahren sales

▫️Risk mitigation & financial preparedness:

💠Debtor insurance continued on all receivables

💠Added Citibank as second banker first bill-discounting facility (₹3-4 Cr done in Mar’26, scalable); working capital limits enhanced to support growth

▫️Management additions:

💠New CEO (ex-DuPont, 30 years flexo expertise) for Creative Graphics line

💠New plant head for Wahren; manpower increase primarily for new capacities

▫️Supply chain & hedging:

💠Still not fully out of woods but visibility improving

💠Significant aluminum inventory built as natural hedge; hedging enabled but not yet active (premiums high)

💠Price hikes fully passed on to clients (partnership model); no long-term contracts — monthly orders allow flexibility

▫️Client & market dynamics:

💠Pharma clients understand temporary supply issues (industry-wide); no demand drop; sticky business with high qualification barriers

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

1

15

3,445

May 21

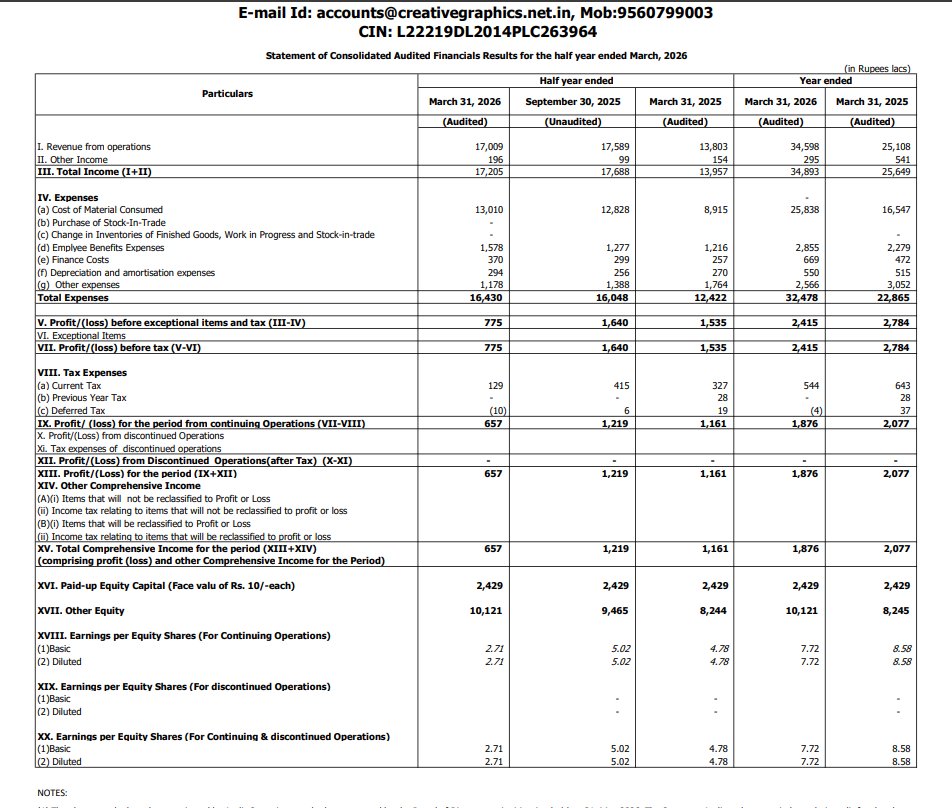

Creative Graphics Solutions India Limited (SME) H2FY26 Results:-

#H2FY26 #Stockmarket #Nifty #Creativegraphics

H2FY26 vs H2FY25

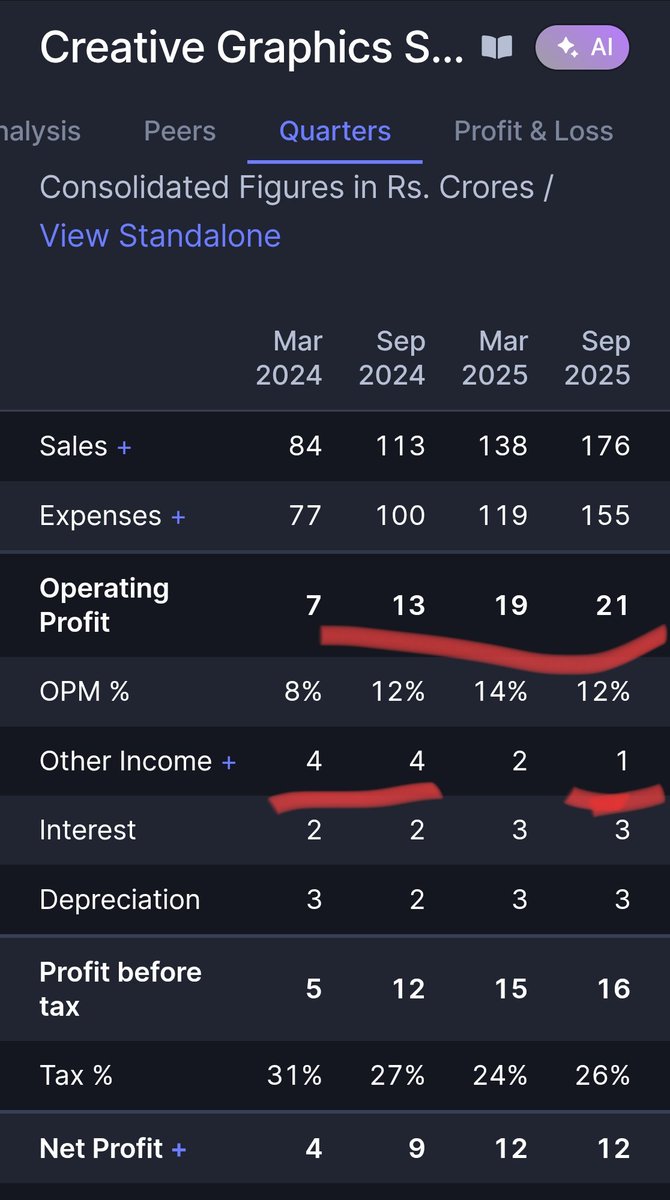

Revenue 170.09 Cr vs 138.03 Cr ( 23.23% YoY)

EBITDA 12.43 Cr vs 19.08 Cr (-34.85% YoY)

EBITDA Margin 7.31% vs 13.82% YoY

PBT 7.75 Cr vs 15.35 Cr (-49.51% Yo)

PAT 6.57 Cr vs 11.61 Cr (-43.41% YoY)

Other Income 1.96 Cr vs 1.54 Cr YoY

2

1,313

Mar 11

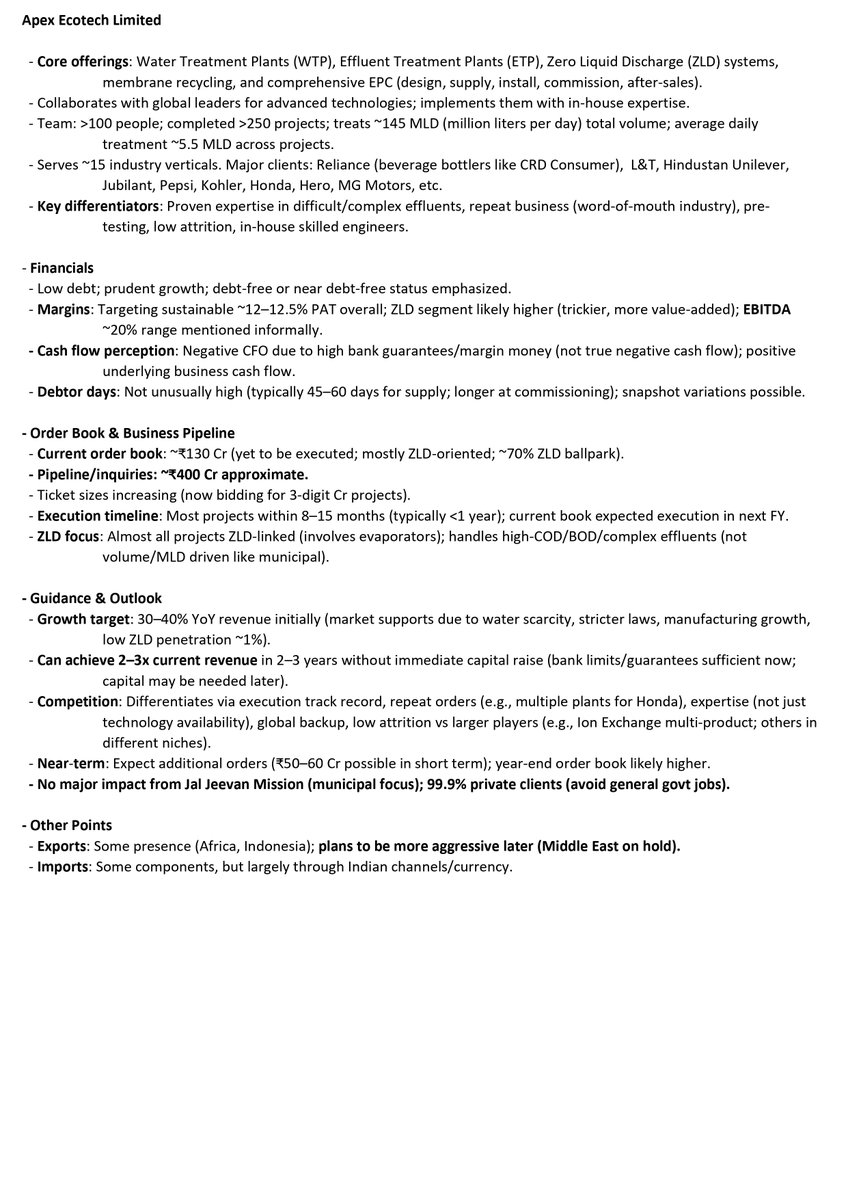

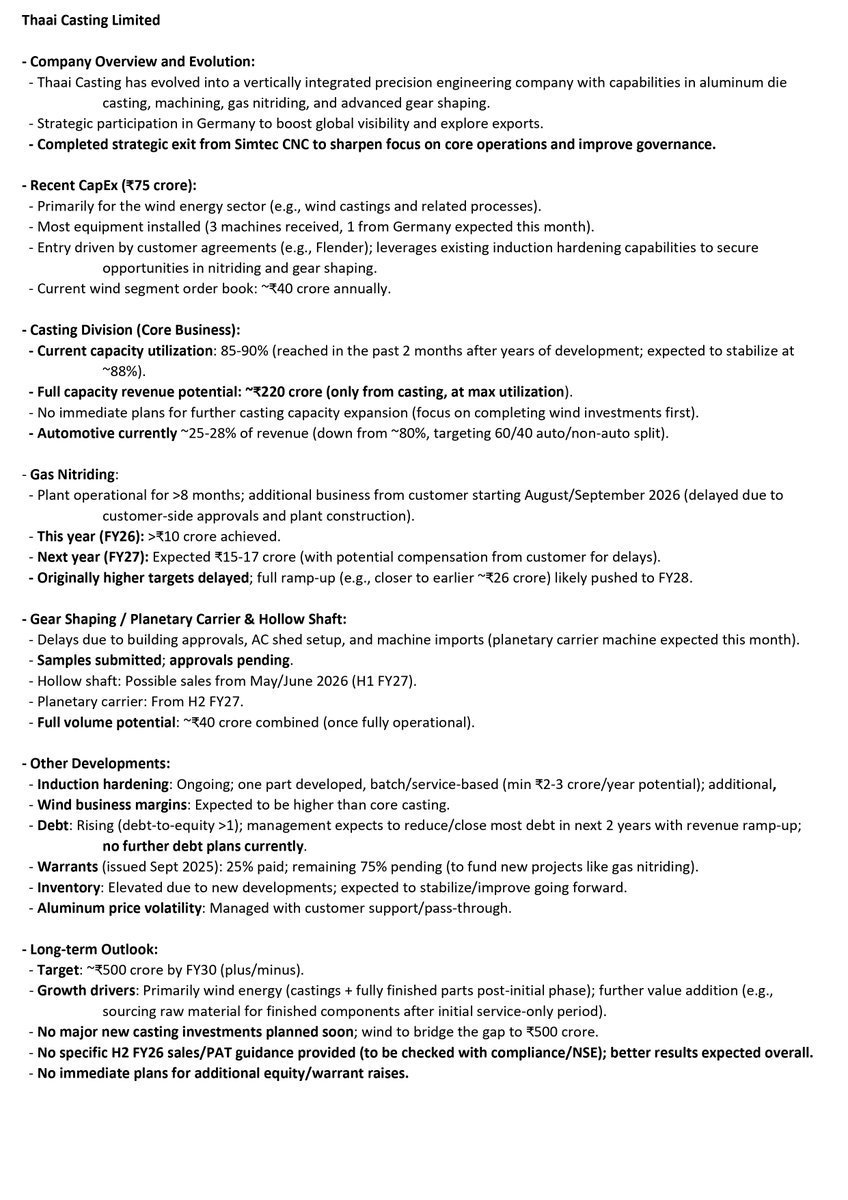

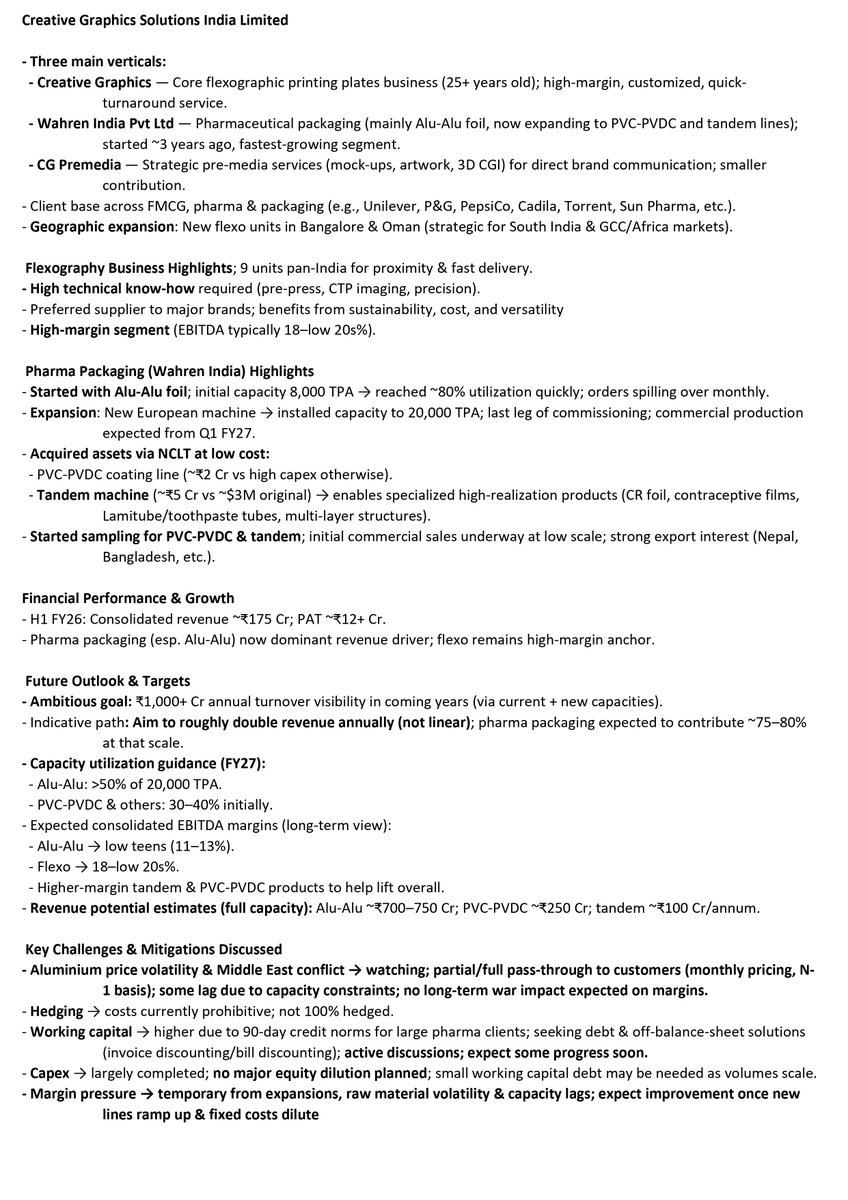

Arihant Bharat Connect Conference March '26:

👉Day 4:

💠Creative Graphics Solutions

💠Thaai Casting

💠Sadhav Shipping

💠Apex Ecotech

💠KVS Casting

#cgraphics #apex #thaaicasting #tcl #sadhav #sadhavshipping #kvscasting #kvs #apexecotech #creativegraphics #bharatconnectconference #arihantcapital

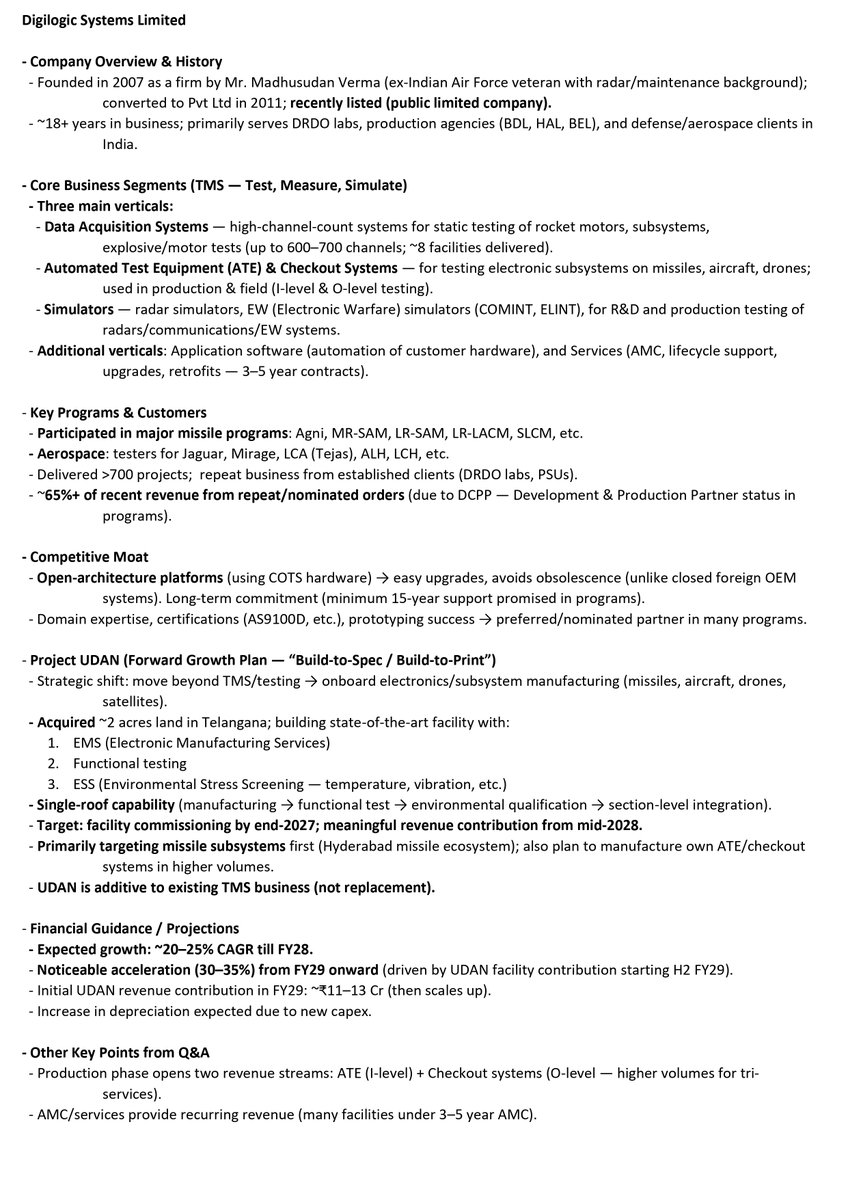

Mar 11

Arihant Bharat Connect Conference March '26:

👉Day 4:

💠Fredun Pharmaceuticals

💠Sugs Lloyd

💠Digilogic Systems

#digilogic #digilogicsystems #sugs #sugslloyd #fredun #fredunpharma #bharatconnectconference #arihantcapital

7

3

31

7,315

With Biroller, you are putting your faith in headlights that will increase your visibility so much that you will feel like an eagle who can spot anything from miles above.

Shop now on @amazonIN

#carlights #carlighting #bikerlovers #CreativeGraphics #creativitymatters

2

37

21 Dec 2025

Great to see Creative graphic being presented at AIS, I had a chance to present it at HIE and we have put out an instructional level report on them as well

Also @Orbit_Cap had put out a beautiful presentation on ztech as well

#creativegraphics #ztech #IAS2025

21 Dec 2025

IAS 20-20 : Dec 2025

1. Rajeev Agarwal - Tamilnad Mercantile Bank (Secured loan book franchise)

2. Piyush Sarawagi - Macpower CNC Machines (High-value-high-margin-machines growing)

3. Ankit Kanodia - Jayaswal Neco Industries (Turnaround almost complete...at inflection point)

4. Aggarwal Brothers - GHCL Textiles (Worst is behind)

5. Vijay Bharadia - Claro energy (Unlisted)

6. Kumar Saurabh - 3B Blackbio DX (Quality company in a growth sector run by quality promoters)

7. Parveen Yadav - DCM Shriram (On a growth trajectory)

8. Akshay Jogani - MTAR Technologies (90cr PAT to 300cr PAT in 2 years)

9. Gunjan Kabra - Valiant Communications (Final puzzle of Energy value chain)

10. Ishmohit Arora - CSB Bank and Fedbank Financial Services (Gold-en Transformation)

11. Rukmik Oza - KEC International (T&D is still alive)

12. Vivek Mashrani - Eicher Motors (Focussed Growth)

13. Ganesh Nagarsekar - Pyramid Technoplast (Peak capex cycle done)

14. Sonam Srivastava - Lumax Auto Technologies (20-20-20-20)

15. Shubham Sethi - Kwality Pharmaceuticals (New growth triggers and new geographies)

16. Nitin Mangal - Greaves Cotton (dual-engine growth story)

17. Shashank Mahajan - Z-Tech India (Sustainable and scalable creativity)

18. Vikas Gupta - REC Ltd (Mispriced multibagger)

19. Gaurav Agarwal - Creative Graphics Solutions (Cash Engine Growth Option = Asymmetric Compounding)

20. Amitabh Vatsya - JNK India (Moving to high value-add with large TAM)

2

2

20

4,398

20 Nov 2025

Creative Graphics Solutions

#CGraphics

#CreativeGraphics

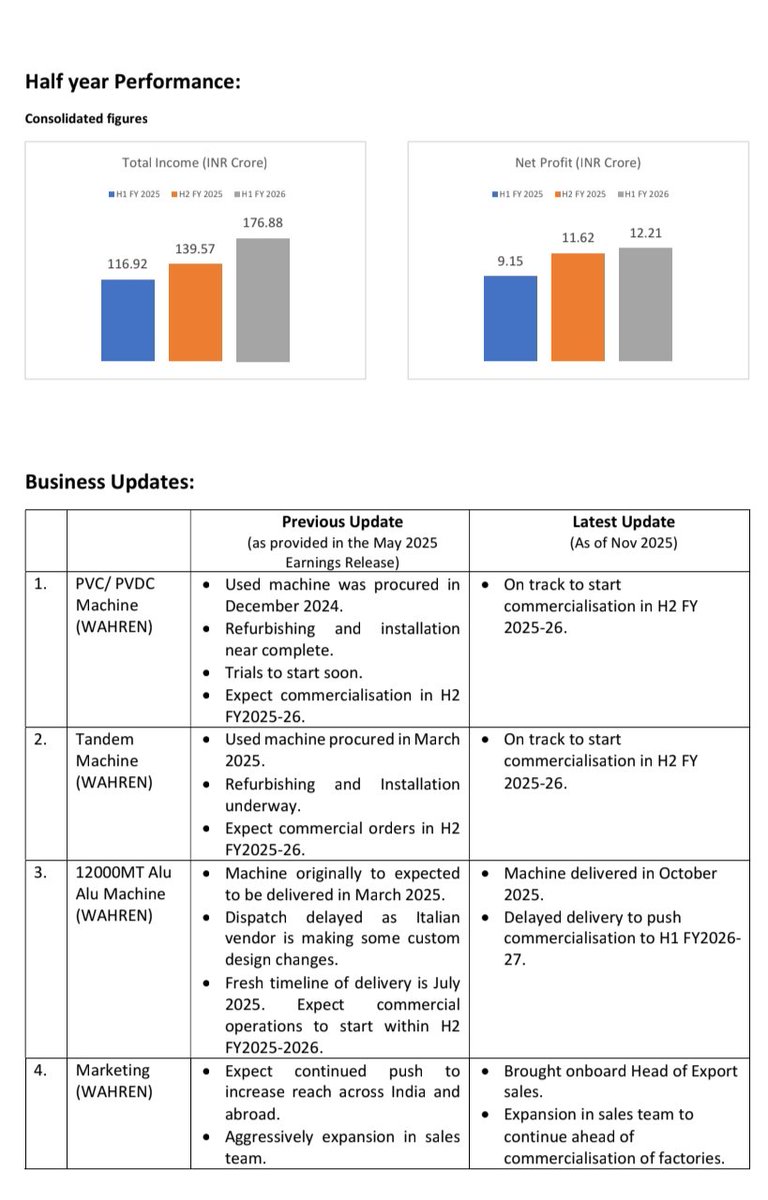

H1FY26 Concall pointers:

Very good concall with great clarity from management wrt business insights, future plans,new capacity ramp up and utilization targets

Expects H2 to be higher/stronger than H1 because multiple new lines are coming online in H2FY26

1.PVDC/PVC line commercialisation in H2

2.Tandem line commercialisation in H2

3.Bangalore flexo plant already up and running and ramping up well

4.Oman flexo plant expected in H2- Trial runs ongoing

Wahren (pharma packaging) will continue to grow much faster than the flexo plating business

Strong enquiries from multiple pharma companies

Known for quality and best pricing

Margins:

Expects current to sustain/improve over time because:

Raw material price increases are now being passed on

Shift in product mix to higher-value products (PVDC & Tandem have better gross and EBITDA margins)

Can go back to/ has good scope to exceed 8-9% PAT margins once scale up benifits and product mix change kicks in as operating leverage will start playing out

Capacities:

Alu-Alu

Current capacity

8,080 MT/annum

75% utilisation

New Italian machine (12,000 MT) delivered Oct 2025

Commercialisation in H1FY27

Total capacity post expansion:

20,080 MT/annum

Expects 75–80% utilization on existing capacities

30–40% on new machine in FY27 and 70% by FY28

PVDC/PVC coated line:

New capacity online from H2FY26 Commercialisation on track

Capacity of12,000 MT/annum

15%-20% utilization in H2FY26

Target 70–80% utilization by end of FY27

Significantly higher realizations vs Alu-Alu

Tandem line:

Commercialisation on track for

Better margins expected

Strong enquiries

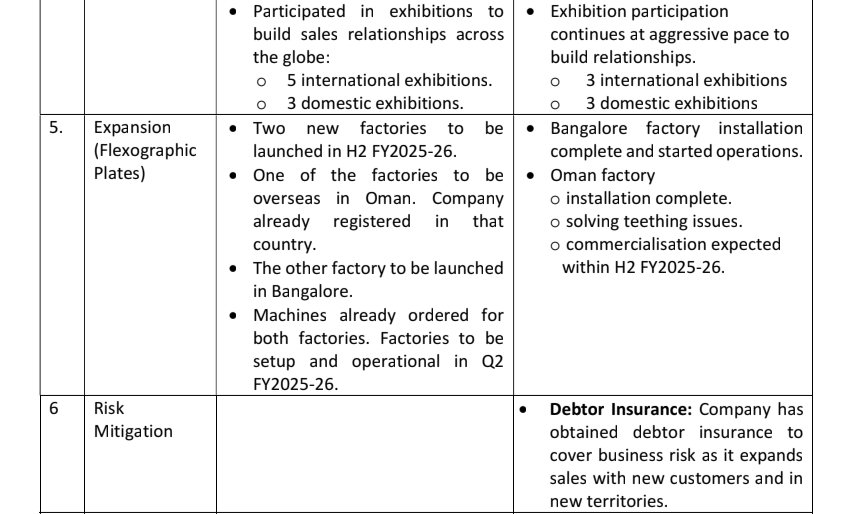

Flexo Plate Business Expansion: Bangalore plant already started operations, ramping up well

Oman plant

Installation complete, solving teething issues

Commercialisation expected in H2FY26

Can ramp up well as demand is very strong

Exhibition participation and good response for the products

6 international 6 domestic in last 12 months

Exports to be 20% of total revenues

4-5% higher margins here

Large pharma clients added (Aurobindo, Torrent Pharma, Sun Pharma in process)

Shift from small to A clients now visible and focus would continue in that direction

Aluminium price spike impact largely absorbed

Almost 100% passthrough now possible on new orders

2

8

113

18,326

17 Nov 2025

📔 15 Nov Note No5 . H1FY26 RESULTS BRIEF REVIEW . IS IT GOOD? Some More!

EARKART, PRARUAH, JAY AMBE, ADCOUNTY, ENSER, SA TECH, CREATIVEGRAPHICS, DE NEERS TOOLS, EMA PARTNERS, CANARYS

EARKART: IS IT OKAY?! The numbers does not warrant the valuation it gets (which seem to be driven by VIP invetor presence) . H1 revenue is better then previous H2. Slightly lower than H1Fy25. TTM Pat has come down to Rs.5.43Cr from 6.88Cr. Rs.221 was at 44 p/e . Now 56x.

Very Recent IPO: There is Rs.17Cr capex fund to set up hearing clinics. May be that would help in Fy27. But the market is much narrower than Lenskart. So take care!

PRARUH TECH: NOT GOOD AT ALL! Computer hardware seller SUDDENLY finds buyers vanished after IPO?! Sales 28Cr (H1Fy25) to 34 Cr (H2FY25) and suddenly now in this H1 after IPO, it has crashed to 17Cr with just 98Lakh PAT!

Very Recent IPO: Opening scene doesn’t look good at all

JAY AMBE SUPERMARKET: OKAY . H1 is just above H2FY25 and far better than H1FY25. But margin is very much down compared to previous H1. Rs.103 was at 33p/e. Now 30.5x

Very Recent IPO: There is 8.9Cr capex for adding new stores. So expect better numbers in FY27.

ADCOUNTY: GOOD. There are signs of growth. Sales in H1 is lower than that in H2Fy25 but 5Cr higher than previous H1. TTM Pat has gone up from 13.7Cr to 15.8Cr. Rs.178 was at 29p/e. Now 25x. About 35Cr for WC and capex should help to report better numbers in H2

ENSER: GOOD But the excessive bonus and split has damaged the stock by making it into a under Rs.20, penny stock. H1 Revenue (44Cr) is higher than both H1 & H2 of Fy25 Rs.18 was at 18p/e. Now 19.5x (Approximate number since Consolidated H2Fy25 is not given)

Company has to deliver 60 Cr and above to improve EPS nicely, to avoid getting stuck below Rs.20

SA TECH: NOT GOOD. NO GROWTH LOSS reported Last 3 half year results show ~50Cr sales. This is even with 6Cr additional epmploee costs in H1Fy26 compared to previous 2 periods. Though segmentwise revenue is not provided, considering high staff costs we can safely assume, there is hardly any GCC income. TTM Pat is down to 2.27Cr from Rs.7.4Cr. Company has reported LOSS in this H1. Rs.38 was at low 7p/e. Now 22x

CREATIVE GRAPHICS: GOOD. Signs of growth after lackluster previous periods from time of listing. H1 Revenue has flared up to 177 Cr and beats both previous H1 and H2. There is potential for higher sales in H2 and beyond with factory expansion Rs.206 was at 24p/e. Now 21x.

DE NEERS TOOLS: FLAT. No GROWTH. With this flat result and 15% promoter stake sale, the stock is likely to consolidate (with negative bias) till good sales growth is reported. Rs.161 was at low 8.8p/e. Now same. FLAT Better not to get stuck for long unless there is some company guidance of H2 sales of 85 to 90Cr. .

EMA PARTNERS: FLAT with slight positive bias. Marginal 3Cr increase to 43Cr sale in this H1s with repect to previous H1 and H2 which were flat at 39Cr. Bottom line remains unchanged. Rs.98 was at 18p/e. Now SAME. Unless there is around 50 to 55cr sales in H2, this stock won’t move, in this hard market.

CANARYS AUTOMATION: VERY GOOD with SUBSIDIARY Revenue. Company has reported 66Cr income and 4.86Cr PAT from subsidiary in H1. (Is this from FORTIRA Inc acquired in April 2025???) This is consolidated to get revenue figure of Rs.101Cr in H1 which is a very big jump (double the usual revenue ) This should have positive impact on stock . The TTM Pat is 10.84Cr ( minority interest less). Rs.29 ws at 23p/e. Now . 17x.

Previous Lists

List 4: x.com/RajStockWatch/status/1…

LIST 3: x.com/RajStockWatch/status/1…

List 2: x.com/RajStockWatch/status/1…

List 1: x.com/RajStockWatch/status/1…

Posts 1, 2 and 3 with Result Links: x.com/RajStockWatch/status/1…

12 Nov 2025

H1FY26 RESULTS: Some Interesting SME Stock Results. Good, Bad and Ugly too!

Save THREAD 🧵For Future Reference

Post 1/

BOOKMARK 🔖 THIS FIRST POST so that you can refer the thread later

(You can also find Result review by searching Company Name (single word only) at @rajstockwatch

Vision Infra: x.com/RajStockWatch/status/1…

LT Elevator: x.com/RajStockWatch/status/1…

Sahaj Solar: x.com/RajStockWatch/status/1…

Kaushalya Logistics: x.com/RajStockWatch/status/1…

Shree Refrigeration: x.com/RajStockWatch/status/1…

Trident Techlabs: x.com/RajStockWatch/status/1…

Techera: x.com/RajStockWatch/status/1…

Kabra Jewels: x.com/RajStockWatch/status/1…

POSITRON: x.com/RajStockWatch/status/1…

SADHAV SHIPPING: x.com/RajStockWatch/status/1…

CapitalNumbers: x.com/RajStockWatch/status/1…

Namo eWaste: x.com/RajStockWatch/status/1…

ChemKart: x.com/RajStockWatch/status/1…

ZTECH: x.com/RajStockWatch/status/1…

TRUE COLORS: x.com/RajStockWatch/status/1…

PATIL AUTOMATION: x.com/RajStockWatch/status/1…

SAFE ENTERPRISES: x.com/RajStockWatch/status/1…

CONNPLEX: (Error: New screens being added is >60) x.com/RajStockWatch/status/1…

… Continued to Post 2 🧵

BOOKMARK 🔖

2

2

33

7,417

16 Nov 2025

Creative Graphics

#CGraphics

#CreativeGraphics

Strong H1FY26

Highest ever revenue, EBITDA, PBT and PAT in comps history

2nd half should be more stronger due to new machines that would contribute in H2

H1FY26:

Rev at 176cr vs 113cr⏫56%

H1 at 138cr

EBITDA at 21cr vs 13cr⏫62%

H1 at 19cr

PVC/PVDC machine:

Tamdem machine:

On track to be commercialized in H2FY26

12000 Mt Alu Alu machine:

Delivered in Oct 2025

H1FY27 commercialization

Flexographic plates:

2 new factories to be launched in H2

Operational from Q2 -Bengaluru

Oman factory to commence in H2FY26

6

9

178

41,138

24 Oct 2025

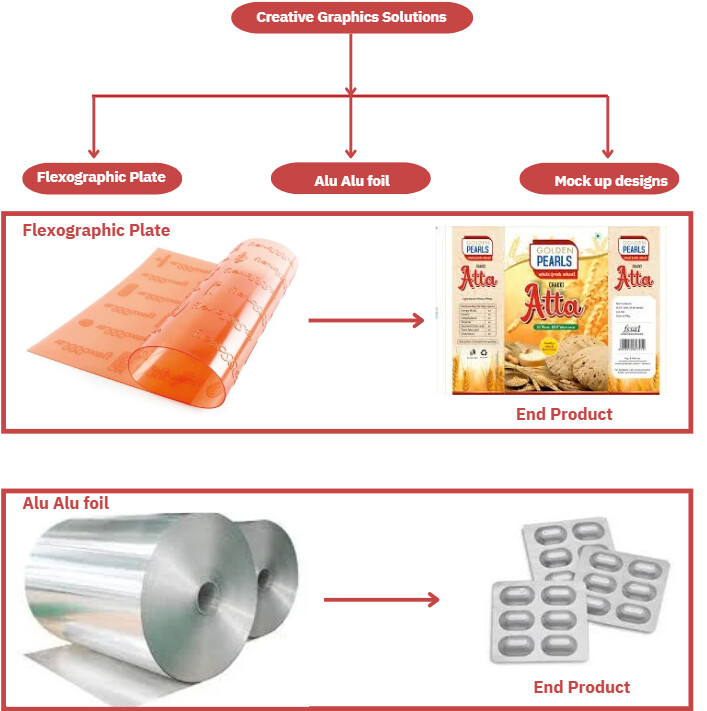

CG is a leading player in pre-press printing, specializing in flexographic plates that are fast, cost-effective, and eco-friendly. Its units include CG Pre Media for FMCG prepress services and Wahren for advanced pharma packaging foils.

CMP - 210

#flexographic

#CreativeGraphics

1

2

395

11 Oct 2025

Which do you prefer?

DM today, let's give your brand tranquil visuals (pun intended) ......

#EchoverseGaming #LogoDesign #GraphicDesign #designs #CreativeGraphics #DesignCommunity #NaijaDesigners #VisualDesign #BrandGraphics #DesignVibes

1

1

2

21

9 Oct 2025

Virtual realities can be real too... Believe

Plug in. Power up. Play hard. ⚡

VR so real, you’ll forget what’s real 😎

#EchoverseGaming #GraphicDesign #FlyerDesign #CreativeGraphics #DesignCommunity #NaijaDesigners #VisualDesign #BrandGraphics #DesignVibes

1

1

3

30

30 Sep 2025

fiverr.com/s/gD3k5YW

🎨 "Logo design e creativity er notun chhobi."

🚀 "Brand identity ke aro prokashito korun."

📩 "DM kore apnar design er idea share korun."

#LogoDesign #BrandIdentity #CreativeGraphics

#SunnySanskariKiTulsiKumari #Bengalis #Paxlovid #Tamilnadu

2

114

29 Sep 2025

Creative Graphics, a leading provider of high-quality flexographic printing plates for over 20 years in India, showed its pre-mounted ...

@IndiaCorrExpo #DeepanshuGoel #flexographic #CreativeGraphics #flexoplates #automation #pharmaceutical

Read More... packagingsouthasia.com/appli…

2

102

23 Sep 2025

I don't believe in taking right decisions.

I take decisions and them make right.#graphicdesign #creativegraphics #brandidentity #brand #brandstrategy @President Museveni 2026-2031 @Maama Janet Museveni💛🇺🇬 @Muhoozi Keinerugaba original

2

127

8 Sep 2025

A Minimalist Simple Design for Bimmie Stitches which one would you go for A or B

Smiles Graphics

#design #CreativeGraphics #flyerdesign #graphicdesign #flierdesign #logodesign #socialmediadesign

1

26

6 Sep 2025

⚽️⚽️ Elevate Your Game with Bold Design!

At Limitless Design, we don’t just design — we bring energy, motion, and purpose to life through *dynamic visuals* like this!

Whether you’re in sports, fashion, music, or business, your brand deserves visuals that *jump off the screen* — just like this.

✅ Sports Flyers

✅ Athletic Brand Identity

✅ Event Posters

✅ Bold Social Media Content

📲 Let’s create something powerful and limitless together.

DM or Call Now: 0541418061 / 0504592947

Instagram: @Limitless.design._

Limitless Design – Where Creativity Takes Flight.

#SportsDesign #CreativeGraphics #LimitlessDesign #BasketballFlyer #BrandDesign

5

13

11

305

6 Sep 2025

🏀 Elevate Your Game with Bold Design!

At Limitless Design, we don’t just design — we bring energy, motion, and purpose to life through *dynamic visuals* like this!

Whether you’re in sports, fashion, music, or business, your brand deserves visuals that *jump off the screen* — just like this.

✅ Sports Flyers

✅ Athletic Brand Identity

✅ Event Posters

✅ Bold Social Media Content

📲 Let’s create something powerful and limitless together.

DM or Call Now: 0541418061 / 0504592947

Instagram: @Limitless.design._

Limitless Design – Where Creativity Takes Flight.

#SportsDesign #CreativeGraphics #LimitlessDesign #BasketballFlyer #BrandDesign

8

15

13

271

5 Sep 2025

WENS is turning every car into a masterpiece

#WENS #Ceramiccoating #Cardetailing #Detailingwithstyle #Creativegraphics #Digitalart

4

2,433

3 Sep 2025

Turning vision into visuals, church design that inspires.

#DesignClients #ChurchBranding #CreativeGraphics #FaithDesign #GraphicDesign

2

60

14 Aug 2025

From idea 💡 to masterpiece 🍽️ this food flyer proves what Medu Studios can do for your brand. Let’s design visuals that promote, elevate & make your business unforgettable 🚀

#MeduStudios #FoodFlyerDesign #GraphicDesign #Branding #CreativeGraphics #DesignThatSells #medugraphics

2

60