Mar 14

Loton: Dynamic Crypto Pools

Many people are still asking what Loton actually is and what they should expect from the upcoming beta launch on March 16, 2026.

To make everything clear, we’ve prepared a detailed presentation that explains the concept, the idea behind dynamic crypto pools, and what the beta test will bring.

If you want to understand the project better before the launch, this presentation will help you get the full picture.

👉 Read the presentation:

telegra.ph/Loton-Dynamic-cry…

The beta test chat is also open if you want to disc

uss the project or ask questions with the community.

💬 Got questions or thoughts? Drop them in the comments, we’d love to hear your feedback.

#Crypto #DeFi #Web3 #CryptoPools #CryptoLaunch #CryptoCommunity #Blockchain #BetaTest

7

81

YAP on Mindo đang nóng dần lên, và những pool này thật sự đáng để nhìn kỹ hơn.@TauntCoin mang màu sắc thử nghiệm rất rõ, build nhanh và có cộng đồng tương tác tốt.

@useTria đi theo hướng hạ tầng, ít ồn ào nhưng càng đào càng thấy chắc.

@PerceptronNTWK chơi bài AI đúng nghĩa, không chỉ narrative mà có chiều sâu sản phẩm.

@intodotspace khá thú vị ở cách tiếp cận data và không gian số, làm chậm nhưng đều.

@c8ntinuum vẫn giữ phong độ với tư duy multichain dài hạn, càng về sau càng thấy rõ lợi thế.

@DeepNodeAI thì khỏi bàn, nền tảng security là combo rất khó bỏ qua.

@helios_layer1 mang vibe L1 mới, chưa quá đông nhưng tiềm năng mở rộng còn xn--rng-6mz.Không phải pool nào cũng x2 x3 ngay, nhưng nếu kiên nhẫn, đây là những cái tên đáng để farm và theo dõi dài hơn một chút.#Mindo #YAP #CryptoPools #Web3

26

16

128

26 Nov 2025

If you are looking to buy $YB and not sure how it accrues value? You might want to read this.

On @yieldbasis borrowing $crvUSD and locking it with $BTC provides 2x yield to LPs but how does the value flow back to $YB & $CRV holders?

Interesting thing about LPing on @yieldbasis: Borrowing $crvUSD creates demand instead of sell pressure.

Every $crvUSD borrowed is paired with $BTC and locked into @CurveFinance, which means:

-> No sell pressure

-> Deeper liquidity

-> Stronger peg

-> More fee flows across Curve pools

This loop also routes real value back to both $YB and $CRV:

> BTC/crvUSD trading fees flow to ybBTC holders & veYB (via the dynamic admin fee)

> Rebalancing volume drives more fees to veCRV across cryptopools & stableswap

> Borrow interest gets recycled inside YieldBasis to power the rebalancing engine

> Curve receives a share of $YB emissions via gauges, strengthening CRV voting over BTC pools

Simple flow: Borrow $crvUSD -> lock it -> deepen liquidity -> generate volume -> fees -> value accrues to $YB & $veCRV.

17 Oct 2025

How @yieldbasis eliminates impermanent loss(please note it is not due to incentives but due to the design)

Lets say, we deposit in an AMM and start with 1 BTC and $100,000 in stablecoins, and if the BTC's price doubles to $200,000, our AMM position might end up with approximately 0.707 BTC and $141,000 in stablecoins, totaling around $283,885.

In contrast, simply holding would have given us $300,000, resulting in about a 5.7% IL.

How does it work in @yieldbasis and how does it eliminate this loss?

1. We deposit BTC worth $100,000 at current price(assume)

2. The protocol borrows an equal value of $crvUSD ($100,000) using our $BTC as collateral.

3. Our 1 BTC and the borrowed $100,000 crvUSD are paired and supplied into the Curve BTC/crvUSD liquidity pool.

4. The resulting Curve LP tokens are then used as collateral for the $crvUSD debt.

5. The system maintains a 2× leverage ratio, meaning the debt is always 50% of the total LP value.

This is achieved through automated rebalancing mechanisms involving arbitrageurs and virtual pools.

By maintaining this constant leverage and ensuring the position tracks BTC price 1:1, YieldBasis effectively eliminates impermanent loss.

Rebalancing:

When BTC's price changes:

->If BTC price rises, the LP's value increases, but the debt remains fixed. To restore the 50% debt ratio, arbitrageurs can bring in additional crvUSD, mint more LP tokens, and adjust the debt accordingly.

->If BTC price falls, the LP's value decreases, but the debt remains fixed. To restore the 50% debt ratio, arbitrageurs can remove some LP tokens, withdraw crvUSD, and reduce the debt accordingly.

This dynamic rebalancing ensures that our position always tracks BTC price movements, maintaining the 1:1 correlation and eliminating impermanent loss.

Earning with YieldBasis:

1. We earn trading fees from the underlying Curve pool directly in BTC.

2. We can stake your ybBTC to earn YB token emissions instead of trading fees. Additionally, vote-locking YB tokens grants voting power and a share of BTC fees.(Similar to the $CRV token holders getting bribes)

Important things to note:

1. The debt ratio is also balanced to 50%

2. CRVUSD is initially borrowed with BTC as collateral and

3. LP position after depositing in AMM is again used as collateral for the CRVUSD that was borrowed

4. As price changes, arbitragers can balance the pool to earn additional rewards

5. Additional incentives in $YB for depositing

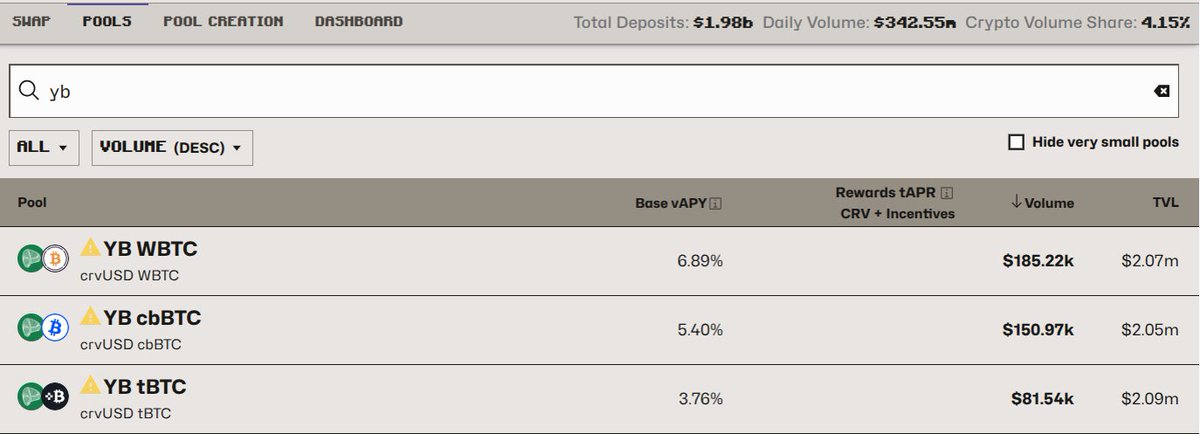

6. Pool will later add other assets and will have higher demand for crvUSD.

10

5

44

5,792

24 Nov 2025

Not all charged fees make it to DAO indeed! Especially the case for cryptopools.

Good to count vote incentives to veCRV also

1

3

110

22 Nov 2025

It deviates when cryptopools unbalance and goes back to this value when they rebalance. In huge volatility they can be unbalanced for longer than few days!

2

458

20 Oct 2025

crvusd share in curve cryptopools is swinging 40–60%, showing a 10% mismatch vs backing. with each yb pool (wbtc, cbbtc, tbtc) at $100m tvl, curve needs to absorb ~$30m crvusd. stable pools act as a sink and can take a 25% imbalance, putting required pool tvl at $40m — aligned only if total crypto tvl sits near $300m

1

2

466

11 Oct 2025

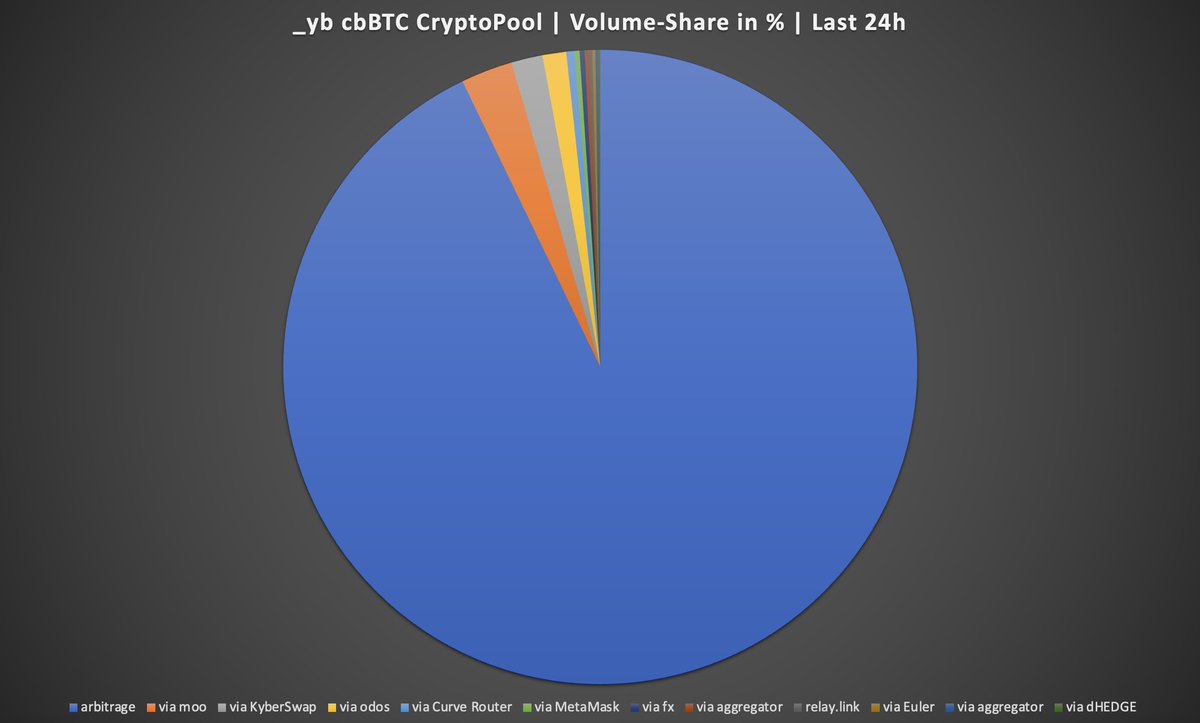

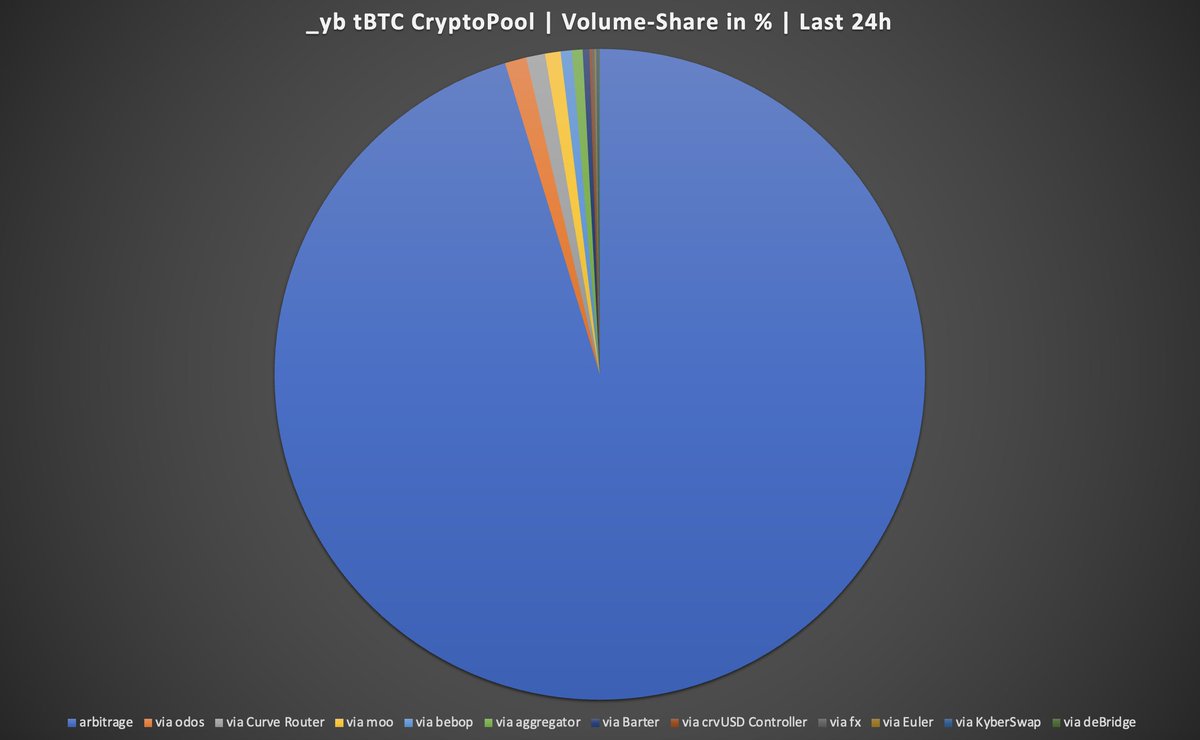

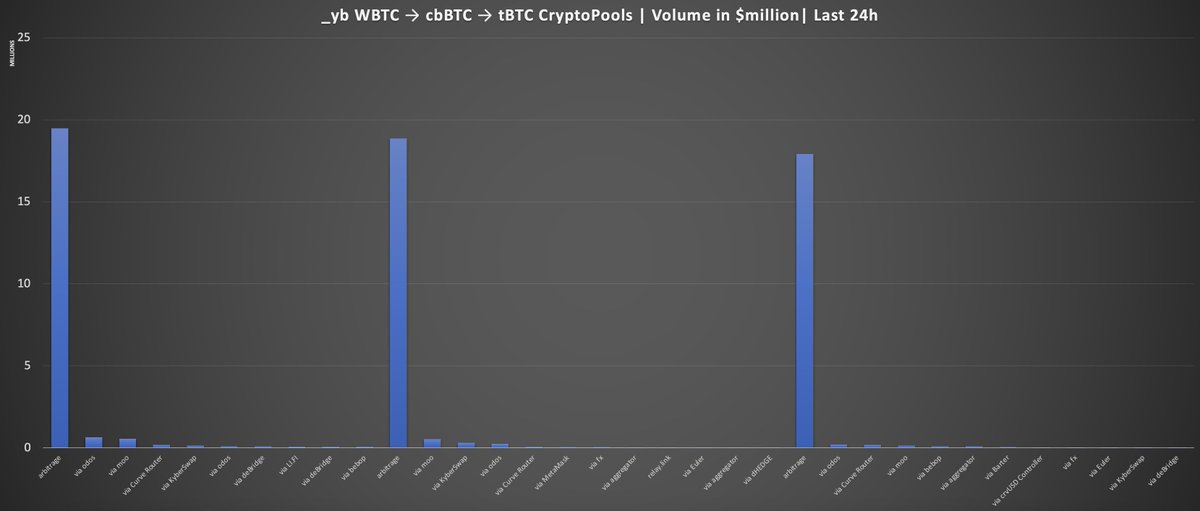

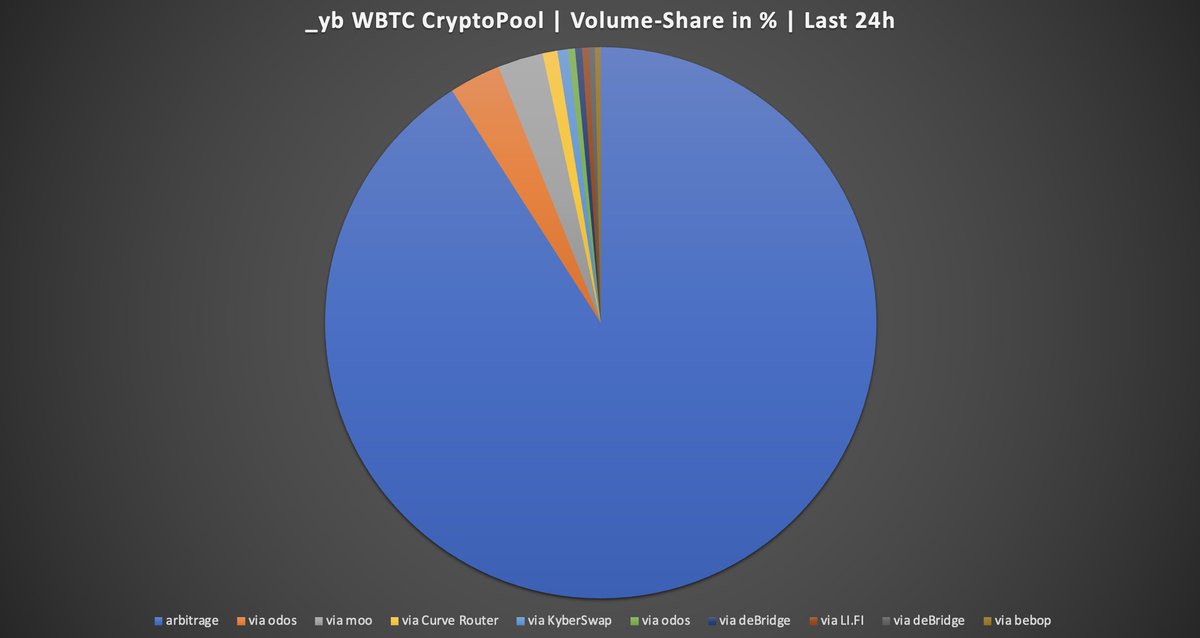

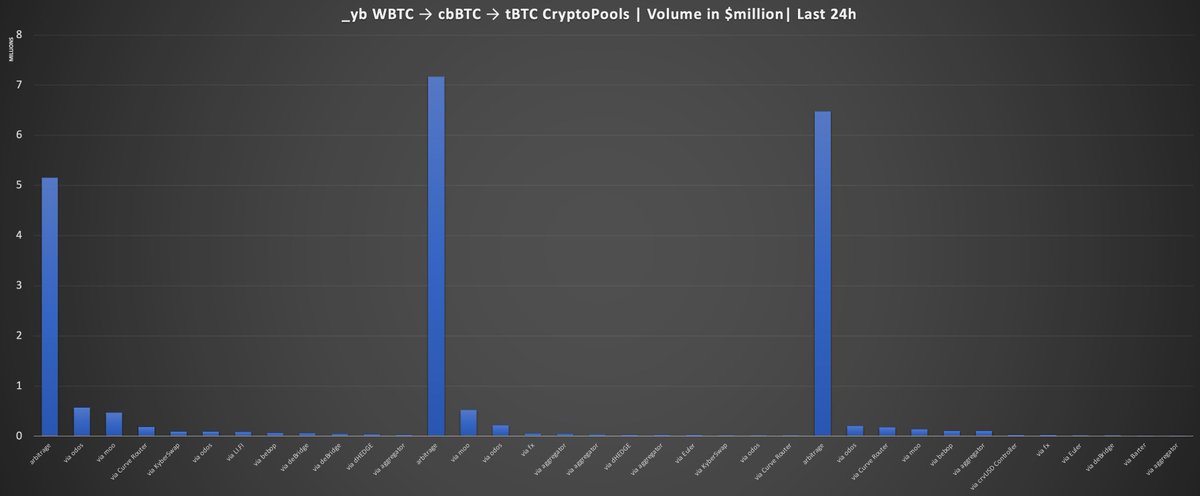

Origin of Volume in the new @yieldbasis CryptoPools at @CurveFinance. Close to 400k$ in combined swap-fees.

4

15

2,026

29 Sep 2025

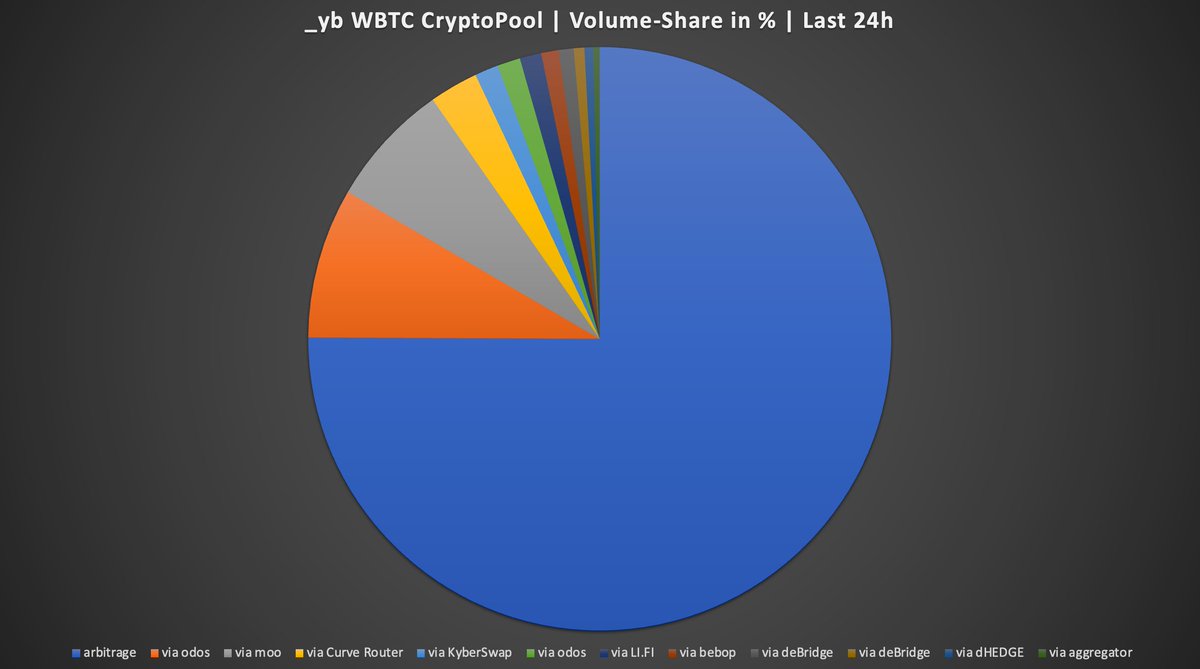

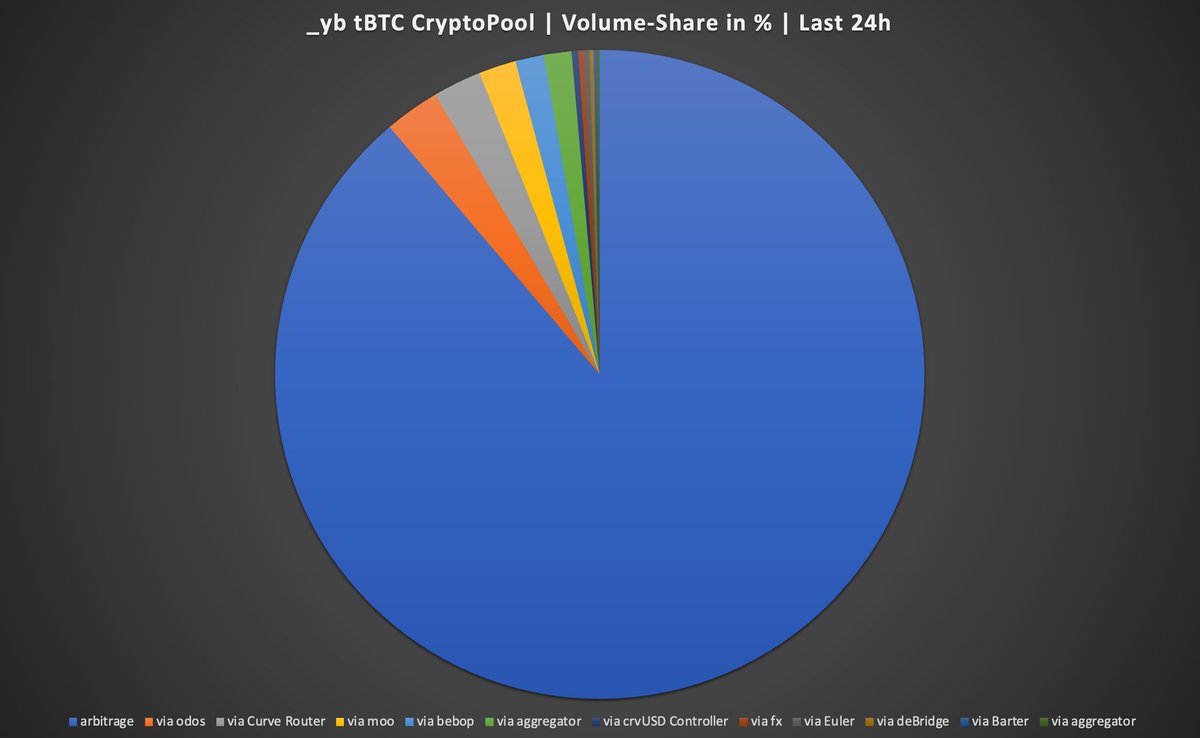

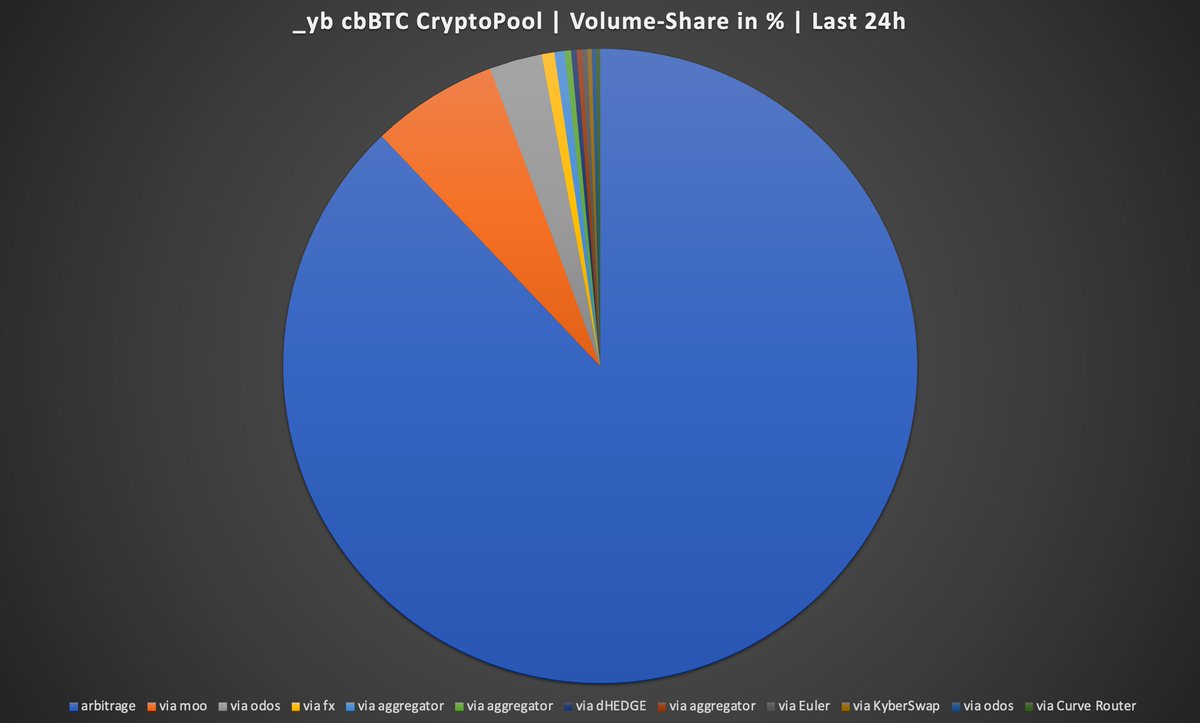

Cryptopools at @CurveFinance related to @yieldbasis are heating up. Looks like all organic volume so far - DEX aggregators and arbitrage

26

35

385

36,961

27 Sep 2025

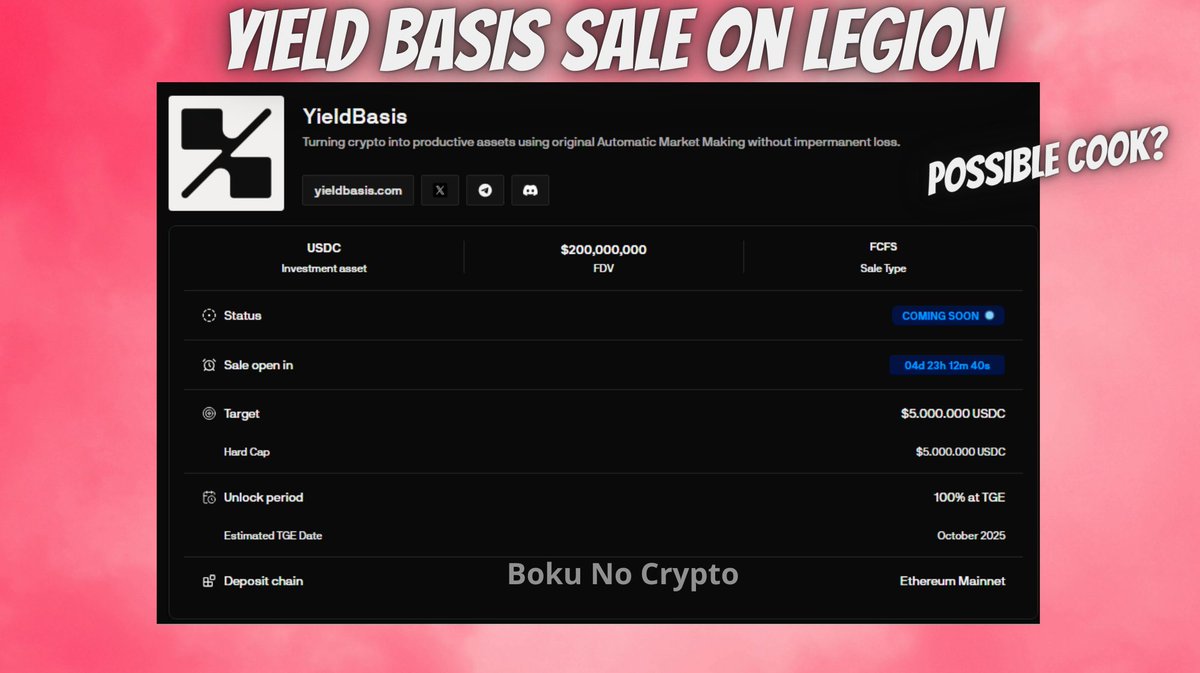

YIELD BASIS SALE POSSIBLE GOOD SALE?

i think is worth make a look on this pre-sale because can be a easy profit.. OBV DYOR and can be a W or a L , for my vibes can be a W with this analysis:

@yieldbasis is a DeFi protocol that aims to eliminate impermanent loss by using an auto-leveraging AMM and specialized cryptopools that maintain constant leverage to convert volatility into yield. It targets BTC/ETH liquidity, publishes technical docs and a research paper, and plans a YB token and protocol emissions.

The pre sale apply will open on 29 September and you will buy at 200M FDV

🔸Why i'm bullish?

- The founder is Michael Egorov (the Curve Finance founder) so he know very well the many problems on defi, and with this project he try solve one of these problems (the impermanent loss problem)

- 100% unlocked at TGE

- Is the first sale from Kraken on legion, you know many times the first time is a cook

- Defi tokens is very good, u saw many defi projects tokens where not was ultra hyped or overhyped, but the token at TGE reached 1B FDV (a example treehouse)

- is already integrated on Curve

- is not for all, but i suggest trying!

🔸How?

- Register on Legion legion.cc?homie=3D93ED95

- Complete the KYC and try connect the best wallet and a good twitter account for get a score

🔸How to be join on the sale?

For the first stage you need apply and write why u wanna join, how much u wanna deposit and a important thing is u need having a better score of 350 on Legion, you need deposit USDC on Ethereum Mainnet!

The team will select and decide if u can participate on the sale, give u a full allocation or partial or nothing

For the second stage

This stage is FCFS and will be on 1 October! If you got declined you can try on FCFS phase, in this sale Kraken users and legion will simultaneously sell the remain tokens!

That's all! personally i will join, and i shared my analysis why, if you think is not worthy you can just skip :)

Good luck!

4

1

15

1,518

19 Sep 2025

Curve Finance community to vote on a $60M proposal to make CRV a yield-bearing asset

The new yield basis would allocate 35%-65% of its value to holders of vote-escrowed CRV, while an additional 25% would be reserved for the ecosystem @CurveFinance

The Curve Finance decentralized autonomous organization (DAO) is voting on a proposal that could open up new income streams for the protocol and its ecosystem.

The proposal, introduced in August by founder Michael Egorov, would establish a $60 million credit line of crvUSD for a yield basis. Voting began on Wednesday, with 97% of votes cast in support of the proposal at the time of writing.

Under the Yield Basis, holders of CRV who stake their tokens would receive veCRV (vote-escrowed CRV) in return, essentially creating income for stakers. Yield Basis would return between 35% and 65% of its value to holders of veCRV, while an additional 25% would be reserved for the ecosystem.

Current voting for the $60 million credit line proposal. Source: Curve Finance

Egorov said the credit line would be enough to create pools for three assets: WBTC

WBTC

$115,428.47

, cbBTC (cbBTC) and tBTC (tBTC).

“In order to get more incentives for Curve ecosystem as well as to pay a fee for having Curve technology (cryptopools) powering its core, Yield Basis makes an allocation equal to 25% of YB which Yield Basis liquidity providers

1

2

78

18 Sep 2025

CRYPTO NEWSWIRE: ORQO Group Launches $370 Million Digital Asset Yield Platform

ORQO Group launched with $370 million, aiming to bridge traditional finance and digital assets. It plans a yield platform for Ripple's RLUSD stablecoin and tokenized real-world assets.

A new institutional asset manager, ORQO Group, has launched with $370 million in assets under management, signaling a significant move to bridge traditional finance with the burgeoning digital asset space.

Headquartered in Abu Dhabi, ORQO’s ambitious plan centers on building a yield platform for Ripple’s RLUSD stablecoin, leveraging the rapidly growing trend of tokenizing real-world assets (RWAs).

ORQO consolidates four distinct entities: private debt specialist Mount TFI, digital hedge fund Monterra Capital, blockchain engineering studio Nextrope, and the MiCA-compliant decentralized finance (DeFi) protocol Soil.

This strategic combination provides both off-chain asset management expertise and on-chain capabilities, positioning the group to become a global on-chain asset manager.

Currently licensed in Poland and Malta, ORQO is seeking further approval in Abu Dhabi, eyeing the Middle East as a crucial hub for regulated digital asset growth.

The firm’s Soil platform is central to its strategy, designed to connect RWA access with crypto capital.

It aims to offer returns on stablecoin deposits from tokenized private credit, real estate, and hedge fund strategies.

This initiative is part of a broader market shift, where traditional instruments like private credit and U.S. Treasuries are being moved onto blockchain networks.

While the RWA market is currently around $30 billion, it is projected to skyrocket to $18.9 trillion by 2033, underscoring the immense potential ORQO is tapping into.

The group plans to open credit pools for RLUSD holders, allowing institutional treasuries and protocol reserves to earn yield, further solidifying the convergence of traditional and digital finance.

#ORQOGroup

#CryptoNews

#DigitalAssets

#YieldPlatform

#RLUSD

#RippleStablecoin

#TokenizedRWAs

#RealWorldAssets

#DeFi

#InstitutionalCrypto

#TradFiMeetsCrypto

#BlockchainFinance

#AbuDhabiHub

#MiCACompliant

#SoilProtocol

#MountTFI

#MonterraCapital

#Nextrope

#PrivateCredit

#StablecoinYield

#CryptoTreasury

#OnChainAssets

#RWARevolution

#DigitalAssetManagement

#HedgeFundTokenization

#BlockchainEngineering

#RegulatedDeFi

#MiddleEastCrypto

#CryptoLaunch

#AssetTokenization

#YieldFarming

#InstitutionalAdoption

#CryptoBridge

#RWAmarket

#StablecoinDeposits

#TokenizedRealEstate

#USDTreasuriesOnChain

#CryptoGrowth

#FinTechInnovation

#DecentralizedFinance

#GlobalAssetManager

#PolandLicense

#MaltaLicense

#AbuDhabiApproval

#CryptoConvergence

#PrivateDebtTokenized

#HedgeStrategies

#CryptoPools

#FutureOfFinance

1

1

166

17 Sep 2025

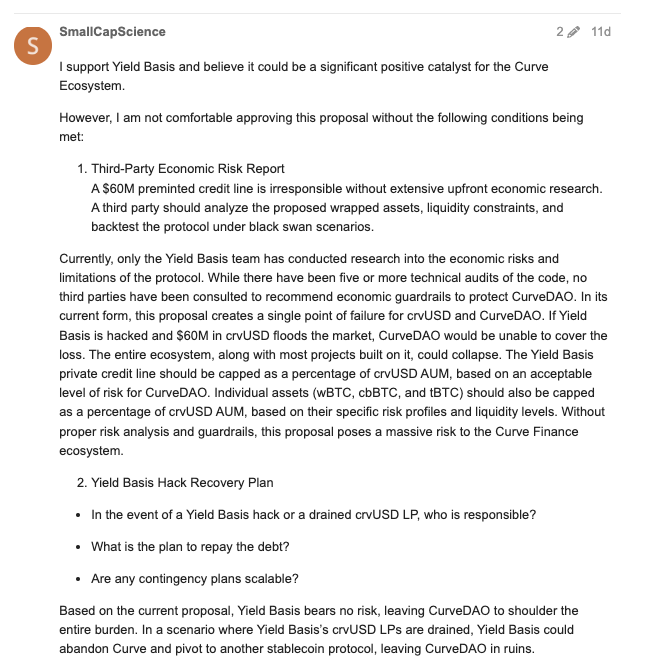

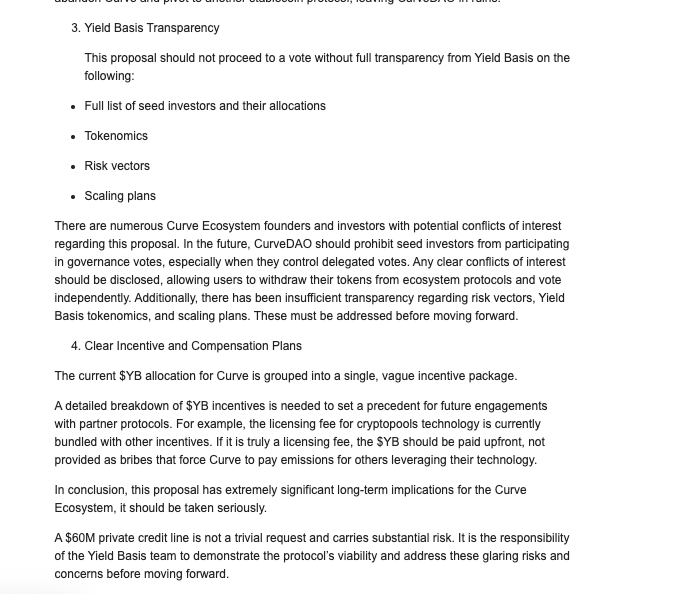

Let me respond to these concerns, as it seems like the Small Cap Scientist did not read the proposal very well.

1. We had 6 audits (and actually 7th ongoing just in case, but looks good). This is exactly because safety is the first priority. As a guard rail, emergency stop of the protocol is given to Curve Emergency DAO multisig. The system was well communicated and studied in advance.

2. If anything happens - of course it'd be on Yield Basis to deal with it to the highest degree possible. The risk though is true for anything new launched tightly integrated with Curve, new Curve products etc, so we did actually more audits than new Curve code usually has just in case.

3. The breakdown of the allocation is added to the proposal. But if anything - it is very natural to invite notable persons from the ecosystem as investors in such a project. If you disagree - you need to lock CRV for veCRV and vote only with those. But I think that partner projects are the strength of Curve!

4. Paying Curve is going to be via allocation controlled by veCRV going as a stream proportional to inflation. It will be only UP TO CURVE DAO to decide how to direct it! If Curve DAO decides to not incentivize crvUSD pools but to use it in any other way - fine, but I think buying votes for crvUSD/stable pools like crvUSD/USDC is the best use here. Cryptopools related to crypto liquidity working for Yield Basis should get no CRV inflation (and there are good economic reasons why)!

17 Sep 2025

The current @yieldbasis proposal is very dangerous for @CurveFinance, I'll be voting "No".

This vote is extremely extractive from CurveDAO and the implications of this vote concern me for the future of the protocol.

My Concerns:

1. Economic Risk -

No third parties evaluated the economic risks of the protocol, only the Yield Basis team.

This credit line should be capped on a percentage basis of $crvUSD TVL. Individual wrapped assets ($wBTC, $cbBTC, $tBTC) and their pools also need caps to prevent systematic risk to $crvUSD.

There are no guardrails at all currently as the proposal was written by Yield Basis.

2. Hack Recovery Plan -

The way this is structured, a Yield Basis Hack is the responsibility of @CurveFinance.

$crvUSD TVL is $250M. If any $crvUSD in the LPs are drained, the balance sheet hole will be too large to fill. The whole $CRV ecosystem would likely go to zero while Yield Basis takes on no liability.

$YB would be free to launch on top of another stablecoin ecosystem the next day leaving CurveDAO with all the $crvUSD debt.

3. Transparency - The Yield Basis seed round participants and their allocations have not been disclosed to CurveDAO.

Devs/Founders from within the ecosystem did not disclose their seed stake in $YB and will be voting with delegated votes.

4. Clear Incentives and Compensation -

$YB hasn't released full details of their tokenomics or incentive systems.

Yield Basis also plans to pay for Curve licensing through bribes. This is a cost to CurveDAO as emissions are paid. They shouldn't be paying emissions on another protocol using their technology.

Conclusion -

This proposal at scale gives $crvUSD a single point of failure that is entirely controlled by a third party protocol (YB).

There are massive conflicts of interest all over this that need addressed. There is also absolutely no excuse for the lack of transparency when requesting a $60M credit line.

CurveDAO needs to protect themselves here first, and Yield Basis should come second.

These requests aren't extremely time consuming and should benefit both parties to discuss.

My concerns were posted 10 days ago to the discussion page, I haven't received any response.

It's worth noting, I will gladly vote in favor of a @yieldbasis credit line if the glaring risks and transparency issues are addressed.

(Discussion Page - gov.curve.finance/t/create-a… )

12

19

137

51,383

15 Aug 2025

New implementation for cryptopools. Very well suitable for several use cases (FX on chain, @yieldbasis)

curve.finance/dao/ethereum/p…

10

27

173

35,707