Jun 12

🌊

Wave-powered #FloatingDataCentres are emerging as one of AI’s most unconventional infrastructure experiments — @DataCentre_Mag

#AIworkloads #datacenterpower #datacenter

👉 datacentremagazine.com/news/…

1

16

Jun 11

800V HVDC Hype vs Reality: Why the Timeline Is More Nuanced (and Delayed) Than the Market Thinks

Convequity’s AI Value Chain scan highlights another area where post-rebound enthusiasm has gotten ahead of infrastructure realities. Similar to CPO, 800V HVDC is seen as closer to commercial readiness than it actually is. For investors, the practical answer right now is mostly no — despite the surface-level “yes.”

Here’s the breakdown:

1. Rubin’s 50V DC Preference Remains KeyNVIDIA’s Rubin platform still backs 50V DC input for the compute tray. This forces an extra layer of conversions if you’re pushing 800V from the grid.

2. Solid State Transformers (SST) Lag on Medium VoltageCurrent SiC-based SST production is LV-focused. No meaningful MV SST support yet. Result for customers:

Step down MV grid (13.2–20kV) → 400/415V AC

Then LV SST → 800V DC

Then another step-down to 50V DC for the tray

That’s an inefficient round of step-down/step-up/step-down. Not ideal.

3. The Ideal Direct Path Is 2 Years AwayMedium Voltage SST that goes grid → 800V DC → compute tray directly is still early. Hyperscalers won’t flip the switch overnight.

4. Bipolar 400V Architecture Is the Faster On-RampHyperscalers already have mature bipolar ±400V designs via OCP. Chinese operators have been running 400V variants for years. This path is quicker and lower-risk — especially for customer ASIC clusters.

Second-order winner: Further amplifies $GOOG TPU efficiency edge and $AVGO ASIC momentum.

Bottom line: 800V has real long-term potential but the near-term infrastructure bottlenecks and existing 400V momentum mean the market is pricing in speed that isn’t fully here yet. We continue to track the SST and power conversion resolver timeline closely in our framework.

What stands out to me is how often these power architecture debates echo the optical side — the “obvious” upgrade takes longer in practice.

#AIInfra #DataCenterPower #Semiconductors

3

26

3,728

Jun 10

🇨🇳 China’s World-First AI-Power Island: Prefabricated Power for AI Data Centers

Modern prefabricated power supply station in Qingdao, built like modular building blocks. This container-style “AI-Power Island” was assembled on-site in just five months (nearly 70% faster than traditional methods). It is designed specifically to power AI data centers and can reduce electricity cost per AI token by around 30%. Sleek industrial design with green accents, ready for rapid deployment.

#ChinaAI #AIPowerIsland #DataCenterPower #ChinaTech #Qingdao #AIInfrastructure #ChinaInnovation #PrefabricatedConstruction

Apr 28

🇨🇳China Plans World’s First Orbital Data Center Constellation

Beijing startup Orbital Chenguang secured $8.4 billion in credit lines from 12 major Chinese banks to develop the world’s first large-scale orbital data center constellation in sun-synchronous orbit.

The satellites will harness constant sunlight for power and use the vacuum of space for natural cooling. The ambitious project aims to deliver over 1 gigawatt of computing power by 2035 to support AI workloads, addressing Earth’s constraints on energy, land, and cooling.

Date: April 2026

Source: Xinhua / China Daily / Orbital Chenguang

#OrbitalDataCenter #ChinaSpace #SpaceDataCenter #OrbitalChenguang #AIinSpace #SpaceComputing #ChinaTech #GigawattAI #FutureOfAI #SpaceEconomy

3

11

796

Jun 9

$SRE surged 4.0%, $CECO followed suit with a 17.6% gain, $FLNC saw a significant rise, and $FIX also gained momentum.

Bullish rationale: Explosive growth in data center power demand, record-high backlogs for advanced energy storage solutions, and policy and technological support are creating a powerful synergy.

Culmination Market Sentiment (Peak): Every AI computation requires stable power—companies like $SRE are the unsung heroes behind the scenes! The synergy between AI and renewable energy has sent market sentiment surging like an electric current!

#SRE #CECO #EnergyStorage #AIEnergy #Renewables #DataCenterPower #GridTech

87

Jun 9

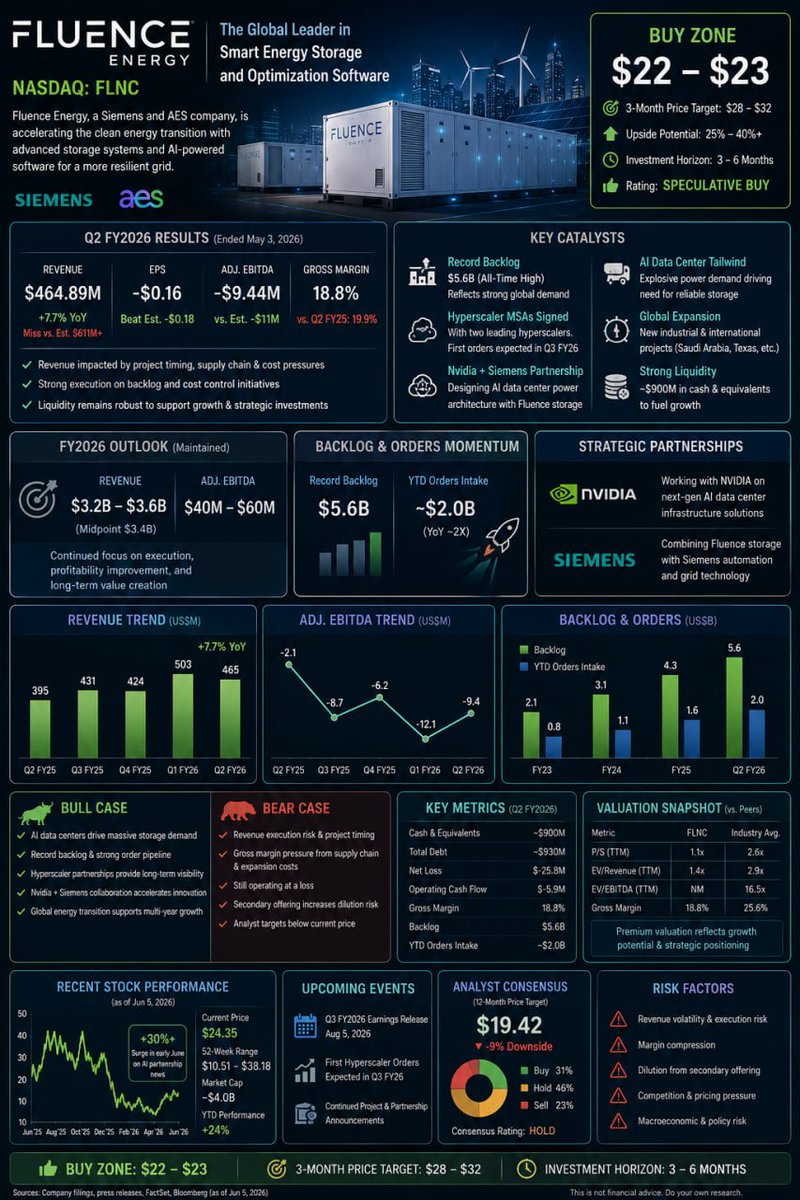

$FLNC: A global leader in smart energy storage systems and optimization software (a Siemens AES joint venture), deeply benefiting from the surge in power demand from AI data centers, grid stability, and renewable energy integration.

Q2 FY2026 (reported May 6): Revenue $464.89M (YoY 7.7%, significantly below expectations of $611M ); EPS -$0.16 (beat consensus of -$0.18); Adjusted EBITDA -$9.44M. Full-year guidance maintained: revenue $3.2–3.6B (midpoint $3.4B), adj. EBITDA $40–60M.

Key catalysts:

Record backlog $5.6B (historical high); YTD order intake ~$2.0B (doubled YoY); signed Master Supply Agreements (MSAs) with two major hyperscalers, First order expected in Q3; collaboration with Nvidia and Siemens on AI data center architecture design drove a >30% stock surge in early June.

Other: secondary share issuance (to increase float), addition of AES executive to the board; industrial/international contracts (e.g., Saudi Arabia, Texas). Early Q1 saw a sharp drop after missing revenue and shrinking margins, then rebounded as the AI/energy storage theme warmed up.

Key reasons:

Positives: AI data center pipeline surge, record backlog, hyperscaler MSA, Nvidia collaboration, ample liquidity (~$900M).

Headwinds: historical revenue misses, gross margin pressure (supply chain/expansion costs), still unprofitable, analyst price targets below current price, dilution pressure from secondary offering.

Buy point: $22-23

#FLNC #AIEnergy #EnergyStorage #DataCenterPower #NvidiaEnergy #Renewables #SemiconductorPower

1

2

496

Jun 9

$FLNC Shines a Light of Stability on AI Data Centers

Key Event: $FLNC signs an expanded supply agreement with a hyperscaler, setting a new record for its order backlog.

Bullish Rationale: Surging AI power consumption is creating grid bottlenecks; advanced energy storage combined with intelligent software offers the perfect solution, while endorsements from Siemens and AES ensure strong execution capabilities.

Conclusion & Market Sentiment (Climax): Every AI operation requires reliable power—$FLNC is the unsung hero! The synergy of AI and renewable energy themes has fully ignited market sentiment!

Risk Warning: Uncertainties remain regarding project execution and gross margins; we recommend closely monitoring financial reports for verification.

#FLNC #EnergyStorage #DataCenterPower #AIEnergy #Renewables #GridTech #CleanEnergy

1

2

320

Jun 8

$GLXY Galaxy Digital

Galaxy Digital jumped over 21% today, fueled by AI data center momentum at its Helios campus and broader crypto market recovery. Strengths center on its diversified digital asset and compute infrastructure business, with major power capacity deals supporting revenue growth. Digital assets / financial services & AI infrastructure sector. Interesting for trend followers — positioning at the intersection of crypto and AI compute makes it worth monitoring amid sector tailwinds.

#GalaxyDigital #GLXYRally #AICrypto #DataCenterPower #DigitalAssets #HeliosCampus #CryptoRebound

1

108

Jun 8

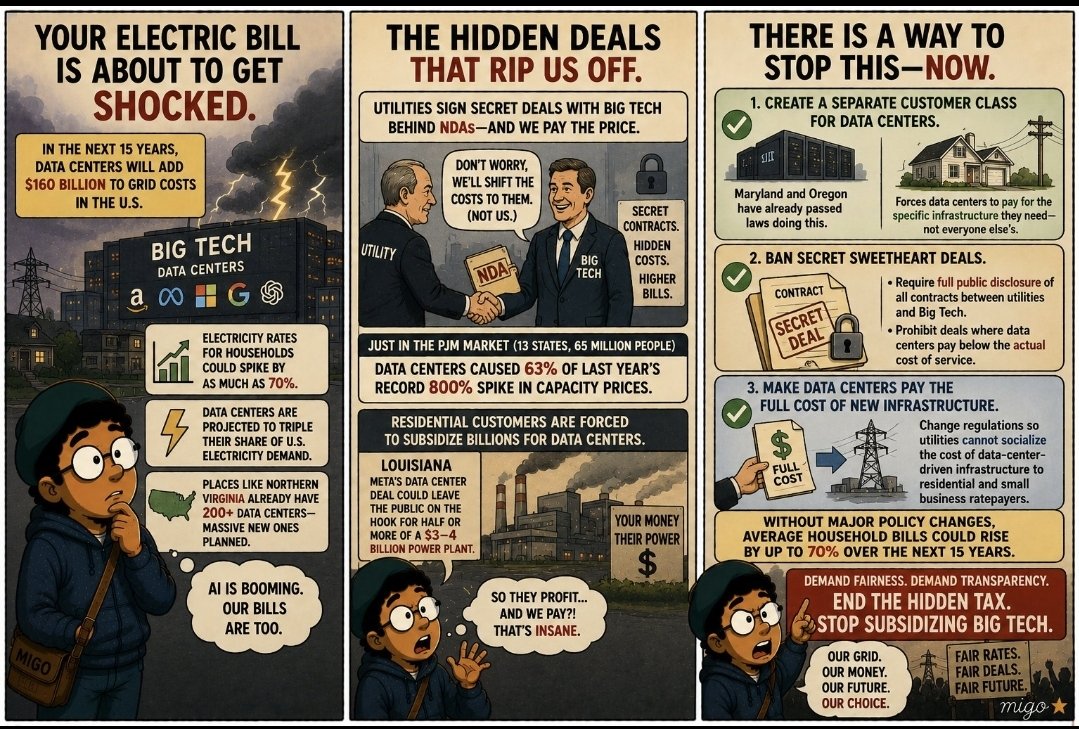

Imagine opening up your power bill and it went up 26%! DUE to AI DATA CENTERS!

We saw the possibility of gold rush mentality decisions with the AI build out, but not like this!

#DatacenterPower #datacenters #water #Australia #AI #FAI

dailymail.com/news/article-1…

40

Jun 8

Well we warned about this for 3 years. The total lack of consideration for local communities in the way of water use and electricity, shows the greed and tone deaf nature of a gold rush bubble.

Oh, and people’s power bill soaring as a result was the kicker.

dailymail.com/news/article-1…

#DatacenterPower #datacenters #water

36

Jun 7

US data center construction YTD $49.5B — strong but 50% of 2026 plans risk delay/cancel from grid/transformer shortages. Key for power systems engineers. #DataCenterPower

11

#DataCentreLive:

The London Summit revealed an industry being pushed to evolve on every front at once, including grid strain and cybersecurity fears — @DataCentre_Mag

#datacenterpower #talentshortages #sustainability #datacenters

👉 datacentremagazine.com/news/…

1

3

64

Attempted justification for AI Data Centers. Only employment is building them. Nobody said why thousands of Surveillance Units being built over US. AI designed to take jobs. Who pays taxes after robbed population? #DatacenterPower #datacenters #artificial

3

5

131

May 31

And that's when I realized...

Exicom may not remain just an EV charging company.

It is quietly expanding into:

⚡ #BatteryStorage

⚡ #DataCenterPower

⚡ #DCMicrogrids

⚡ #TelecomInfrastructure

⚡ #EnergyManagement

#EnergyTransition #CleanEnergy #BESS

1

2

162

Is the biggest threat to the nuclear renaissance a lack of private capital, or a supply chain that simply isn't ready to deliver?

#NuclearBusiness #NuclearRenaissance #CleanEnergyInvestment #EnergyTransition #DataCenterPower #NuclearSupplyChain #EnergyMarkets #NetZeroInfrastructure #EnergyPolicy #CleanTech

1

3

4

94

If we want to scale small modular reactors (SMRs) fast enough to meet AI data center demand, should we focus on harmonizing global regulation or building standard, mass-produced factory lines first?

#NuclearBusiness #SMRs #CleanEnergyInvestment #NuclearRenaissance #EnergyTransition #DataCenterPower #NuclearRegs #NetZeroInfrastructure #EnergyMarkets #PoweringAI

2

2

4

153

How much are we willing to pay for regulatory delay before realizing that a standard, factory-built reactor is the only way to fund the clean energy grid of tomorrow?

#NuclearBusiness #SMRs #CleanEnergyInvestment #NuclearRenaissance #EnergyTransition #DataCenterPower #NuclearRegs #NetZeroInfrastructure #EnergyMarkets #PoweringAI

1

4

182

May 30

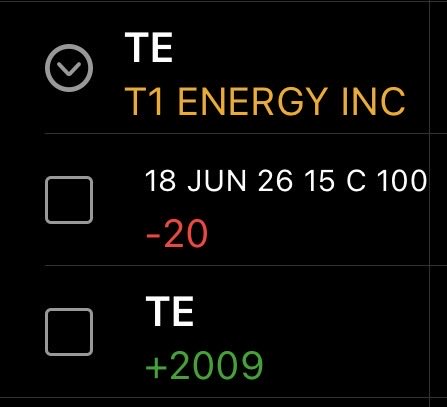

$te expecting to roll out and up over and over and over 🤑 #datacenterpower #datacenter $iren $cifr $keel

2

1,134

May 30

Sorry, but this intimidation is not gonna work. So basically you can burn down cities in protest like an ICE or Floyd protest and no consequences, and they think people are going to back down after peacefully protesting over concerns about data centers effects on communities like with power, water and quality of life???😂

This is America? We’re coming up on our 250 year anniversary and corporate government minions, think this approach will work rather than hearings and get togethers out concerns??

We’ve been saying this for three years that not every location is good for a data center!!

Some locations are fine, some are not. How is this even something controversial?

#aidatacenters #DatacenterPower

4

2

12

671

May 30

China has deployed underwater data centers, a commercial subsea facility off the coast of Hainan and off the coast of Shanghai

By leveraging cold seawater for cooling rather than HVAC systems, these facilities cut power consumption by up to 30%

🇨🇳

#China #DatacenterPower #Energy

3

104

I see a lot of crying about data centers of late, I always liked TNG #DatacenterPower #datacenter

1

2

35