$EEGI — Valye Company Analysis

Eline Entertainment Group, Inc. (EEGI) transitioned from business abandonment and court-appointed custodianship in 2022 to a developmental-stage entity focused on sourcing merger or acquisition opportunities. The company currently has no re

Key points:

• EEGI has operated with zero revenue since 2022 following operational abandonment and subsequent custodianship intervention.

• Persistent operating losses and negative cash flows have worsened annually, with operating income declining by roughly 26% year-over-year in 2025.

• Liquidity is severely constrained; cash balances are effectively nil with current liabilities exceeding current assets, producing a zero current ratio.

• The company operates as a developmental-stage entity focusing exclusively on identifying merger or acquisition targets but lacks any active agreements or firm plans.

• Control rests with a majority shareholder holding preferred shares with enhanced voting rights, influencing governance post-custodianship.

Read: valye.com/news/eegi-company-…

#ValyeAI #Stocks #StockAnalysis #StocksInFocus #EEGI #StockMarket #Finance #MergersAndAcquisitions #DevelopmentStage #CorporateRestructuring

2

5

804

Mar 31

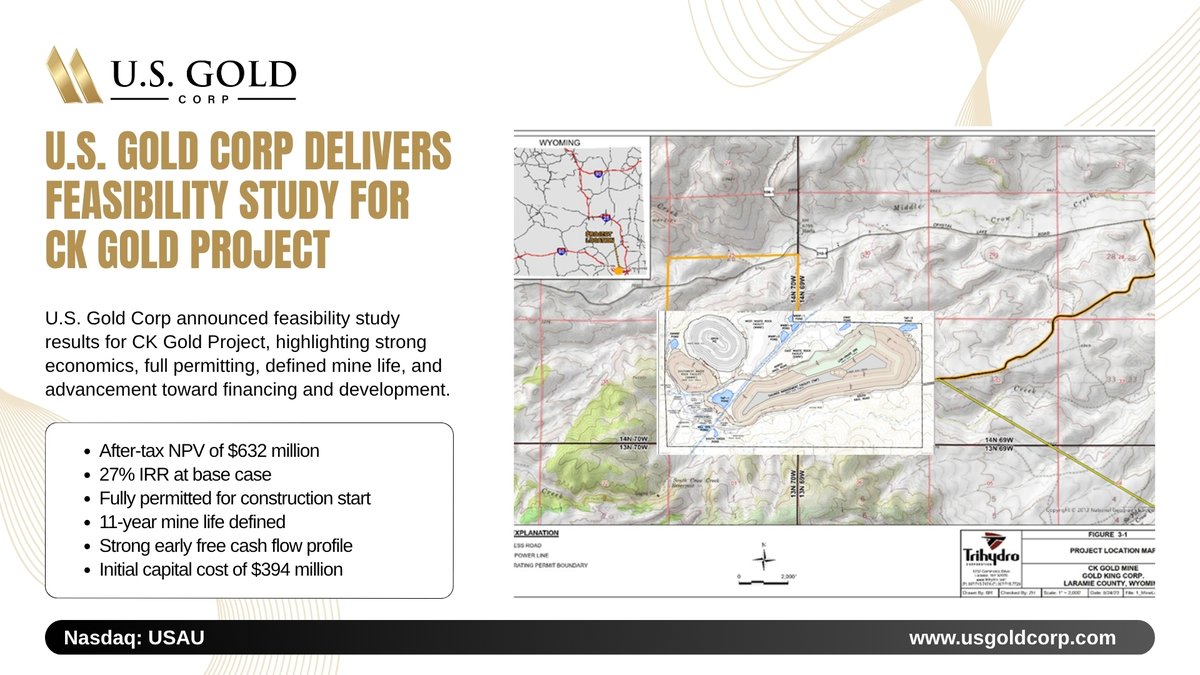

U.S. Gold Corp. ("US Gold" or the "Company") (NASDAQ: USAU) is pleased to announce the results of its Feasibility Study (the "FS") for the development of its wholly-owned CK Gold Project ("CK" or the "Project"), located in southeast Wyoming 20-mile from Cheyenne.

George Bee, President, CEO and Director of U.S. Gold Corp. commented

The Feasibility Study is the culmination of 5-years of work to engineer and permit a U.S. domestic project ready for immediate development. CK is one of the most compelling, resilient, and capital-efficient copper-gold-silver projects in the U.S. ready for development.

Read More - usgoldcorp.com/news-media/pr…

#usau #usgold #usgoldcorp #ckgold #feasibilitystudy #goldproject #coppergold #silver #wyoming #miningstocks #goldstocks #resourceinvesting #preciousmetals #miningnews #developmentstage #minefinance #projectdevelopment #northamericanmining #commodities #stockmarket #investing #juniorminers #growthstocks #miningdiscovery

7

113

18 Jun 2025

$TERN

Attached is page 1 of a 6-page Oppenheimer analyst report on TERN issued today entitled:

"ELVN-001 TERNs the Spotlight to '701"

Oppenheimer has an 'Outperform' rating on TERN with a $20 price target.

Oppenheimer's 'Summary' regarding TERN in the report includes the following:

"In light of recently reported Ph1 ELVN-001 data presented at EHA, we wanted to share our perspective on implications to TERN-701.

Bottom line, while updated Ph1 efficacy of ELVN-001 appears promising, we believe the commercial opportunity for TERN-701 persists, given the multi-billion dollar CML market and '701's emerging profile vs. ELVN-001 and asciminib, including:

1) positive signals of safety, with no reported AE-related discontinuations in '701's interim readout;

2) specifically targeting the ABL myristoyl pocket (STAMP) inhibition compared to ELVN-001's active-site mechanism;

3) enhanced DDI profile; and

4) greater dosing convenience relative to asciminib.

Efficacy focus remains on '701's 6-mo. MMR readout on track for 4Q25, as we expect this clinical endpoint to have meaningful read-through to '701's pivotal trial and contextualize its differentiating features.

-- PRICE TARGET CALCULATION:

We value TERN with DCF methodology assuming a 12% discount rate, reflecting risk that we believe is associated with a developmentstage biotechnology company, and a -5% terminal value growth rate based on assumed patent expirations beyond 2039, driving our 12-18 month PT of $20. We forecast risk-adjusted peak total revenues of ~$2.7B in 2038.

KEY RISKS TO PRICE TARGET:

■ Clinical efficacy: TERN’s therapeutic pipeline fails to meet the clinical efficacy endpoints for its program in CML and obesity.

■ Clinical safety: A safety signal emerges from clinical studies of TERN’s pipeline therapies.

■ Manufacturing risk: Manufacturing issues could hinder regulatory approval or limit penetration of the commercial market.

■ Regulatory risk: Regulators raise additional requirements or concerns around development, delaying or preventing regulatory approval.

■ Commercial/competitive/reimbursement risk: Competitive pressures from development assets could lower market potential for the therapeutics in TERN’s pipeline. Negotiations with payors could limit market opportunity of the company’s therapeutic pipeline.

■ Financing: TERN may require additional funds to conduct additional studies or commercialize the company’s pipeline therapies.

Note: We see TERN, as a stock trading under $5, as speculative and appropriate for risk tolerant investors."

(Page 1 is not available here as X does not allow me to post pages from reports on this platform)

2

535

Today we are finaly releasing the news of what we have been on to expand Blogchain and help this sector grow.

We are working on our own crypto/trading AI interface that will assist crypto traders on gathering news, trail your stop loss/profit taker, place trades that you set in the future if it hits certain parameters, automate the creation of tokens… and much more.

It will be the best tool for all traders that want to engage in the market in the most efficient way possible.

Hope you are excited about the future,

We are!

Blogchain team

#AI #Developmentstage #crypto #trading #bot #devs #stockmarket #blogchain #blockchain #blockchainAI

1

1

4

2,955

19 Jul 2024

Big fker isn't he the boy, he must be the postman's 🤔🤣

He needs to carry the muscle he's put on 💪🏾

#Developmentstage ✅

5

32

1,443

Aaannnnd another one: Guido joined the team as a Development Intern 👋

#developmentintern #internship #frontenddevelopment #development #team #intern #stage #developmentstage #stagiair

3

542

#IoT-focused #CyberAttacks have occurred in 82% of healthcare organizations…

Even Captain Obvious would say that #VulnerabilityManagement should be integrated into the #DevelopmentStage.

Find out how in our new blog post: bit.ly/3lcHGEw

2

15 Feb 2021

#screenwriting some interviews for #VampThrapy. I finished Vlad and Danté. Now on to one of our females: Illyandra. #filmmakerlife #Filmmaking #LuckeyBomFilms #wearingmorethanonehat #Director #actorslife #DevelopmentStage

3

7 Feb 2021

Getting a meeting going, working on projects. #filmmakerlife #Filmmaking #LuckeyBomFilms #wearingmorethanonehat #Director #actorslife #DevelopmentStage #TheDriver #VampThrapy #Death2Cupid

2

18 Jan 2021

How to Kick Off a Film: Where Do You Start?

Well, it’s different for all of us, but here are some things to think about...

(studentfilmmakers.com/how-to…)

#Filmmaking #StagesOfFilmmaking #DevelopmentStage #PreProductionStage #FilmProduction

3

18 Jan 2021

Development Phase: Our Roadmap

As elementary as it sounds, defining who, what, where, when and how becomes the very foundation to a successful project.

(studentfilmmakers.com/develo…)

#Filmmaking #StagesOfFilmmaking #DevelopmentStage #LearnFilmmaking

4

17 Jan 2021

meeting at the #BrandingRoom tonight. We're heavily discussing things about #VampTherapy. I'm still finishing my second draft. #filmmakerlife #Filmmaking #LuckeyBomFilms #wearingmorethanonehat #Director #actorslife #DevelopmentStage @goldenaphoto

2

11 Nov 2020

#MobileAppDevelopmentChecklist!

Here's the #mobileappdevelopment life cycle guide which should be easier for you to plan the #budget and make crucial decisions as your #app enters each #developmentstage.

dotcominfoway.com/blog/compr…

#DotComInfoway #DCI #AppDevelopmentGuide

3

2

23 Oct 2020

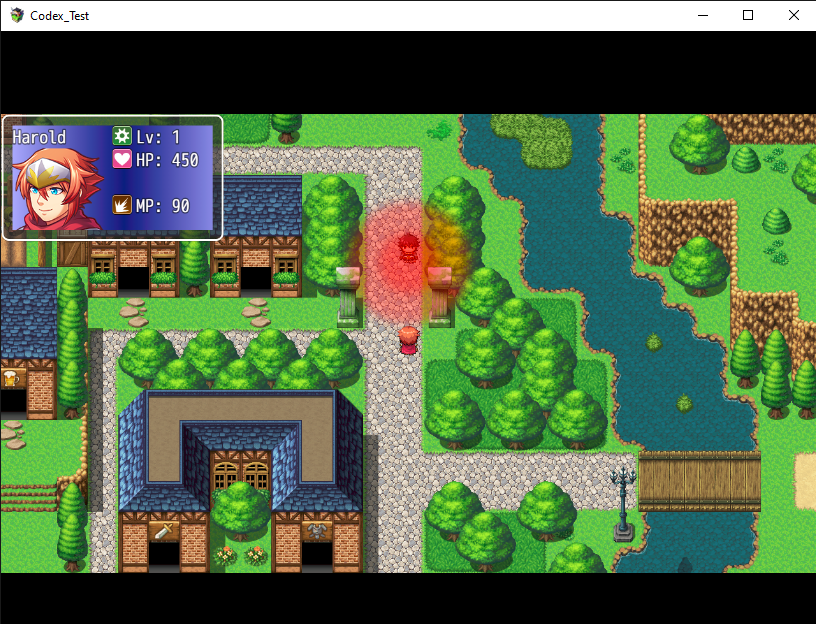

Soft red light centered on event. Lighting system more or less complete. Just a few tweaks to go regarding blends.

Now for the map environment behavior...

#rpgmaker #indiedev #gamedev #ProjectHaven #DevelopmentStage

1

5

4 Mar 2020

#LifeHappens update: I'm on page 74 written out by hand. That's going from the last printed draft, page 39. So much has been added through my #screenwriting and I'm finishing an emotional scene. #LuckeyBomFilms #filmmakerlife #DevelopmentStage

2

1

3

24 Oct 2019

"Paling utama apabila mereka kekal bermotivasi, yakin dan berani terutama ketika penguasaan bola. Ia mgkin tidak memberi keputusan skg, tp kami percaya mereka akan lebih baik utk 2,3 tahun akan dtg." - nzr

#developmentstage

#believeinprogress

#trusttheprocess

23 Oct 2019

DISASTER FOR BELIA @FASelangorMy AS THE CLOCK HEADS TO FULL TIME!

At the last minute, Belia Selangor scored a comedic own goal! It's 1-0 to MBSA FC!

#BELSELvsMBSA

#SCL2019

#LigaUntukJuara

#EarnedNotGiven

#FootballSelangor

3

6

28 Sep 2019

#DidYouKnow @Sobantwana01 started off at the #DevelopmentStage at the #jazzyjoburgmarket last year! A great way to promote and empower artists is what we aim for as #SBJOJ22.Catch her now as she goes on! #JazzUnleashed #LiveTheMusic #SBJOJ22 @StandardBankArt #SBYA @jazzcorner

6

4

30 Jul 2019

#womenintech Update:

The lesson on creating forms in JavaScript was challenging.

With support from @Sir_BrianAO and extra practice hours, our #womenintech will pull through. Definitely.

#WomenWhoCode

#100daysofcode

#javascript

#softwaredevelopment

#UWAT2019

#DevelopmentStage

6

12

29 Jul 2019

To gain sales, Business Founders need to find their customer.

This procedure requires strategy in Business Development.

Photos from both Morning & Evening sessions @iSpaceGh.

#WomenInBusiness

#UWAT2019

#DevelopmentStage

4

14