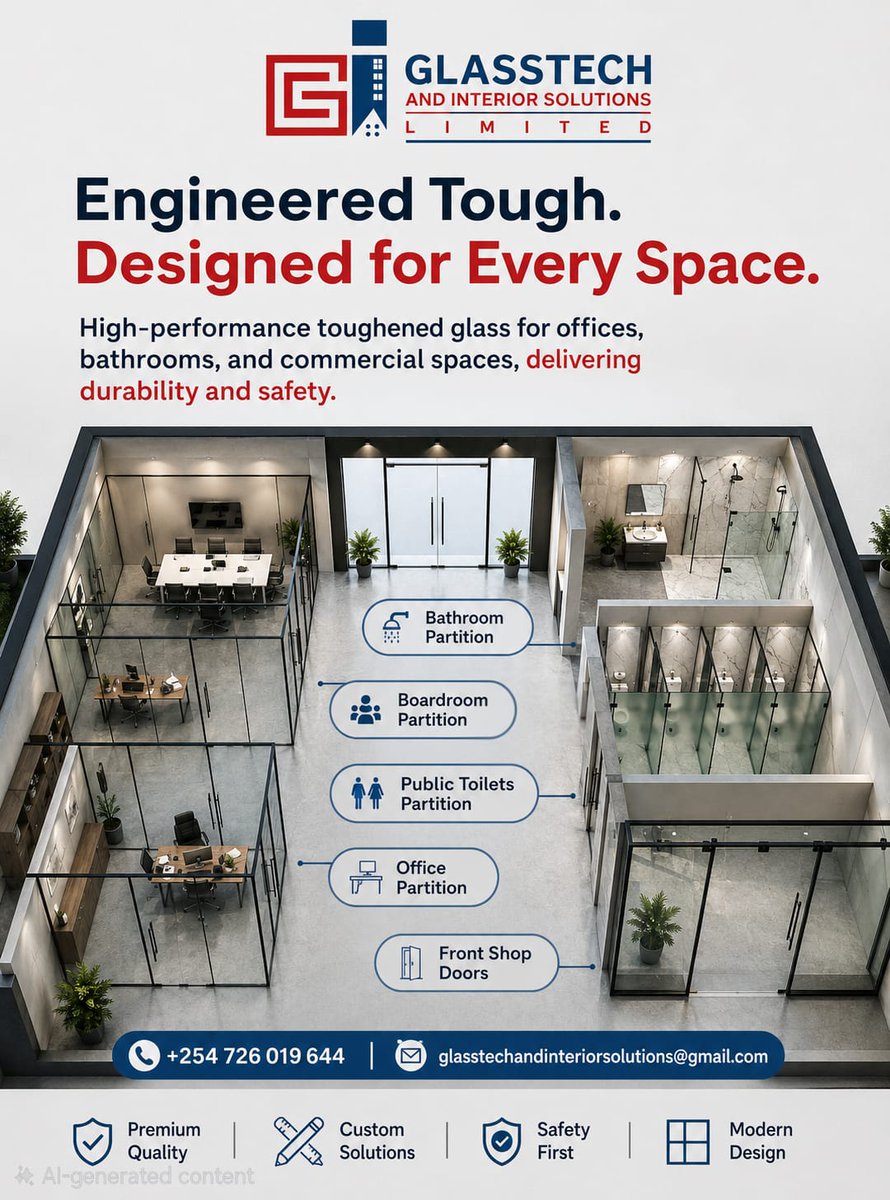

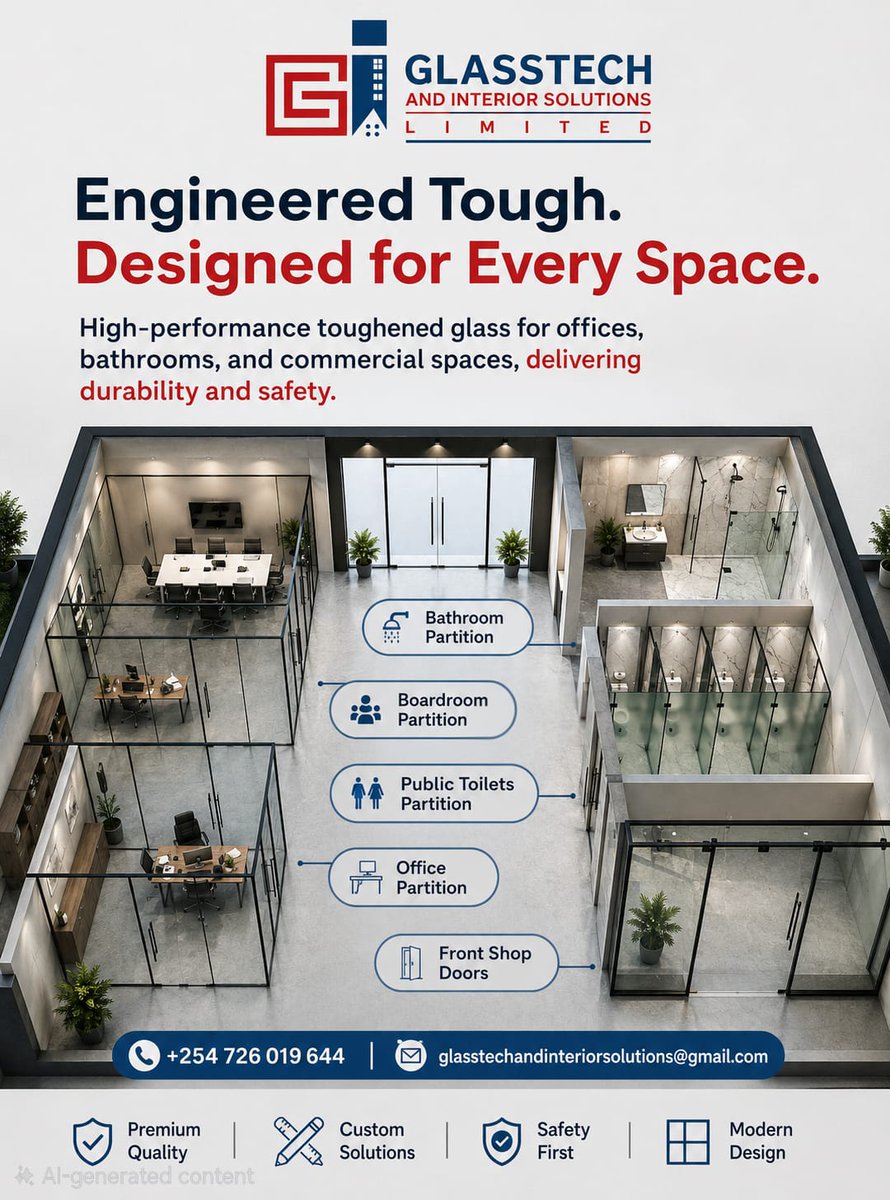

Building? Renovating? Upgrading?

Don't compromise on quality.

At Glasstech, we create modern spaces with: 🔹 Aluminium Windows & Doors 🔹 Frameless Showers 🔹 Glass Partitions 🔹 Autoglass Solutions

Professional workmanship. Lasting results.

📲 WhatsApp 0726 019 644 for a free consultation.

19

May 26

Modern spaces require materials that combine durability and style and premium glass installations are becoming a preferred choice for offices and homes.

Glasstech provides these solutions. Contact 0726019644

Install POS ERP Etims. Get RobiVisitor App. #RobisearchSMEimpact

7

138

May 26

If you're remodeling your corporate office, open plans are out and sleek glass divisions are in. Glasstech handles everything from premium boardroom partitions to custom office setups that look incredibly sharp. Get POS/eTims #RobisearchSMEimpact Get RobiVisitor App

9

125

May 26

Engineered for strength and designed for elegance. From office partitions to modern shower cubicles, Glasstech delivers premium glass solutions built to last. Call 0726 019 644. Get POS/eTims #RobisearchSMEimpact Get RobiVisitor App

1

41

🚨 TOP 20 STOCKS THAT ABSOLUTELY CRUSHED Q4 FY26 🚨

A thread you CANNOT afford to miss if you're serious about markets 🧵👇

1/ 🟢 BHAGYANGR

46.3% revenue growth (guided 35-40%) 258% PAT surge ₹59 Cr CFO

Copper demerger on June 9th = massive catalyst incoming 🔥

2/ 🟢 NAVINFLUOR

992 bps margin expansion (crushed 28-30% guidance)

Debt/Equity now just 0.31x — this company is on a DELEVERAGING beast mode 💪

3/ 🟢 ETERNAL

Revenue nearly TRIPLED 📈 ( 196.4%)

Quick Commerce: ₹265 Cr PROFIT vs ₹82 Cr LOSS last year

625.7% YoY growth. Read that again. 🤯

4/ 🟢 TIPSMUSIC

92.9% PAT growth 🎵

Beat 20% guidance by 10 FULL POINTS

Content costs at 10.2% vs 18% guided limit — insane capital discipline

5/ 🟢 ACUTAAS

33% revenue growth 35.87% EBITDA margin (guided 28-30%)

CWIP surged 155% — capacity explosion is coming 🏭

6/ 🟢 CGCL

PAT of ₹9,491 Mn — beat guidance by 11.7%

ROE hit 16.49%... FY28 TARGET achieved in FY26 ⏰

2 years AHEAD of schedule. Wow.

7/ 🟢 SMARTWORKS

First FULL YEAR of profitability ✅

440 bps margin expansion

Crossed 10 MILLION sq ft operational portfolio 🏢

8/ 🟢 PHOENIXLTD

EBITDA margins at 60.8% vs 56-57% guidance 🏆

Residential segment surged 122.3% YoY

Mall housing = unstoppable combo 🔥

9/ 🟢 EQUITASBNK

PAT grew 405% YoY 🚀🚀🚀

Provisions DROPPED 52%

GNPA: 2.60% | NNPA: 0.72%

All universal bank license criteria: ✅ MET

10/ 🟢 STLTECH

Enterprise/Data Center mix hit 36% (target was 30%) 📡

Turned PAT positive at ₹59 Cr

The strategic pivot is WORKING

11/ 🟢 TMB

Advances grew 20.78% vs 16% guidance

GNPA at multi-year LOW of 0.73% 📉

Quiet, consistent, and completely underrated 🤫

12/ 🟢 AURUM

₹505.4 Cr annualized ARR — target achieved ✅

91% DEBT REDUCTION — effectively debt-free 💰

1740 bps EBITDA margin expansion. Monster quarter.

13/ 🟢 VEDL

FY26 EBITDA beat guidance by 12% 🏅

Aluminum margins 1600 bps

Power segment EBITDA surged 365% ⚡

14/ 🟢 CHENNPETRO

PAT grew 1349% 🤯🤯🤯

GRM more than doubled to $9.28/bbl

Throughput at 111.5% CAPACITY UTILIZATION

Refining is back, baby 🛢️

15/ 🟢 CHOICEIN

PAT 39.1% (guided 25-30%) ✅

EBITDA margins beat guidance by 620 bps

Broking segment grew 110% 📊

16/ 🟢 ATUL

Life Science Chemicals margins expanded 921 bps 🧪

Free cash flow: ₹847.90 Cr

Virtually DEBT-FREE balance sheet

Turnaround of the year candidate 🏆

17/ 🟢 INFOBEAN

30.1% revenue growth vs mid-teen guidance 💻

PAT MORE THAN DOUBLED

Cash conversion ratio: 1.22x — quality earnings 💎

18/ 🟢 CEATLTD

PAT 47.7% — crushed double-digit guidance 🚗

D/E conservative at 0.60x

Dividend INCREASED by 350% 🎉

Tyre sector quietly printing money

19/ 🟢 FEDFINA

AUM growth 22.9% vs 12-15% guidance 🏦

Credit costs: 0.89% (well-controlled)

PAT grew 52.6% YoY

20/ 🟢 SEJALLTD

Glasstech hit EBITDA break-even 🪟

D/E collapsed from 4.16x to 0.99x via ₹94 Cr equity raise

Turnaround CONFIRMED ✅

🏁 SUMMARY THREAD:

✅ Guidance beats across revenue, margins & PAT

✅ Deleveraging stories picking up pace

✅ Turnarounds confirming in multiple sectors

✅ FY27 looks STRONG for these names

If this thread added value: Like, RT and comment your thoughts on the same.🔁

Follow for more data-driven market insights 📊

⚠️ NOT INVESTMENT ADVICE. Do your own research. Past performance ≠ future returns.

#StockMarket #NSE #BSE #IndianStocks #Investing #Q4Results #FY26Results #EarningsSeason #FundamentalAnalysis #StockScreener #Multibagger #ValueInvesting #GrowthStocks #EquityResearch #MarketAlpha #StockPicks #FinTwitter #dalalstreet #NIFTY #SENSEX #SmallCap #MidCap #LargeCap #TradingCommunity #WealthCreation #PortfolioManagement #EarningsCall #QuarterlyResults #MarketOutperformers #BeatTheStreet

6

10

71

9,400

Top-20 results in Q4 FY26 and a one-liner on why.

1) BHAGYANGR: Delivered a major beat with 46.3% revenue growth (vs 35-40% guidance), a 258% PAT surge, and strongly positive CFO of ₹59 Cr ahead of the June 9th copper demerger.

2) NAVINFLUOR: Exceptional performance with 992 bps margin expansion (beating 28-30% guidance) and significant deleveraging as Debt/Equity improved to 0.31x.

3) ETERNAL: Revenue nearly tripled ( 196.4%) driven by Quick Commerce turning profitable (₹265 Cr profit vs ₹82 Cr loss) and growing 625.7% YoY.

4) TIPSMUSIC: Exceptional Q4 with 92.9% PAT growth, beating 20% guidance by 10 points while content acquisition costs were kept to 10.2% vs the 18% guided limit.

5) ACUTAAS: Major guidance beat with 33% revenue growth and 35.87% EBITDA margin (vs 28-30% range), supported by a 155% surge in CWIP for capacity expansion.

6) CGCL: PAT of ₹9,491.52 Mn exceeded guidance by 11.7%, while ROE hit 16.49%, achieving the FY28 target two years ahead of schedule.

7) SMARTWORKS: Reported first full year of profitability with 440 bps margin expansion and crossed the 10 million sq ft operational portfolio milestone.

8) PHOENIXLTD: Major outperformance with EBITDA margins at 60.8% (beating 56-57% guidance) and the residential segment surging 122.3% YoY.

9) EQUITASBNK: PAT grew 405% YoY as provisions declined 52%, with the bank now meeting all universal bank license criteria (GNPA 2.60%, NNPA 0.72%).

10) STLTECH: Strategic pivot confirmed as Enterprise/Data Center revenue mix reached 36% (beating 30% target) and the company turned PAT positive at ₹59 Cr.

11) TMB: Beat guidance across advances (20.78% vs 16%) and business growth (17.57% vs 14%) while driving GNPA to a multi-year low of 0.73%.

12) AURUM: Achieved ₹505.4 Cr annualized ARR target and effectively became debt-free (91% debt reduction) with a 1740 bps EBITDA margin expansion.

13) VEDL: FY26 EBITDA beat management guidance by 12%, while Aluminum margins expanded 1600 bps and the Power segment saw a 365% EBITDA surge.

14) CHENNPETRO: Transformational FY26 with PAT growing 1349% as GRM more than doubled to $9.28/bbl and throughput reached 111.5% capacity utilization.

15) CHOICEIN: PAT growth of 39.1% exceeded 25-30% guidance while EBITDA margins beat the guided range by 620 bps, led by the Broking segment's 110% growth.

16) ATUL: Strong turnaround in Life Science Chemicals (margins expanded 921 bps) and robust free cash flow of ₹847.90 Cr with a virtually debt-free balance sheet.

17) INFOBEAN: Major revenue beat (30.1% growth vs mid-teen guidance) with PAT more than doubling and a strong 1.22x cash conversion ratio.

18) CEATLTD: Revenue and PAT ( 47.7%) beat double-digit guidance while maintaining conservative leverage (0.60x D/E) and increasing the dividend by 350%.

19) FEDFINA: Beaten guidance on AUM growth (22.9% vs 12-15%) and credit costs (0.89%), while PAT grew 52.6% YoY.

20) SEJALLTD: Confirmed turnaround with Glasstech reaching EBITDA break-even and balance sheet deleveraging from 4.16x to 0.99x D/E via a ₹94 Cr equity raise.

Note : This is not an investment advise.

2

3

11

2,625

Feb 19

Sejal Glass Ltd: High-Growth Architectural Glass Turnaround with Strategic Global Partnerships

Sejal Glass Ltd: ~₹684 CMP, a Mumbai-based value-added architectural glass processor (est. 1998) that has successfully emerged from financial stress and is now scaling aggressively in the premium façade and interior glass segment

Jiggar Savla (Whole-time Director) is leading the operational expansion. Under his leadership, the company has transitioned from a sub-₹50 crore revenue base in FY23 to a projected ₹350 crore run-rate business, driven by inorganic expansion and international technology alliances

Mixed Q3 FY26 performance (announced Feb 2026):

• Net Profit at ₹5.01 crore, up 48.7% YoY (down 37.6% QoQ)

• Revenue at ₹100.81 crore, up 63.6% YoY

Sequential profit compression driven by margin moderation (PAT margin 5.04% vs 7.81% in Q2) and elevated finance costs

Key business characteristics:

• Strategic partnership with Saint-Gobain India: Executed the Propel Project Participation Agreement, positioning Sejal as a preferred manufacturing partner for advanced, high-performance architectural glass products

• Inorganic expansion: Successfully integrated the architectural glass division of Glasstech Industries, expanding manufacturing footprint across Taloja (Maharashtra) and Erode (Tamil Nadu), strengthening pan-India execution capability

• Technology moat in niche segment: Entered into a technology licensing agreement with Polymer Technology SRO for fire-rated glass manufacturing — a high-margin and compliance-driven commercial infrastructure segment

• Export-led growth model: International operations (primarily via UAE subsidiary) contributed ~72% of H1 FY26 revenue, providing geographic diversification and higher realizations

• Aggressive scale-up turnaround: Revenue has expanded ~28x since FY21, marking one of the fastest growth trajectories in the domestic architectural glass space — albeit supported by higher leverage

• High leverage monitorable: Debt-to-Equity at ~4.1x reflects asset-heavy expansion; deleveraging through internal accruals remains the key re-rating trigger

• Relative valuation discount: Trading at a meaningful discount to industry leader Asahi India Glass Limited (P/E ~82x) and peers like Borosil Renewables Limited, despite stronger near-term growth and low PEG (~0.2x)

• Operational risk: Elevated working capital cycle and high debtor days remain structural risks; cash-flow discipline will determine sustainability of the turnaround.

5

33

2,486

27 Nov 2025

Acknowledges Glasstech drag on margins right now, but expects EBITDA breakeven by Q4 and then improvement from FY27.

Not seeing slowdown in UAE real estate; if anything, broad-based growth across all emirates starting Africa/Europe to de-risk geography.

1

1

42

24 Nov 2025

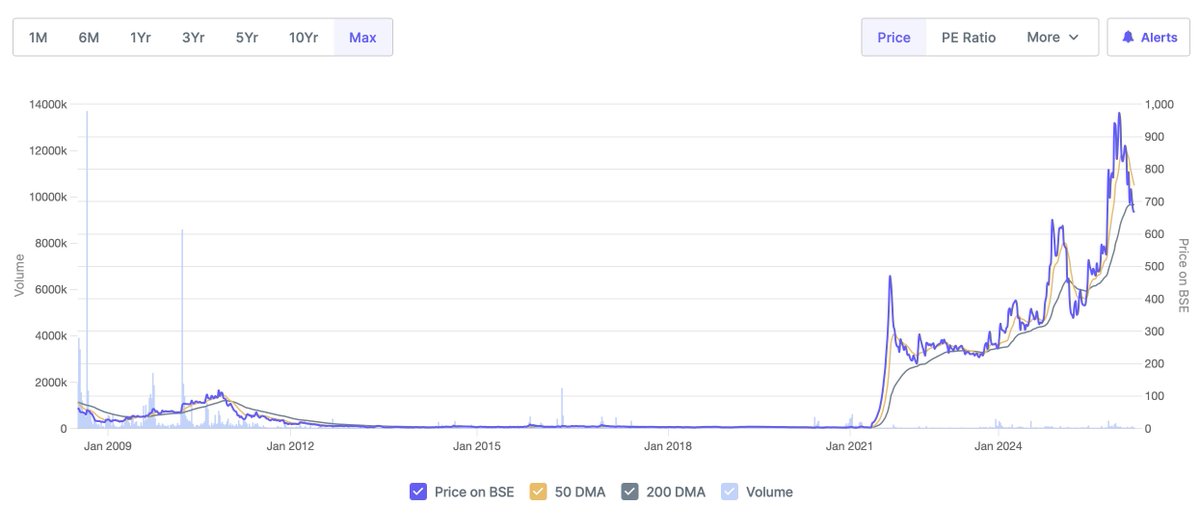

Sejal Glass Reports Strong Growth & Expansion Plans 🚀 | MCap 834.26 Cr

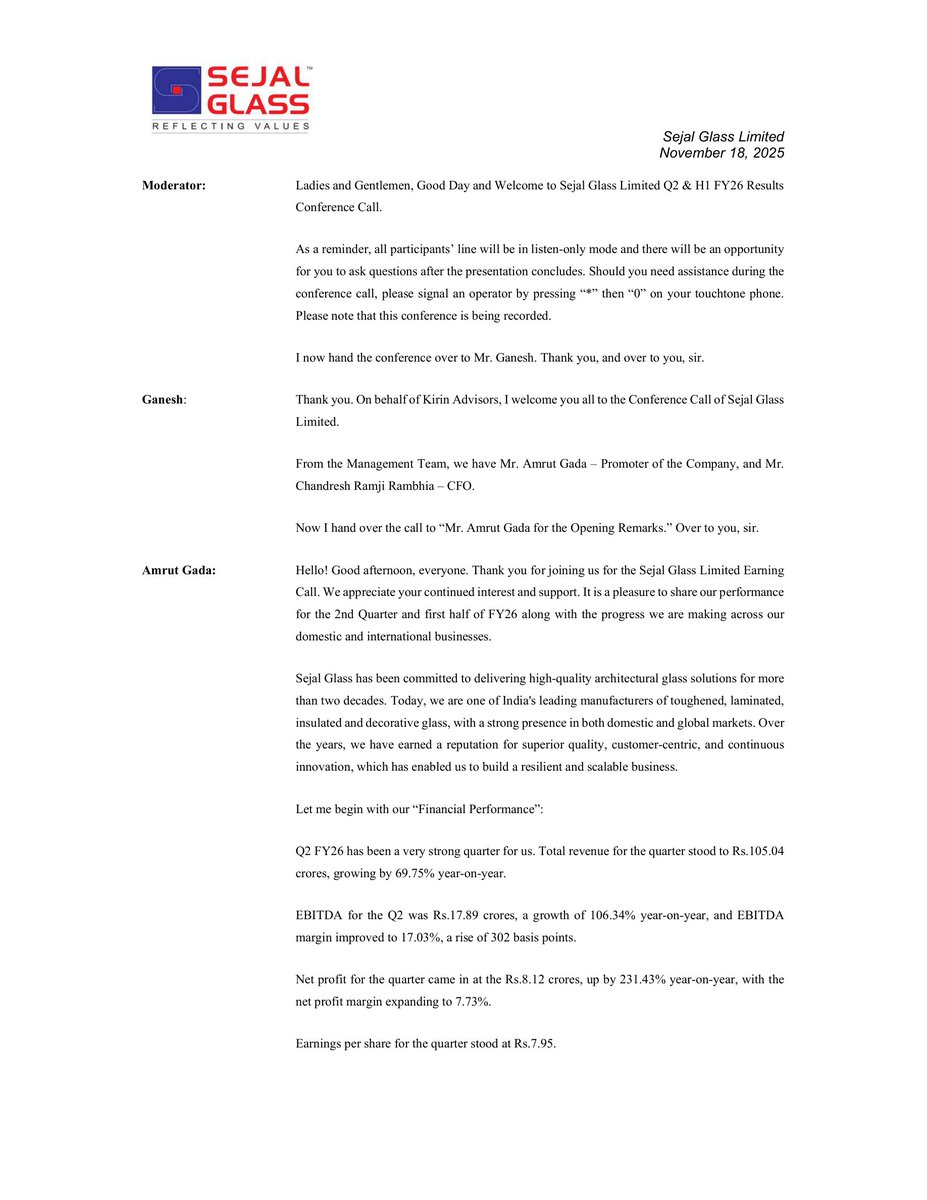

- Q2 FY26 revenue: ₹105.04 Cr (69.75% YoY growth)

- Q2 EBITDA: ₹17.89 Cr (106.34% YoY growth), margin at 17.03%

- Q2 net profit: ₹8.12 Cr (231.43% YoY growth), margin at 7.73%

- H1 FY26 revenue: ₹182.81 Cr (59.03% YoY growth)

- H1 EBITDA: ₹30.38 Cr (89.40% YoY growth)

- H1 net profit: ₹12.53 Cr (226.30% YoY growth)

- Revenue mix: 72% international, 28% domestic

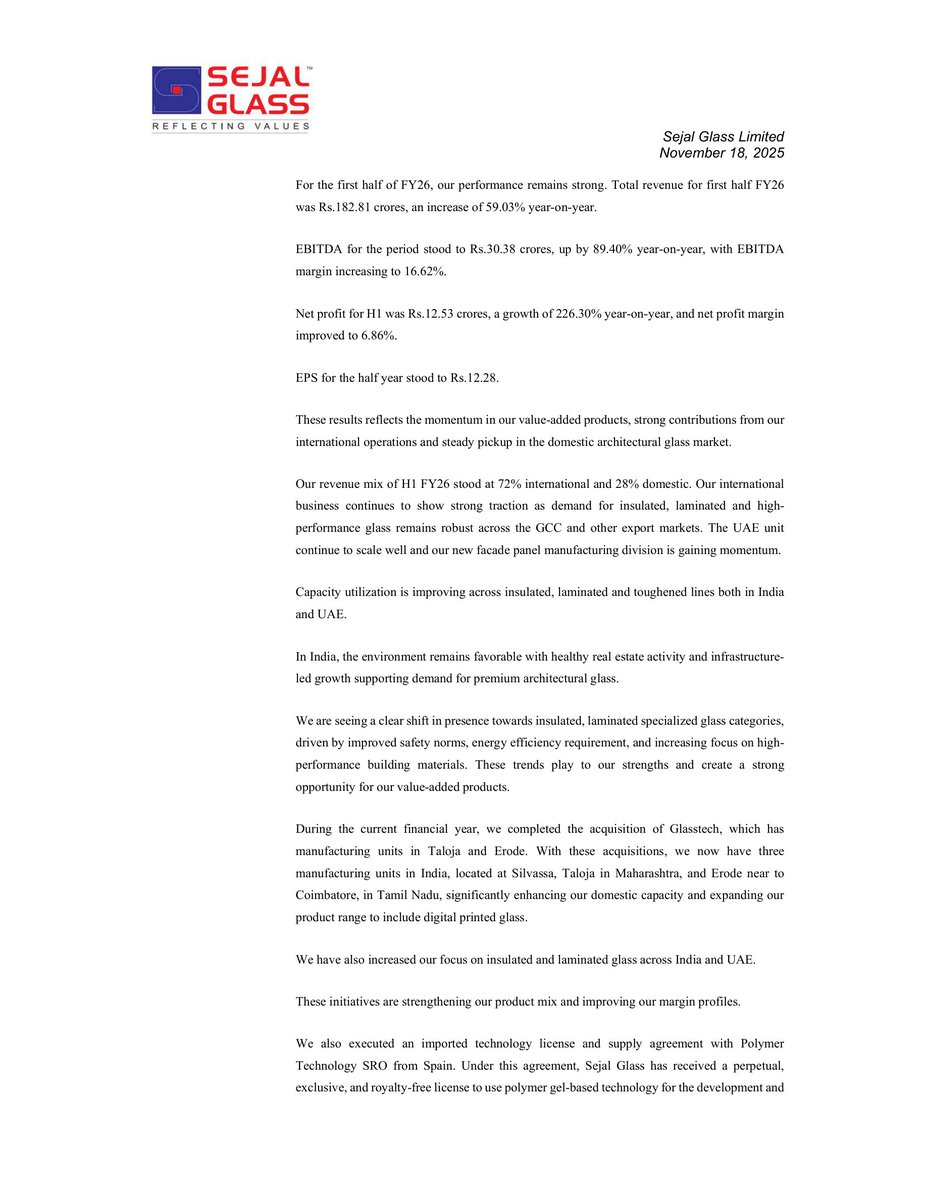

- Acquired Glasstech, adding manufacturing units in Taloja & Erode

- Signed tech agreement with Spain's Polymer Technology for fire-rated glass

- Exploring new markets in Africa & Europe

- Targeting ₹400 Cr revenue for FY26

- Focusing on high-value products: bulletproof, fire-rated, digital printed glass

- UAE capacity utilization: 90% (IG glass), 47% (laminated)

- India capacity utilization: 88% (laminated), 30% (IG glass)

- Strategic supply agreement with Saint Gobain for raw materials

Complete Source: bseindia.com/xml-data/corpfi…

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

Preview 👇 (First 4 out of 18 pages)

2

518

28 Oct 2025

Glasstech and Interior Solutions Ltd. offers top-tier glass solutions for homes, offices and vehicles.

From toughened glass to aluminum windows, every project is handled with precision.

Join OnlineSMEs Training and BuySell Na RobisearchLTD today. #RobisearchFreeMarketDay

5

1

182

28 Oct 2025

Choose durable, low-maintenance Aluminium windows & frameless balconies from Glasstech and Interiors. We deliver QUALITY YOU CAN TRUST for a sleek, modern look that lasts. Join OnlineSMEs Training #RobisearchFreeMarketDay BuySell Na RobisearchLTD

1

18

28 Oct 2025

Glasstech and Interiors provides custom designs TAILORED FOR YOU for homes, offices, and interiors. We cover everything from stunning partitions to sleek facades. Join OnlineSMEs Training #RobisearchFreeMarketDay BuySell Na RobisearchLTD

1

11

28 Oct 2025

Glasstech offers durable glass & aluminium built to last, backed by our SEAMLESS SERVICE from consultation to installation. 📍 Visit us: Sunrise Centre, Northern Bypass Rd. Join OnlineSMEs Training #RobisearchFreeMarketDay BuySell Na RobisearchLTD

Transform your space with Glasstech and Interior Solutions Ltd. From stunning glass partitions to stylish shower cubicles, they bring modern beauty and brightness to your home or office. Join OnlineSMEs Training and BuySell Na RobisearchLTD. #RobisearchFreeMarketDay

2

123

Transform your space with Glasstech and Interior Solutions Ltd. From stunning glass partitions to stylish shower cubicles, they bring modern beauty and brightness to your home or office. Join OnlineSMEs Training and BuySell Na RobisearchLTD. #RobisearchFreeMarketDay

12

6

4

612

28 Oct 2025

For modern spaces that reflect elegance, trust Glasstech and Interior Solutions Ltd.

They provide mirrors, frameless glass, and auto glass replacement with professional installation.

Join OnlineSMEs Training and BuySell Na RobisearchLTD. #RobisearchFreeMarketDay

8

1

316

28 Oct 2025

Transform your interiors with Glasstech and Interior Solutions Ltd. Experts in premium glass partitioning and sleek shower cubicle installations designed to enhance every modern space.

BuySell Na RobisearchLTD, Join OnlineSMEs Training #RobisearchFreeMarketDay

10

11

3

689

23 Oct 2025

📢 Bersiap untuk Pameran Kaca & Fasad Terbesar di Asia Tenggara! Glasstech Asia & Fenestration Asia 2025 kembali hadir di Indonesia.

Sebagai ajang paling berpengaruh di Asia untuk kaca, jendela, pintu, fasad, dan teknologi kaca, #GAFA2025 akan menghadirkan:

✅ Pameran Kaca & Fenestrasi yang menampilkan solusi mutakhir

✅ Arsitek, kontraktor, pengembang, dan pelaku industri dari seluruh Asia

✅ Para pakar industri yang membagikan wawasan tentang tren terbaru yang membentuk masa depan

Catat tanggalnya!

📅 6–9 November 2025

📍 Hall 5, ICE BSD City

Pameran ini akan mempertemukan para profesional, desainer, arsitek, dan produsen untuk mengeksplorasi tren terbaru, produk inovatif, dan solusi berkelanjutan dalam industri kaca dan fasad.

👉 Daftarkan dirimu secara GRATIS di ishk.infosalons.com.cn/reg/g… atau bisa klik link yang ada di bio instagram @glasstechasia

Temukan inspirasi, peluang, dan inovasi hanya di Glasstech Asia & Fenestration Asia 2025!

#GAFA2025 #GlasstechAsia #B2Bexpo #eventbsd

#WonderfulIndonesia #KemenparRI #SetahunBerdampak

1

1

2

457

19 Oct 2025

Sejal Glass Limited:

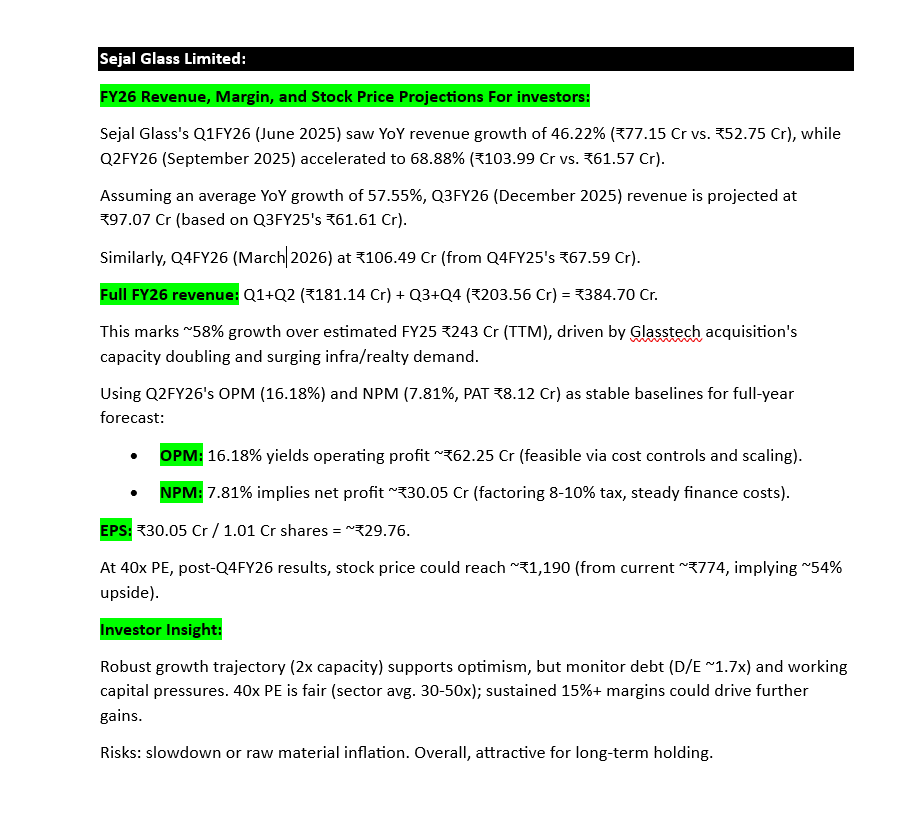

FY26 Revenue, Margin, and Stock Price Projections For investors:

Sejal Glass's Q1FY26 (June 2025) saw YoY revenue growth of 46.22% (₹77.15 Cr vs. ₹52.75 Cr), while Q2FY26 (September 2025) accelerated to 68.88% (₹103.99 Cr vs. ₹61.57 Cr).

Assuming an average YoY growth of 57.55%, Q3FY26 (December 2025) revenue is projected at ₹97.07 Cr (based on Q3FY25's ₹61.61 Cr).

Similarly, Q4FY26 (March 2026) at ₹106.49 Cr (from Q4FY25's ₹67.59 Cr).

Full FY26 revenue: Q1 Q2 (₹181.14 Cr) Q3 Q4 (₹203.56 Cr) = ₹384.70 Cr.

This marks ~58% growth over estimated FY25 ₹243 Cr (TTM), driven by Glasstech acquisition's capacity doubling and surging infra/realty demand.

Using Q2FY26's OPM (16.18%) and NPM (7.81%, PAT ₹8.12 Cr) as stable baselines for full-year forecast:

OPM: 16.18% yields operating profit ~₹62.25 Cr (feasible via cost controls and scaling).

NPM: 7.81% implies net profit ~₹30.05 Cr (factoring 8-10% tax, steady finance costs).

EPS: ₹30.05 Cr / 1.01 Cr shares = ~₹29.76.

At 40x PE, post-Q4FY26 results, stock price could reach ~₹1,190 (from current ~₹774, implying ~54% upside).

Investor Insight:

Robust growth trajectory (2x capacity) supports optimism, but monitor debt (D/E ~1.7x) and working capital pressures. 40x PE is fair (sector avg. 30-50x); sustained 15% margins could drive further gains.

Risks: slowdown or raw material inflation. Overall, attractive for long-term holding.

#SEJALLTD #SejalGlass #Q2Results #Q2FY26 #StockMarket

Disclaimer:

This analysis is purely for educational and informational purposes. It is not intended as financial advice or a recommendation to buy, sell, or hold any stock. These are rough estimates based on my own calculations — and I’ve personally suffered losses many times in the past from such analyses. Please do your own research (DYOR) and consult a qualified financial advisor before making any investment decisions.

19 Oct 2025

Sejal Glass Limited's Q2 & H1 FY26 results (ended Sep 30, 2025) reflect transformative growth post its April 2025 acquisition of Glasstech's architectural glass business, boosting capacity via new plants in Maharashtra and Tamil Nadu.

Consolidated revenue surged 326% YoY to ₹7,719 lakhs, driven by 95% domestic sales, with net profit exploding 857% to ₹1,110 lakhs (EPS ₹0.85).

Margins improved to ~14%, aided by synergies, though expenses rose 286% on materials and finance costs (₹1,062 lakhs).

EBITDA approximated ₹1,920 lakhs ( 300%).

Standalone, the holding company reported losses of ₹147 lakhs (vs. ₹22 lakhs prior), widened by acquisition costs like depreciation (₹278 lakhs) and no tax relief from carry-forwards.

#SEJALLTD #SejalGlass #Q2Results #Q2FY26 #StockMarket

Balance sheet expanded 37% to ₹38,852 lakhs assets, with PPE up 38% and debt-to-equity at ~1.7x.

Cash from operations hit ₹4,228 lakhs ( 1,423%), funding ₹7,523 lakhs capex; closing cash ₹535 lakhs ( 17%).Challenges:

Elevated leverage and working capital strain from receivables.

Outlook: Strong infra/realty demand positions Sejal for FY26 momentum.

4

5

239