Amitava Chakraborty retweeted

#GarwareHitech

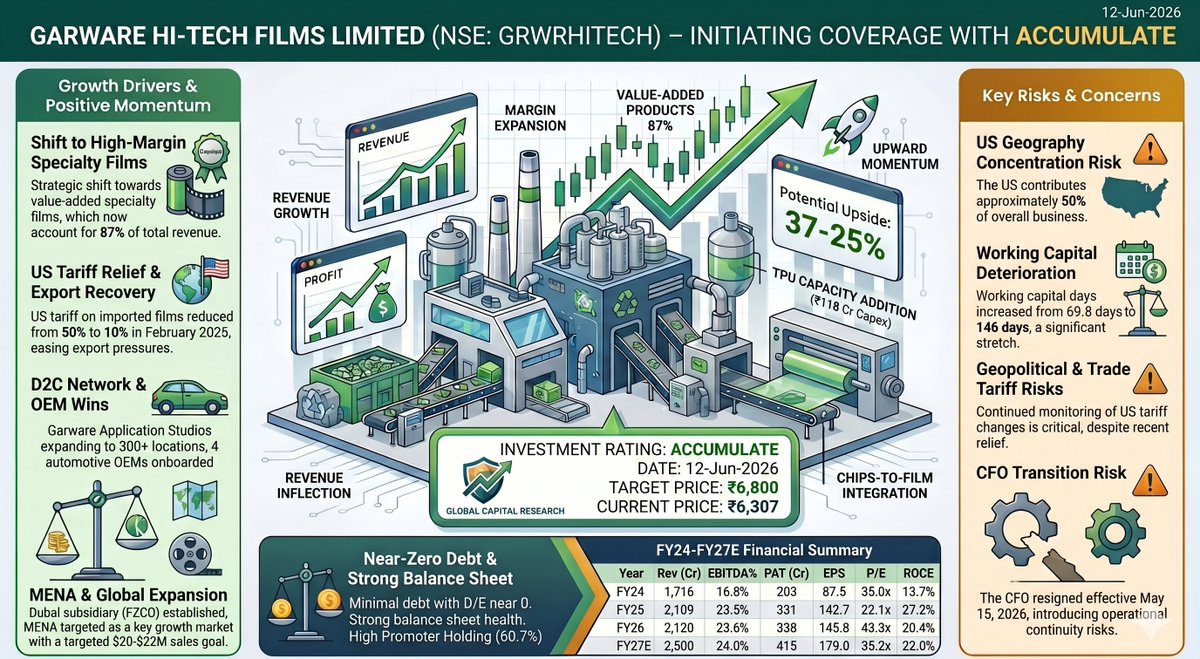

Growth Drivers & Positive Momentum:

1. Shift to High Margin Specialty Films: These now make up 87% of total revenue- a strategic move from commoditized films to higher value products.

2. US Tariff Relief & Export Recovery: US tariffs on imported films were reduced from 50% to 10% in Feb 2025 easing pressures and supporting exports (US is 50% of business).

3. D2C Network & OEM Wins: Expanding direct to consumer presence (300 locations) and onboarding automotive OEMs.

4. MENA & Global Expansion:

New Dubai subsidiary (FZCO) targeting $20-22M sales as a growth market.

5. Capacity additions (e.g., TPU line with ₹118 Cr capex) and Chips to Film Integration.

2

5

41

3,538

Miko Aguiluz retweeted

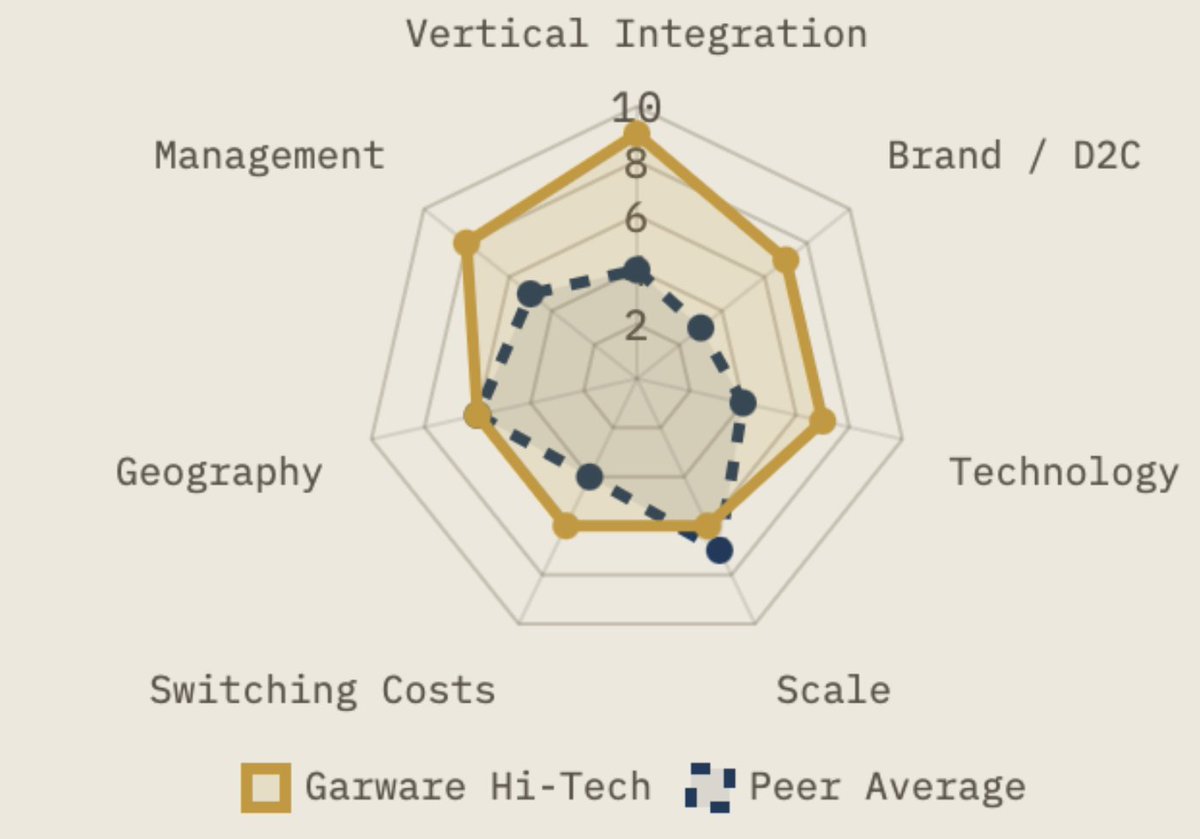

#GarwareHiTech Films is becoming a materials science company not a film company. Most investors still put Garware in the same bucket as packaging film manufacturers.

But today around 87% of revenue comes from value added specialty products such as Sun Control Films (SCF), Paint Protection Films (PPF), and other high margin solutions. The business model has become far closer to a specialty materials company than a commodity film manufacturer.

This distinction matters because specialty material companies globally often command much higher valuation multiples than packaging companies.

The TPU backward integration story may be bigger than investors realize

Most investors know a TPU line is coming. What many don't appreciate is that TPU is the heart of PPF.

Currently TPU is one of the most critical and expensive inputs. Garware's 118 crore TPU project is expected to be commissioned around October 2026.

If execution is successful, benefits could include better gross margins, reduced dependence on external suppliers, faster product development, better quality control and stronger competitive moat

Several investor discussions have highlighted that management expects TPU integration to support future margin expansion.

The real moat is the application ecosystem. Investors usually focus on manufacturing capacity.

But Garware is quietly building:

- Global Application Studios

- Garware Home Solutions

- Large installer networks

- Direct-to-consumer channels

The company now has hundreds of application studios and is expanding internationally. A competitor can buy machinery but building a trained installer network across multiple countries is much harder.

Exports are the hidden engine. Many still see Garware as an Indian company. In reality, exports contribute roughly three fourths of sales and the company has presence in more than 90 countries. If management executes well in the US, Middle East and global architectural film markets, the addressable market becomes far larger than India's market alone.

PPF could become larger than what investors currently model. Today most discussions revolve around Sun Control Films. However, PPF is one of the fastest growing and highest value categories globally.

Garware is India's only professional grade PPF manufacturer, expanding capacity aggressively, onboarding automotive OEMs and investing heavily in TPU integration. If PPF continues compounding at a high rate, it could become the biggest earnings driver over the next several years.

Many investors still value Garware as a film manufacturing company. However a potentially more accurate description could be a global specialty materials company with dominant positions in Sun Control Films, Paint Protection Films, proprietary coating technologies, installer networks and upcoming TPU backward integration. If the market fully shifts from the first narrative to the second, the valuation framework itself could change substantially.

3

9

92

7,313

Jun 12

A good day for the PF. But looking at the recent past nothing is certain. Both parties might backtrack by weekend. Else need to see how markets behave next week.

PF stocks that surprisinlgy stayed -ve today

GarWareHiTech

Ideaforge

HSCl

Overall ~4% gain and PF closed at ATH.

Top performers.

NetWeb

Senores

Goldiam

337

Jun 12

Garware Hi-Tech Films: Specialty films (87% of revenue) fuel growth and margin expansion. Strong balance sheet, export recovery, OEM wins, and capacity additions support the outlook. ACCUMULATE. CMP ₹6,307 | TP ₹6,800. 📈 #Stocks #GarwareHiTech #Investing

102

Jun 10

A small-cap company operating in a niche segment with very limited competition.

Garware Hi-Tech manufactures Paint Protection Films (PPF) and Sun Control Films used in luxury cars, premium homes, malls, airports, and commercial buildings.

The company delivered strong Q4 results and operates a high-margin, high-growth business model.

In this video, we analyze the business, growth drivers, and future opportunities. 👇

#stockmarketnews #garwarehitech

1

2

11

550

Jun 9

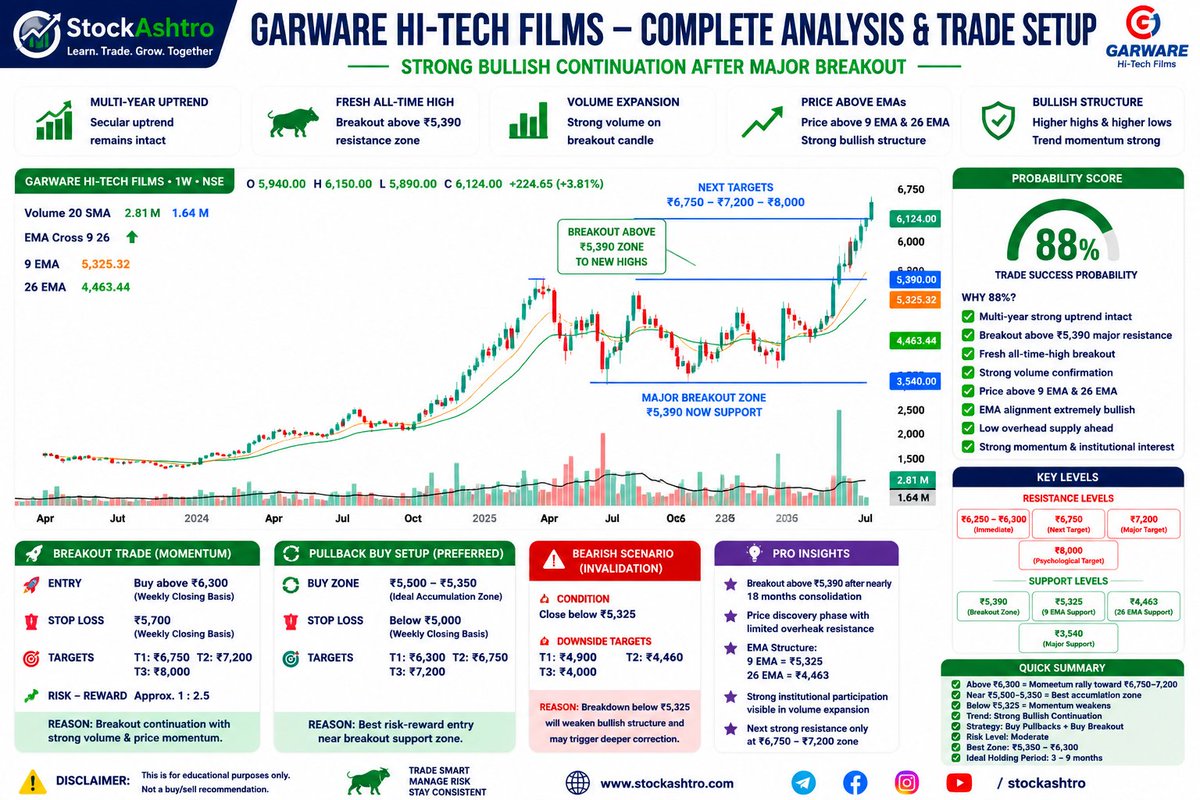

🚀 GARWARE HI-TECH FILMS hits a fresh All-Time High! 📈🔥

✅ Multi-year uptrend intact

✅ Breakout above ₹5,390 major resistances

✅ Momentum firmly with the bulls

Follow @StockAshtro for daily breakout stocks

#GarwareHiTech #BreakoutStocks #SwingTrading #StockMarketIndia

2

139

Jun 9

Garware Hi-Tech Films Q4FY26 concall looks incredibly strong

Zero Debt, 2,500 Cr revenue visibility 📈

• Launching high-margin TPU & PDLC films 🚀

• 4 new Indian Automotive OEMs onboarded for PPFCapacity utilization hitting 85% . #GarwareHiTech #StocksToWatch #StockMarketIndia

Jun 8

Garware Hi-Tech Films , understanding the value chain advantage and understanding the product economics , capability mapping and qualitative depth analysis and also attaching the first half of the call notes , second is also available on the feed folks

185

Jun 7

Future Predictions & Management Guidance :💥 💥

FY27 Revenue Goal: Management aims for ₹2,500 crore in revenue for FY27, which translates to an 18% growth rate.

Margin Outlook: EBITDA margins are expected to remain robust, hovering within the 20% to 25% range.

Capacity Expansion: The newly announced SCF line will add ~1,200 LSF in capacity, while current PPF lines run at high utilizations, setting up steady future volume growth.

Global Reach: The company is significantly scaling up direct-to-consumer (D2C) brands and expanding its Global Application Studio footprint to increase volume contributions to 25%-35% (up from 10%-15%).

💥 Key Operational Updates:

Massive Capex Approval: The board approved a ₹192 crore investment to build an advanced Sun Control Film (SCF) line with robotics and automation. Commercial production is expected in June 2027.

Backward Integration: The Thermoplastic Polyurethane (TPU) backward integration line will commission in October 2026, boosting margins in Paint Protection Films (PPF).

New Product Launch: Unveiled three new product lines: TPU-based UV printable films, PDLC specialty films (Privacy on Demand), and Graphic Solutions.

Distribution Push: Garware Home Solutions centres are targeted to scale to 50 studios by FY27, alongside the expansion of 11 international Application Studios in the USA and UAE.

#garwarehitech #sharemarket #stockmarket

Jun 7

Garware Hi-Tech - sun control & paint protection films maker. Took a 50% US tariff blow, absorbed the pain to hold customers, kept investing in capacity. Tariffs now down to 10% & runway is clear again 🚀

Read more about the business here 👇

1

8

628