May 28

🆕 El contenido del MASC no necesita incluir una «posibilidad de acuerdo», según la AP de Madrid.

🔶 La Audiencia Provincial de Madrid ha determinado que, en los Medios Adecuados de Solución de Controversias, no es necesario que se exprese «una posibilidad de acuerdo», sino únicamente que quede claro el objeto de la avenencia. Una decisión con la que el tribunal corrige la inadmisión de una demanda presentada por GovCom Abogados, y marca una línea a seguir en estos nuevos trámites prejudiciales obligatorios.

confilegal.com/20260528-el-c…

3

3

338

May 16

GovCom Essentials:

When media outlets write, “The White House did not immediately respond to a request for comment,” what they mean is that the government did not allow them to shape the agenda or reframe the issue.

Make no mistake: these are not disclaimers, but powerful framing devices.

#GovCom101

May 14

U.S. Border Patrol chief Michael Banks is resigning in the latest leadership shake-up of officials implementing President Donald Trump’s immigration crackdown. apnews.com/article/border-pa…

10

101

DAMN so many of yall have gotten into the podcasting thing recently! sending me messages saying:

"Hey, I need a quick favor 🙏🏾. I’m in the running to co-host a major podcast event with Spotify & Google. It’d mean a lot if you could drop a vote for me 🗳️💯. Appreciate you! LINK: (random steam of numbers and letter).govcom

🤣🤣🤣

5

20

583

Jan 14

Your disgusting and a shameful self serving lying 🤥 individual can we have legislation for a Govcom? You’d be rubber ducked

2

70

1 Oct 2025

puede ser que un ministro les ataque. ¿Por qué a Bolaños no le pone nervioso ni le preocupan las sentencias irregulares de mis clientes? El Gobierno debe callar y esperar a que la Justicia haga su trabajo», lamenta De la Torre, abogado de Govcom.

3

98

20 Jun 2025

Govcom has come to stay we project government business and counter misinformation

2

2

5

184

20 May 2025

A heartfelt thank you to everyone who made the #RockITGov Triple Crown Networking Event a night to remember!

Although we could not attend in person, it was an honor for Valencia Social Technology Digital Strategies (VSTDS) to serve as a media sponsor for such a dynamic and community driven event.

Seeing the energy, collaboration, and Derby spirit come alive across social media reminded us of what makes this community so special.

Get ready for the RockITGov Golf event on June 27th, hosted by the one and only, @depeekii ⛳️🏌️🏌️♀️🏌️♂️

Registration Link: rockitgovgolf.com.

Check out the RockITGov website here: rockitgov.org.

Interested in social media marketing services? Contact us at: VSTDSmarketing@gmail.com

#VSTDS #GovCom #GovCon #MediaSponsor #Community #SocialTechnology #DigitalStrategies #SocialMedia #Marketing #Success #Visibility #Learn #Build #RiseTogether #SocialNetworking #OpenForBusiness

1

2

62

30 Dec 2024

Viasat $VSAT —despite its brutal -70% YTD price collapse—may offer substantial upside for contrarian investors. Note that none of this is financial advice; always do your own due diligence.

*The Macro Backdrop: Why S/MID Securities Are Beaten Down (Dec 30th, 2024)

Broad market outflows from small- and mid-cap names have indiscriminately punished countless companies, including Viasat. In a risk-off environment, passive ETFs, quant funds, and other algorithmic strategies often perpetuate “momentum selling,” dragging stock prices below fair value. Viasat, being in the crosshairs of both cyclical broadband weakness and short sellers laser-focused on its debt, has seen its share price battered—while the underlying fundamentals quietly pivot toward defense.

1) Why the Valuation Is Dirt Cheap

Equity < Liquidation Value?

The stock is trading as if bankruptcy were imminent, yet in a worst-case liquidation, Viasat’s satellites, orbital slots, and other intangible assets (e.g., spectrum rights) would likely fetch more than its current market cap. This means the market is pricing the company below the value of its underlying assets.

* Below Liquidation Value: The market is pricing Viasat below the worth of its hard-to-replicate assets (satellites, orbital slots, spectrum rights), meaning even a “fire sale” could exceed the current market cap.

* Severe EV Multiple Discount: Viasat’s EV/EBITDA (~4×) is abnormally low compared to the 6–8× typical of defense or aero-comm companies, signaling a mispriced “distress” scenario.

* Robust Revenue vs. Tiny Market Cap: Revenue could surpass $4.5B YTD while the market cap hovers near $1B—an extreme disconnect that assumes near-term collapse despite recent contract wins.

* Tangible & Intangible Asset Value: Orbital “real estate” and spectrum allocations are finite, high-demand resources; they carry significant resale value missing from the current share price. The intangible asset value expands the Core NAV far past the current market cap.

* Debt Overhang Is Manageable: Refinanced maturities and increasing defense/government cash flows reduce the likelihood of insolvency—a key oversight in the “bankruptcy pricing” thesis.

* Catalysts for Re-Rating: A shift in market perception (realizing Viasat isn’t doomed), ongoing defense contract momentum, and reduced CapEx (boosting free cash flow) could trigger a sharp rebound from oversold levels.

No True Threat of Insolvency

Yes, the debt from acquiring Inmarsat is large, but management has already refinanced its obligations, easing near-term liquidity risks. Meanwhile, new government/defense contracts (NASA, DoD) are rolling in, indicating that major clients (who do in-depth financial vetting) see Viasat as a viable partner.

Key Point: The stock is so beaten down that you’re paying less than “fire-sale” prices for a company that is neither in imminent danger nor lacking strategic direction.

2) Not a Growth or Stalwart—But a Turnaround

Legacy Broadband Woes?

Competition from Starlink and others has hammered the perception of Viasat’s consumer broadband segment. That’s partly why the market has sold off so aggressively.

Defense & GovCom Pivot

Crucially, Viasat is transitioning to a defense-first identity—a space that often commands higher margins and has far fewer competitors. The newly expanded defense pipeline is becoming the core driver of revenues, offsetting any broadband weakness.

CapEx Peaking → FCF Improvement

Heavy satellite-related spending is nearly behind them. As CapEx normalizes, free cash flow should rise—giving Viasat even more room to reduce debt and invest further in high-value government segments.

Key Point: This is not some high-growth darling, nor an established blue-chip. It’s a “fallen angel” that could re-rate sharply if its defense pivot continues delivering results.

3) Short-Term Catalysts & Upside Triggers

Short Interest ~23%

A large chunk of the float is betting on further downside. If Viasat posts better-than-expected earnings, announces new contract wins, or shows clear traction on paying down debt, those shorts may start covering. This alone can accelerate any price recovery.

Market Recognition of Defense Potential

The minute the broader market stops viewing Viasat as just a consumer-satellite “also-ran” and starts seeing it as a legitimate defense/GovCom contractor, we could see a significant multiple expansion—from its current rock-bottom to something more in line with other aerospace/defense names.

Refinancing & Debt Maturity Relief

The new debt terms remove the doomsday scenario. As management continues to extend or restructure maturities, concerns about default will fade, reducing the equity risk premium and supporting a higher share price.

Key Point: Any one of these factors could cause the market to reevaluate Viasat’s risk profile, potentially triggering a sharp move upward from depressed levels.

4) Technicals & Sentiment: The Set-Up

Oversold Levels

Viasat is trading near multi-year lows. Historically, these kinds of “off the cliff” valuations arise from indiscriminate selling (including forced liquidations by funds). They can also mark major long-term bottoms.

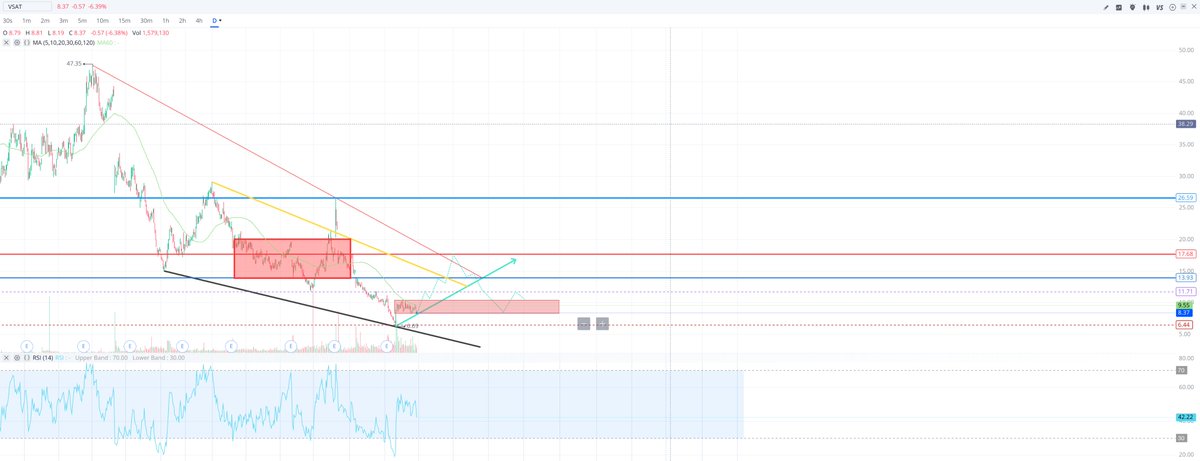

Possible Range TargetsNear-term, a move back to the $11–$14 range is plausible if sentiment shifts.

Above that, $17–$18 is a key technical pivot: a break there could signal a more robust turnaround, potentially targeting the mid-$20s.

Key Point: The downside appears limited by fundamental valuation floors, while the upside could be substantial if short interest unwinds and new defense news flow improves sentiment.

5) Bottom Line: A High-Conviction Contrarian Bet

- Summary of the Bull Thesis Massively Undervalued: Trading well below asset values; worst-case scenarios appear over-discounted.

- Defense Pivot Is Real: NASA/DoD aren’t awarding contracts lightly—Viasat’s systems and expertise are in demand.

- Debt Overhang Is Manageable: Refinancing done; CapEx peaking; free cash flow set to improve.

- Short Squeeze Potential: ~23% of the float is short; positive news or improving fundamentals could force covering.

- Forced Selling Created a Misprice: Pension-fund liquidations had nothing to do with the company’s quality.

Final Take: This isn’t a simple growth story or a blue-chip mainstay, but rather a deep-value turnaround where the risk-reward is skewed in favor of long-term upside. Viasat’s transformation—coupled with asset coverage that significantly exceeds its current valuation—makes the current share price a compelling entry point for contrarian investors seeking a high-conviction setup.

$VSAT

2

2

857

23 Dec 2024

My breakdown on Viasat! — Bullish in the near to mid term:

I’ve personally experienced Viasat’s service on a commercial flight, and frankly, it wasn't great. It’s clear that the commercial broadband segment is under pressure and won’t be the company’s growth engine moving forward. That said, Viasat plays a unique role in servicing less populated and specialized airline routes, which still provides value in specific markets — As well as maritime. In my view, the company’s future lies in its pivot toward defense, where it can build a stronger identity. By maintaining its commercial aviation & maritime segment as a steady revenue source to service LBO debt from the Inmarsat acquisition, $VSAT can continue moving forward and focus on its transformation into a defense-first, high-value operation.

My Breakdown!

$VSAT is a legacy broadband company transforming silently solidifying itself a rising defense contractor.

Recent tailwinds include:

- Debbie Wasserman Schultz buying equity (public disclosure) *chairs the committee's Subcommittee on Military Construction, Veterans Affairs, and Related Agencies.

- December 2024: Viasat Awarded up to $568 Million IDIQ Contract from General Services Administration to Support C5ISR Capabilities for U.S. Defense Forces

- December 2024: Portion of $4.82B NASA contract, which includes money for Viasat to support missions in low Earth orbit.

These are just the start of a bigger pivot. Let’s dive into why this stock, down 70% YTD, could be wildly undervalued.

1/ Down 70% YTD—Yet a Rising Star?

$VSAT share price collapse (nearly -70% this year) has overshadowed a dramatic pivot into defense & government. Recent NASA and DoD contract wins highlight its evolving identity—no longer just a “legacy broadband” name, but a critical partner in national security & space initiatives.

2/ Bearish to Bullish—Catalysts Everywhere

- Defense Revenue: Up significantly the past 6 months, signaling a sticky & growing segment that commands higher margins.

- Debt Restructuring: Viasat refinanced LBO debt (from the Inmarsat deal), extending maturities & easing near-term liquidity fears.

- EPS YoY Improvement: Management executed cost controls & integration strategies, drastically reducing losses.

- Institutional Forecasts: Multiple analysts project 2026 profitability, suggesting the heavy CapEx phase is peaking.

3/ Valuation Disconnect: A True “Deep Value”

- GAAP NAV: Trading at just 0.2× book value by some measures—even a conservative “core tangible” estimate gets near 1×.

- EBITDA Multiples: Current multiple doesn’t reflect the rising share of defense revenue. If that segment outpaces consumer broadband, Viasat’s EV/EBITDA could re-rate sharply (think 6–8× vs. today’s ~4×).

- Margin of Safety: Even in a worst-case “distressed buyout,” valuations could exceed the current share price. Under a normal synergy case, fair value multiples look far higher.

4/ The Debt “Overhang” … or Growth Driver?

- Yes, Viasat took on big debt, but it effectively doubled top-line revenue by acquiring Inmarsat. Heavy satellite CapEx is nearing completion, which should free up cash to pay down debt. Lenders also wouldn’t extend these terms if Viasat’s financial profile was truly unsound—and NASA/DoD awarding contracts post-financial compliance checks underscores viability.

5/ Policy & Macro Tailwinds

- New Administration (US) & UN Allies: Heightened focus on space, cybersecurity, and secure global comms = potential multiyear expansion in satellite defense budgets.

- Military Spending Trend: Broader NATO & allied defense budgets are rising; that’s a direct catalyst for Viasat’s government solutions.

*Trump administration asking UN countries to increase individual spending by 5% respectively.

6/ Short Interest at ~23%

A staggering 23% of float is short—possibly due to legacy broadband worries & debt fears. But if Viasat’s defense pivot continues to gather steam, this setup could trigger a short squeeze. Bearish sentiment is precisely what has driven the stock to deep-value levels, offering contrarians a potential opportunity.

7/ Pension Fund Liquidation of Senior Notes and Equity:

- Earlier this year, certain pension funds liquidated a significant portion of Viasat's private notes and associated equity positions. These sales were concentrated during Q2 and Q3 of 2024 and are estimated to have involved tens of millions of dollars worth of securities. The forced liquidation of these notes and equity further sank Viasat's share price, exacerbating the already bearish sentiment in the market. Importantly, this selloff was unrelated to the company's fundamentals but rather tied to portfolio rebalancing and liquidity needs by these funds. This creates a classic mispricing opportunity for patient investors, as the downward pressure on the stock doesn’t reflect the improving financial health or strategic pivot underway at Viasat.

8/ The Future Identity: Defense GovCom

Viasat is evolving beyond consumer satellite internet. DoD, NASA, and allied military contracts offer high barriers to entry, multi-year deals, and robust margins—forming a moat absent in the competitive consumer broadband space. As the defense share of revenue climbs, expect the market to re-rate the stock upward.

9/ Bottom Line: Undervalued, Underestimated

- Down 70% in 1 year.

- Trading at 0.2×–1.0× NAV, depending on intangible adjustments.

- EPS rebound yoy, debt refinancing done, defense ramp accelerating.

- Analysts see profitability by 2026, with potential share prices far above current levels.

10/ Addressing Legacy Broadband Threats: The Biggest Bear Argument

- Yes, Viasat’s legacy commercial broadband business faces real competition—most notably from Starlink.

Here’s why this bear case, while valid, is not the death knell for the company:

- Starlink’s Strengths: Lower latency and competitive pricing in consumer markets.

Viasat’s Counterpoints:

Established Moat in Commercial Markets:

- Many businesses, airlines, and maritime fleets already use Viasat systems, creating significant switching costs due to installed hardware and integration.

- Government Preference: National security-related contracts typically favor established defense contractors with track records in secure comms (where Viasat excels).

11/ Can Defense Cover Legacy Weakness?

- Even with an aggressive decline in legacy broadband revenues, the growing defense segment may offset most (if not all) of the blow:

- Sticky, High-Margin Defense Revenue: As defense grows toward 50% of total revenue, it becomes the dominant driver—helping stabilize cash flows.

FCF Leverage from CapEx Tapering: With CapEx from satellite launches winding down, free cash flow is set to grow. That additional cash can be used to: Pay down debt, reducing interest expenses.

- Fund further growth in government/defense initiatives.

- The pivot to defense mitigates the risks posed by legacy competition and creates a runway for sustainable growth—even if consumer broadband declines sharply.

12/ Why This Threat Isn’t Fatal

While competition in consumer broadband is real, Viasat’s strategy minimizes exposure:

- Contracts & Installed Base Lock-In: Existing contracts (commercial, aviation, maritime) limit customer churn.

- Defense as the New Growth Engine: Revenue is shifting toward high-barrier industries where Viasat’s expertise is hard to replicate.

- Debt Restructuring Supports Pivot: Increased free cash flow allows Viasat to de-lever while aggressively investing in defense—ensuring the pivot succeeds.

13/ The Market Isn’t Pricing This Transition

- The legacy broadband bear case is already baked into the stock price (down 70% YTD). What’s not priced in is:

The ability of defense revenue to replace and surpass legacy losses.

- A free cash flow inflection point as CapEx declines.

The market rerating Viasat as a defense-first company with higher-margin, recurring revenue streams.

14/ Bottom Line on Legacy Threats

Bearish sentiment has over-emphasized competition risks in commercial broadband while ignoring the stabilizing effect of the defense segment. Viasat is actively reducing its reliance on legacy markets, and the pivot is working. With growing FCF, stabilizing revenue, and rising defense contracts, the headwinds are being addressed—and the long-term outlook is far stronger than the current price implies.

Final Take: Short-term sentiment is brutal, but value is found where others don’t look. Viasat’s pivot, backed by credible contracts and strategic CapEx near its peak, suggests the market hasn’t priced in the defense-driven upside. As they de-lever and showcase sustainable gov/defense revenue, that 70% drop could be the oversold moment opportunistic investors sought.

Citations:

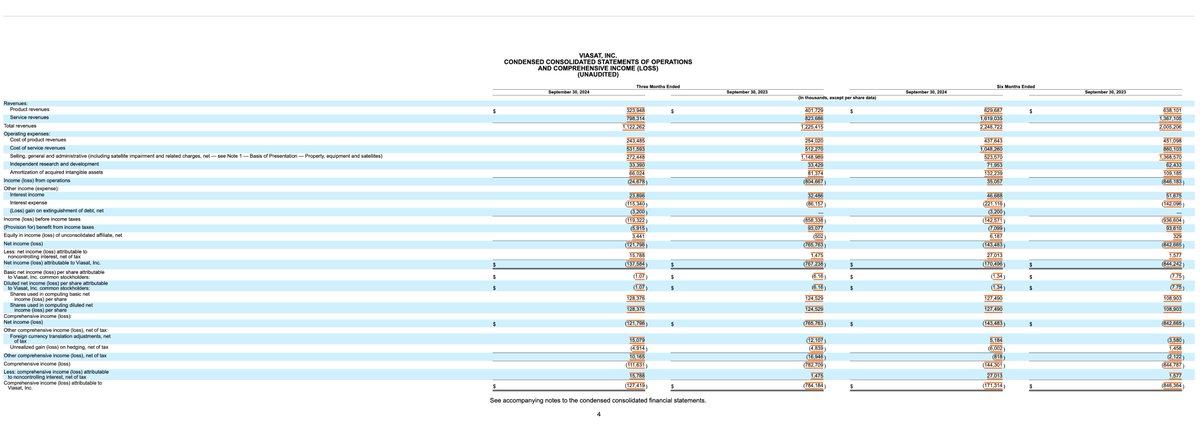

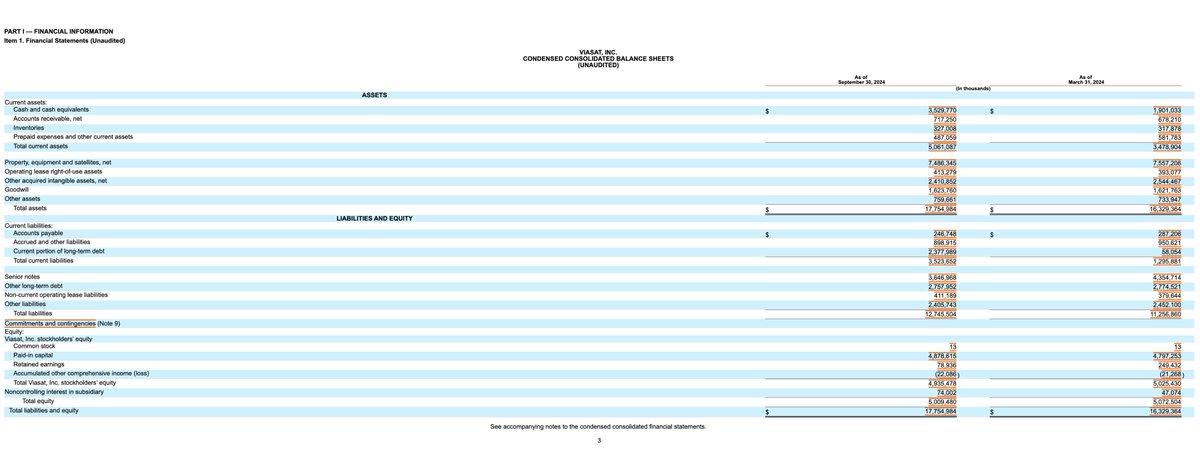

- SEC Edgar latest 10Q, attached Income Statement & Balance Sheet.

- JPM Equity Research, December 20th Report on 26' and beyond outlook. (Privileged) ~ $15 to $12 Price Target.

This information is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any securities. I hold a position in $VSAT | Please conduct your own research or consult a licensed financial advisor before making investment decisions.

2

3

341

11 Nov 2024

Me liking Greg’s tweet while we in GOVCOM like seriously guys IDGAF

1

5

180

20 Oct 2024

Para Pakar Komunikasi Berikan Refleksi Komunikasi Satu Dekade Presiden Jokowi, Katanya....: Govcom, mitra humas pemerintah, merilis Govcom Insights, tentang sebuah laporan yang membahas perjalanan komunikasi Presiden Jokowi selama satu dekade terakhir. dlvr.it/TFX6Q3

1

749

4 Jul 2024

Prezado Sr @eztourinho, espero que se encontre bem e com saúde.

Na posição de reitor da UFPA, gostaria que o Sr pudesse analisar os tuítes abaixo com teor misógino de um professor, tentei contato com a universidade, também enviei e-mails a reitoria, Govcom e não obtive retorno.

2 Jul 2024

O professor da @UFPA_Oficial o @diegocmiranda2 também xingou de piranha e outros a @renatajbarreto , a @Amandavettorazz , a @CarolDeToni , a @Biakicis e dezenas de mulheres em seu perfil.

Sinceramente espero uma posição da universidade a respeito do comportamento do professor.

24

158

819

16,017

4 Jun 2024

We're one week out from @FORUM_govcon's Innovation Awards! @Blake_Harvey_, VP of Growth at Red Team, is kicking off the event with an overview of the market, contracting trends, and end of fiscal year advice. See you on June 11!

#FORUMnnovationAwards #leadership #awards #govcom

2

42

20 May 2024

Hoje, em Washington, acontece a 2ª edição do Diálogo de Alto Nível Brasil-Estados Unidos. A reunião será copresidida pela Secretária-Geral das Relações Exteriores, Maria Laura da Rocha, e pelo Secretário de Estado Adjunto dos EUA, Kurt Campbell. #govcom #bicentenárioeuabr

1

26

7 Mar 2024

The #SBIR Knowledge Academy from @ForwardEdgeAI is a powerful use of #AI available to everyone today! It helps startups and government acquisition professionals accelerate the transition of Phase I/II SBIRs to Phase III. Agencies can sole source Phase III SBIR contracts in days versus months.

Explore and use The Academy online at lnkd.in/gxAV4_me. Your guide while there is Maven, our large language model (LLM) trained on SBIR information and relevant sections of the Federal Acquisition Regulations (FAR).

#SBIR #STTR #LLM #generativeai #generativeaitools #artificialintelligence #govtech #govcom #governmentcontracting #governmentcontracts #governmentprocurement #governmentfunding #governmentcontract

2

288

23 Feb 2024

“In theory, theory & practice are the same. In practice, they are not.” - A. Einstein.

We concluded the #GovCom week by visiting Doordarshan & Aakashvani Bhawans. This completes the full circle of #GovCom's theory & practise workshop organised by Dept of ADPR&DM at @IIMC_India

7

115

22 Feb 2024

"Wars are perennial, they continue, their forms may change "

The narrative built by the media & the actual side of truth around the #Agniveer scheme was cleared by @RDXThinksThat Sir. This concludes the 4th day of #GovCom workshop organised by the Dept of ADPR&DM. @IIMC_India

1

11

735

17 Jan 2024

@AdamRutherford maybe what is needed here some kind of best practice word template for resigning ministers to use? #govcom

16 Jan 2024

Here go again: double space between greeting and first line. Poor choice of sans font, two pages, double justified. Inelegant, clunky and lacking in grace 4/10

2

264

6 Dec 2023

Crime pela internet com loja famosa não dá . Vou até a o fim agora .

Fraude ! Não entregaram minha compra e nem devolveram o meu dinheiro

Ponto frio e casa e vídeo .

#ponto

#Govcom #procom #prefeiturario #pcerj #sbt #globo #record #globonews #cnnbrasil #radiotupi #radioglobo

2

5

5

229