Please join us for our weekly Kitely Community Meeting today, June 14 at 1 PM PDT. Meet new friends, learn what's new, share & ask questions. Everyone is welcome! We hope to see you there!

TP to Welcome Center: bit.ly/KitelyWelcome

#opensim #hypergrid

10

**GateCrashers is LIVE!** gatecrashers.events

The Hypergrid finally has its own event hub! Post events, list venues, browse the calendar, bookmark your favorites, and teleport to the action with one click!

*Built with love for the OpenSim community — See you at the party!*

1

Jun 10

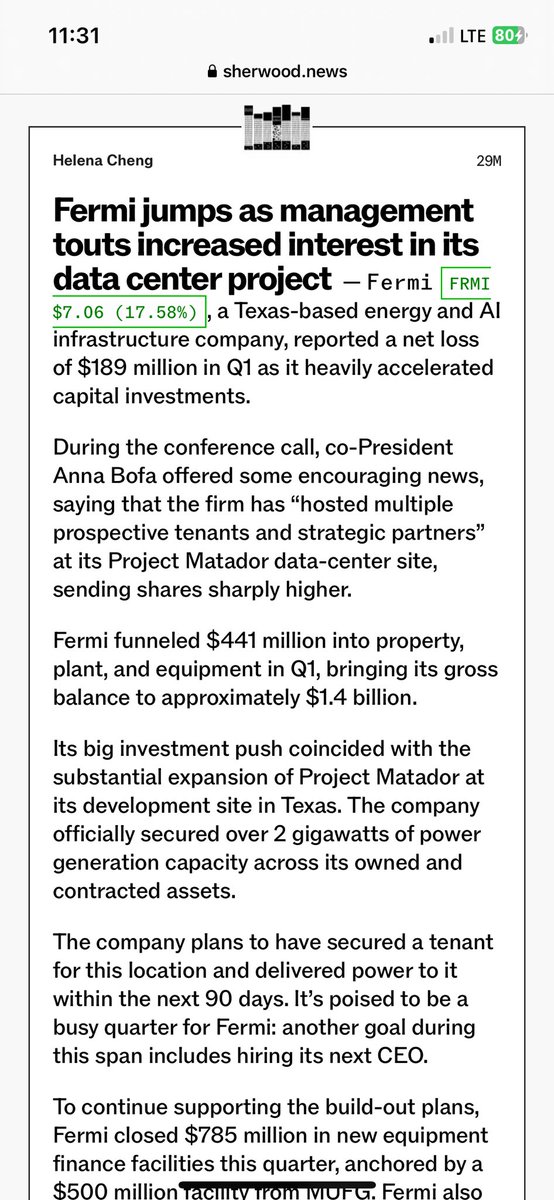

$FRMI 🔥 19% Fermi is ripping on AI power momentum! Project Matador:

→ ~2 GW secured generation

→ 11 GW in permitting

→ $785M equipment financing locked Building the world’s largest private HyperGrid for hyperscale AI in Texas. Despite the board drama, this AI power beast is waking up. Still only ~$4B market cap with massive long-term runway. 📷#FRMI #AIPower #ProjectMatador

3

927

Jun 7

Please join us for our weekly Kitely Community Meeting today, June 7 at 1 PM PDT. Meet new friends, learn what's new, share & ask questions. Everyone is welcome! We hope to see you there! :wave:

TP to Welcome Center: bit.ly/KitelyWelcome

#opensim #hypergrid

2

2

18

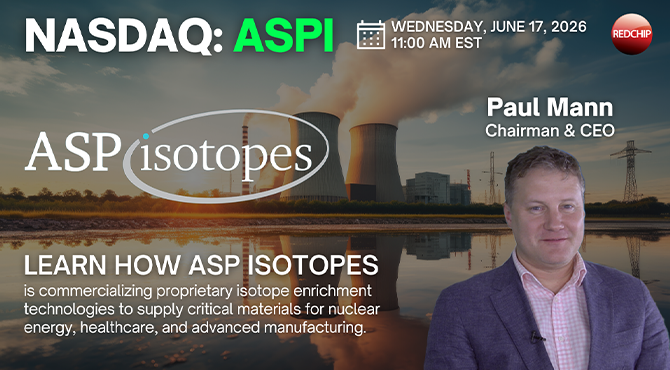

ASP Isotopes (Nasdaq: ASPI) | Investor Webinar | June 17 at 11:00 AM ET — Mark Your Calendar

The critical materials supply chain is being redrawn — and ASP Isotopes is positioning itself at the center of it. From isotope enrichment facilities now in commercial production in South Africa to a transformational acquisition that expands ASPI into helium and natural gas, the company's June 17th investor webinar is the opportunity to understand why this story is accelerating.

Why investors are watching:

- Signed definitive agreements with TerraPower (founded by Bill Gates) to supply up to 150 MT of HALEU over 10 years beginning 2028

- Joint venture with Fermi America (co-founded by former U.S. Energy Secretary Rick Perry) to build a HALEU enrichment and stable isotope facility at the 11GW HyperGrid campus in Texas

- Global HALEU demand valued at $37B through 2037, with structural Western shortages in Silicon-28, Ytterbium-176, Nickel-64, and Lithium-6/7 historically supplied by Russia and China

Register now to secure your spot for the June 17 webinar and hear directly from ASPI's leadership on the company's commercial trajectory and growth roadmap.

Register here: redchip.news/43xNii4

$ASPI $SMR $NNE $OKLO $UUUU $CEG $VST $CCJ $UEC $LEU $GEV $BEP

1

284

Jun 3

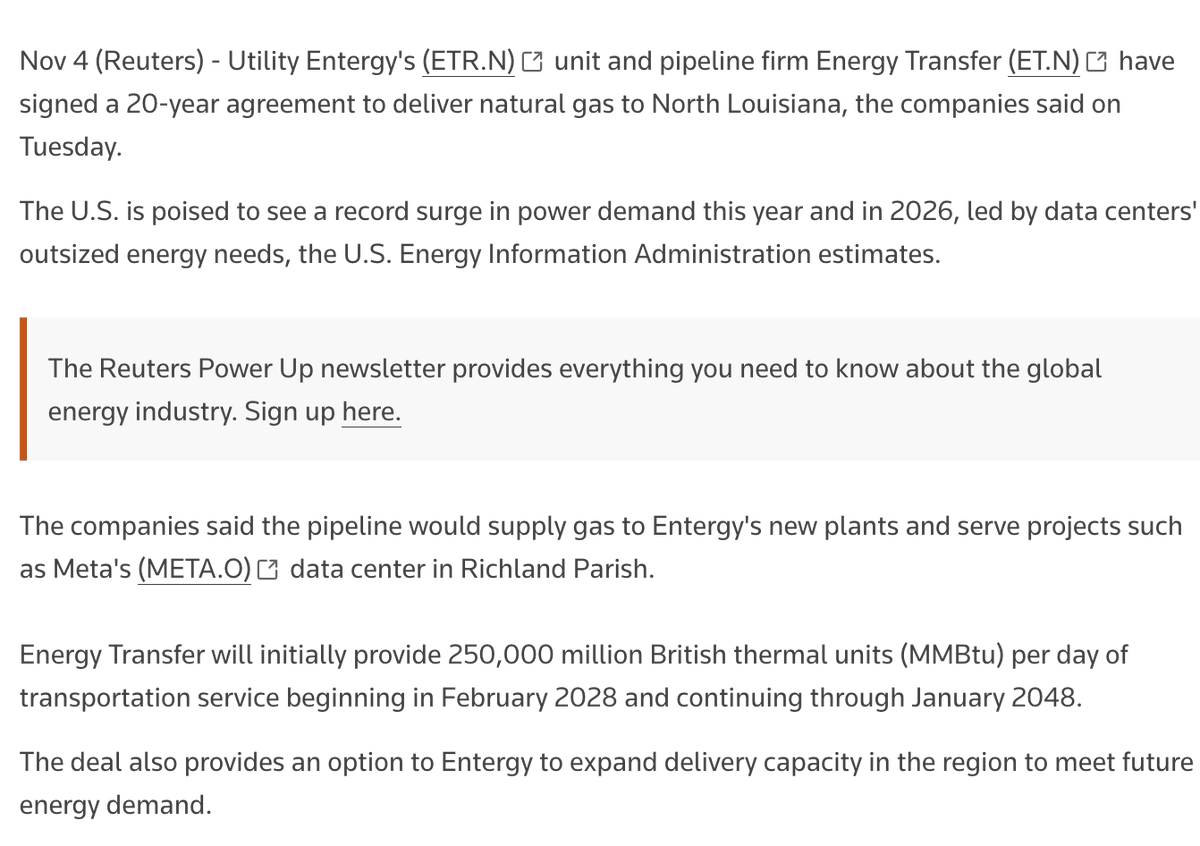

$ET is quietly becoming the backbone of AI energy few are talking about yet.

Energy Transfer has signed 6 Bcf/d in data center gas deals in the last year:

🔹 Oracle — 900K Mcf/d across 3 campuses, already delivering to Abilene TX

naturalgasintel.com/news/ene…

🔹 Fermi America — 10-year deal powering an 11 GW AI HyperGrid campus in Amarillo TX, one of the largest planned in the US

datacenterdynamics.com/en/ne…

🔹 Entergy Louisiana / Meta — 20-year deal supplying gas for Meta's hyperscale AI data center in Richland Parish via Tiger Pipeline

energytransferfacts.com/blog…

🔹 CloudBurst — Long-term supply to a 1.2 GW AI-focused campus in central TX

🔹 VoltaGrid — Fueling 2.3 GW for Oracle's AI campuses

US data center capacity is expected to go from 24 GW → 100 GW by 2030.

AI doesn't run on vibes. It runs on natural gas. And $ET has 140,000 miles of pipeline feeding it.

This is the picks-and-shovels play, sleeper pro max.

May 27

I aped a huge amount of Nokia $NOK OTM leaps and oh boy it achieved to my wildest imaginations lmao.

Energy Transfer $ET is a huge sleeper for the AI energy bull run.

At $19 something, option contract leaps still dirt cheap, already stacking AI data center partnerships across the country.

✅ Oracle: supplying 900 MMcf/d of natural gas to 3 data centers, already flowing gas to Abilene TX campus

naturalgasintel.com/news/ene…

✅ VoltaGrid x Oracle: powering 2.3 GW of AI data center infrastructure through ET's pipeline network

pgjonline.com/news/2025/octo…

✅ Fermi America: 10 year deal supplying 300,000 MMBtu/d to the HyperGrid AI campus in Amarillo TX

energytransferfacts.com/blog…

✅ CloudBurst Data Centers: up to 450,000 MMBtu/d, enough to generate 1.2 GW of behind the meter power for their AI campus in San Marcos TX

ir.energytransfer.com/news-r…

✅ Entergy Louisiana (powering Meta's $27B hyperscale data center): 20 year deal for 250,000 MMBtu/d via Tiger Pipeline

1012industryreport.com/oil-g…

✅ 140,000 miles of pipeline across 44 states

✅ Q1 2026 EBITDA up 20% YoY

✅ Raised full year guidance to $18.2B $18.6B

✅ ~7% distribution yield with 3 5% annual growth target

✅ Jefferies just upgraded today

I'm buying a huge bulk amount of OTM option contracts, relax and enjoy coming back a year later.

It's either a mansion or I don't give a fuck just a macbook pro's cost.

1

3

747

🏆Top 20 future-focused asymmetric setups dominating the AI Space Nuclear Autonomy trade.

These aren't yesterday's winners. These are tomorrow's compound machines.

🥇 1/ $SIVE/ $SIVEF - Sole CW DFB laser source for ALL CPO winners. U.S.-Sweden TPD signed. MSCI inclusion May 29.

🥈 2/ $IREN - $NVDA $2.1B warrants at $70. $9.7B Microsoft $3.4B NVIDIA $5.8B Dell. 5GW power moat.

🥉 3/ $EOSE - Cerberus 32% extended lock-up. $24.3B pipeline. Non-flammable chemistry mandatory for hyperscale.

⚛️ 4/ $IONQ - Q1 755% YoY. RPO $470M. Missile Defense Agency AWS/Azure/Google integrated.

🚀 5/ $RKLB - Backlog $2.2B doubled YoY. DoD $190M HASTE. Confidential customer 5 Neutron 3 Electron through 2029.

📡 6/ $ASTS - 3,900 patents 1,100 MHz spectrum irreplaceable. 60 MNO partners. 3B subscribers. FCC authorized.

🔬 7/ $AAOI - $200M single 1.6T order. $324M backlog. Mediacom DOCSIS 4.0. Vertical integration moat.

⚗️ 8/ $ASPI - Fermi America 11 GW HyperGrid. European reactor MOU. Multi-vertical: HALEU medicine helium quantum.

☢️ 9/ $IMSR - Standard LEU fuel = no HALEU dependency. Riot Platforms MOU. 7.8 GW pipeline.

🛡️ 10/ $ONDS - Q1 1,065% YoY. $457M backlog. DoD-aligned defense rail drones.

🧠 11/ $PENG - AI biz >60% revenue. Memory inflection 53% YoY. Nokia exec joins board.

🚛 12/ $AUR - NVIDIA Volvo PACCAR partnerships. Hirschbach 500-truck deal 2027. $1.28B cash.

⚡ 13/ $DGXX - Cerebras $1.1B 10-year contract. Q1 EBITDA POSITIVE. Zero debt.

⚙️ 14/ $NVTS - Official NVIDIA 800V partner. GaN SiC. Powers Kyber Rubin Ultra.

📺 15/ $HLIT - 95% market share virtualized cable. $582M backlog ( 87% YoY).

☀️ 16/ $TE - First profitable quarter continuing ops. Q1 232%. G2_Austin Phase 1 Q4 2026.

🔋 17/ $IQEPF - MACOM £45M strategic investment board seat. Lazard Strategic Review.

📊 18/ $WYFI - Phase 2 billing starts MAY 30. NC-1 99MW operational. $160M Paris B300 deal.

💎 19/ $ADEA - Q1 beat 13.5%. Recurring royalty IP model. Multi-vertical licensing.

🔌 20/ $CRDO - Q3 FY26 201% YoY ($407M). DustPhotonics silicon photonics acquisition. >$500M FY27 optical revenue.

THREE KEY REASONS THESE LEAD:

1️⃣ STRUCTURAL CHOKEPOINTS capital can't solve. Pricing power compounds.

2️⃣ INSTITUTIONAL ANCHORS validating the thesis — NVIDIA, Cerberus, MACOM, Microsoft, DoD, AWS Azure Google, Cerebras, Hirschbach.

3️⃣ CONTRACTED REVENUE VISIBILITY through 2029 — $9.7B $3.4B $1.1B $2.2B $1.2B $24.3B in stacked commitments.

The AI infrastructure capex cycle is feeding through compute, storage, power, packaging, launch, comms, and autonomy SIMULTANEOUSLY.

Position for the chokepoint compound. Hold through the multi-year inflection.

This is how generational wealth gets built.📈

9

12

60

5,578

🚨 The Top 20 future-focused ASYMMETRIC setups dominating the AI Space Nuclear Autonomy chokepoint trade. 🔥

These aren't yesterday's winners.✅

These are tomorrow's compound machines.✅

Here's the full institutional stack:

🥇 1/ $SIVE / $SIVEF - The Photonics Chokepoint

Sole-source CW DFB lasers for ALL leading CPO winners (Ayar, Celestial, Lightmatter, $POET).

→ U.S.-Sweden TPD signed May 22

→ MSCI Sweden Small Cap inclusion May 29

→ Customers ramping production simultaneously 2026-2028

Architecturally unique. Multi-customer locked. Pricing power compounds.

🥈 2/ $IREN - AI Power Compute Vertical Integration

$NVDA holds $2.1B warrants at $70 strike (above current price).

→ $9.7B Microsoft $3.4B NVIDIA $5.8B Dell signed

→ 5GW global power secured (NA Europe APAC)

→ Owns power AND data centers (vertical moat)

Market still calls it a "Bitcoin miner." Repricing imminent.

🥉 3/ $EOSE - Long-Duration Storage Bottleneck

Non-flammable zinc chemistry lithium can't replicate at hyperscale data centers.

→ Cerberus 32% holder extended lock-up YE 2026

→ $24.3B pipeline ( 56% YoY), $644.6M backlog

→ Frontier Power USA structure $1.5B Ariel Green insurance

The ONLY genuine 🟢 in the entire 800V power trade.

⚛️ 4/ $IONQ - Quantum Institutional Anchor

Q1 revenue 755% YoY. RPO $470M ( 554% YoY).

→ Missile Defense Agency SHIELD IDIQ contract

→ AWS Azure Google Cloud directly integrated

→ SkyWater acquisition = vertical chip integration

Defense commercial cloud all anchored simultaneously.

🚀 5/ $RKLB - Space Launch Infrastructure Compound Machine

Backlog $2.2B (doubled YoY). Q1 revenue $200M record.

→ DoD $190M HASTE 20 hypersonic flights

→ Confidential customer: 5 Neutron 3 Electron through 2029

→ Motiv Space Systems acquisition (Mars-proven robotics)

Trump Golden Dome tailwind. Vertical aerospace platform.

📡 6/ $ASTS - Space-Cellular Direct-to-Device Chokepoint

~3,900 patents 1,100 MHz tunable MNO spectrum = irreplaceable IP.

→ 60 MNO partners covering 3B subscribers

→ $1.2B contracted revenue commitments

→ FCC commercial authorization received

Direct-to-device from space. Spectrum IP combination impossible to replicate.

🔬 7/ $AAOI - Optical Transceiver Hyperscaler Anchor

Q1 revenue 51% YoY. Vertical integration laser→transceiver.

→ $200M single 1.6T transceiver order

→ $324M backlog with hyperscaler anchors

→ Mediacom DOCSIS 4.0 multi-year partnership

U.S. manufacturing scale (CHIPS Act aligned). 1.6T ramp H1 2027.

⚗️ 8/ $ASPI - Multi-Vertical Isotope Picks-and-Shovels

Proprietary Aerodynamic Separation Process tech across multiple verticals.

→ Fermi America 11 GW HyperGrid Texas

→ European reactor MOU May 11, 2026

→ HALEU medicine helium LNG quantum isotopes

Sells enrichment tech to whoever wins. Doesn't need to pick reactor winners.

☢️ 9/ $IMSR (Terrestrial Energy) - Nuclear "No HALEU" Advantage

Standard LEU fuel = supply chain MOAT vs every Generation IV competitor.

→ Riot Platforms MOU for data center co-located nuclear

→ 7.8 GW aggregate pipeline (~10 IMSR Plant projects)

→ NRC PIE Topical Report approved May 12

The reactor that's already solved fuel supply other reactors can't.

🛡️ 10/ $ONDS - Defense Drone Inflection

Q1 revenue 1,065% YoY. FY26 guide raised to $390M .

→ $457M backlog stacking

→ Defense rail autonomous drones dual exposure

→ DoD-aligned positioning at scale

Real revenue inflection at sub-$2B mcap.

🧠 11/ $PENG - AI Inference Memory Bottleneck

AI-driven biz >60% of H1 FY26 revenue ( 50% YoY).

→ Integrated memory $308M ( 53% YoY)

→ MemoryAI CXL-based KV cache servers deploying

→ Nokia exec David Heard joins board May 18

Memory is the inference bottleneck. PENG owns the layer.

11

32

131

13,274

May 24

Please join us for our weekly Kitely Community Meeting today, May 24 at 1 PM PDT. Meet new friends, learn what's new, share & ask questions. Everyone is welcome! We hope to see you there! 👋

TP to Welcome Center: bit.ly/KitelyWelcome

#opensim #hypergrid

2

2

26

The nuclear thesis everyone is getting backwards:

You don't have to pick which reactor wins.

You pick the company selling fuel to ALL of them.

$ASPI is the only Western pure-play with proprietary laser-based HALEU enrichment technology.

$OKLO , X-Energy, TerraPower, NuScale - every Gen IV reactor needs HALEU.

$ASPI's customer pipeline:

→ TerraPower (Bill Gates): term loan 10-year supply agreement

→ Fermi America: Texas HALEU facility at 11 GW HyperGrid campus

→ European nuclear partner: HALEU deliveries 2028-2036 (signed May 11)

→ Necsa: South Africa Pelindaba site agreement

→ $30B in customer demand interest disclosed

The miners are still arguing over who strikes gold.

$ASPI is already selling shovels.🚀

2

5

28

2,958

May 15

Major data center projects are actively starting or being proposed across the USA to meet AI demand, with major hotspots in Northern Virginia, Texas, Ohio, and Arizona. Key developments include a 540 MW campus in Hale County, TX (Project Caprock), a $20B, 795-acre site in Joliet, IL, and 15 new Microsoft data centers at the former Foxconn site in Mount Pleasant, WI.Key Data Center Projects & Locations (2026):Texas:Hale County: Aligned Data Centers is building the 313-acre, 540 MW "Project Caprock".Milam County: OpenAI/SB Energy is developing a 1.2 GW data center.El Paso: Meta is investing over $1.5B in a GW-scale data center.Amarillo: Fermi America is planning "Hypergrid," an 11 GW campus.Dallas: Crow Holdings is developing a 245 MW campus on 40 acres.Midwest & Eastern U.S.:Joliet, Illinois: A $20B, 795-acre "Joliet Technology Center" (PowerHouse/Hillwood) was approved.Mount Pleasant, Wisconsin: Microsoft is building 15 data centers at the old Foxconn site.Indiana: Meta is building a 1 GW, $10B campus in Lebanon. Amazon completed an $8B, 30-site project ("Project Rainier").Ohio: Central Ohio is experiencing massive expansion, with significant data center developments occurring near Columbus.Pennsylvania: The "Homer City Energy Campus" is set to become a 4.5 GW facility.Maryland: AWS is evaluating a campus near the Calvert Cliffs nuclear power plant.Western U.S.:Wyoming: Microsoft is acquiring ~3,200 acres in Cheyenne.Utah: A 6,000 MW "Stratos Project" is planned in Box Elder.Nevada: Google is adding 150 MW of geothermal-powered capacity.Federal Lands (DOE Sites):The Department of Energy has identified 16 sites for AI data centers, including Idaho National Laboratory, Oak Ridge Reservation (TN), Paducah Gaseous Diffusion Plant (KY), and Savannah River Site (SC).Key Trends & Hotspots:Top Markets: Northern Virginia leads with 329 data centers, followed by Phoenix (48) and Dallas-Fort Worth.Power-Hungry: New projects are focused on extremely high power capacity, with many campuses targeting 1–6 GW, driven by AI.Energy Partnerships: Companies are increasingly co-locating with, or investing directly in, nuclear power (e.g., TerraPower, Oklo, Vistra)

1

2

76

May 14

Don’t miss the next $OKLO

Up ~22% today off AI data center hyperscaler speculation

I give you $FRMI

AI infrastructure supercycle is accelerating.

Power compute data centers = the real bottleneck of the AI era.

THIS IS A POTENTIAL NEXT-GEN AI POWER INFRASTRUCTURE MONSTER IN EARLY STAGE FORM

100$ STOCK CHILLING AT 7$

~$3.8B market cap

~$243M cash restricted cash

~$1.4B infrastructure already deployed

~$421M debt vs ~$1.07B equity

~$785M new financing secured in Q1

Pre-revenue but already scaling aggressively

Up big today on:

• Earnings call

• Hyperscaler tenant momentum

• AI power demand narrative

• Potential major tenant deal within 90 days

@Flowgod spotted:

~$1.5M unusual 15c activity yesterday 😉

THIS IS THE MOMENT THE STORY CHANGES

Legacy energy development → vertically integrated AI HyperGrid™ infrastructure platform

Same category rotation setup as:

$OKLO $APLD $IREN $NBIS

Why this is getting attention:

~7,570 acre Project Matador mega-campus in Texas

Up to ~17 GW long-term power ambition

~15–18M sq ft AI-ready hyperscale capacity

~2 GW already secured/contracted

~6 GW air permit secured from TCEQ

Additional ~5 GW permit expansion filed

First commercial power targeted in 2026

This is not just a data center company.

This is:

POWER LAND COMPUTE NUCLEAR GAS BESS REIT STRUCTURE

Behind-the-meter private grid model means:

NO waiting 3–7 years for public utility interconnect queues

That’s the entire edge.

FRMI is building:

• Natural gas generation

• Advanced nuclear expansion

• Solar battery storage

• AI hyperscale campuses

• Long-duration infrastructure leases

And they’re doing it all in one hardened Texas location.

Project Matador advantages:

• Adjacent to major gas basin

• Massive water access via Ogallala Aquifer

• Fiber connectivity

• Existing transmission connectivity

• Large-scale contiguous land package

• Designed specifically for hyperscaler AI demand

Infrastructure already underway:

• First 6 Siemens SGT-800 turbines delivered

• Gas lines installed

• Water systems built

• Transmission systems connected

• FEED work underway for nuclear

• NRC EIS pilot participation accelerating process

This is basically:

“Build your own AI power city.”

Commercial momentum:

Management said hyperscaler neo-cloud engagement accelerated materially

Recent site visits increasing

Potential long-term agreements expected within next 90 days

THAT is what the market is reacting to.

Fermi 2.0 reset:

• New chairman Marius Haas

• Permanent CEO search underway

• Institutional scaling focus

• Dallas HQ expansion

• Focus on disciplined execution tenant monetization

The comparisons everyone keeps making:

Closest analog:

$OKLO

Other comps:

$APLD

$VST

$CEG

$EQIX

$DLR

But FRMI is attempting something bigger:

PRIVATE POWERED AI CITIES

Bull case:

AI compute demand explodes

Public grids cannot keep up

Hyperscalers need immediate dedicated power

FRMI becomes one of the first scaled private AI power campuses in America

This is HIGH RISK.

But if execution hits…

THIS COULD BE ONE OF THE BIGGEST AI INFRASTRUCTURE RE-RATINGS OF THE CYCLE

Big picture:

AI demand is exploding

Power shortages are real

Hyperscalers are scrambling

The next trillion-dollar bottleneck is electricity

And the companies solving power first…

Will own the next phase of AI.

$FRMI is very early.

That’s the opportunity.

$NVDA $AMD $SMCI $VST $CEG $OKLO $APLD $NBIS $IREN $CRWV $EQIX $DLR $FSLR $SMR $TLN $ETN $GEV $ANET $ARM $VOO $SPY

DONT MISS THIS GIANT

39

23

267

48,405

May 10

Please join us for our weekly Kitely Community Meeting today, May 10 at 1 PM PDT. Meet new friends, learn what's new, share & ask questions.

Everyone is welcome! We hope to see you there! 👋

TP to Welcome Center: bit.ly/KitelyWelcome

#opensim #hypergrid

2

2

29

May 7

5700 acre hypergrid data center in TX "the largest nuclear power complex in America" with four nuclear reactors and several small modular reactors x.com/itsBexarzy/status/2041…

x.com/itsBexarzy/status/2051…

JBSA named the third potential site for a Department of the Air Force nuclear microreactor

x.com/usairforce/status/2046…

May 6

Under an Executive Order & Dept of Energy, they are actually labeled as hypergrid critical defense facilities with nuclear reactors. whitehouse.gov/fact-sheets/2…

Pressurized water H20 (or D20 aka heavy water) neutron moderators are used for cooling.

1

4

5

1,347

May 6

Under an Executive Order & Dept of Energy, they are actually labeled as hypergrid critical defense facilities with nuclear reactors. whitehouse.gov/fact-sheets/2…

Pressurized water H20 (or D20 aka heavy water) neutron moderators are used for cooling.

1

2

1,475

Le fonti rinnovabili sono sempre più centrali per il futuro energetico del Paese. Per integrarle serve una rete più moderna, efficiente e a ridotto impatto ambientale.

Con #Hypergrid, Terna avvia un grande progetto di ammodernamento della rete elettrica nazionale: nuove dorsali e collegamenti sottomarini in corrente continua, affiancati alla valorizzazione delle infrastrutture esistenti.

La Dorsale Adriatica è un tassello fondamentale di questa strategia: un collegamento in gran parte sottomarino e invisibile che unirà Puglia ed Emilia‑Romagna, aumentando capacità di trasporto, flessibilità ed efficienza del sistema a sostegno della transizione energetica.

Guarda il video per scoprire di più.

1

3

9

308

The Grid is the New Frontier: Managing the AI Power Surge. AI isn't just a software challenge; it's a power challenge. Richard Rys explores how LTTSGridEye™ by L&T Technology Services is solving the "Hypergrid" bottleneck........

Read More - industrialautomationindia.in…

1

32

Apr 30

Hypergrid — 11 GW

Stargate Abilene — 1.2 GW

Hyperion — 5 GW

Project Jade — 10 GW

Project Rainier — 2.2 GW

Stargate UAE — 5 GW

Google India Hub — 1 GW

Vantage Frontier — 1.4 GW

SoftBank Ohio Campus — 10 GW

They are not setting up a cyber cafe. They want building infrastructure.

3

1

10

934