⎐كُـود⎐كوبِون⎐خـِصم⎐

⎐ايهرب⎐ايهيرب اهرب

⊵GCA5893⊴

⎐نون⎐

⊵S3Q⊴

⎐نمشي⎐

⊵AABN⊴

⎐باث▬اند▬بودي⎐

AB6K⊴

⎐ناتشورال ⊴تاتش⎐

⊵C37⊴

⎐فوغا⎐كلوسـيت⎐

⊵V1⊴

⊴ماكـس ⊴

⊵A9B⊴

___

IbEO

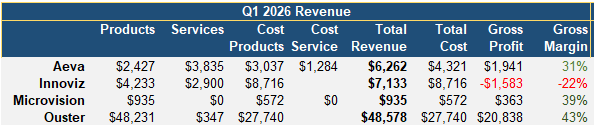

📡 All Western LiDAR companies have now reported, and the numbers once again confirm what has been obvious for years: $AEVA, $INVZ, and $MVIS remain development-stage science projects compared to the commercial scale of $OUST.

📈 Product revenue tells the story:

• $INVZ: $4.2M product revenue

• $AEVA: $2.4M product revenue

• $MVIS: roughly $300K from former Ibeo products ~$600K tied to Luminar programs

• $OUST: $48M product revenue

💰 Gross margin percentages can mislead at first glance. In absolute dollars, Ouster generated roughly 28x more gross profit than the other three combined, helped by Innoviz posting negative gross profit.

🏦 Yet $AEVA still commands a $1.3B valuation. Innoviz shareholders have reason to be frustrated: a company generating ~$7M in revenue trades near a $160M market cap, while another generating ~$6M trades at a billion-dollar valuation.

🤝 The difference comes down to market perception, Sylebra ownership, LG Innotek backing, and investor willingness to fund the story. Meanwhile, Innoviz continues relying on ATM dilution near 60 cents.

⚠️ Despite partnerships, announcements, and new product launches, Innoviz still depends heavily on NRE revenue. Without it, the business model appears increasingly challenged.

🎯 The market is betting that Aeva eventually succeeds while largely giving up on Innoviz.

4

1

26

3,524

The market is treating $MVIS like a struggling pre-revenue hardware firm with a ticking debt clock. The reality is they just quietly executed a distressed rollup masterclass—buying up the core IP of failed rivals like Luminar and Ibeo for pennies on the dollar. Armed with 735 patents and a strict non-Chinese supply chain, this is no longer just an automotive tech bet; it’s a binary geopolitical play on the consolidation of Western sensing architecture. ♟️ #Lidar #AutonomousVehicles

auth.flash.stocksentinel.ai/…

2

449

May 3

The way he slightly opened his jacket while singing ‘Nae geo ibeo hudi yujihae geori~~’ 😭🫠

ZiZi

ZiZi

15

48

411

🚨Heads-up to an economic history meeting in the wonderful Sardinia:

CfP: 15th IBEO Workshop - Economic History Annual Meeting

... 🌏 Alghero

📆July 9, 2026

The submission deadline is April 20

To submit your paper: crenoslef.wixsite.com/ibeo/a…

More info: associazionestoriaeconomica.…

5

6

482

Feb 27

O sea ¿La ibeo no contrató a gente profesional para armar bien ese templete?

3

250

Honored to be invited to deliver the Keynote Lecture in health economics at the XV IBEO Workshop in Corsica, June 10-12 2026

📢 Submissions are open

crenoslef.wixsite.com/ibeo/c…

4

102

Feb 13

$MVIS @MicroVision just turned the lidar graveyard into its own empire.

First Ibeo (perception software flash lidar, 2023), then Scantinel (FMCW 1550nm long-range tech, late 2025), and now Luminar assets out of bankruptcy (Iris Halo sensors, IP, talent, contracts for $33M in 2026).

While others burned billions and folded, MVIS quietly consolidated the best pieces like scanning FMCW proven automotive contracts into one powerhouse.

@naval is right: uncoordinated tribes get wiped out. Organized ones eat the field.

The lidar consolidation era is here, and MicroVision is the last one standing tall.

Who’s next? 🚀📡 $MVIS

#LiDAR #Autonomy #MVIS #Consolidation

1

22

683

Feb 4

🚨 $MVIS Speculation Corner: What if the Luminar asset scoop ($33M for IRIS/Halo talent/contracts from bankruptcy) was just the opening move apart from IBeo and Scantinel?

Here’s a wild thought , could MicroVision be quietly setting up for another acquisition play?

Two targets that keep circling my head .. 👇

1️⃣ LeddarTech : insolvency (filed June 2025), ops shut down. What if $MVIS carve out their lidar IP perception/fusion stack?

2️⃣ Voyant Photonics : not distressed; actually thriving. Their Helium™ chip-scale FMCW prototypes (fresh off CES 2026 buzz) Carbon™ lineup heading to production. Silicon photonics FMCW with per-pixel velocity ultra-compact design… total synergy potential with Scantinel , if price/timing align?

Big picture: As China floods the low-end and Western lidar peers bleed cash, $MVIS might be quietly building a versatile perception portfolio via selective, opportunistic buys , not billion dollar R&D burns.

Totally speculative. No filings, no rumors … just pattern-watching and theory-crafting.

What’s your take?

🔹 LeddarTech fire-sale assets next?

🔹 Voyant as future FMCW fit?

🔹 Or something else entirely?

DYOR, not advice 🚀

#Lidar #Autonomy #Speculation

1

22

544

Feb 3

candu banget part jake geo ibeo hudi sama part jungwon di ending 😭🫰🏻

1

36

2,290

14 Oct 2025

Ein LiDAR-System ist nicht von einer einzigen Firma, da es sich um eine Technologie handelt, die von vielen verschiedenen Unternehmen entwickelt und eingesetzt wird. Der ursprüngliche Prototyp stammt von der Hughes Aircraft Company aus dem Jahr 1961. Heutzutage gibt es zahlreiche Hersteller und Anwendungsbereiche, wie beispielsweise die Volvo-Partnerschaft mit Luminar für das autonome Fahren, die Microvision-Übernahme von Ibeo, sowie die Nutzung durch Fraunhofer IPMS und Cepton Technologies für die Entwicklung von Sensoren.

Es gibt auch LiDAR von/mit BrainChip.

1

2

46

28 Sep 2025

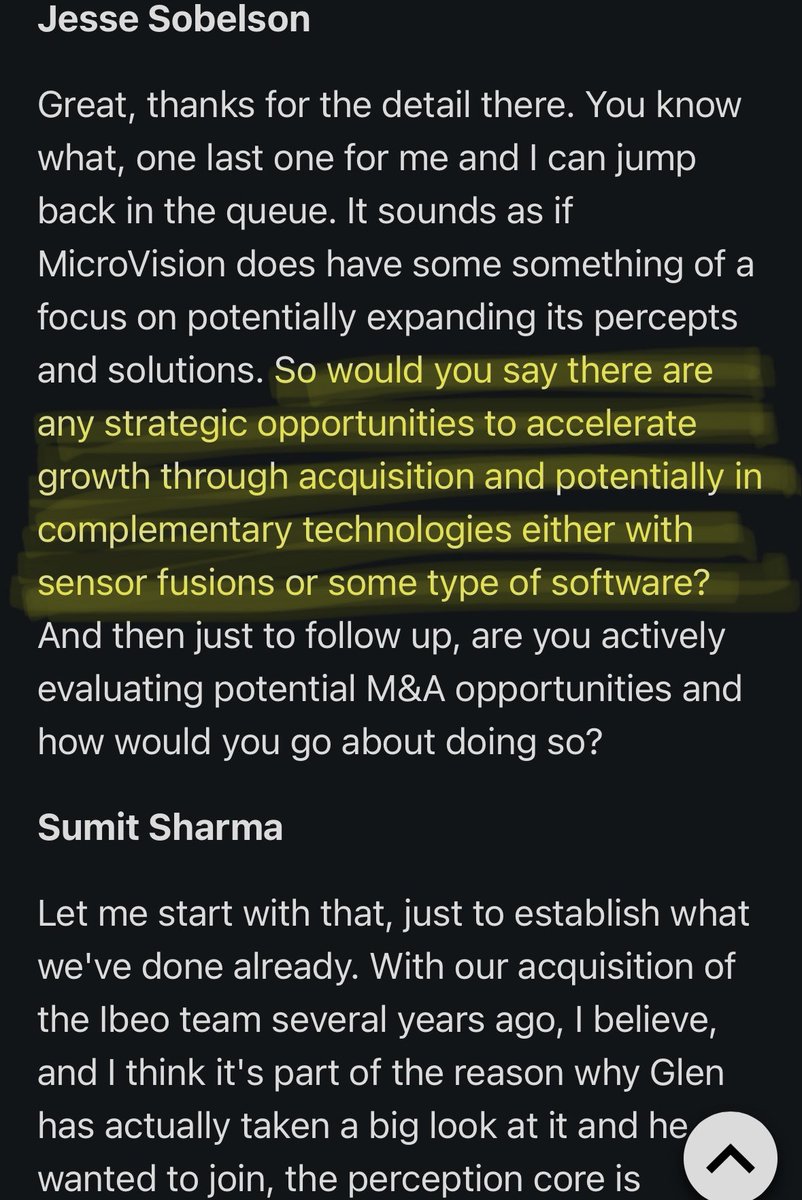

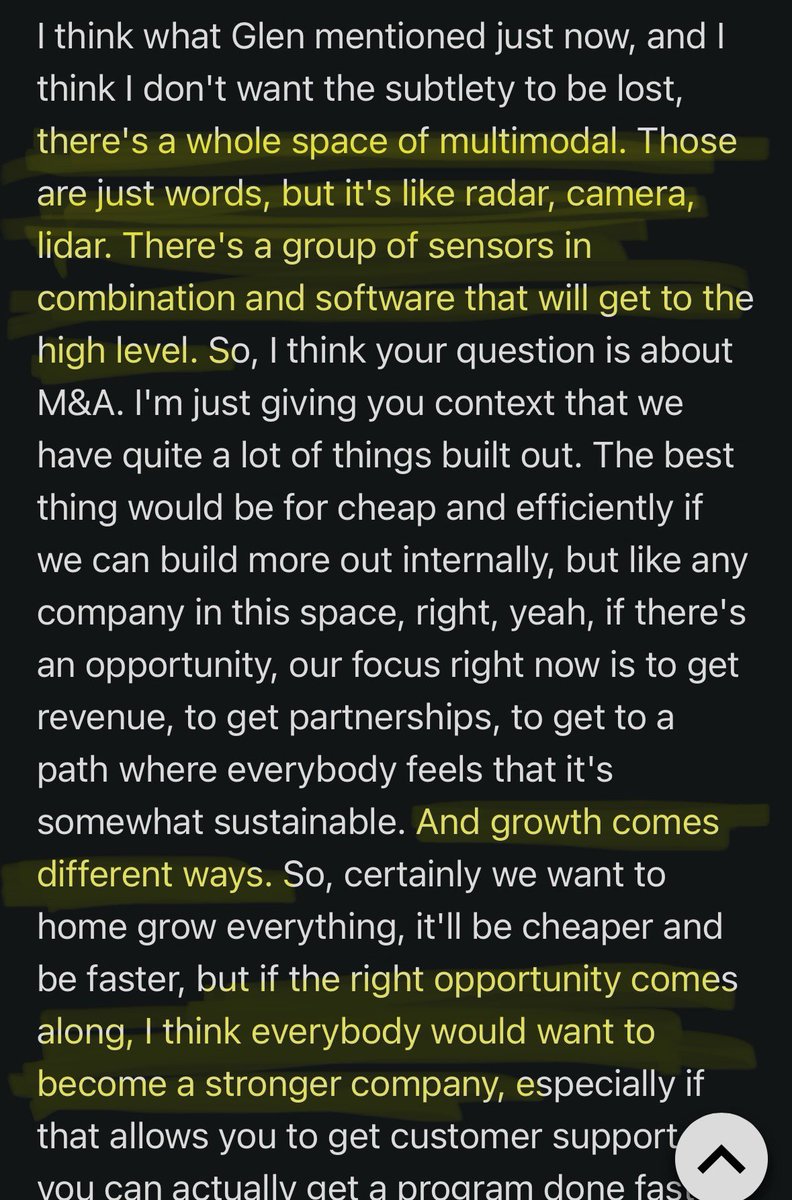

$MVIS 4Q 2024 EC transcript

Question about further M&A

Maybe it’s not Luminar, perhaps AEye, but adding a 1550nm long range sensor, and/or radar and camera capabilities seems like the next step in growth, no? To “build a full solution?”

Glen (who came to MVIS with a background in radar) also talks about looking at all technologies for Gen 2 of tri-LiDAR in his most recent press conference. 16:55 min mark

youtu.be/JnpVWAmyYM4?feature…

Seems like we might see MicroVision make another Ibeo type of move in the not too distant future.

8

2,281

14 Jun 2025

만일 라이다가 정말 미래 자율주행과 휴먼로이드 로봇에 필수 부품이라면 벌써 대기업들이 뛰어 들었어야 하고 활발히 M&A가 이루어져야 할텐데…🤔

(Grok)

아래는 라이다(LiDAR)를 설계하는 주요 기업들의 이름, 국가, 위치만 간략히 리스트업한 표입니다.

• Velodyne LiDAR - 미국 - 캘리포니아

• Luminar Technologies - 미국 - 플로리다

• Innoviz Technologies - 이스라엘 - 텔아비브

• Ouster - 미국 - 캘리포니아

• Aeva Technologies - 미국 - 캘리포니아

• Cepton Technologies - 미국 - 캘리포니아

• Hesai Technology - 중국 - 상하이

• RoboSense - 중국 - 선전

• LeddarTech - 캐나다 - 퀘벡

• Leica Geosystems - 스위스 - 헤르브루크

• Quanergy Systems - 미국 - 캘리포니아

• Baraja - 호주 - 시드니

• Livox - 중국 - 선전

• Teledyne Optech - 캐나다 - 온타리오

• Sick AG - 독일 - 발트키르헨

• RIEGL Laser Measurement Systems - 오스트리아 - 호른

• FARO Technologies - 미국 - 플로리다

• Waymo - 미국 - 캘리포니아

• AEye - 미국 - 캘리포니아

• Ibeo Automotive Systems - 독일 - 함부르크

• Benewake - 중국 - 베이징

• Innovusion - 중국/미국 - 상하이/캘리포니아

• Lumotive - 미국 - 워싱턴

• Analog Photonics - 미국 - 매사추세츠

• SOS Lab - 한국 - 광주

14 Jun 2025

이거 보면 웨이모의 태생적, 기본적 한계가 명확히 드러남. 웨이모는 지금 기술로는 안정적으로 산길을 달리지 못함. 그 산길 말고 다른 길을 선택하여 해도 고속도로라 갈 수 없음. LA에서도 마찬가지.

LA 웨이모 운행 지역: x.com/bogusjack/status/18653…

그러면, 과연 HD Map이 없어서 못 가는 걸까? No. Safety를 고려할 때 불안정해서임. 만일 기술적으로 안정되었다면 상대적으로 오래전에 런칭한 샌프란, 피닉스 등에서 이미 해결되었어야만 함. 논리적으로.

그런데, 웨이모는 그 부분도 개발하고 있다하지만, 코어 도시로만 확장 중. Business Development 관점에서 보면 이건 경쟁사이 치고 달리니 급한 나머지 할 수 있는 부분만이라도 확장하자는 의미. 불완전한 확장이지.

그렇다면, 웨이모는 왜 산길이나, 골목길, 하이웨이를 달리지 못할까? 난 그 이유가 라이다라고 봄. 아무래도 3D 데이터다 보니 좁고 구불구불한 산길, 좁은 골목길, 빠른 하이웨이에서 직관적으로 저건 뭐다라고 판단할 때 우리는 눈으로 인지하지만은 대략적인 것만 보고도 뇌로 “아 저거지”라고 빨리 판단해서 대응하는데, 라이다를 가지고 아무리 정교한 3D 데이터를 생성한다 해도 상대적으로 시간이 0.1~2초라도 더 소요된다면 그건 자율주행에서 치명적임.

이 부분이 해결이 안되었기 때문에 아직까지도 먼저 시작한 샌프란이나 피닉스, LA에서 산길, 골목길, 하이웨이를 달리지 못하는 것이라 봄. 이게 사실이라면 치명적인 단점이고 고성능 반도체 칩의 개발이 반드시 뒤따라야만 함. 그러면, 시간이 늦음.

그냥 개인적 의견.

16

9,750

3 Jun 2025

On last monday 26th May, I presented part of my work - coauthored with @claudio_detotto and @biancabiagi - at the XIV IBEO Workshop in Corte. A heartfelt thank you to all the colleagues who attended the session and shared a feedback!!!

@UnivCorse @umrlisa @crenos_sardegna

5

371

26 May 2025

Kickoff of the 14th IBEO workshop in Corte — let's go! 🎉

@TorreAndr @biancabiagi @umrlisa @crenos_sardegna

2

59

Back then, optimism fueled a boom in startups and IPOs. But Level 3 autonomy never arrived. LiDAR development proved extremely expensive, and as interest rates rose, the industry—already drowning in red ink—was hit hard. Massive layoffs followed.

In 2022, Ford and Volkswagen shut down their joint venture Argo AI. Germany’s Ibeo and America’s Quanergy Systems filed for bankruptcy. Even Velodyne, once an industry leader, merged with competitor Ouster in 2023.

Of the 80 companies in the vehicle LiDAR space around 2020, fewer than 20 remain. Survivors like Luminar—once hailed for making its founder Austin Russell the youngest self-made billionaire—have suffered. Luminar’s stock, which peaked at $71.70 in December 2020, now trades at $3.63—a -99.5% drop. Innoviz has seen a similar collapse.

1

22

3,991

10 Mar 2025

🚨Last chance! Only 5 days left to submit!🚨

XIV WORKSHOP #IBEO, Corsica (Corte🇫🇷), 26–28 May

Topics

-Urban & Regional Economics

-Health Economics

-Sustainable Tourism

Submission deadline: 15 March

crenoslef.wixsite.com/ibeo/c…

@biancabiagi @TorreAndr @lciuccipoggi @crenos_sardegna

2

6

245