Christoph Lütge retweeted

📺 Watch IEAI Director Christoph Lütge's Q&A with the alignAI Doctoral Network: youtu.be/GqEAVFzJrpE

#alignAI #IEAI #TUM #MSCA #HorizonEurope #DoctoralNetworks #TRAIF2026

2

3

202

Jun 15

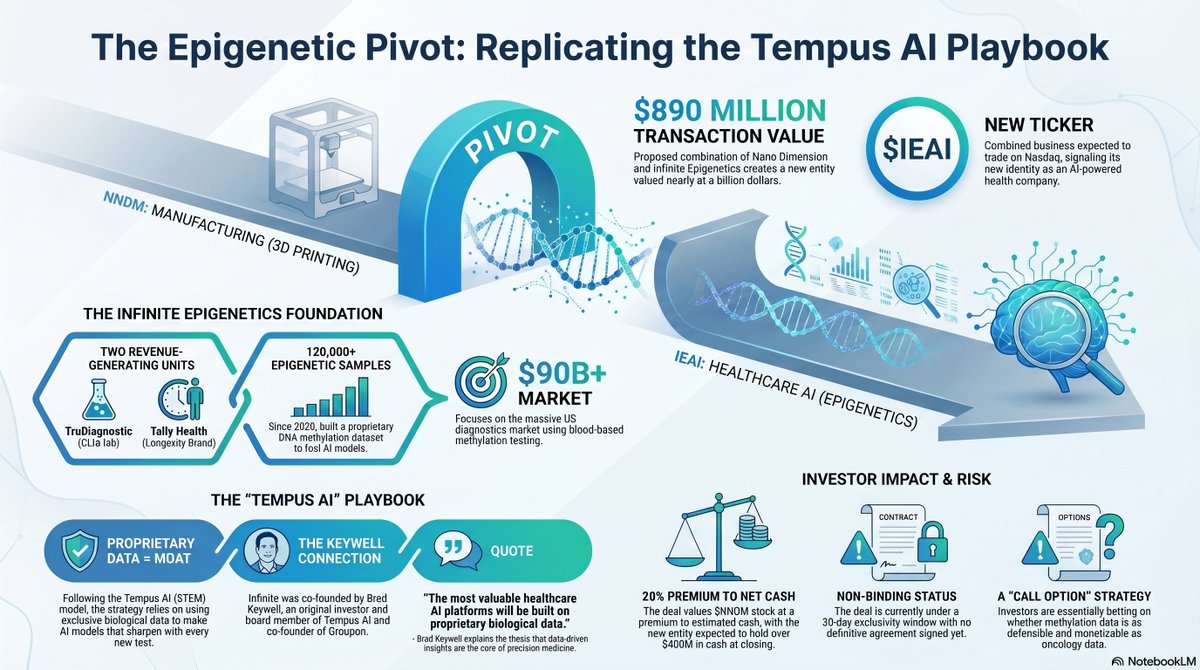

A 3D-printing company turning into a healthcare AI company. Whose playbook this is, and it is the $TEM AI playbook, brought by one of $TEM 's own early backers.

$NNDM signed a non-binding term sheet to combine with Infinite Epigenetics, an AI-powered preventive health and diagnostics company, at an $890 million transaction value. The combined business would trade on Nasdaq under the proposed ticker $IEAI. Infinite is built on two real revenue-generating units, the CLIA lab TruDiagnostic and the longevity brand Tally Health, with more than 120,000 epigenetic samples collected since 2020 and a proprietary DNA methylation dataset aimed at a $90 billion plus US diagnostics market.

Infinite was co-founded by Brad Keywell, an original investor and board member of $TEM AI and Eric Lefkofsky's longtime partner from the Groupon and Lightbank years. $NNDM 's own deck names the template in plain sight: Exact Sciences ($EXAS) proved molecular diagnostics can scale in public markets, GRAIL ($GRAL) validated methylation testing from blood, and $TEM proved that proprietary clinical data plus AI can create a brand new category in precision medicine.

Keywell put the thesis directly. Brad Keywell, co-founder of Infinite Epigenetics and an original investor and board member of $TEM , said: "We believe the most valuable healthcare AI platforms will be built on proprietary biological data, leveraging AI for novel discoveries and insights."

That sentence is the entire Tempus model. $TEM came public in June 2024 at $37 a share and built a moat out of data no one else had, more than 500 petabytes across more than 2,000 healthcare institutions, where every new case made the AI better. Infinite is betting the same logic holds one layer deeper, on the epigenome, where each test feeds the model and the model sharpens the next test.

The catch is that pedigree is not a product and a term sheet is not a deal. This is non-binding, with a 30-day exclusivity window and no definitive agreement signed yet. The open question is whether methylation data proves as defensible and as monetizable as the multimodal oncology data $TEM Tempus assembled, and whether reverse-merging into a cash shell is as clean a path as $TEM 's own IPO was.

For existing $NNDM holders, the term sheet values their stock at a 20 percent premium to estimated net cash and leaves them a minority slice of a company expected to hold over $400 million in cash at closing, plus a contingent value right on the legacy assets. They are swapping a shrinking manufacturing business for a call option on the $TEM playbook run back in epigenetics.

Would you rather own the proven version in $TEM or the team trying to rebuild it?

It's not a sprint, it's a marathon.

Jun 9

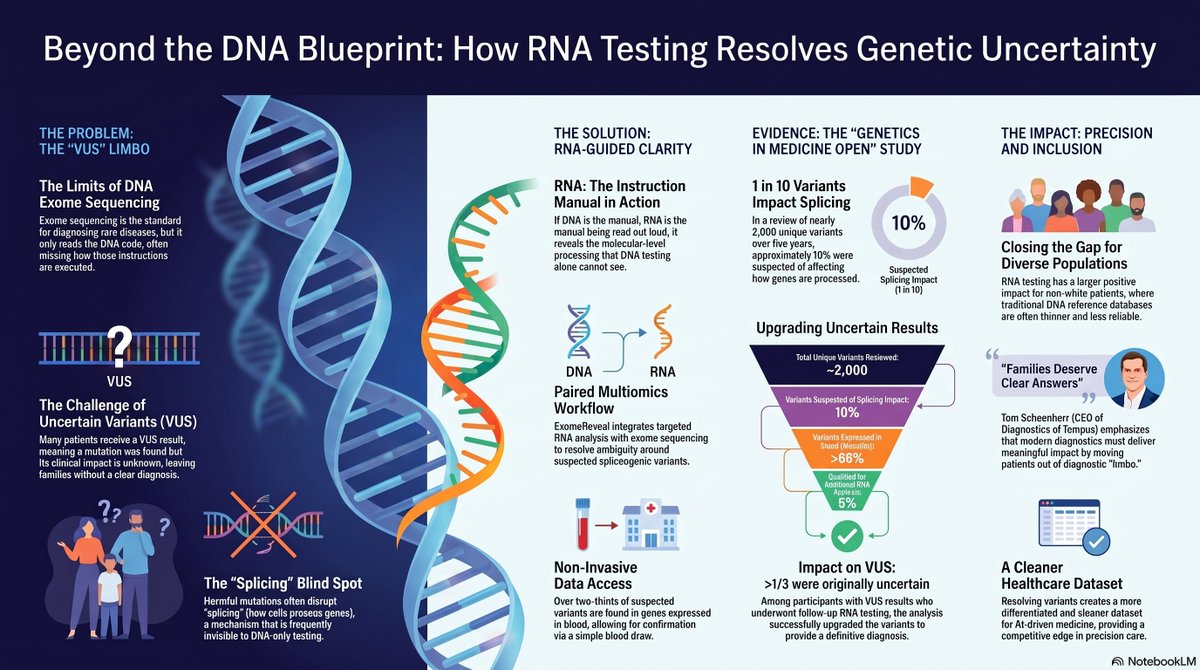

This $TEM study looks like a dry science paper, but it shows where the edge in AI medicine actually sits.

The tech in short. Exome testing reads the part of your DNA that codes for proteins, where most disease mutations hide. The problem is it often returns a variant of uncertain significance, a spelling change you cannot judge from DNA alone. RNA fixes that. If DNA is the instruction manual, RNA is it being read out loud, so it shows directly when a mutation breaks how a gene is spliced. Ambry, now owned by $TEM, runs RNA on top of the DNA exome to turn an uncertain result into a clear one.

The proof: nearly 2,000 variants over five years, about one in ten splicing related, and most in genes you can confirm from a simple blood draw. RNA also helped non white patients more, where the databases are thinner.

My take. This is not a revenue event, it is a data event. $TEM is a data company first, and almost no one else runs paired DNA and RNA at this scale. That is the quiet edge. The catch is it still has to turn that lead into profit, and diagnostics lives on reimbursement.

Validation, not a catalyst.

Do you value $TEM more for the AI or the data underneath it?

It's not a sprint, it's a marathon.

1

2

9

1,205

Jun 15

Nano Dimension signs non-binding term sheet to merge with Infinite Epigenetics, valuing Infinite at $890M. The combined company would trade as IEAI on Nasdaq, with over $400M cash at closing. Infinite owns TruDiagnostic and Tally Health, 120K samples, AI-powered diagnostics fo…

1

56

Jun 15

Nano Dimension $NNDM signed a non-binding term sheet to merge with Infinite Epigenetics in a deal valuing Infinite at $890M.

The combined company would operate as Infinite Epigenetics and trade on Nasdaq under $IEAI, with over $400M in expected cash at closing.

Infinite owns TruDiagnostic and Tally Health, has collected 120K epigenetic samples since 2020, and focuses on AI-powered diagnostics for chronic diseases including cardiovascular disease, Type 2 diabetes, COPD, and MASLD.

5

2

31

11,113

Jun 15

$NNDM Nano Dimension merging with Infinite Epigenetics — pivoting its Nasdaq listing and cash into AI-powered epigenetics diagnostics.

Infinite owns TruDiagnostic (120K samples, CLIA lab) and Tally Health. $890M transaction value. Combined company keeps $400M cash, no dilution needed.

Ticker becomes $IEAI. Term sheet only — 30-day exclusivity running now.

Not financial advice.

1

473

Following its premiere during @TRAIF2026 @amerikahaus, the #MoralPLaixDocumentary is released online1 Watch it reflect on its themes and join the ongoing conversation! #LLMs #Chatbots #AI #AIEthics #MoralPLai #IEAI

ieai.sot.tum.de/moralplai-re…

53

Last week, guest lecturer, Prof. Thomas Maak held a talk entitled: 𝘙𝘦𝘴𝘱𝘰𝘯𝘴𝘪𝘣𝘭𝘦 𝘓𝘦𝘢𝘥𝘦𝘳𝘴𝘩𝘪𝘱 𝘰𝘧 #𝘈𝘳𝘵𝘪𝘧𝘪𝘤𝘪𝘢𝘭𝘐𝘯𝘵𝘦𝘭𝘭𝘪𝘨𝘦𝘯𝘤𝘦 at the course #EthicsofAI held by Prof. Christoph Lütge. We thank Thomas for his insightful talk!

#TRAIF2026 #IEAI

1

2

48

It's time for good gestures in this invasion. The US blockade has hurt us immensely, plus the world. Let's kill two birds with one stone. Let's give the world an opened Strait in exchange for IEAI inspectors into Iran to see what the poop is on their nuke ambitions. Gestures.

2

3

35

It's time for good gestures in this invasion. The US blockade has hurt us immensely, plus the world. Let's kill two birds with one stone. Let's give the world an opened Strait in exchange for IEAI inspectors into Iran to see what the poop is on their nuke ambitions. Gestures.

1

1

1

24

#TRAIF2026 𝗣𝗮𝗻𝗲𝗹 𝗢𝗻 𝗔𝗜 𝗔𝗻𝗱 𝗘𝗱𝘂𝗰𝗮𝘁𝗶𝗼𝗻

Moderated by Prof. Nicole Lønfeldt, panelists: Prof. Christiane Lütge, Prof. Anna Keune & Prof. Sneha Das.

📺&📰: bit.ly/4uBC2ww

@amerikahaus @TU_Muenchen

#IEAI #TUM #MSCA #DoctoralNetworks #HorizonEurope

2

4

323

📣 #IEAI #SpeakerSeries with Christopher Cowton

“#𝘈𝘐𝘌𝘵𝘩𝘪𝘤𝘴 𝘢𝘵 𝘞𝘰𝘳𝘬: 𝘙𝘦𝘧𝘭𝘦𝘤𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 𝘋𝘦𝘴𝘪𝘨𝘯𝘪𝘯𝘨 𝘛𝘳𝘢𝘪𝘯𝘪𝘯𝘨 𝘧𝘰𝘳 𝘈𝘤𝘤𝘰𝘶𝘯𝘵𝘢𝘯𝘵𝘴”

📅 June 24

🕔 12:00–1:00PM

📍 TUMThinkTank

🔗 bit.ly/4fsYuUB

We look forward to welcoming you!

2

4

370

How about a end to the blockade, relief the Strait. In Exchange, Iran will gladly allow IEAI inspectors in to quantify the Uranium they have. This would be a positive implantation, too bad our idiot is stuck not knowing what to do, surrounding by Dumbfucks. #VoteBlue2026

1

4

46

"Tentative Deal" with Iran if Trump goes for it. It's about as real as my third eye. I bet he'll rely on the old "Iran will have no nuclear weapons". This is the main sticking point when we don't even know for sure how much enriched Uranium unless IEAI inspectors get in.

3

4

52

I awaken to the news that the US and Iran exchanged strikes, more craziness on top of craziness. I don't want the invasion to continue, I want an exchange of a different sort. It's all about gestures at this time, instead of bombing, undo the blockade, add IEAI inspectors.

2

3

86

TYVM for your answer. Recall when we Bombed Iran's nuke facilities back in June, then we bomb nuke sites on Feb 28? Seems they probably have some, but how much? I don't trust the Mossad, nor Netanyahu. Maybe if we bug the Hell out of them to put IEAI in there, all bets are off.❤️

1

4

44