Qlder 🇦🇺🚜 🇬🇧 #NoDigitalID retweeted

Its also near impossible to get it down to 30% because indexation is on your initial investment cost.

2

10

498

Yes, it's 30% rate after indexation minimum, which doesn't affect someone earning over $45K.

1

9

Heidi retweeted

Australians trying to calculate their capital gains with indexation

4

3

39

957

Finn Z retweeted

Did you know that the “inflation indexation” under Labor’s new ambition tax doesn’t actually protect you from inflation?

In fact it does the complete opposite: the higher inflation is the higher your CGT rate goes!

This is because Treasury’s modeling assumes you only hold one asset. If you hold more than one you get punished because you are not allowed to offset real gains with real losses.

The chart below is from my modelling of tens of thousands of tax outcomes on randomly created 20-share portfolios in the U.S. share market.

Higher inflation = higher tax rate.

12

16

83

4,173

That depends on inflation. After indexation you won't be paying tax on $1,000 but something less and then only if you bought the watch to be a collectable.

179

If you invest in assets as your business then CGT isn't applicable.

You pay normal income taxes (usually as a corporate entity @ 25%) and claim normal expenses.

You also don't get to claim indexation on the profits but you can carry forward losses like any other business.

1

8

What? A capital loss is a deduction against a capital gain.

Buy 2 houses 10 years ago for $100K each (ignore indexation).

Sell a house for $90K. Capital loss $10K. Carry it forward.

Sell the second house for $110K, capital gain of $10K, offset by capital loss, net CGT 0.

1

9

I think that's it, the legislation requires the "oldest" gains to be offset first, currently you can choose which investment gain the loss offsets.

Will affect someone with recent large gain than older ones, even after indexation, especially because losses are not indexed.

1

9

The whole thing needs to be scrapped.

30% minimum tax is completely unfair for low income earners and will not affect the 'wealthy' at all.

Not applying indexation to losses is going to kill direct share ownership and will still affect businesses regardless of carve-outs.

1

26

Why did the Government choose to introduce the indexation method from 1 July 2027 instead of simply reducing the existing 50% CGT Discount to one third (33%) or one quarter (25%)? Wouldn't lowering the discount percentage from that date have been simpler to administer?

207

The government has announced a partial backdown on their tax agenda. They have taken on one of the @AusTaxpayers suggestions by expanding eligibility for the small business CGT discount, but the changes don't go far enough.

As outlined by the ATA last week, if the government wants to go ahead with CGT reform, they need to make serious changes:

(1) scrap the 30% minimum

(2) cost-base indexation must be higher than just CPI

(3) apply indexation to all long-term investments (e.g. savings accounts)

(4) allow investors to reset their cost-base each year

(5) reduce the top marginal tax rate

(6) expand eligibility for small business & tech CGT discounts

So far they have only moved on one of those issues, which is not good enough. If they can't bring themselves to fix their CGT policy, then they should scrap it entirely and stick with the current approach.

austaxpayers.substack.com/p/…

3

2

15

473

I've just read the proposed startup carve outs here (consult.treasury.gov.au/c202…) and it raises more questions than it answers.

If the Government's own solution to the damage caused by these tax changes is to exempt certain companies, that's already a sign the policy has serious problems.

Putting aside the enormous damage that will still be caused by the 30% minimum tax and indexation changes for every other investor, this carve out consultation is full of unanswered questions:

- What happens if a startup is acquired after four years rather than five? It seems the Government only wants to support success if it happens after an arbitrary holding period which is now longer than the current 3 year employee share scheme concession.

- What happens to employee shares issued while a company was under 10 years old, but the company is over 10 years old on 30 June 2027? The consultation paper suggests they wont be eligible. Why not?

- Why should a software company receive relief from a near 47% tax because it qualifies for the R&D Tax Incentive, while a healthcare, agricultural or professional services business doesn't? Apparently some entrepreneurs are more equal than others.

- Once a shareholding exceeds $10 million, the concession disappears and they're back to facing tax rates approaching 47%. That's effectively telling entrepreneurs: build a successful business, but just not too successful. It's a strange message for a country that says it wants more innovation, investment and ambition. The consultation paper points to international precedents, yet the proposal falls well short of global benchmarks. In the U.S. the QSBS regime can reduce the effective tax rate on qualifying startup gains to around half of what an Australian founder could face under these rules!

If you're an ambitious founder trying to build the next Canva, Atlassian or a business worth $100 million or $1 billion, the message remains that Australia doesn't want to back you all the way through the journey. These carve outs tell Australians to dream small...

During the Senate inquiry we heard several non-founders claim that founders don't think about tax settings.

Of course they do!

Founders have to leave stable jobs, often invest their own savings, sell or mortgage their homes, take enormous risks and spend years with no guarantee of success. Tax settings are part of that opportunity cost calculation.

The most ambitious founders create most of the jobs, build globally competitive businesses and ultimately generate substantial tax revenue for Australia. If the incentives aren't right, many simply won't build those businesses here.

The more carve outs, exemptions and special rules that get added, the clearer it becomes that this policy is being designed on the run.

10

26

112

2,877

Jim, this is pathetic damage control from a lying failure.

Your “BREAKING” announcement is a humiliating backflip after weeks of backlash to the May 2026 Budget’s CGT reforms: replacing the 50% discount with inflation indexation a 30% minimum tax floor on gains from 1 July 2027.

Facts you can’t spin:

• There are ~2.7 million active small businesses.

• You just raised the turnover threshold for existing small business CGT concessions (the 15-year exemption, 50% active asset reduction, etc.) from $2M to $10M so 98% now qualify and dodge your new harsher rules.

• This isn’t “generous new concessions” or “support for innovation”—it’s you desperately carving out the mess you created because small business owners and startups told you your tax grab would kill exits and punish ambition.

• The core rip-off remains for everyone else: shares, crypto, non-qualifying assets, and higher earners still get the 30% floor even on low real gains.

Your “clarity and confidence” line is pure gaslighting. You rushed an ideologically driven Budget, got torched, and now pretend this U-turn is leadership.

**Resign. Australia can’t afford another flip-flop from this incompetent Treasurer.**

16

48

We keep debating whether the capital gains tax rate should be 10%, 12.5%, or 20%.

But we are arguing about the wrong number.

The moment the indexation benefit was removed, the tax rate written in the law stopped being the real rate. The real rate now goes up quietly every year with inflation. Let us look at the math:

You invest: ₹10 lakh.

The timeline: You hold it for 20 years while inflation runs at 6%.

The reality: To buy the exact same things today, your ₹10 lakh needs to become ₹32 lakh.

Your real profit is negligible. Your money buys exactly what it did two decades ago.

But on paper, the system sees a ₹22 lakh gain. And you will pay a 12.5% tax on it. That is a tax on a profit that does not exist. You are literally paying a tax on inflation.

The biggest problem? The longer you stay invested, the more you get taxed on the passage of time rather than actual growth. The intent is to reward long-term investors. But without indexation, the effect is opposite - the longer you hold, the more you are taxed on money you never actually made.

We see this every ITR season with property and gold held for decades. People face massive tax bills that have nothing to do with their actual returns.

We aren't overtaxing real wealth. We are taxing money that lost its value while the investor waited.

2

182

So happy for the @continuedev team that they finally get the recognition they deserve. Quite funny though that cursor finally acquires them after having built their own product based on the continue codebase. I remember the first months of cursor when they didn’t even have a UI difference with the continue vscode extension. Cursor had a wonderful engineering idea of using same continue indexation logic but run it on cloud for better performances and speed.

Well played @NateSesti

@cursor_ai

12

No, mate. We just have different views.

The indexation is a discount on taxes owed. There's no moral reason why I should *also* have my losses indexed.

Self-interest, sure. But no first principles justification.

5

20

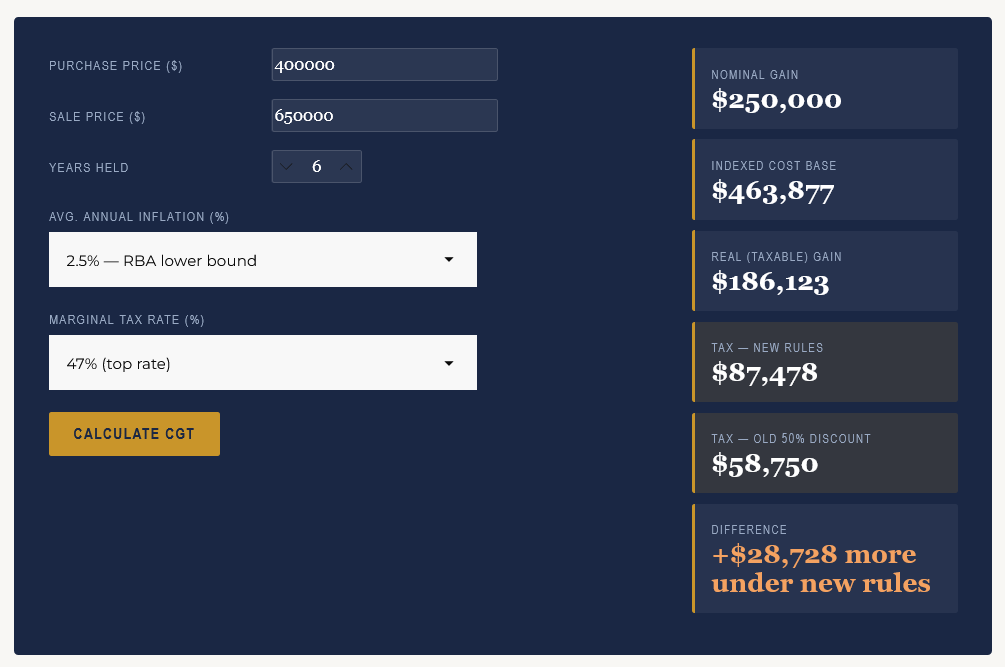

Australia's CGT rules are changing from 1 July 2027 - most property investors will pay MORE tax, not less.

Under low inflation, the new indexation system is worse than the old 50% discount.

Try - Free calculator 👇

australianreal-estate.com/Re…

#CGT #PropertyInvestment #TaxReform

8