We enjoyed connecting with #retail leaders at #NRFPROTECT this week and sharing how #InfinityAI is helping modernize security operations.

Thank you to everyone who stopped by to learn more!

Book a meeting: hubs.li/Q04lbCl00

#RetailSecurity #SituationAwareness

7

Andre OrphEe retweeted

29 Sep 2024

🔥 InfinityAI vs Midjourney 🔥

🚀 While Midjourney excels in the general AI-generated art field, InfinityAI is more focused on Web3 and the Bitcoin ecosystem.

🏂 InfinityAI is dedicated to empowering creators in decentralized spaces, offering seamless integration with Fractal and bringing true ownership of digital assets.

🧡 Our platform is built for the future of AI-generated content, involving NFTs, DeFi, and the world of creator economies.

🌍 Are you ready to explore the next evolution of AI in Web3?

#InfinityAI #Fractal #Bitcoin #AIGC

25,368

775

1,474

129,738

Visit Booth #7055 at #ITSAmerica today and see how #InfinityAI helps identify congestion anomalies, infrastructure disruptions, and emerging incidents in real time while enabling coordinated response workflows across transportation environments.

#AI #SituationAwareness

18

May 28

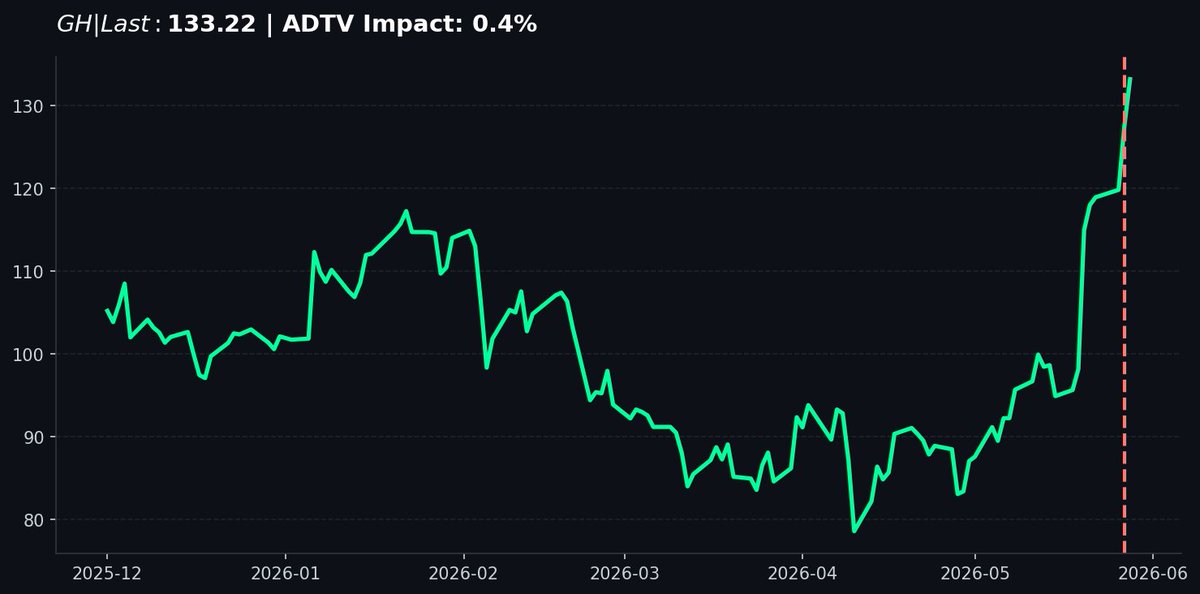

🚨 $GH INSIDER SELL: CLO LIQUIDATES POSITION INTO MOMENTUM RALLY

The Chief Legal Officer at Guardant Health has offloaded equity following the recent parabolic move driven by the American Cancer Society’s endorsement of the Shield blood test and FDA approval of the Liquid CDx panel.

TRANSACTION DATA:

- Actor: Saia John G. (Chief Legal Officer)

- Volume: 9,994 shares

- Average Price: $125.08

- Total Capital Deployed: $1,250,079.50

- Liquidity Impact: 0.45% of 30-day ADTV

CONVICTION SCORE: 4/10

MARKET THESIS:

This sale is a tactical profit-taking event rather than a signal of structural failure. With the stock up significantly on the back of the Shield test inclusion in colorectal screening guidelines and the integration of InfinityAI at the 2026 ASCO meeting, the CLO is capturing liquidity at a local resistance level near the $130.00 max call open interest strike. While the fundamental tailwinds from FDA clearances are robust, the current price action is extended. Expect consolidation as the market digests the recent 25% monthly surge; the insider is simply de-risking into the current retail and institutional FOMO cycle.

🤖 AI-Curated Data Pipeline | Not Financial Advice

157

May 28

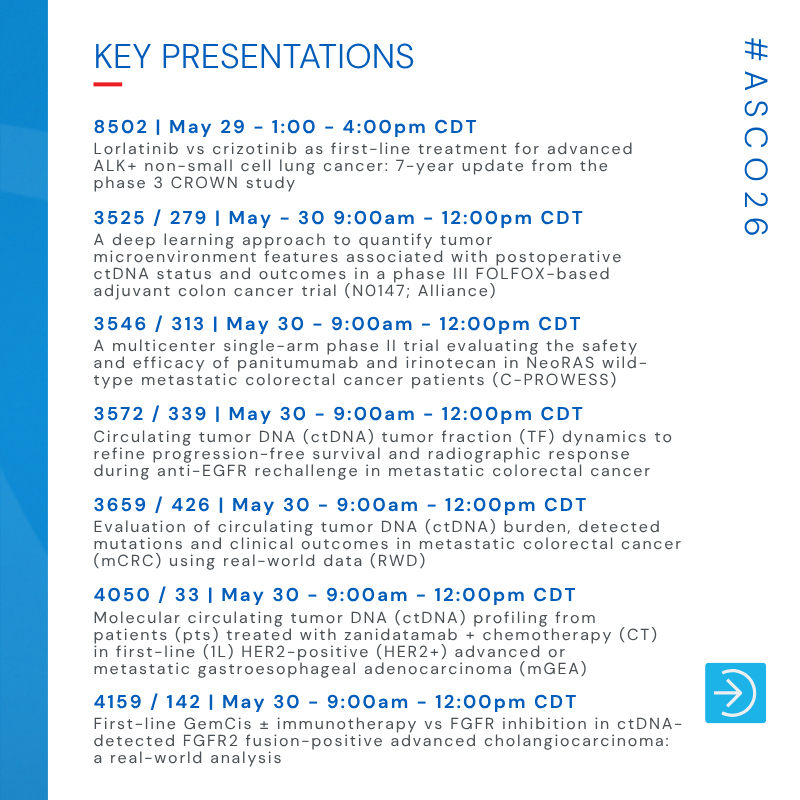

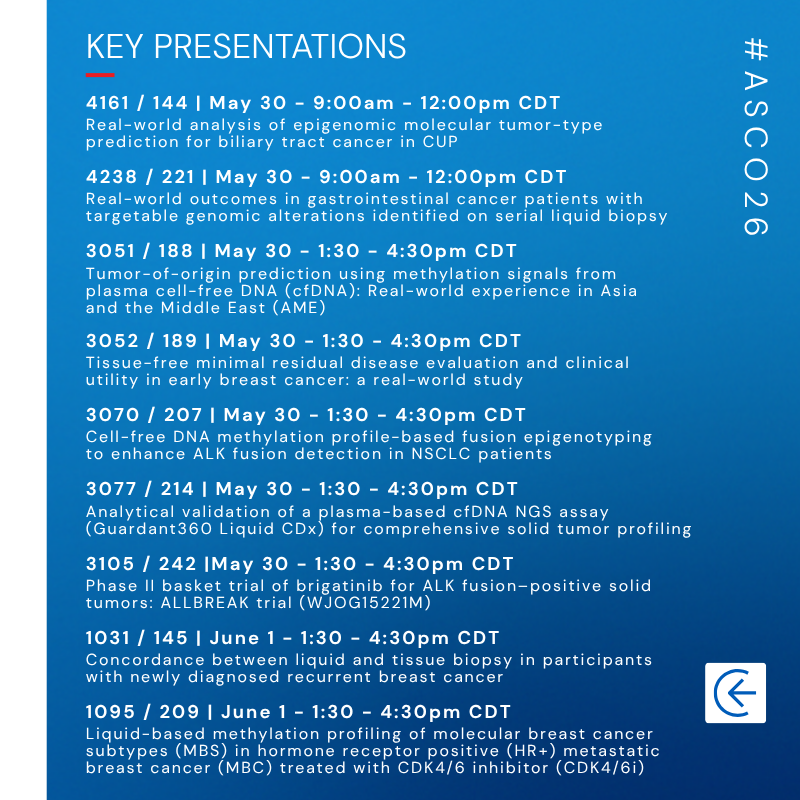

As #ASCO26 gets underway, we’re set to share 38 abstracts showcasing advances in methylation-based tumor classification, liquid biopsy technology, and the expanding clinical utility of our InfinityAI-powered portfolio as the #GlobalOncology community comes together in Chicago.

Details: bit.ly/4e9OkXH

1

4

391

May 26

AI ecosystems like InfinityAI are the real game-changers

the way they’re blending community and utility this early feels like the future.

1

10

May 26

AI is moving fast, but the real winners will be the platforms building ecosystems, not just tools.

InfinityAI is positioning itself at the intersection of AI, community, and Web3 and it’s interesting seeing how aggressively they’re growing their presence this early.

The AI narrative in crypto is only getting stronger. Projects that combine utility, accessibility, and strong community execution could dominate the next cycle.

Definitely one to keep an eye on. 👀

Join the movement.

t.me/infinitydaolab

25

73

76

571

May 25

@defiprince_ Welcome! First, head to kickoff.fun, connect your wallet, and link your X account. Then reply with: create InfinityAi INFINITY. Let's go!

72

Meet Userful at @InfoComm to experience #InfinityAI — unifying #cybersecurity, physical #security, #IoT, and enterprise systems for faster detection and response.

Book a meeting with the team on June 17-18: hubs.li/Q04hPHzX0

#AI #DigitalTransformation #SituationAwareness

1

1

76

Don’t miss the chance to see Userful #InfinityAI at Booth #110 during TechEx NA!

#InfinityAI unifies cybersecurity, IoT, physical security, and enterprise systems into one operational view.

Stop by to see it in action!

#EnterpriseAI #DigitalTransformation @TechEx_Event

1

14

May 17

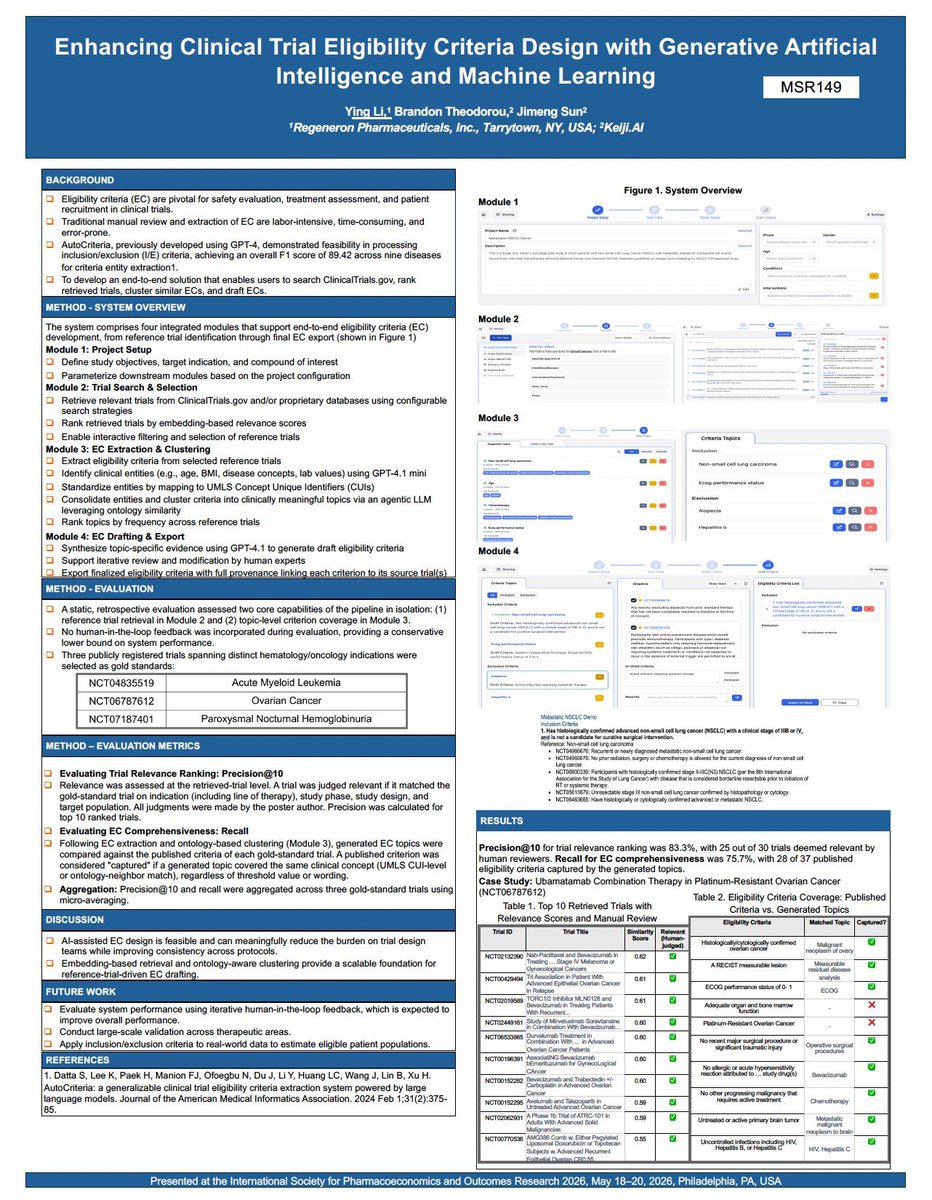

🚀 Heading to #ISPOR2026 in Philadelphia next week (May 18–20)?

Keiji AI is at booth #213 with two posters in collaboration with our customers:

1️⃣ With Regeneron (MSR149): end-to-end generative AI for clinical trial eligibility criteria — 83.3% precision on reference trial retrieval, 75.7% recall on EC coverage.

2️⃣ With Guardant Health: InfinityAI Studio, the agentic AI assistant for RWE feasibility analysis — 12/15 prior analyses replicated exactly, SUS score of 73.

Come find both posters, then come to booth #213 to meet the team and see TrialMind live.

Keiji AI's TrialMind is the AI-native platform for clinical trials. Backed by foundational research published in Nature, Nature Communications, Nature BME, Nature Machine Intelligence, Cell Patterns, NeurIPS, ICLR, AAAI, and ICML, and trusted by leading pharma companies and real-world data vendors, Keiji AI's TrialMind platform turns months of trial work into days — securely, traceably, and at scale.

#ISPOR2026 #ClinicalAI #GenerativeAI #AgenticAI #RealWorldEvidence #KeijiAI #TrialMind

1

119

May 17

Keiji AI <> Guardant Health Collaboration (Agentic AI for RWE)

🧪 Real-world evidence teams are drowning in dataset complexity. What if an agentic AI could turn a feasibility question into a defensible, code-backed answer — in minutes?

At #ISPOR2026, we are excited to present joint work with Guardant Health on InfinityAI Studio — an agentic AI assistant that automates cohort design, statistical computation, and analytic code generation for real-world feasibility analyses through a no-code, conversational interface.

📊 Results from the structured User Acceptance Testing (UAT):

• 8 of 8 non-technical users completed all core feasibility tasks

• 12 of 15 prior feasibility analyses replicated with exact results

• SUS score of 73 — acceptable usability

• Strongest user signal: "very strong desire to use"

Under the hood: adaptive schema discovery, preliminary analysis planning, iterative code generation in Python/R/SQL, and a self-correction loop — all orchestrated via Model Context Protocol (MCP), making Studio interoperable with the broader AI agent ecosystem (including Claude Code).

👉 Find our poster — "User Evaluation of an Agentic AI Assistant for Real-World Evidence Feasibility Analysis" — by Angela Watkins and Amar Das (Guardant Health), Jimeng Sun and Brandon Theodorou (Keiji AI).

📍 Then come to Keiji AI booth #213 for a live walkthrough and to talk to our team about how an AI-native platform fits into your RWE and clinical trial workflows.

Keiji AI's TrialMind is the AI-native platform for clinical trials. Backed by foundational research published in Nature, Nature Communications, Nature BME, Nature Machine Intelligence, Cell Patterns, NeurIPS, ICLR, AAAI, and ICML, and trusted by leading pharma companies and real-world data vendors, Keiji AI's TrialMind platform turns months of trial work into days — securely, traceably, and at scale.

#ISPOR2026 #RealWorldEvidence #AgenticAI #RWE #ClinicalAI #GuardantHealth #KeijiAI #TrialMind #MCP

1

202

Let’s meet at Booth #7055 at @ITS_America and see how #InfinityAI can act as your virtual #AI operator—continuously monitoring operational data so your team can focus on response.

📅 Book a meeting: hubs.li/Q04gDy690

#ITSACE2026 #SmartTransportation @ITSAEvents

1

7

Stop by Booth #322 at #NRFPROTECT to see how #InfinityAI unifies retail security!

We eliminate silos by centralizing video, POS, and fraud data into one live operational view for real-time insights.

📅 Book a meeting: hubs.li/Q04gpqkn0

#RetailSecurity #SituationAwareness

6

May 7

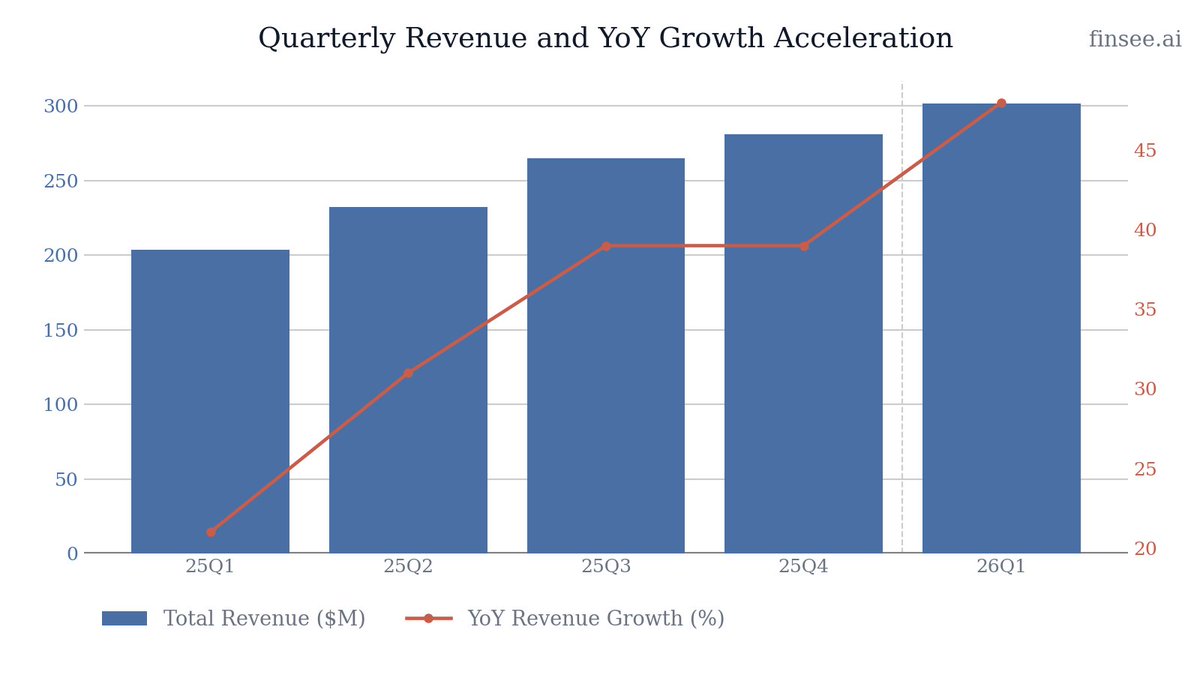

$GH Q1 2026 earnings: Hypergrowth Continues, Shield Screening Leads the Charge

Guardant Health delivered its fifth consecutive quarter of accelerating revenue growth, posting a massive 48% YoY top-line increase to $301.7 million in Q1 2026. The story is dominated by explosive volume gains: Shield screening tests surged nearly 400% YoY to 44,000, while the core Oncology testing business saw volumes jump 47%. Management raised full-year guidance across all major metrics, confidently projecting 32-34% annual revenue growth. However, capturing this market share requires immense capital. Non-GAAP operating expenses increased 34% YoY to $268.1 million as the company builds out its commercial infrastructure. Despite the higher top line, GAAP net loss widened to $112.1 million. The fundamental investment debate remains unchanged: Guardant is successfully executing a massive land-grab in oncology and screening, but company-wide profitability remains a longer-term milestone.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐅𝐥𝐚𝐰𝐥𝐞𝐬𝐬 𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐢𝐚𝐥 𝐄𝐱𝐞𝐜𝐮𝐭𝐢𝐨𝐧 — Guardant is proving its ability to scale. Screening revenue jumped over 600% YoY, and core Oncology volumes accelerated to 47% growth, indicating significant market share gains and excellent product-market fit.

• 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐑𝐚𝐢𝐬𝐞𝐬 𝐒𝐢𝐠𝐧𝐚𝐥 𝐂𝐨𝐧𝐟𝐢𝐝𝐞𝐧𝐜𝐞 — Management significantly raised FY26 revenue guidance to $1.30-$1.32 billion and boosted Shield volume expectations to up to 245,000 tests, signaling strong visibility into near-term demand.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐓𝐡𝐞 𝐂𝐨𝐬𝐭 𝐨𝐟 𝐒𝐜𝐚𝐥𝐢𝐧𝐠 — Growth is expensive. Non-GAAP operating expenses jumped by $68.5 million YoY, driving the GAAP net loss deeper to $112.1 million. The company is trading near-term profitability for long-term market dominance.

• 𝐒𝐡𝐢𝐞𝐥𝐝 𝐀𝐒𝐏 𝐃𝐢𝐥𝐮𝐭𝐢𝐨𝐧 𝐑𝐢𝐬𝐤𝐬 — As Shield volumes scale beyond the initial Medicare ADLT population and penetrate younger, commercially insured demographics, average selling prices (ASPs) may face downward pressure until broad commercial coverage is established.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. The fundamental execution is pristine. A 48% revenue growth rate at a $1.2B annualized run rate is rare. While the cash burn is substantial, the $1.2 billion cash position provides ample runway to fund this land-grab.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐒𝐡𝐢𝐞𝐥𝐝 𝐒𝐜𝐫𝐞𝐞𝐧𝐢𝐧𝐠 𝐕𝐨𝐥𝐮𝐦𝐞𝐬 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐑𝐚𝐝𝐢𝐜𝐚𝐥𝐥𝐲

The Shield commercial launch is exhibiting textbook hypergrowth. Test volumes jumped from 9,000 in 25Q1 to 44,000 in 26Q1. Strategic infrastructure moves, including a nationwide multi-year collaboration with Quest Diagnostics and activation of direct-to-consumer campaigns during Colorectal Cancer Awareness Month, are effectively driving awareness and translating directly into robust clinical ordering.

🟢🟢 𝐂𝐨𝐫𝐞 𝐎𝐧𝐜𝐨𝐥𝐨𝐠𝐲 𝐅𝐫𝐚𝐧𝐜𝐡𝐢𝐬𝐞 𝐒𝐡𝐨𝐰𝐬 𝐍𝐨 𝐒𝐢𝐠𝐧𝐬 𝐨𝐟 𝐒𝐥𝐨𝐰𝐢𝐧𝐠

Despite being a more mature segment, Oncology volumes are accelerating, growing 47% YoY (up from 38% growth in 25Q4 and 25% in 25Q1). Guardant360 Liquid and Guardant360 Tissue both demonstrated significant expansion. Growth is being further catalyzed by therapy response monitoring via Guardant Reveal and the addition of whole transcriptome profiling to the Guardant360 Tissue capabilities.

🔴 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬 𝐄𝐱𝐩𝐚𝐧𝐝𝐢𝐧𝐠 𝐭𝐨 𝐅𝐮𝐞𝐥 𝐭𝐡𝐞 𝐅𝐢𝐫𝐞

To support this massive growth, Guardant is spending heavily. Non-GAAP operating expenses surged 34% YoY to $268.1 million. Management explicitly raised full-year OpEx guidance to a midpoint of $1.06 billion, citing commercial infrastructure expansion and marketing activities for Shield and Oncology. While revenue is growing faster than OpEx (48% vs 34%), the absolute dollar gap remains a headwind to near-term profitability.

🟢 𝐁𝐢𝐨𝐩𝐡𝐚𝐫𝐦𝐚 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 𝐚𝐧𝐝 𝐂𝐨𝐦𝐩𝐚𝐧𝐢𝐨𝐧 𝐃𝐢𝐚𝐠𝐧𝐨𝐬𝐭𝐢𝐜𝐬 [NEW]

The company continues to deeply embed its technology within the pharmaceutical ecosystem. Guardant secured FDA approval for Guardant360 CDx as a companion diagnostic for Arvinas and Pfizer’s VEPPANU. Furthermore, the InfinityAI real-world evidence platform successfully supported the approval of Daiichi Sankyo’s ENHERTU. A newly announced collaboration with Nuvalent will focus on developing targeted cancer therapy companion diagnostics.

🔴 𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐒𝐮𝐛𝐬𝐭𝐚𝐧𝐭𝐢𝐚𝐥

Free cash flow for Q1 was $(71.2) million, a slight deterioration from $(67.1) million a year ago. While the company maintains a robust balance sheet with $1.2 billion in cash and marketable securities, the continued reliance on high cash burn to acquire market share limits financial flexibility in the event of unforeseen macroeconomic or regulatory shocks.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐍𝐨𝐧-𝐆𝐀𝐀𝐏 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧: 66%

Stable. Gross margins improved 100 basis points YoY from 65% in 25Q1, indicating that despite rapid volume scaling and the introduction of lower-ASP screening tests, the company is successfully driving down cost-of-goods-sold (COGS) through operational efficiencies and lab automation.

𝐁𝐢𝐨𝐩𝐡𝐚𝐫𝐦𝐚 & 𝐃𝐚𝐭𝐚 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $53.0 million

Stable growth. This segment grew 17% YoY. While it lags the hypergrowth seen in the clinical clinical testing divisions, it provides high-margin, relatively predictable revenue backed by major pharmaceutical partnerships and data licensing agreements.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐓𝐨𝐭𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $1.30 to $1.32 billion

Accelerating. The guidance was raised from a prior range of $1.25-$1.28 billion. The new midpoint ($1.31B) implies a 33% YoY growth rate over FY25's $982 million, showing phenomenal durability for a business operating at this scale.

𝐅𝐘𝟐𝟔 𝐒𝐜𝐫𝐞𝐞𝐧𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $186 to $198 million

Accelerating. Raised significantly from the previous $162-$174 million range. This is driven by an increased volume forecast of 230,000 to 245,000 tests, reflecting higher confidence in sales rep productivity and the early impact of the Quest Diagnostics partnership.

𝐅𝐘𝟐𝟔 𝐎𝐧𝐜𝐨𝐥𝐨𝐠𝐲 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐆𝐫𝐨𝐰𝐭𝐡: 28% to 29%

Accelerating. Raised from 25%-27% previously. Management now expects Oncology volume to grow greater than 35% (up from ~30%), underscoring intense demand for Guardant360 and Reveal.

𝐅𝐘𝟐𝟔 𝐍𝐨𝐧-𝐆𝐀𝐀𝐏 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬: $1.05 to $1.07 billion

Accelerating. Raised from the previous $1.03-$1.05 billion. The company is actively reinvesting top-line outperformance back into commercial infrastructure to maximize its first-mover advantage in the blood-based cancer screening market.

𝐅𝐘𝟐𝟔 𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐁𝐮𝐫𝐧: $185 to $195 million

Stable. Despite the increase in OpEx guidance, the FCF burn forecast remains unchanged and represents a solid improvement compared to the $233 million burned in FY25, highlighting that gross profit expansion is helping to absorb the higher commercial spend.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐒𝐡𝐢𝐞𝐥𝐝 𝐀𝐒𝐏 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲

With the expected massive scaling of Shield volumes, what is your assumed Average Selling Price (ASP) trajectory for the remainder of 2026, particularly as the mix shifts toward commercially insured populations?

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 𝐓𝐢𝐦𝐢𝐧𝐠

You've increased OpEx guidance to capitalize on the Shield launch momentum. At what specific revenue run-rate or volume threshold do you expect to see meaningful operating leverage where expense growth flattens out?

𝐐𝐮𝐞𝐬𝐭 𝐂𝐨𝐥𝐥𝐚𝐛𝐨𝐫𝐚𝐭𝐢𝐨𝐧 𝐈𝐦𝐩𝐚𝐜𝐭

Can you quantify the expected volume contribution from the new nationwide Quest Diagnostics collaboration in the second half of 2026 versus organic direct-sales efforts?

𝐍𝐞𝐱𝐭-𝐆𝐞𝐧 𝐒𝐡𝐢𝐞𝐥𝐝 𝐏𝐢𝐩𝐞𝐥𝐢𝐧𝐞

With the commercial success of the current Shield assay, what is the latest timeline and regulatory strategy regarding the readouts and potential launch of the Shield V2 product?

492

Come to Booth #110 at #TechEx North America and see how #InfinityAI helps teams triage, investigate, and respond to events instantly.

Book a meeting: hubs.li/Q04fbq2t0

#EnterpriseAI #DigitalTransformation #CyberSecurity @TechEx_Event

1

13

Meet us at #Intermodal2026 to see how #InfinityAI helps #logistics and #supplychain teams build real-time #controltowers with unified data and AI insights.

Book a meeting: hubs.li/Q04bRGMr0

#SituationalAwareness #DataVisualization

11

Really sharp launch Zoho Projects Infinityai, bringing this level of flexibility into project management like this is a big shift, especially when teams can shape workflows, dashboards, and automation around how they actually operate instead of forcing rigid structures. Layering AI on top for summaries, suggestions, and bottleneck detection is where this gets powerful. What’s crazy though is tools like this don’t realize how perfectly this fits into crypto builder workflows, that space is chaotic, fast-moving, and heavily automation-driven, with teams constantly coordinating launches, updates, and infra across multiple tools. Having adaptive, AI-assisted project tracking like this is serious leverage. I’ve got visibility options to get this trending in my space and across X timelines, DM me.

27

🚨 Latest #Oncology Update!

🔷 Real-world evidence generated using Guardant Health’s InfinityAI platform supported the approval of ENHERTU® (Trastuzumab deruxtecan) in Japan for previously treated HER2-positive advanced solid tumors, complementing data from DESTINY clinical trials.

🔷 This highlights the growing role of real-world evidence in precision oncology, enabling broader application of HER2-directed therapy across tumor types and informing regulatory decisions in biomarker-defined populations.

🔗 Read more: bit.ly/ONCOnews-31-Mar-01

#ONCOnews #OncoAlert #OncEd #Oncology #CancerResearch #PrecisionMedicine #TargetedTherapy #CancerCare #PersonalizedMedicine #Biomarkers #Genomics #CancerGenomics #RealWorldEvidence #RWE #ClinicalResearch #ClinicalTrials #TranslationalMedicine #MedicalInnovation #HealthcareInnovation #Pharma #Biotech #OncologyCommunity #CancerTreatment #HER2 #MetastaticCancer #SolidTumors #OncologyUpdates #EvidenceBasedMedicine #MedicalEducation #FutureOfMedicine #DigitalHealth #AIinHealthcare #AIinMedicine #CompanionDiagnostics #LiquidBiopsy #GlobalHealth #MedTech #ScienceCommunication

94

Mar 30

Real-world evidence is shaping what comes next in #PrecisionOncology.

Evidence generated from our InfinityAI platform contributed to the recent approval of ENHERTU® in Japan for previously treated patients with HER2-positive metastatic solid tumors—highlighting how real-world evidence is gaining traction with regulators and opening new pathways in rare, biomarker-defined populations.

Read more: bit.ly/4talsn0

2

229