12 Nov 2025

The Great Health Insurance Debate: Is your policy really protecting you or just ticking a box? Many don’t realize claims are rejected for reasons they never read about. DM for a real checkup.

#HealthInsurance #InsuranceDebate #ClaimReality #DMForHelp

2

2

144

22 Oct 2025

We are proud to celebrate the brilliant students of KNUST, winners of the Insurance Debate 2025, organized by the Insurance Awareness Coordinators Group (IACG) and National Insurance Debate!

#GLICOLife

#InsuranceDebate

#InsuranceAwareness

#IACG

1

2

63

21 Oct 2025

We are proud sponsors of the brilliant KNUST team representing the 2025 National Insurance Debate, and guess what?

They have made it to the FINALS!

#GLICOLife

#InsuranceDebate

#TeamKNUST

#IACG

#InsuranceAwareness

1

2

68

21 Jan 2025

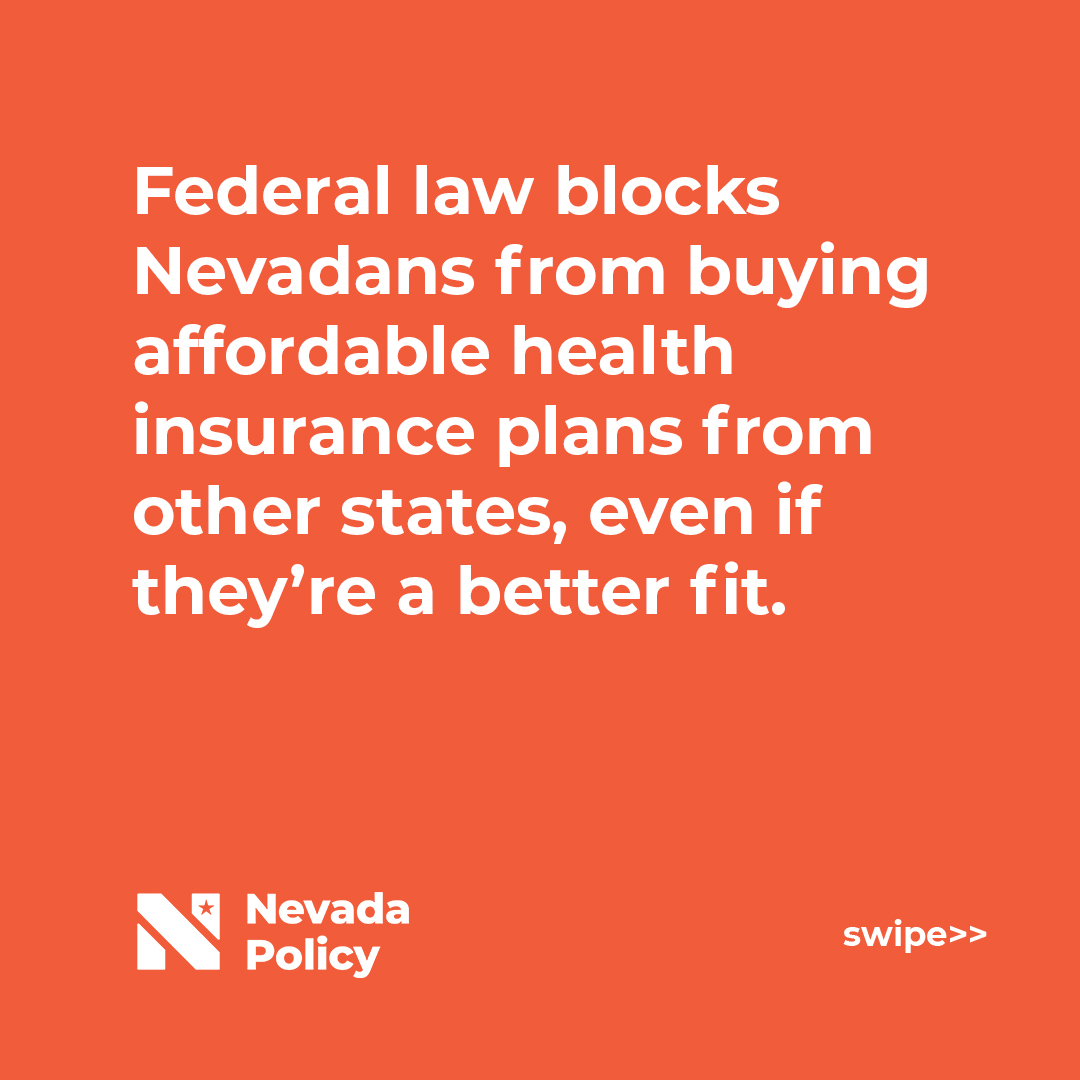

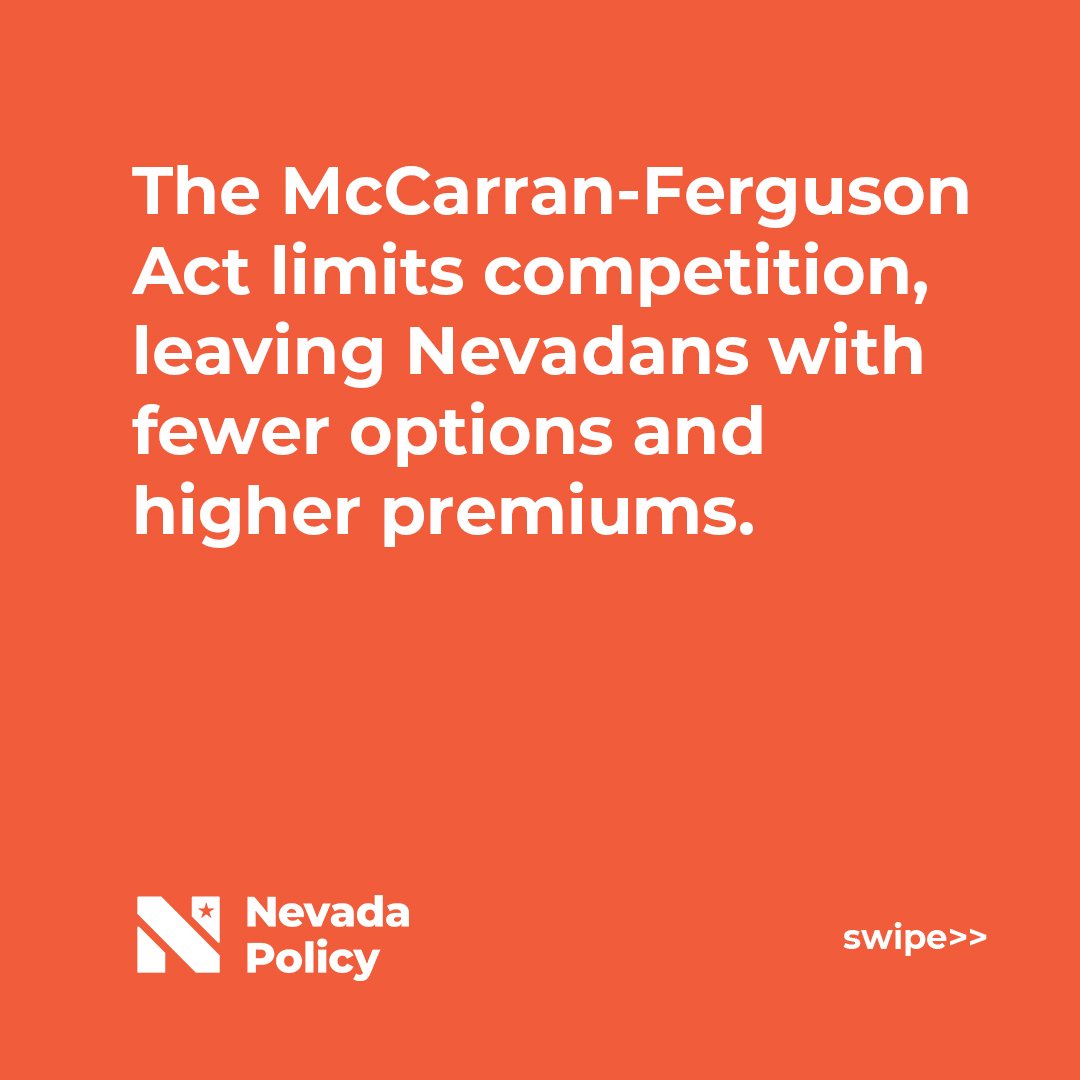

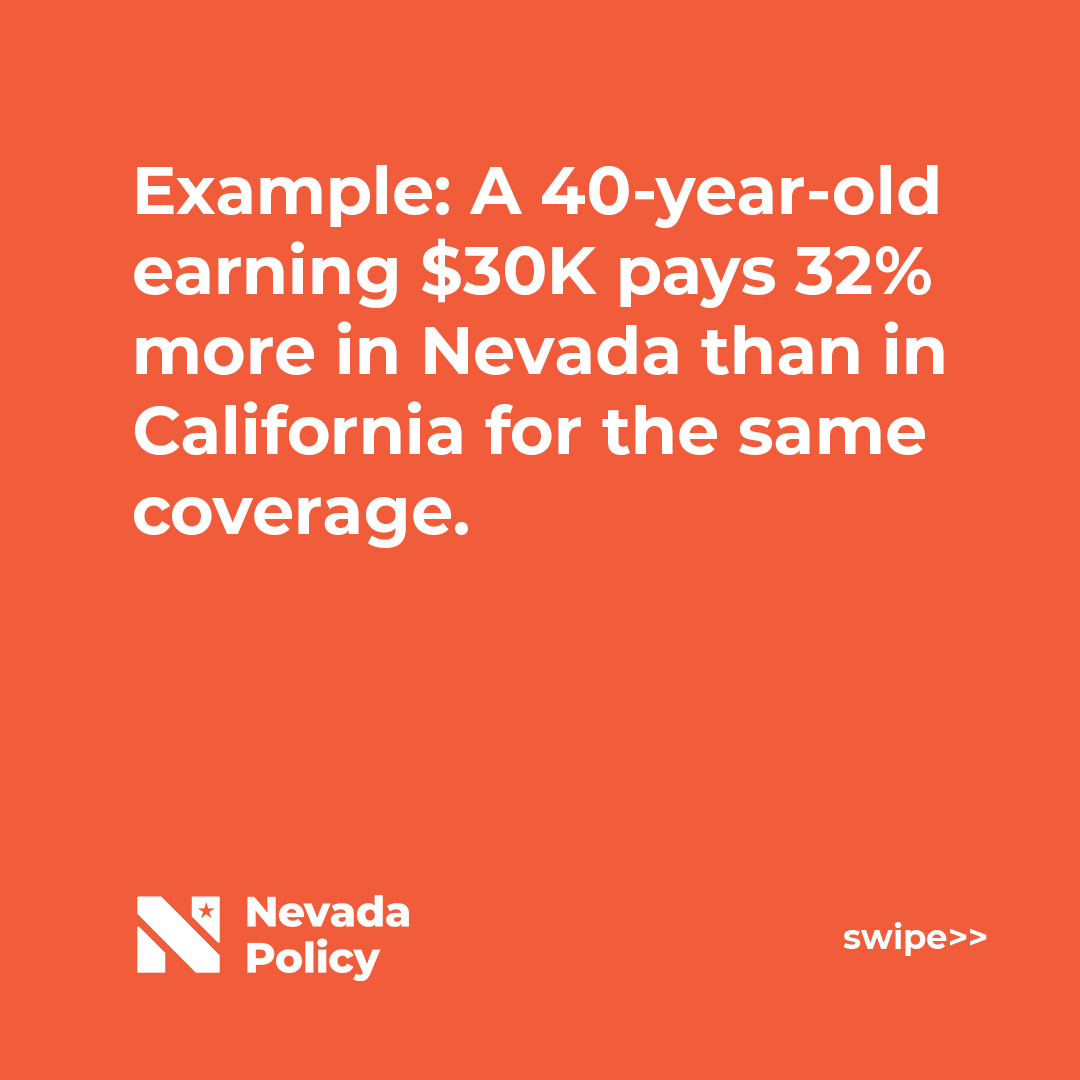

We pay more for health insurance than Californians... WHY?

Comment below what you think. #nevadapolicy #HealthInsurance #InsuranceDebate #NevadaPolitics #HealthcareCosts #PolicyDiscussion #NevadaLife #InsuranceRates #HealthCareAwareness #NevadaCommunity

2

2

181

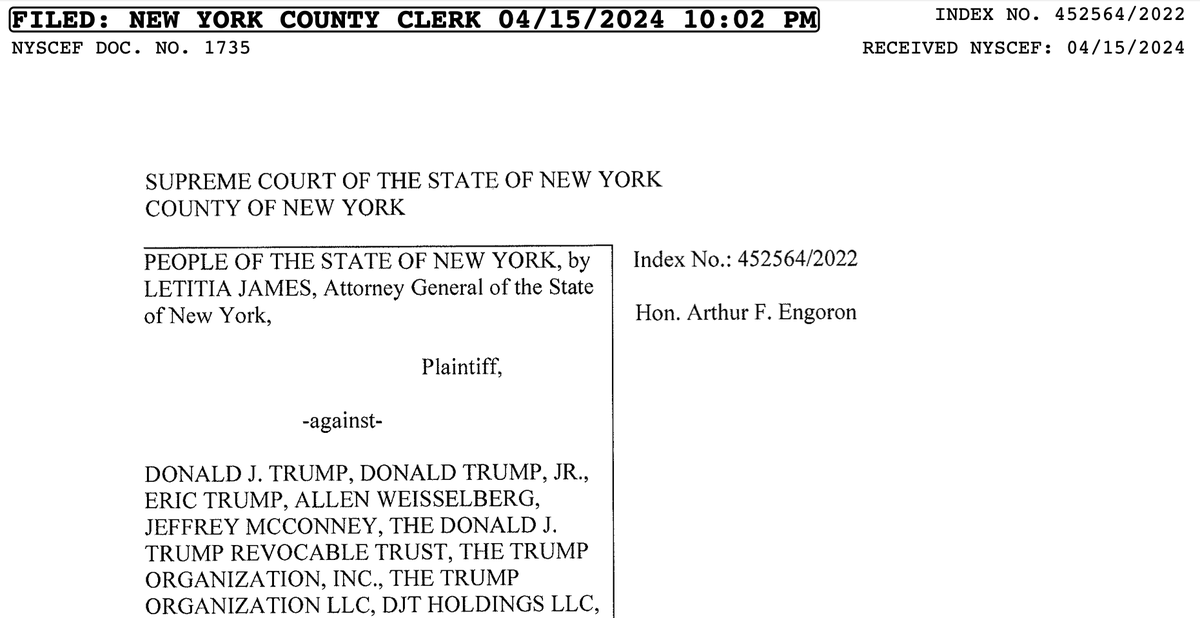

16 Apr 2024

🔍 Concerns loom as NY AG questions the adequacy of Knight Specialty Insurance as a surety. Will regulatory compliance, financial stability, and control over $175M in collateral meet strict standards? Stay tuned as the case unfolds.

#LegalNews #InsuranceDebate

16 Apr 2024

The Attorney General (AG) of New York may have several concerns regarding the legitimacy and sufficiency of Knight Specialty Insurance Company (KSIC) as a surety, despite the arguments presented in the memorandum. These concerns could include:

1. Regulatory Compliance and Licensing: One primary concern could be the status of KSIC as a non-admitted carrier in New York. Even though KSIC is licensed in Delaware and qualifies as an excess lines insurer in New York, the AG might question whether KSIC should be permitted to issue surety bonds without a certificate of qualification under New York insurance law. This certificate ensures that the insurer meets specific regulatory standards necessary to protect public interest.

2. Financial Stability and Independence: The AG might also scrutinize the financial arrangements described in the memorandum, such as the collateral and reinsurance agreements. While KSIC and its parent company, KIC, reportedly have significant assets and equity, the AG may seek further proof of their liquidity and ability to promptly fulfill financial obligations under the bond, especially in adverse scenarios.

3. Control over Collateral: Concerns may arise about the practical aspects of the control agreements over the collateral account. The AG might question the enforceability and reliability of these agreements, particularly how quickly and effectively KSIC can exercise control over the funds if required.

4. Risk of Conflict of Interest: The AG may also be wary of potential conflicts of interest, especially if KSIC's decisions or financial stability are too closely tied to the fortunes of its parent company or other involved entities. There might be doubts about KSIC's ability to act independently in the best interest of the bond's beneficiaries.

5. Precedent and Legal Interpretation: The AG might challenge the interpretation of legal statutes and precedents cited in the memorandum. This could include questioning the application of CPLR sections and New York Insurance Law as they pertain to the qualifications of KSIC as a surety.

6. General Concerns about Excess Lines Insurers: Finally, there might be broader concerns about the role of excess lines insurers in critical financial undertakings like large surety bonds. The AG may argue that excess lines insurers, generally used for risks not insurable in the standard market, should not be involved in fundamental judicial financial instruments without stricter oversight.

Each of these concerns reflects broader issues of public policy and legal interpretation that the AG might raise to ensure that financial and regulatory protections are adequately maintained.

7

9

1,102

2 Aug 2023

Thank you for bracing this networking opportunity @WaceraKieha, glad you grasped a thing!

Thanks to @PacisInsurance & @reinsurancesolutions for making it happen!

#insurancemeetngreet #insurancedebate

2

5

115

29 Jul 2023

Happening now, The insurance Meet n Greet at The Edge!

#insurancemeetngreet

#insurancedebate

1

4

58

15 Nov 2019

This is the motion for the 2nd Day,first round...all the best Teams. #InsuranceDebate

@USIUAfrica

@DebateKenya @Mmu_DebateClub

1

2

14 Nov 2019

This year's tournament has attracted 32 teams from 12 institutions of higher learning across the country, making it one of the most competitive tournaments in the debate calendar.

| #InsuranceDebate |

1

2

3

9 Nov 2019

I first interacted with @DebateKenya during 2018's Insurance debate that was held in cuea uni.It's yet another time to grace the event.

#InsuranceDebate

1

1

2

31 Oct 2019

Earlier today during the insurance Cafe we through General Insurance presented by Mary Wahome.

In this, one must have insurable interest I.e must stand to loose financially if risk happens.

General Insurance is short term. Usually annual. They are renewed.

#insurancedebate

1

1

2

26 Jan 2018

1

3

6

5 Dec 2017

“In #business: #startup #small-business #entrepreneur #tech #wob . Don’t be quick to #collect accountable #Service or #Products must accommodate the transaction or #deal , whichever the case maybe @Nationwide.”

#Jerusalem #InsuranceDebate #consumer-never-win #change-coming #2018

4 Sep 2017

6

6

16 Aug 2017

#insurancedebate first i will consider the premium to be paid

16 Aug 2017

What would you consider b4 taking an insurance cover? @amina_icram @GrayMarwa @fredodhiambo388 @mauricejuniorre

4

1

15 Jul 2016

We really need to start this discussion. Is the concept of #insurance helpful or hurtful to our country? #insurancedebate

1 Dec 2015

#Insurance as profession has optimistic future–close call but glad to see @brokingbod win excellent #InsuranceDebate bit.ly/1jt6NQ4

1

1

Will #insurance will ever match medicine, law or accountancy in the public’s eye? #Insurancedebate results are in

insuranceage.co.uk/insurance…

26 Nov 2015

Did @brokingbod sway u with his arguments? Voting suggests there might be some hope for the sector #insurancedebate

1

1