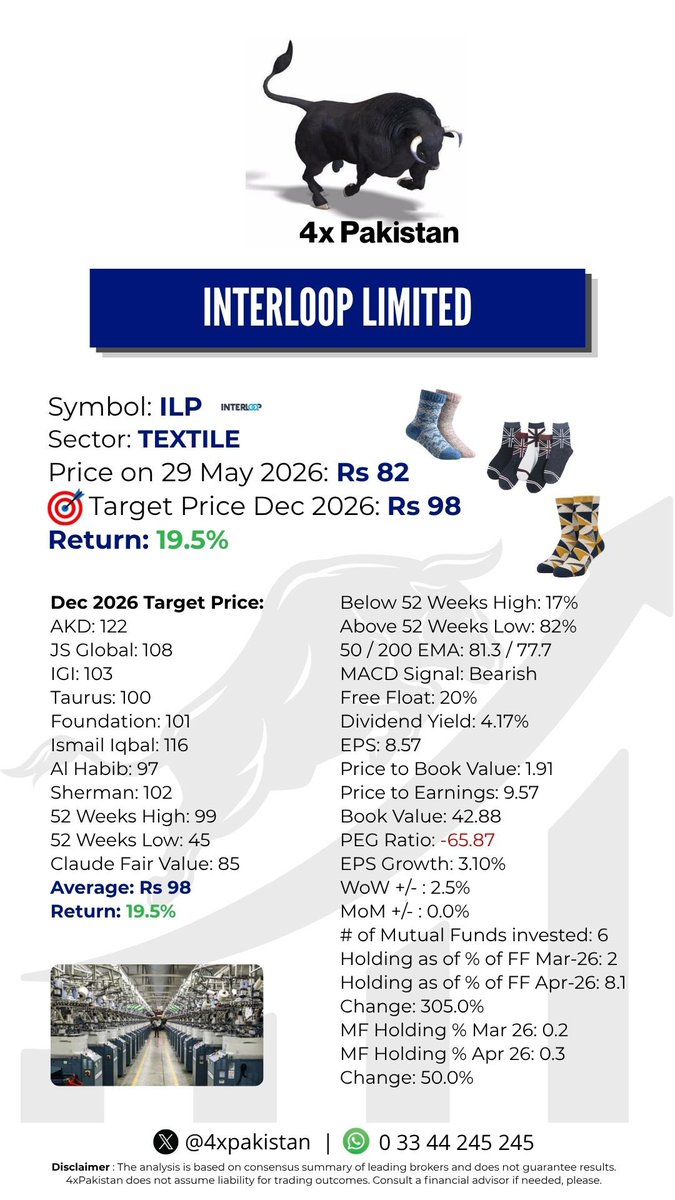

Weekly Top 10 Outperformers KSE-100 Index💸

Open Trading Account in PSX 🔰Click to WhatsApp:wa.me/923122070092?text=INVE…

#stockmarket #KSE100 #PSX #TPLRF1 #TPL #REITFund #JVDC #InternationalSteels #ISL #HGFA #HBLGrowth #ILP #Interloop #BNWM #PSEL #INIL #PKGS #DGKC #Pakistan

1

112

Jun 11

Watkins glen still has 11. The interloop used to count and they took that from us and I am still not used to calling it a 7 turn track.

133

Jun 9

RUPEE FIXATION

In Pakistan’s economic debate, few ideas return as predictably as the call for a weaker rupee. Whenever exports falter, the case is familiar: the currency is overvalued, competitors have gained an exchange-rate edge, and Pakistan has priced itself out of world markets. Exchange rates do affect margins and investment. But they do not, on their own, create competitiveness. Treating the rupee as the central explanation for weak exports obscures deeper failures.

Vietnam challenges the notion that currency depreciation alone can deliver export success. Its textile and garment exports are estimated at about US$46 billion in 2025, helped by policy continuity, investment, skills, compliance and integration into global supply chains. Competitiveness is built as much in factories, ports, training centres, power systems and boardrooms as in foreign exchange markets.

Bangladesh offers a different but equally relevant lesson. Its taka has weakened at times, but the country’s garment performance cannot be explained by exchange rates alone. Ready-made garment exports rose from about US$31.5 billion in FY2020-21 to US$39.3 billion in FY2024-25. Scale, compliance, reliability and established buyer relationships have mattered as much as price. Pakistan, by comparison, recorded textile exports of about US$17.9 billion in FY2024-25.

The comparison is uncomfortable because it points to the real problem. Too much of Pakistan’s export basket remains concentrated in price-sensitive products: yarn, grey cloth, basic fabrics, towels, bed linen and lower-end knitwear. These products matter and generate foreign exchange. But they compete in segments where buyers can switch quickly and price remains decisive.

By contrast, Vietnam and Bangladesh have moved more aggressively into value-added apparel tied to global brands and complex supply chains. In those segments, price still matters, but it is only one variable among many. Buyers care about quality, consistency, reliability, speed, compliance, traceability and scale. Once a supplier is trusted on those dimensions, exchange-rate movements become less decisive than they are in commodity-style trade.

Pakistan has its own examples. Interloop, which supplies major global brands including Nike, Adidas and Puma, has built its position through investment in technology, automation, sustainability, workforce capability, and long-term customer relationships. The company’s own public profile emphasises responsible manufacturing, traceability, and large-scale integrated production, rather than any special exchange-rate advantage.

The same logic applies to established exporters such as Gul Ahmed, whose scale and integrated operations have supported long-running relationships in home textiles, including with international buyers such as IKEA. What such firms demonstrate is simple: durable export success comes from capability, reliability and compliance. Currency may influence margins at the edge, but it does not substitute for those fundamentals.

This distinction matters because devaluation is often presented as a costless cure. It is not. Pakistan’s textile sector relies heavily on imported cotton, synthetic fibres, dyes, chemicals, machinery, spare parts and energy-related inputs. A weaker rupee raises the cost of all of them. Higher export receipts are therefore partly offset by higher production costs, especially in import-intensive sectors.

More importantly, devaluation does nothing to fix the bottlenecks that have held exports back for years. It does not improve logistics, reduce port delays, lower domestic transport costs, strengthen cotton yields, upgrade worker skills or deliver policy consistency. It cannot compensate for unreliable energy pricing, cumbersome taxation, or weak adoption of man-made fibres and product development.

Repeated reliance on exchange-rate adjustment is therefore a distraction. It offers a quick macroeconomic answer to what is, in reality, a microeconomic and institutional problem. Countries that succeed in exports do not merely become cheaper; they become more dependable, more productive and more valuable to buyers.

Vietnam’s experience underlines the point. Its rise has been built on policy continuity, supply-chain integration, technology, skills and a steady shift towards higher-value products. It increasingly competes on speed, compliance and quality rather than simply low cost. Pakistan has yet to pursue that path at scale.

None of this means exchange rates are irrelevant. An overvalued currency can damage exports, distort incentives and encourage imports over domestic production. The rupee should reflect economic fundamentals and remain market-based. But it is unrealistic to expect a one-off depreciation to compensate for years of underinvestment in competitiveness.

The policy agenda is clear. Pakistan must move up the value chain through better skills, improved cotton quality, wider use of man-made fibres, stronger design and product development, modern machinery, efficient logistics and predictable taxation. It must make formal investment easier, not harder. It must help exporters build capabilities that make buyers stay even when cheaper alternatives exist.

Pakistan’s best exporters have already shown what works. Sustainable export growth is built not on being cheaper for a season, but on being better for the long term. Until that lesson shapes policy as much as business strategy, the rupee will remain an alibi while competitors keep winning customers.

@mincompk @StateBank_Pak @Financegovpk

82

All lanes are now open on LA 3132 West at the Interloop Expressway (I-220 East/I-20). Congestion remains minimal.

82

The left lane is blocked on LA 3132 West at the Interloop Expressway (I-220 East/I-20) due to a stalled vehicle. Congestion is minimal at this time.

92

Imran Choudhry retweeted

Jun 6

10 PSX Mid-Caps investors are watching for long-term SIP 👇

Systems Ltd (SYS) – IT exports, digitalisation

Interloop (ILP) – Textile, global brands, ESG

Air Link (AIRLINK) – Mobile assembly, electronics

Lucky Core (LCI) – Chemicals, pharma, premium play

Thal Ltd (THALL) – Auto parts, engineering

Millat Tractors (MTL) – Agri, rural economy

National Foods (NATF) – FMCG, exports, brand power

Avanceon (AVN) – Automation, industrial tech

Octopus Digital (OCTOPUS) – Cloud, SaaS, digital infra

TPL Trakker (TPLT) – Tech, logistics, mapping

Themes: IT exports, manufacturing, agri, FMCG, digitalisation, CPEC infra.

Many are sector leaders with ROE >20% & low debt.

Mid-cap = High risk, high reward. SIP karo, bhool jao.

#PSX #KSE100 #MidCap #SIP #Pakistan #Investing

5

42

2,612

Jun 6

💥 5X Revenue 5X Profit in 5 Years 🚀

PSX ke silent compounders.

Na shor, na hype… sirf wealth 👑

Systems Ltd (SYS) – IT exports 6x

Interloop (ILP) – Textile 5.5x

Avanceon (AVN) – Automation 7x

Meezan Bank (MEBL) – Deposits 5x, Profit 6x

Air Link (AIRLINK) – Mobile assembly 10x

TPL Trakker (TPLT) – Turnaround 5x

Octopus Digital – Cloud/SaaS 8x

Service Global (SGF) – Shoe exports 5x

Feroze1888 (FML) – Home textile 5x

Highnoon Labs (HINOON) – Pharma 6x

Theme: Exports, IT, manufacturing, digitalisation

PSX mein bhi 5x baggers hain. Bas nazar chahiye. 👀

#PSX #KSE100 #Multibagger #Pakistan #Compounding #SYS #MEBL

2

6

53

3,670

Jun 3

Pakistani Companies Making Their Mark Globally🌍

Several Pakistani companies are punching above their weight in key industries by market cap / global relevance:

Engro Corp – Rank #8 in Fertilizer & Agri Solutions, Asia

MCB Bank – Rank #14 in Islamic Banking globally

Systems Ltd – Rank #1 IT exporter from Pakistan, Top 3 in MEA

HBL – Rank #27 in Banking, South Asia | 1700 branches

OGDC – Rank #1 in Oil & Gas E&P, Pakistan | Top 100 Asia

UBL – Rank #2 in Digital Banking adoption, Pakistan

Luck Cement – Rank #3 in Cement, MENA region

PAK Elektron (PEL) – Rank #5 in Home Appliances, South Asia

Interloop – Rank #1 Hosiery supplier to Nike/Adidas globally

Searle – Rank #2 Pharma exporter from Pakistan

Packages Ltd – Rank #4 in Packaging, Middle East

Hub Power (HUBCO) – Rank #1 Independent Power Producer, Pakistan

PSX – Rank #1 Stock Exchange, Frontier Markets

Bottom line: We don’t have Adani-level market caps yet, but we own textiles, IT, cement & fertilizer in the region.

Problem isn’t talent. It’s scale listing.

#Pakistan #PSX #Economy #KSE100 #MadeInPakistan #Exports

7

45

3,240

بزنس لیڈرز نے حکومت کی معاشی استحکام کی پالیسیوں کو سراہا ہے، تاہم سیلریڈ کلاس اور کاروباری طبقے پر ٹیکس بوجھ میں کمی اور ٹیکس نیٹ کی توسیع ناگزیر ہے۔ ایکسپورٹ لیڈ گروتھ کے لیے ٹیکسیشن ریفارمز اور برآمدات میں اضافہ وقت کی اہم ضرورت ہے۔

مصدق ذوالقرنین، چیئرمین Interloop Limited

12

15

116

May 30

[FNRP]

"So I've been scouting around interloop labs recently"

"Every now and then the voyager brings down a zero point from his ship"

"Now I'm not a rocket scientist but I'm assuming he's rebuilding the zero point"

"There's nothing that I can really do but report my findings"

4

252

May 29

Faisalabadi Seths are more rich, Interloop, Sitara, Ibrahim, are giants

1

3

13

1,020

May 29

Top 10 Textile Companies in Pakistan by Market Capitalisation.

(May 2026)

Interloop Ltd — Rs 115.4 billion

Kohinoor Textiles — Rs 84.2 billion

Nishat Mills — Rs 69.1 billion

Sapphire Textiles — Rs 29.7 billion

Feroze1888 Mills — Rs 25.1 billion

Sapphire Fibres — Rs 24.8 billion

Gul Ahmed Textile — Rs 21.8 billion

8

23

154

17,007

May 22

Interesting. Then will likely survive even if she’s got interloop Metz causing SBO. She needs to be strong enough for suppressive therapy bf the TIL tho. When was her surgery 4/27?

1

1

122

May 18

Today I’ve been marks the 20th year at job in @InterloopLtd . To all the great people I’ve met and worked with "Thanks"! It’s been a wild, wonderful ride. Thank you for being an essential part of my 20 years journey in Interloop.

1

1

3

53

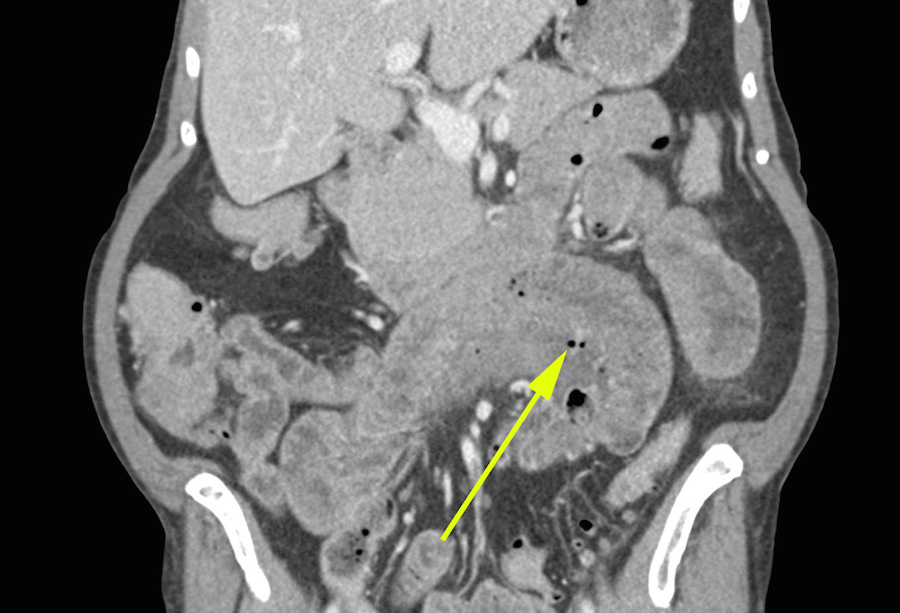

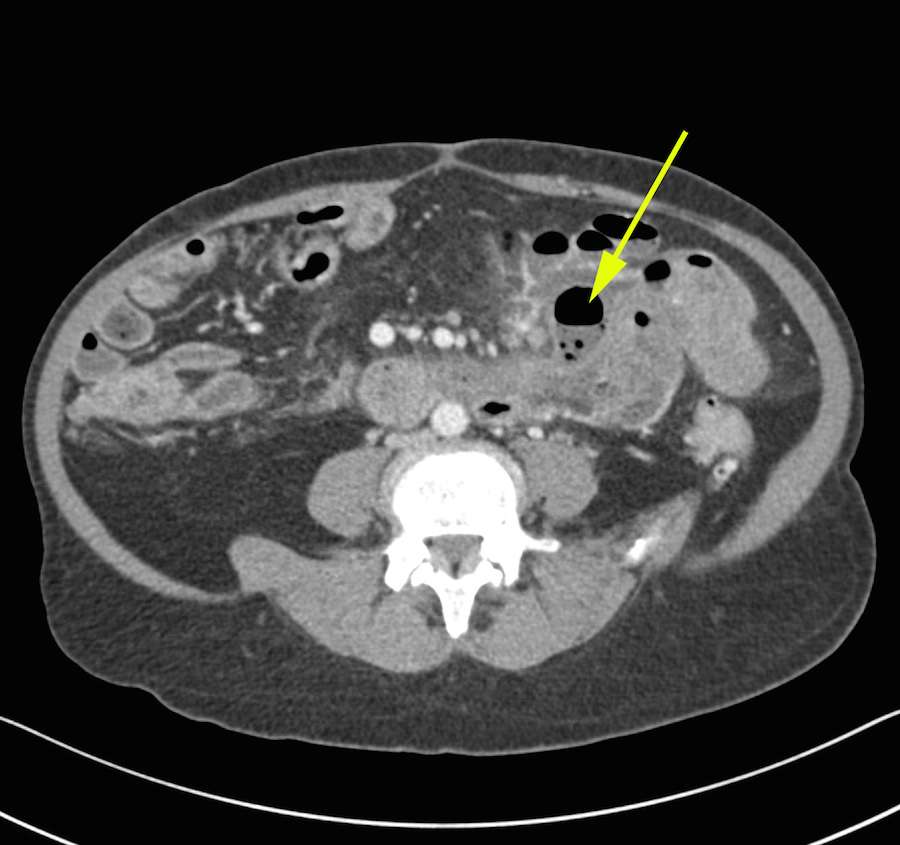

Jejunal Diverticulitis with Interloop Abscess

2

24

1,378

NASCAR

NASCAR

Has Interloop really provided solid returns except in the few years after IPO?

Why not ENGROH and POL ?

Any preference for having MARI among all other Energy chain listed companies ?

1

3

605