19 Dec 2024

Inventurus Solutions : शानदार लिस्टिंग, अब क्या करें?

@ResearchVivek

#InventurusIPO #IPOAlert #IPOListing #stockmarketnews

1

5

643

19 Dec 2024

Inventurus Knowledge Solutions IPO Listed 1856.00 where IPO Price is 1329 Rs.

Profit in Percentage : 39.65%

#IKS #iksipo #InventurusIPO #Inventurus #InventurusKnowledgeSolutions

4

759

19 Dec 2024

5 minutes chart pf Inventurus knowledge solutions IPO

Clean break out at 1930

There was entries at both 1897 and 1930 rs

Those who got allotments congratulations if you are still holding

#IPOAlert #InventurusIPO

1

383

19 Dec 2024

volume rush is happening at inventurus Ipo side

adrenaline rush is happening at my side😅😅

Try to watch charts in 1 min or 5 min .... lot of things you can learn

#InventurusIPO #IPOAlert

19 Dec 2024

Whatttaa aaa closing in inventurus knowledge IPO

last 20 mins thriller

enjoyed watching it in 1 min chart

HUGE VOLUMES in last min 20 mins

closed very strongly

moved from 1920 to 2020

#IPOAlert #InventurusIPO

1

2

208

19 Dec 2024

Bought Inventurus Knowledge early morning at average price of 1898 rs as it was breaking out

and was checking the one minute chart

last 20 mins was mind blowing 🤯🤯🤯

really enjoyed watching it

#InventurusIPO #IPOAlert

2

1

260

19 Dec 2024

Whatttaa aaa closing in inventurus knowledge IPO

last 20 mins thriller

enjoyed watching it in 1 min chart

HUGE VOLUMES in last min 20 mins

closed very strongly

moved from 1920 to 2020

#IPOAlert #InventurusIPO

1

1,178

19 Dec 2024

#OnETNOW | "In next 3 to 5 years, earnings growth will be faster than revenue growth," say Sachin Gupta and Nithya Balasubramanian of IKS Health as the company lists on the bourses today

These are the statements on margins, regulations in healthcare, tech talent and more👇

@ikshealth #StockMarket #InventurusIPO #iksipo

1

5

2,004

19 Dec 2024

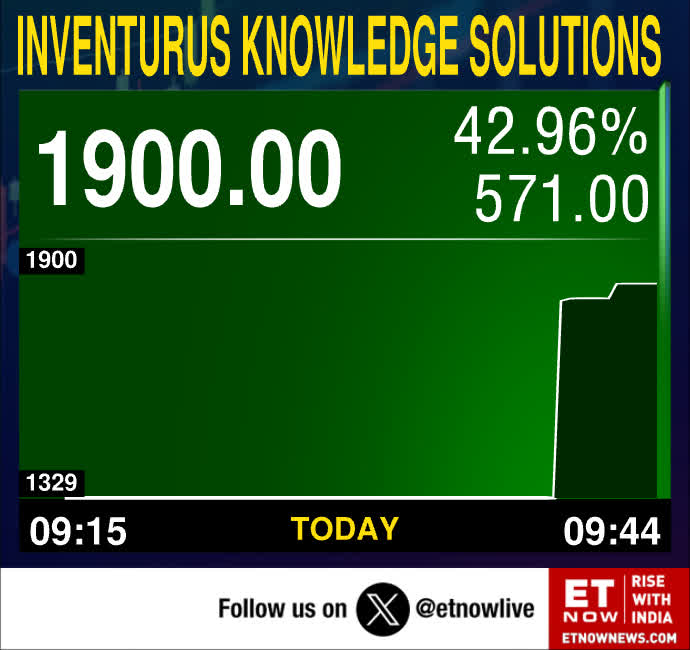

#MarketsWithBS | Shares of Inventurus Knowledge Solutions made a strong #DStreet debut on Thursday, in an otherwise weak market. On #NSE, Inventurus Knowledge Solutions shares listed at Rs 1,900, reflecting a premium of 42.96% per share against the issue price of Rs 1,329.

#InventurusIPO @KGaurav2806 #markets #sharemarket #stockmarket

mybs.in/2dbIPb9

1,275

19 Dec 2024

As expected, the listing happened as anticipated -

Inventurus Knowledge Solutions IPO Listing Details -

Listing Price ( NSE ) - ₹1900.0

Offer Price - ₹1329

Listing Premium - 42.96%

Profit -

1 Lot Retail Profit - ₹6,281

HNI Profit - ₹87,934

#InventurusIPO

#IPOListing

15 Dec 2024

Inventurus Knowledge Solutions Ltd. ( IKS Health ) IPO , Close Tomorrow ( 16 - 12 - 24 )

Final View - Subscribe due to strong fundamentals, robust financials, and alignment with trends in digital healthcare growth. However, the high valuation and concentration risks should be carefully considered , the biggest negative point is that it is full of OFS.

SWOT ANALYSIS -

Strengths -

1. Strong Client Retention and Diverse Client Base - 98% of revenue is from repeat customers, demonstrating strong client loyalty.

Serves 778 clients, including major organizations like Mass General Brigham Inc. and Texas Health Care PLLC.

2. Technologically Advanced and Scalable Business Model - Technology driven solutions with a focus on automation, data analytics, and digital tools.

Asset-light, scalable model contributing to profitability and cost-efficiency.

3. Global Workforce and Expertise - Over 13,528 employees, including 2,612 clinically trained professionals.

Strong domain expertise in healthcare outsourcing and operations.

4. Acquisition of Aquity Holdings - Expanded clinical documentation and revenue cycle management services, enhancing growth potential and service offerings.

Weaknesses -

1. Geographic and Revenue Concentration - Overdependence on the US market: 95.78% of revenue comes from the US, creating vulnerability to risks in this geography.

Forex Risk - Exposure to currency fluctuations due to international operations.

2. Reliance on a Few Large Clients - Heavy reliance on a small number of large clients, which may impact stability if major clients are lost.

3. Limited Diversification Outside Healthcare - The company’s focus is largely on healthcare, limiting diversification across other sectors.

4. Debt Financing - Despite being net cash positive, the company has significant borrowings, which may impact profitability ratios and flexibility in operations.

Opportunities -

1. Growing Demand for Digital Healthcare Solutions - Increasing demand for SaaS-based healthcare solutions and compliance with healthcare regulations.

Opportunities for growth in emerging technologies like AI, telehealth, and robotic process automation ( RPA ).

2. Inorganic Growth via Acquisitions -

Potential for further expansion through acquisitions, as demonstrated by the acquisition of Aquity Holdings.

3. Global Healthcare Digitalization Trends - Rising adoption of digital healthcare platforms across geographies beyond the US, such as Canada and Australia, offers market expansion potential.

Threats -

1. Cybersecurity Risks - Exposure to sensitive healthcare data, which makes the company vulnerable to cyberattacks and breaches.

2. Risk of Technological Obsolescence -

Healthcare technologies are rapidly evolving, and failure to innovate could result in losing competitive advantage.

3. Regulatory and Compliance Risks -

Increasing global regulations around healthcare data and technology can lead to higher compliance costs and operational challenges.

4. Economic and Market Volatility -

Global economic uncertainty, geopolitical risks, and changing healthcare policies may impact profitability.

Financial Overview -

1. Revenue Growth -

FY23: ₹10,313 Mn

FY24: ₹18,179 Mn

Revenue has grown significantly, with a CAGR of 54.29% from FY22 to FY24.

2. Profitability -

PAT ( FY24 ) - ₹370.49 Cr ( 20.38% margin )

EBITDA ( FY24 ) - ₹5,203 Mn ( 28.6% margin)

EBITDA Margin: Reduced from 38.9% in FY22 to 28.6% in FY24, but still strong.

3. PE Ratio: The company has a PE ratio of 55 ( Post Ipo ) at the upper price band, indicating high growth potential but also higher valuation risk.

I am Not Sebi Registered ...Views are Personal . DYDD

#Inventurus

#IKS

#IPOAlert

@Anuj17544072

@CAShubhamGoel1

@Vaibhav_99_

@SanketAgrawal99

@manoj38826

3

688

19 Dec 2024

#MarketAlert | Bumper D-Street debut for IKS Health!

IKS Health lists at Rs 1900 - a premium of 43% to issue price, this is the latest update👇

@ikshealth #StockMarket #InventurusIPO #iksipo @NSEIndia

19 Dec 2024

LIVE | D-Street debut for IKS Health; WATCH👇

@ikshealth #StockMarket #InventurusIPO #iksipo @NSEIndia x.com/i/broadcasts/1vOxwrodd…

1

1

4

2,665

19 Dec 2024

Inventurus IPO की दमदार लिस्टिंग! हर शेयर पर हुआ इतना मुनाफा, झुनझुनवाला फैमिली ने भी कर रखा है निवेश

#InventurusIPO #IPO

zeebiz.com/hindi/stock-marke…

1

1

1,824

19 Dec 2024

LIVE | D-Street debut for IKS Health; WATCH👇

@ikshealth #StockMarket #InventurusIPO #iksipo @NSEIndia x.com/i/broadcasts/1vOxwrodd…

2

4,918

19 Dec 2024

#MarketAlert | New listing: Inventurus Knowledge Solutions pre-open indicative price👇

@ikshealth #StockMarket #InventurusIPO #iksipo

1

4

1,937

19 Dec 2024

Inventurus Knowledge Solutions IPO

IPO Price: 1329

Listing Price: 1856 🔥

Gain: 39.65% 🔥

Retail Profit: 5797 🔥

#IPOListing #InventurusIPO

3

1

42

4,578

18 Dec 2024

18 Dec 2024

ALLOTMENT OUT

International gemological institute (IGI) IPO

Link :

kosmic.kfintech.com/ipostatu…

Congratulations for who ever got it.

#IPOAlert #ipoallotment #Christmas

#InternationalGemmologicalInstituteIPO

2

2

4

410

#InventurusKnowledgeSolutions #Latest #GreyMarketPremium

For more such #Updates and #MarketInsights visit my.soctr.in/x & "follow" @MySoctr

#Nifty #nifty50 #investing #BreakoutStocks #Breakout #Nse #nseindia #Stockideas #stocks #StocksToWatch #StocksToBuy #StocksToTrade #StockMarket #trading #Nse #Nseindia #Stocks #Trades #StocksInNews #stockmarkets #Experts #Investment #Strategy #Revenue #Growth #Investors #Investor #Returns #Margin #stockmarketindia #Outlook #Overview #Earnings #InventurusIpo #InventurusKnowledge #InventurusKnowledgeIpo #ApplyIpo

3

344

18 Dec 2024

#Inventurus Knowledge Solutions #IPO Allotment is Out.

Check the status.

linkintime.co.in/initial_off…

Listing Date: 19 Dec 2024

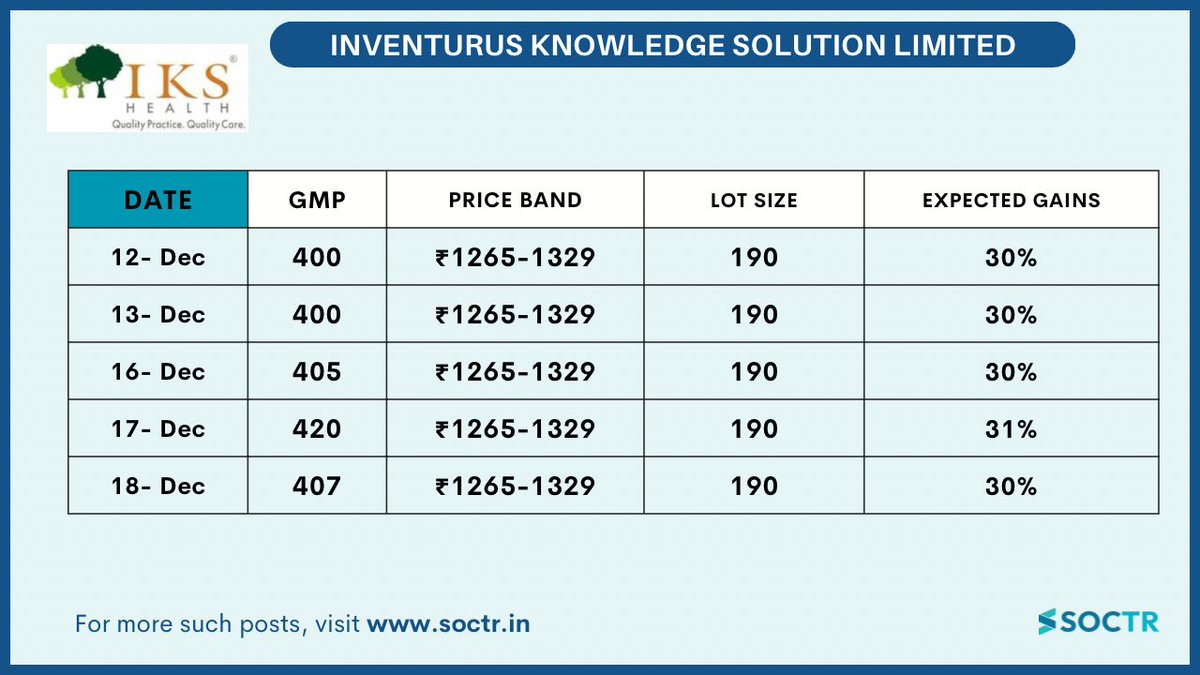

GMP: 407 (30.62%) 🔥⬆️

#IPOAlert #GMP #InventurusKnowledgeSolutions #IPO

#MainboardIPO #InventurusIPO

2

625

17 Dec 2024

I had got 1 allotment in #InventurusIPO

Very fair allotment.Registrar had done his part to best he can

#mobikwik #SaiLife #vishalIPO #VerifiedBySensibull #Bitcoin #nse #bse #fii #x #Inventurus #JUSTIN #igiil #BREAKING #nifty #banknifty #sensex #StockMarketIndia #forex #stocks

17 Dec 2024

Got 1 allotment in #InventurusIPO and no allotment in #YashHighvoltage #IPO friends. All together a good day

#mobikwik #SaiLife #vishalIPO #VerifiedBySensibull #Bitcoin #nse #bse #fii #x #Inventurus #JUSTIN #BREAKING #nifty #banknifty #sensex #StockMarketIndia #forex #stocks

9

3,592

17 Dec 2024

➡️Allotment Out.

👉 Inventurus Knowledge Solutions IPO

Link :

linkintime.co.in/Initial_Off…

#IPOAlert

#InventurusIPO

1

308

17 Dec 2024

ALLOTMENT OUT 👉

Inventurus Knowledge Solutions IPO Link : linkintime.co.in/Initial_Off……

Anyone got it?

#IPOAlert #InventurusIPO

2

459