Jun 12

Mr Market doesnt see it this way with $JSECCD getting slaughtered on a pretty positive day!

1

1

188

Jun 11

There you go - $JSECCD

“ MVNO market will triple in 4 years”

Jun 11

Africa Analysis forecasts that the South African MVNO market will triple in 4 years and become the growth engine of South Africa’s cellular market. mybroadband.co.za/news/cellu…

1

5

1,785

May 26

Pepkor - $JSEPPH

- Return on Assets 20,7% ✅

-Pepkor Holdings’ cellular business has pivoted decisively from selling phones to financing them, the JSE-listed retailer’s interim results showed on Tuesday, with its smartphone rental book swelling to R2.6-billion in the six months to 31 March 2026 even as overall handset volumes plateaued. ✅

The group’s FoneYam smartphone rental product activated 1.3 million new accounts during the half – growth of 32% from the comparable period – taking its active customer base to 2.4 million. The rental book has grown from R1.7-billion a year ago, a 53% expansion in 12 months.

Total handset sales across Pepkor’s brands, by contrast, came in at roughly 6.7 million units for the six months – broadly flat against the 6.8 million recorded a year earlier, when the group cited GfK data showing it sold eight of every 10 prepaid handsets in South Africa. That market share figure is not included in this set of results. ✅

Pepkor’s active cellular Sim base now exceeds 30 million, delivering revenue that grew to R1.1-billion

At Pep, 4.9 million handsets were sold (up 4.1%) and 750 000 FoneYam accounts were activated (up 42%). At Ackermans, 1.6 million handsets were sold (up 6.2%) and 531 000 FoneYam accounts were activated (up 14%). TechCentral. ✅

Technically - Reversal in play over R22,35! One to watch with TPs at R33-34.

Small positive for CellC $JSECCD - The rent to buy smartphone program is offered in partnership with CellC. ✅

3

15

3,884

May 21

$JSECCD - Exepecting them to come in with decent Year end numbers!

Fwd 4.4 PE ....!

May 21

Allan Gray believes Cell C’s transformation has made it an attractive investment despite its previously complex structure and troubled past.

dailyinvestor.com/investing/…

1

5

1,929

May 7

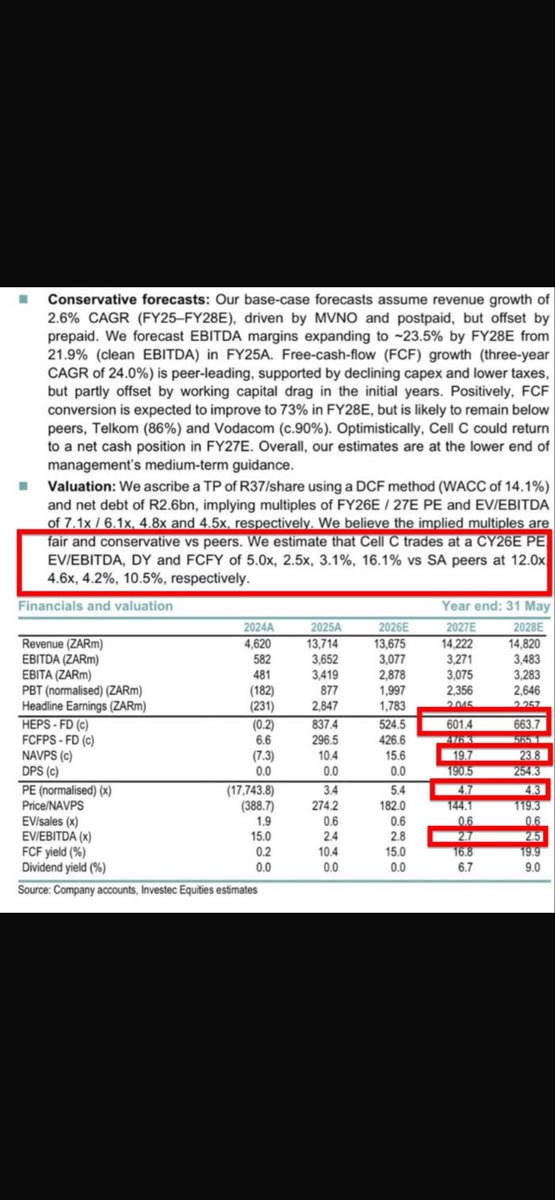

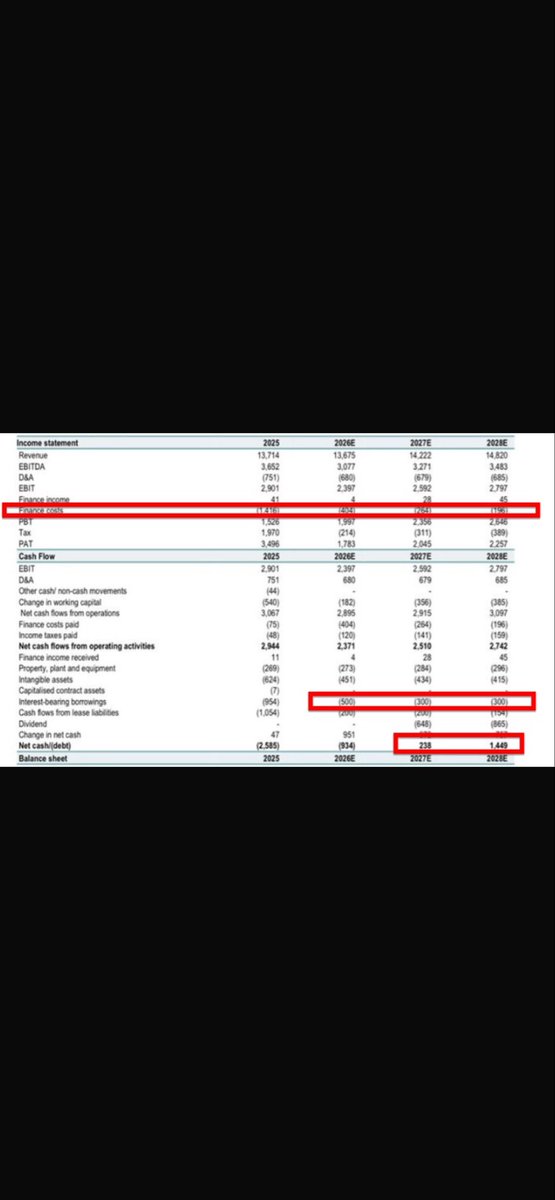

CellC ( $JSECCD )

From Investec’s 64 page coverage.

Highlights : ( using conservative no”s)

- Stock is 5 PE vs peers 12 PE

- EV / EBITDA - 2,5 x vs 4,6 peers

- FCF yield 16% vs peers 10,5%

- DY in 27 of. 6,7% vs 4,2% … going to 9%.

- Company already paid R500m ( Balance R1,4bn vs Handsets) at interim ( Debt), paying R300m pa.

- Interest payments from R404m to R264m to 196m etc.

- Means company is exp. To be NET CASH > R230m in FY 27 an R1,44bn in FY 28 - Post Divis!!

- EBITDA from R3bn to R3,5bn over next FY 26 to FY 28

Don’t believe me - see below!

1

7

1,603

Apr 22

Some worthy comparisons:

$JSECPI of Fwd 30 P/E

$JSEBLU just over 5 Fwd P/E ( used to command double)

$JSECCD just over 4,2 Fwd P/E

I still think the smart play here is for BLU to sell down CCD stake to 26% from 49,5% and for CPI to buy BLU ( 26% in CCD stake). Clear as chips the MVNO roadmap is leading to VAS / Fintech ops becoming the second largest profit contributor. Management will want to protect that MOAT IMO and taking BLU at a lower multiple to their biz while retaining the “ negative vote “ in CCD will be on their mind!

EE webinar tomorrow - $JSEBLU

DYOR

Apr 22

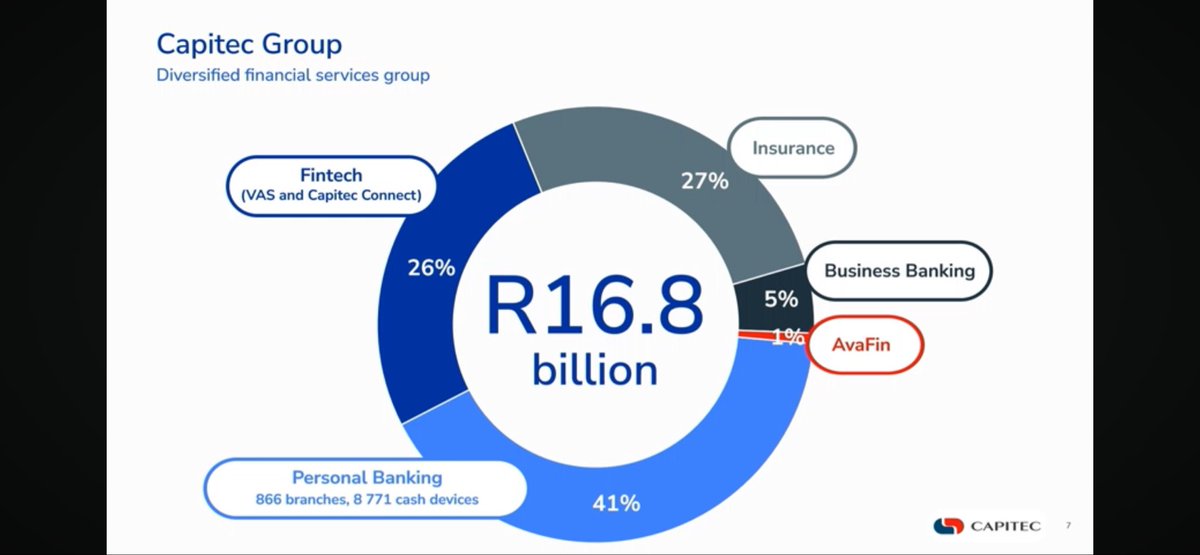

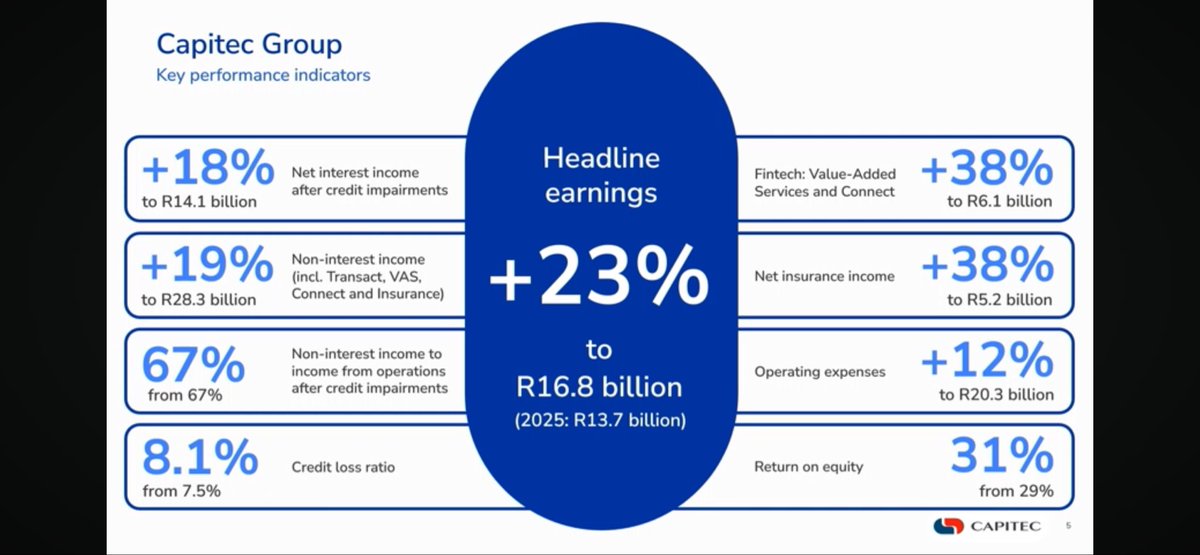

CAPITEC ( $JSECPI)

A good look through with Capitec Connect more than doubling its Net Income contribution to R442m. Capitec Connect runs on CellC s wholesale network.

Full FY2026 annual results deck (year ended February 2026).

Here’s the complete picture on Capitec Connect specifically:

Scale & Active Users

1.5 million clients active in the last 3 months, up 67% year-on-year. Data usage tripled — from 13.4 to 40.5 petabytes, up 202%. ✅

Voice

Free Connect-to-Connect calling launched as a new feature. 768 million minutes used, up 150%.✅

Pricing — passing savings back

Lower Connect data prices saved clients R330 million in the year. An additional R78 million worth of free data (3 petabytes) was given to clients. ✅

Total client savings across the whole bank attributed to Connect data and Capitec Rewards was R108 million.

Revenue contribution

VAS and Connect combined generated R6.1 billion, up 38% — and this segment now constitutes 26% of total group headline earnings of R16.8bn, making it the second-largest earnings contributor after Personal Banking (41%). ✅

Net transaction income including VAS and Connect reached R20 billion for the year, up 16%.✅

New product — Connect Devices

Launched in FY26: Apple and Samsung devices orderable via the app, delivered in 3 days, payments from R181/month with zero deposit, bundled with 12 months of free 5GB data. No network locking. ✅

Strategic positioning

On the forward-looking strategy slide, “Connect and Insure” is explicitly named in the Accelerate bucket — meaning management views it as a near-term growth driver, not a peripheral product.✅

Bottom line: Connect has moved beyond proof-of-concept. 1.5 million active MVNO subscribers, tripling data volumes, a device financing offering, and now 26% of group earnings coming from the Fintech (VAS Connect) segment.

The deliberate price-to-grow strategy — sacrificing ARPU for subscriber growth — is textbook for an MVNO using the banking relationship as the acquisition channel.

With CellC $JSECCD providing the wholesale vertical and Blue label Unlimited $JSEBLU providing the aggregator vertical ( processing majority of CPIs prepaid and large VAS transactions - this level of Growth ( as above) should be seen as a positive !

1

2

9

2,821

Apr 22

CAPITEC ( $JSECPI)

A good look through with Capitec Connect more than doubling its Net Income contribution to R442m. Capitec Connect runs on CellC s wholesale network.

Full FY2026 annual results deck (year ended February 2026).

Here’s the complete picture on Capitec Connect specifically:

Scale & Active Users

1.5 million clients active in the last 3 months, up 67% year-on-year. Data usage tripled — from 13.4 to 40.5 petabytes, up 202%. ✅

Voice

Free Connect-to-Connect calling launched as a new feature. 768 million minutes used, up 150%.✅

Pricing — passing savings back

Lower Connect data prices saved clients R330 million in the year. An additional R78 million worth of free data (3 petabytes) was given to clients. ✅

Total client savings across the whole bank attributed to Connect data and Capitec Rewards was R108 million.

Revenue contribution

VAS and Connect combined generated R6.1 billion, up 38% — and this segment now constitutes 26% of total group headline earnings of R16.8bn, making it the second-largest earnings contributor after Personal Banking (41%). ✅

Net transaction income including VAS and Connect reached R20 billion for the year, up 16%.✅

New product — Connect Devices

Launched in FY26: Apple and Samsung devices orderable via the app, delivered in 3 days, payments from R181/month with zero deposit, bundled with 12 months of free 5GB data. No network locking. ✅

Strategic positioning

On the forward-looking strategy slide, “Connect and Insure” is explicitly named in the Accelerate bucket — meaning management views it as a near-term growth driver, not a peripheral product.✅

Bottom line: Connect has moved beyond proof-of-concept. 1.5 million active MVNO subscribers, tripling data volumes, a device financing offering, and now 26% of group earnings coming from the Fintech (VAS Connect) segment.

The deliberate price-to-grow strategy — sacrificing ARPU for subscriber growth — is textbook for an MVNO using the banking relationship as the acquisition channel.

With CellC $JSECCD providing the wholesale vertical and Blue label Unlimited $JSEBLU providing the aggregator vertical ( processing majority of CPIs prepaid and large VAS transactions - this level of Growth ( as above) should be seen as a positive !

2

10

31

6,688

Apr 14

Data Centre bottlenecks:

One could argue all our listed telco companies and plays like $JSEDTC have some advantage here. CellC $JSECCD just Capexed for 2 x new Data centres for its MVNO growth! $JSEMTN is partnering with global players to role out Data Centres in Africa. $JSETKG a clear winner also with BCX!

Cyril has suggested there’s a pipeline of R50bn of Data centres to be built - my question is how ? There’s a global shortage of parts with lead times up to 2 years for certain parts including transformers etc.

Existing Data Centre / Infrastructure should be “ re-valued “ higher ( due to replacement cost)!

Coreweave $CRWV just hiked prices 20% for its services! $NBIS just went to ATH !

2

742

Feb 16

$JSEBLU BLU LABEL UNLIMITED big reset is coming: 'Kitchen sink' interims, $JSECCD CELL C IPO insights, and a clear path to 10%-15% FCF yields! Insiders have been buying. Time to accumulate? Have you? Dive in: sharenet.co.za/views/article…

1

9

1,771

Feb 14

$JSECCD

$JSEBLU

- Mostly INLINE update rel. to pro forma

- if you adjust back the IPO costs ( front loaded to Adj EBITDA and consider 2H CEC we get to R2,95bn EBITDA ( R917m 250m ( 1H) R1167 300m 220m 125m (2H)- ( FY 26 Norm)! - IPO cost R250m CEC R300m , Man fee reversal R220m, TPC Dis R125m.

- Operating CFs normalise with one offs - Int paid R400m falling away ( paid to BLU), lease and Repayment of Int bearing dropping ( now under R280m pa) and R190m for Intangible ( writedown of Spectrum), prop purchase R110m. This should see Operating CF normalise too R2,2bn to R2,4bn pa!

- Reminder Tax rate will be 20% ( not 27%) - Depr R550m and New interest cost ( lease ) R270m =R1,65bn NP an FCF around R1,4bn for FY26 ( adj for one offs)! ( assuming R200m WC)

CEO Mendez very Bullish on 2H coming through on Revenue and margins. Should see impact of Shoprite and Pepkor prepaid especially move up. Whole sale flying and is expected to hold CAGR over 20% - moving R2bn to R4,5bn in Revenue in 5 years alone!!! MVNOs now 5,1m reg subs!

I mentioned BLU would have the Impairment ( tweet below), CellC showed the R3,5bn through Other Income! Silly sell off in BLU on Friday IMO!!

New B/S and New I/S now , … after these numbers much easier reporting AFS to come ( this is the kitchen sink) I see a path for BLU to pay 5% DY ( incl Special ) this year and around 8% in FY27 ( assuming BEE SPV divis flow to BLU )! This is why the CEOs bought 20m shares last year IMO - rising DYs to come!

DYOR - these are my own assumptions.

Feb 3

$JSEBLU

BLU will report later in the month( Interims) - 20th Feb. It’s important to understand that this is the proverbial “ Kitchen Sink” numbers. As such we should see a T/S with a < 20% decrease due to the IPO.

Simply put BLU converted old loans and data worth R13bn and sold

It in the IPO for R9bn ( lower than what th street expected). Thus, leaving an Impairment of R4bn . This is at least in the current price as the IPO happened in Nov ‘25 and should not come as any surprise on reporting!!

For some context , you should know that of the R7,5 bn in data they sold for CellC Equity , BLU only paid R4,4bn ( as CellC gave a Discounts). In addition the R3,75bn Debt to Equity conversion - the real number BLU placed was R1,9bn ( originally) before the rollup over the years!

BLU also sold CEC back to CellC so BLUs EBITDA will be as a consequence lower ( what they get back is 50% earnings in CC) . But the offsets here would be the interest cost they no longer have to pay on CEC loan -R230m a year. The new EBItDA I’m suggesting could be around R800-1bn ( from 1,4bn ) pa. If we look at the post IPO in CellC - BLUs “Investment in Assoc” will be weighted at 49,8% of CellC profits / dividends.

The bigger picture here is - BLU is likely on a GROUP level to report earnings ( combined with CC) of 120-150c for the year. This will be high FCF returns ( esp in 2027/8). It’s likely to expect there will be pro forma numbers due to consolidation , to de consolidation.A NB reminder here is that the impairment is on the CellC Asset sale , it’s NOT an earnings related impairment!! If anything we expect CellC to come in and beat guidance from the PLS!

Now for the good news , this is the extent of it all. We now have two very low cost , low debt operators with Fintech platforms and hence forth crispy clean ( Aug 26) AFS. For BLU it’s now about adding the “ Treasury functionality into the next 6 months an update on their Energy strategy ( where they have just started working with 2-3 Municipalities in SA - High margin biz).

Additional kickers come in the form of SPECIAL DIVIDEND ( 80% probability ) mentioned in Oct last year, my best guess is this is 20-30c range ( outside chance 50c). BLU is also owed R1,4bn on the BEE Sale which moves to R1,65bn by year end. This is 18% of their market cap. This gives them HUGE ammo for capital allocation - Buyback and further special dividends ( if BEE holders get bank funding or sell to new BEE investor at year end)We are also very confident they will initiate an interim dividend in Aug with a focus yield over 5% (IMO)!

Now, CellC aren’t expected to pay a dividend this year but it’s suggested there’s a chance shareholders can vote to elect one still. The market has them paying 7% in 27 and 9,6% in ‘28.

This will be a big contributor to BLU and should see CellC rerate from 6 PE to at least 10 vs peers at 12-15 PE presently. Finally, don’t rule out any corporate action - CellC unbundle could happen in some form ( can’t rule out) or new strategic BEE investors ( I would assume once price moves 20-30% from IPO level).

The price has come back to a great accumulate zone - -950c a good risk reward for a high FCF ( Yes - there will be some Operating CF movements for CellC data purchased that we need to strip out) company looking to reward shareholders after years on the back foot. They have it all to prove.

To recap BLU s EBITDA is likely 1bn 50% CellC R1,5bn = 2,5bn ( rough numbers ). BLUs mkt cap is R8,5bn 1bn debt -cash this stock is trading on a EV / EBITDA < 4 !! FCF is likely to be 10-15% on a “forward basis”. This is what Gold miners are basically pushing through now after the commodity rallies. You can own a high FCF biz like BLU without the cyclical nature of mining companies!

The brothers bought 20m shares in November ( representing 2,4% of co) at roughly 960c \- in Nov 25 , before the closed period!

This is Anchors Top pick I’m told!!

DYOR!!

3

1,377

Feb 13

$JSECCD H1 FY26 results are in! Fresh off their JSE listing, they've turned things around with a deleveraged balance sheet (net debt/EBITDA just 0.6x) after major restructure. Revenue up 1.8% to R5.68bn, adj. EBITDA R917m, and a whopping R3.36bn profit thanks to debt waivers. Key wins: Wholesale 23% on MVNO boom, data traffic 43%. Subs hit 8.6m! Outlook bright with CEC integration fueling growth. sharenet.co.za/v3/sens_displ…

2

4

1,437

11 Dec 2025

Nice interview for those that are still on the Fence - CellC - $JSECCD

@FinanceGhost nice one , perhaps try get the BLU managment on in the future to dig into their Growth strategy and plans ??

ghostmail.co.za/ghost-storie…

1

2

1,158

9 Dec 2025

This article by Capitec included a little nugget of information about "rewarding clients with real value". My read is that it hints at how mobile offerings are being transformed into a complement to other goods and services (e.g. 👇 banking and FMCG retail).

$JSECCD

1

3

458

Cell C $JSECCD : The IPO was bleeding, heavily undersubscribed and on life support.

Then Allan Gray rode in with a 15.54% stake (effectively anchoring it, as its 50% of the public float) and saved the IPO.

The same Allan Gray already owns 14% of Blu Label, the parent.

6

7

43

5,962

27 Nov 2025

Cell C $JSECCD begins trading today. The listing price was confirmed below the offer range at R26.50. This makes the share very cheap relative to the sector (forward PE of 6 times versus ~11 times for peers). We have a fair value of R30.28 on the stock.

1

2

5

1,376

26 Nov 2025

Jorge mentioned they unlocked “ Significant commercials “in Sept - when it was 1,2m rentals mentioned!

$JSECCD

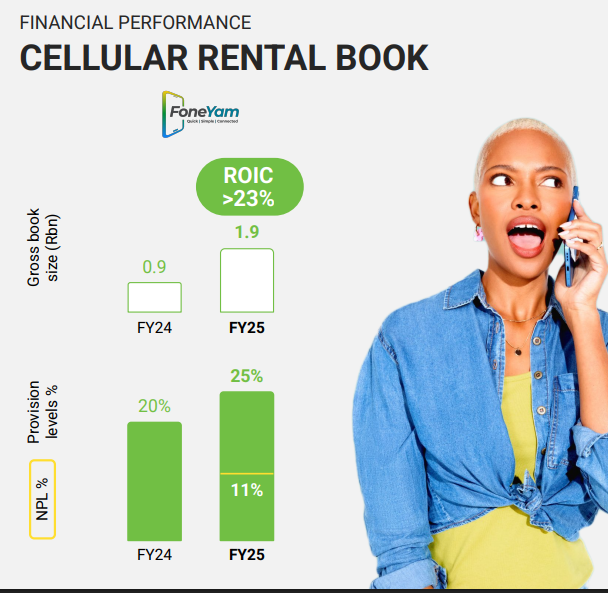

26 Nov 2025

Interesting that Pepkor earns a > 23% ROIC on their FoneYam Cellular Rental Book.

- 2m customers now who need financing to get a smartphone.

- 12M rental contract despite 25% ECLs - still make an excellent ROIC.

3

1,177