Jun 14

speculative high risk/high reward shitcos with charts (no paywall): annualizethis.substack.com/p…

LPTH LightPath Technologies starter position adds at bottom of flag

BFLY Butterfly Network buying dip still

WOLF - Wolfspeed

HIMX - Himax Technologies

ADTN - Adtran Holdings

HYLN - Hyliion Holdings adding on dip to UTL

POET Photonics - Currently minimal position, as it has become controversial.

SIVEF Photonics - Recently sold 1/2 my position (though it current holdings are still substantial) as I believe valuation has gotten way ahead of itself

INV AI - Owns an asset that is best in breed for 2 phase data center cooling - huge TAM market, and that Accelcius asset worth twice the current market cap of INV - I sold this one down on shortseller accusations of fudging their 1st datacenter deal.

KRKNF Defense/Robotics - Supplier to Andural, and play on Ocean defense spend - Peeled some off higher, looking to add back ..looking to add at target/s below

NRGV Energy & SMR - BESS (Battery Energy Storage Systems) data center /energy storage rebuilding of the grid play - huge TAM, continued insider buying by CEO, large position, would like to add but waiting for earnings.//UPDATE - on earnings call CEO made it clear this is a Q4/2027 story - so no add, but pleasantly surprised that stock holding up so far //Would like to add at lower bullseye (not clear I will get the chance)

TGEN Energy & SMR - Make Chillers and trying to break into the datacenter market…One hyper-scaler/neo-cloud potentially a $50M sale - partnered with Vertiv VS $150M market cap…one sale, and will re-rate. Waiting on earnings to see if any new traction

LODE Energy & SMR - Solar panel recycling -Might look to add at those rising MA’s coming up from below - nice size inside buys recently

RDW Space - Defense 2.0/Space play…P/E owner been dumping millions of shares artificially depressing the price - Peeled some off until i’m clear this is not a double top - looking to add back at bullseye if I get the opportunity // Haven’t added back yet

VELO Space - $400M Market cap - Only (?) 3D print system for larger format parts - space industry, and others….Insider owns size. looking to add at bullseye below (on UTL taps)

IQE (PF)

ASPI Energy & SMR - Finally acting well, looking to buy dips //Updated to add acting like shit again…

MYO added on Friday’s dip …position building still

AMSSY Took a placeholder position but am hoping it works it’s way down to the UTL where I want to get more aggressive…hopefully I dont miss loading up because I LOVE the risk/reward looking out a year or two

AIXI high risk - along with my all or none patent NLST …this one has a likely win in the China courts……

NLST Memory Patent litigation play…higher conviction than PRKR - but high risk/high (potential) reward never the less …Their trial was passed down to state courts from federal - no bueno

SGMO Healthcare/Bio Total SPEC / high risk…Sub .12 is sub $50M market cap VS $100’sM in product/platform/patents ….$20M cash left - worst case diluted into oblivion…will stay in for 6ish weeks - but want out before earnings likely

LPKFF Photonics I just bought the earnings dip in the 19’s - would add on any further dips

SHMD Machinery for glass substrates market (semi advanced packaging)…one of the few that can do it…small position until I see better/more market penetration outside of China…don’t like 12% margins….

LWLG Photonics - This is a late 2027 story IMO…been adding on dips

ONDS Defense/Robotics - Getting re-rated to reflect future millions/billions in sales - wrap up of multiple drone related companies… Want to add but want to make certain not a double top up here

BRUN - people smarter than I are questioning the valuation, so I have cut back accordingly….see how it acts at UTL below if it gets there

NNBR Data-center play busbars as well as connectors for chip/server-cooling. starter position adding on dips

1

1

406

Jun 12

$LPKFF offers exposure to two emerging themes: advanced packaging and aerospace manufacturing.

@aleabitoreddit highlights that LPKF may have links to the SpaceX supply chain, while the company's long-term thesis remains tied to glass substrate processing and next-generation packaging technologies.

4

3

388

Recommend people see @ShawarmaCapital on $LPKFF for this. Incredibly vested interests for transformation in small cap German gas’s equipment manufacturer. Would write this up but he’s done all the work already.

2

342

Jun 8

오늘 포트폴리오는 금요일 하락분을 모두 상쇄하고 ATH를 갱신했습니다.

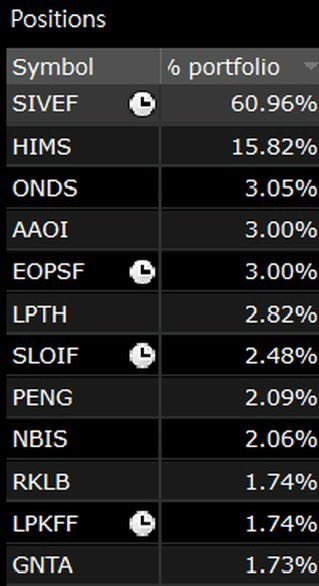

26.06.08. 포트폴리오 비중.

SIVEF 51% HIMS 31% IQEPF 4.5%

LPKFF 3.5% AAOI 3.5% ONDS 1.5%

다시 하락 할 수도 있겠으나 더 살 뿐 아직은 정리할 때가 아니라 생각합니다. 오후 장 봐서 다른 종목들도 쇼핑 좀 해야겠습니다.

90

Jun 8

Wait until more institutions follow suit and buy SIVEF also LPKFF and SLOIF as well in the future !

1

1

264

Jun 8

I 💯 agree with what you say. Dollar cost averaging into a diversified index is a great discipline to learn young and continue with ad infinitum.

I believe where I diverge is on the question of whether putting 100% of your $ in a portfolio consisting of $AAOI, $INFQ, $SIVE, $NBIS, and $LPKFF is wise at this point in the cycle.

2

11

1,843

1

4

6,519

Jun 7

$LPK 今年从 €6 涨到 €24,翻了 4 倍。

空头的结论是:“一家亏损的专利公司,市场在为 2028 年的幻想买单,最后必然暴雷增发。”

他说对了一半,也算错了一半。

对的部分我先认:2025 年营收才 1.15 亿欧、经营仍亏损、当前财报确实难看。

但用财报快照否定 $LPK,本身就是错的框架。这是一个资质认证周期(qualification cycle)的票,逻辑跟 $AEHR 一模一样,量产爬坡前,当期收入不重要,重要的是谁卡住了工艺。

而 $LPK 卡住的,是玻璃基板做 TGV(玻璃通孔)唯一可靠的量产工艺 LIDE:300 项专利、全球主要厂商里 80% 选了它的设备、Intel 和 Samsung 已经是客户。

关键一句:它的官方指引里根本没算先进封装的量产订单。也就是说,H2 任何一笔量产订单落地,都是纯粹的超预期。CEO 最近还自己掏钱在二级市场增持。

你买的不是今天那张财报,是 2027 年所有人都绕不开的那台机器。

时间点你押 2027 还是 2028?评论区说说。

$LPKFF

3

1

16

3,894

St.Moritz retweeted

Jun 5

$LPK $LPKFF yes, I’m still bullish. Plenty of upside as demand is insanely strong for the next gen AI chip ramp up! If you sold this because a pump and dumper bought it then sold it, you’re basically clueless 😂

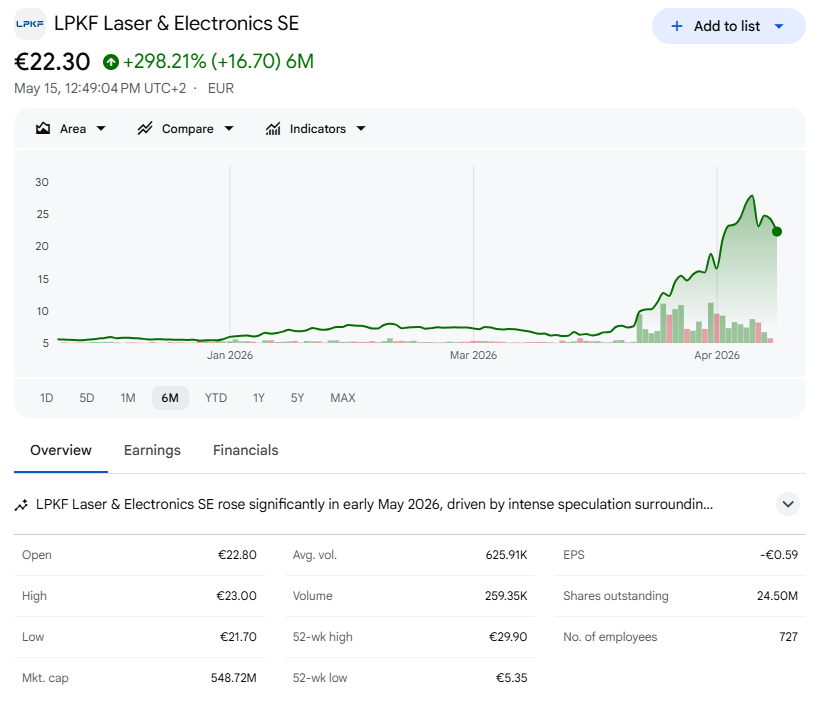

May 15

$LPK $LPKFF Part One of the Re-Rate is Complete. Part Two Takes Us to €1B Market Cap 🚀

I accumulated LPKF Laser & Electronics (LPK) at a sub-€200M cap because the market was sleeping on the company's essential LIDE technology for AI chip packaging. The thesis was simple and I laid it out at length: LPKF owns the only commercially viable, high-volume manufacturing (HVM) ready process for Through-Glass Via (TGV) formation in advanced semiconductor packaging. That process is Laser-Induced Deep Etching (LIDE), and every serious player in the glass substrate race is either qualifying on LPKF equipment or has already placed pilot orders. CEO estimates 70%-80% market share.

Today the stock trades around €22-23 on a market cap near €550M. Part one of the re-rate is done.

I want to be explicit about what that means. The first leg, roughly €5 to €25, was the market waking up to the existence of the LIDE moat. The next leg is anchored to a specific catalyst path that converts speculation into book-and-bill, and that leg takes us to a €1B cap.

The path is order confirmation from named tier-one customers. Management has guided to first LIDE production orders in Q2 2026 (June-July). The investor forum on June 18 in Hanover is where CEO Klaus Fiedler presents the long-term strategy, and that is the venue where I expect customer color and a hard ramp timeline. Q2 earnings on July 23 is the print where the order intake shows up in the numbers. AGM on June 4 brings in Dr. Arne Schneider, currently CEO of Elmos Semiconductor (a publicly traded German automotive semiconductor company), to the supervisory board. Schneider is a former CFO with five years running a listed German semi SE. The appointment signals two things: governance is being recomposed for the semiconductor pivot, and the board is adding financial discipline at the exact moment LIDE moves from R&D spend to capex and working capital scaling. This is the kind of board change you make when you are about to ramp.

On the customer identity question, the public evidence chain is already strong. Samsung Electro-Mechanics' Sejong pilot line was reported by TechSpot in May 2024 as having finalized its supplier list with Philoptics, Chemtronics, Joongwoo M-Tech, and Germany's LPKF, with the same confirmation appearing in Tom's Hardware citing ETNews and later in Digitimes January 2025 confirming Samsung Electro-Mechanics is working with Chemtronics and LPKF on various manufacturing processes. That is four independent trade outlets sourcing back to Korean primary reporting. On the $INTC Intel side, CEO Fiedler has publicly stated LPKF has been in exclusive paid co-packaged optics (CPO) development with a major US semiconductor partner for over two years. A granted 2023 Intel patent describes LIDE-formed TGVs in an Intel CPO architecture. Korean trade press named LPKF and SCHOTT as Intel's glass substrate collaborators going back to 2024. The UTI to LG Innotek route is publicly confirmed: LG Innotek formally announced a partnership with precision glass-processing specialist UTI in January 2026 to develop glass substrates for advanced semiconductor packaging, with UTI expected to handle the TGV process. LPKF is the plausible equipment vendor on that line given the absence of credible alternatives at HVM scale. Absolics in Georgia and DNP in Japan both run pilot lines that need this exact process. The $ONTO Onto Innovation PACE consortium membership puts LPKF tools in qualification at every member's program.

What we are seeing this week is healthy. The stock has done what it needed to do in a short window, and a pause here lets the technical setup reset before the catalyst cluster lands in June and July. Long-term holders are sitting through it because the catalyst calendar is right in front of us. Every dip into the AGM and the investor forum is a gift.

Catalyst stack into summer:

- June 4: AGM Hanover, Dr. Arne Schneider supervisory board confirmation

- June 18: Investor Forum, long-term strategy detail from Fiedler, expected customer color

- Q2 2026: First LIDE production orders per management guidance

- July 23: Q2 earnings, order intake shows up in the numbers

When the orders land and they are attached to a named tier-one customer, the cap moves through €1B with conviction. Management has been telegraphing this catalyst for two years and the evidence chain backs them up. I take them at their word and so does the supply chain.

This technology is essential for next-generation AI chips. Organic substrates are at their physical limit. Glass is the answer for 1.6T-class signaling, high-bandwidth memory (HBM) integration, and co-packaged optics. LPKF holds the patent stack and the qualification lead on the only HVM-ready process that produces defect-free TGVs at panel scale. At a €550M cap, we have merely begun.

I am a long-term holder. I am glad the momentum took a breather. Healthy.

Incredibly bullish LPK into summer.

1

16

5,729

I have some lpkff for glass!!! I’m buying more iqepf tm lol

1

3

61