lfg 🟢

0x8c1BEd5b9a0928467c9B1341Da1D7BD5e10b6549

Side with $LSETH

marketcap-community.guru/com…

Jun 12

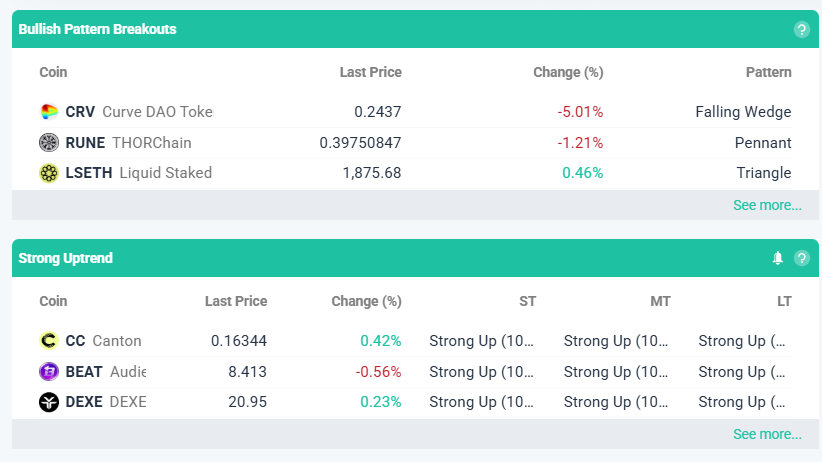

🚀 Crypto Market Highlights

Here’s what’s moving across the market right now:

📈 Bullish Breakouts

$CRV (Curve) → Falling Wedge breakout

$RUNE (THORChain) → Pennant breakout

$LSETH → Triangle breakout

👉 Momentum building after consolidation phases

🟢 Strong Uptrend Leaders

$CCC, $BEAT, $DEXE → Strong Uptrend (10/10)

👉 Strong uptrend across multiple timeframes

⚡ Momentum Turning Bullish

$BTC, $ETH, $BNB → Early bullish momentum inflection

$NEAR, $HYPE → Uptrend fresh MACD upside

👉 Large caps quietly strengthening

📊 Bullish Momentum Confirmation

$MANTA, $IDOL → MACD Buy RSI supportive

👉 Trend momentum alignment = higher conviction setups

🔄 Pullbacks in Uptrend (Dip Opportunities)

$HYPE (-8% 1W)

$BOBO (-5.5%)

$LAB (-18%)

👉 Watching for continuation entries

🔥 Overbought (Caution Zone)

$BEAT (RSI 97)

$VELVET (RSI 99)

👉 Possible short-term cooldown

🧊 Oversold (Bounce Watch)

$BCH, $DCR, $MX

👉 Potential mean-reversion setups

💥 Top Movers

Gainers: $ESPORTS ( 116%), $VELVET ( 115%), $XPL ( 38%)

Losers: $BDX (-63%), $BANANAS31 (-22%)

1

1

246

May 12

I have been critical of @Sharplink recently, and I've finally had the time to properly analyse $SBET's business operation and financial health based on the Q1 report. This will be a LONG update, so be warned!

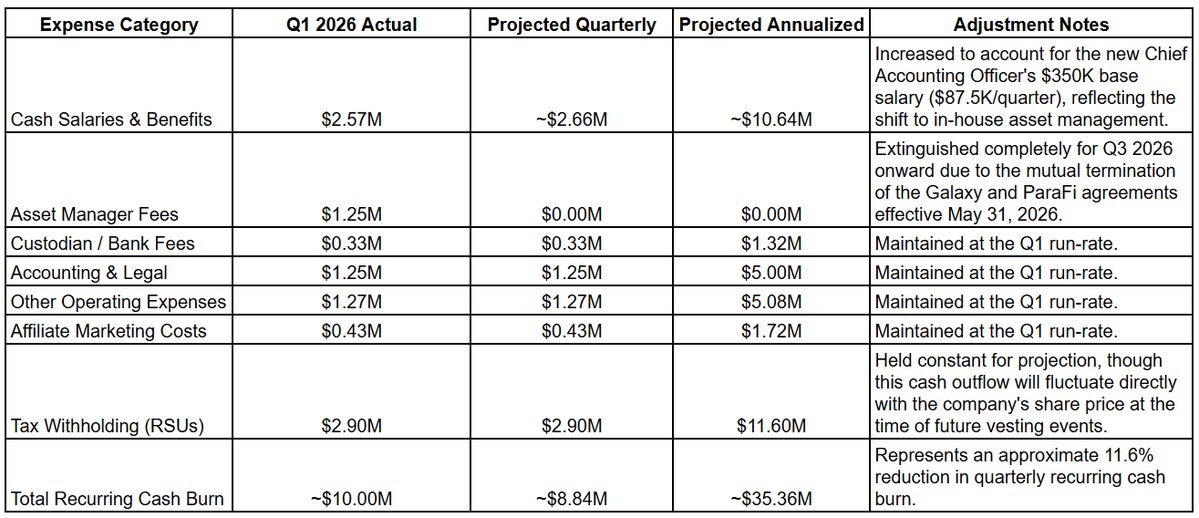

First, Sharplink has disclosed that they have $16.875M cash left on their balance sheet, down from $30.421M in Q4 2025.

This matters because they have recurring cash burn from business operations. Based on Q1 data, and the termination with external asset manager, I project a quarterly cash burn of $8.84M; annualized at $35.36M (see attached table).

Non-recurring costs come from:

• 2025 bonuses paid out

• Severance to former Co-CEO ($981K remaining)

• AP paydown

With $16.875M, they have roughly 2 quarters of operating cash left. Not pretty!

However, what I missed was that management has already prepared for the worst case scenario, in which cash becomes insufficient due to a prolonged mNAV discount.

From page 29 of Q1 2026 10-Q, there is a section that reads Loan Agreement. Sharplink has entered into a Master Lender Agreement with FalconX Charlie Inc. on Nov 26, 2025.

How it works:

• Sharplink can borrow US dollars OR specified digital assets under individually negotiated term sheets

• Borrowings are secured by collateral — USD, digital assets, or eligible securities

• Subject to initial collateral ratio and ongoing margin maintenance requirements

• No defined minimum or maximum loan amount

• FalconX has no obligation to approve any specific lending request (discretionary on their end)

• Loan fees calculated monthly and negotiated per draw

• Contains a termination event tied to specific valuation thresholds - meaning if collateral value drops past a defined point, the facility can be terminated and loans called

In conclusion, they have a way out without selling $ETH or diluting shareholders at compressed mNAV.

Second, Sharplink has entered a non-binding MOU to partner with Galaxy Digital to form the Galaxy Sharplink Onchain Yield Fund.

Details:

• The fund will deploy approximately $125 million. Sharplink is contributing roughly 80% of this capital.

• Sharplink will fund its portion using Liquid Staking Tokens (LsETH). This allows Sharplink to continue earning the baseline Ethereum staking rate while deploying the assets for additional yield.

• Both Sharplink and Galaxy Digital are acting as Limited Partners (LPs) in the fund. Galaxy Digital acts as the General Partner (GP) and manager.

• Galaxy's team will be responsible for sourcing deals, evaluating risk/reward, deploying capital, conducting risk management, performing live on-chain oversight, and handling portfolio construction.

• The fund's primary objective is to provide liquidity to new on-chain protocols, solving their "cold start problem" in exchange for economic incentives for being an early-mover and providing long-term capital.

Personally, I like the deal as it allows Sharplink to capture a higher-risk, higher-reward strategy without increasing headcount. @joechalom described it as a "singles and doubles" instead of a home run, which likely means a yield range of 4-6%.

Lastly, the Q1 2026 10-Q explicitly states that the protocol incentives for providing and maintaining Total Value Locked (TVL) on the Linea network - received through its Strategic Partnership Agreement with ether.fi, EigenCloud, and the Linea Consortium - are paid entirely in the form of ETH and weETH.

ALT Estimated recurring cash cost

5

4

31

3,394

May 11

$SBET Q1 2026 earnings: Massive Paper Losses Mask Underlying Operating Evolution

Sharplink's Q1 2026 results highlight the extreme volatility of its strategy under current U. S. GAAP rules. While the company reported a staggering $685.6 million net loss driven by unrealized ETH market declines and LsETH impairment charges, operational reality is different. Staking revenue reached $11.5 million, up from zero a year ago, as the company holds over 870,000 ETH. However, sequential revenue is decelerating, slipping from Q4 2025's peak despite a larger ETH treasury, raising questions about yield compression. Management's move to launch a $125 million Galaxy Onchain Yield Fund signals a shift from passive staking to more aggressive DeFi strategies.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐏𝐞𝐫𝐦𝐚𝐧𝐞𝐧𝐭 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐁𝐚𝐬𝐞 𝐕𝐚𝐥𝐢𝐝𝐚𝐭𝐞𝐝 — The company successfully transitioned treasury management in-house and continues to accumulate ETH, reaching 872,984 ETH by early May. ETH concentration per share (4.02) has doubled since strategy inception, proving the accretive model.

• 𝐔𝐧𝐥𝐨𝐜𝐤𝐢𝐧𝐠 𝐄𝐧𝐡𝐚𝐧𝐜𝐞𝐝 𝐘𝐢𝐞𝐥𝐝𝐬 — The proposed $125 million Galaxy Sharplink Onchain Yield Fund proves the company is aggressively pursuing institutional-grade yield strategies beyond basic native staking (~3%), which should drive higher future returns.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

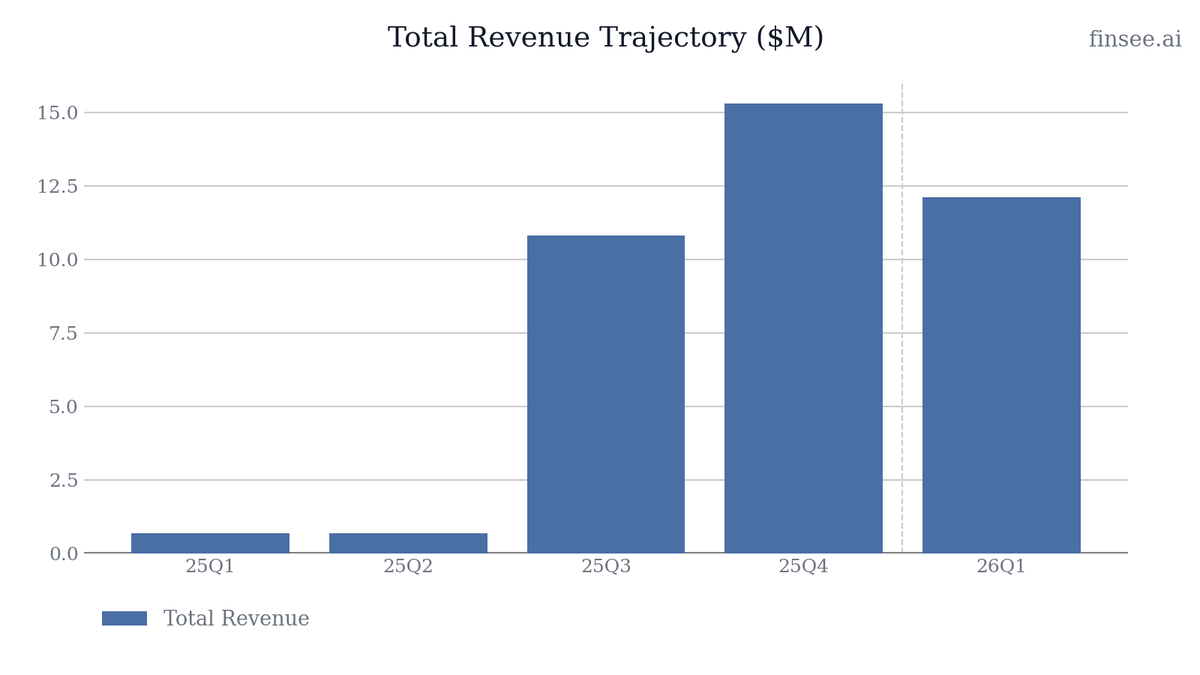

• 𝐘𝐢𝐞𝐥𝐝 𝐆𝐞𝐧𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐨𝐦𝐞𝐧𝐭𝐮𝐦 𝐢𝐬 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 — Despite adding ETH to the balance sheet during the quarter, total revenue dropped sequentially from $15.3 million in 25Q4 to $12.1 million in 26Q1, suggesting lower staking yields or deployment friction during the internalization process.

• 𝐒𝐆&𝐀 𝐁𝐥𝐨𝐚𝐭 — Bringing asset management in-house caused SG&A expenses to explode from $1.1 million a year ago to $9.9 million in 26Q1. The company must prove these fixed infrastructure costs can scale profitably.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The core thesis of accumulating ETH remains intact, and paper losses do not reflect cash destruction. However, the sequential deceleration in revenue combined with a massive spike in operating expenses puts the burden of proof on the new Galaxy Fund to deliver outsized returns.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐄𝐯𝐨𝐥𝐮𝐭𝐢𝐨𝐧 𝐁𝐞𝐲𝐨𝐧𝐝 𝐅𝐨𝐮𝐧𝐝𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐒𝐭𝐚𝐤𝐢𝐧𝐠 [NEW]

Sharplink is accelerating its yield strategy. On May 9, 2026, it signed an MOU for the Galaxy Sharplink Onchain Yield Fund, a $125 million initiative. This specific innovation aims to deploy capital into emerging protocols for stronger risk-adjusted returns, officially moving the company's treasury strategy from standard liquid/native staking into active decentralized finance (DeFi) deployment.

🔴 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐨𝐫𝐲 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞: 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐒𝐞𝐪𝐮𝐞𝐧𝐭𝐢𝐚𝐥𝐥𝐲 [NEW]

Management claims to be 'expanding ETH productivity,' yet the data tells a different story. Q1 2026 staking revenue came in at $11.5 million, a noticeable sequential drop from the $15.3 million reported in Q4 2025. This deceleration occurred even though the total ETH stack grew from 864k to 870k in the same period. This indicates either a drop in network staking yields or friction caused by shifting treasury operations internally.

⚪ 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐨𝐟 𝐀𝐬𝐬𝐞𝐭 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭

Sharplink has severed ties with external managers and transitioned the majority of its ETH treasury management in-house. While this spiked near-term costs, it gives the company direct control over structuring multi-year yield deals and avoids long-term margin sharing with third parties, serving as a long-term margin expansion driver.

🔴🔴 𝐆𝐀𝐀𝐏 𝐀𝐜𝐜𝐨𝐮𝐧𝐭𝐢𝐧𝐠 𝐂𝐫𝐞𝐚𝐭𝐞𝐬 𝐄𝐱𝐭𝐫𝐞𝐦𝐞 𝐇𝐞𝐚𝐝𝐥𝐢𝐧𝐞 𝐍𝐨𝐢𝐬𝐞

The massive $685.6 million net loss is a reversing trend purely driven by U. S. GAAP accounting. Under the historical cost less impairment model, Sharplink recorded a $191.7 million impairment charge on LsETH, combined with a $506.7 million mark-to-market unrealized loss on native ETH. While not an economic realization of loss, this severe opacity restricts traditional screeners and mainstream institutional onboarding.

🟢🟢 𝐌𝐚𝐜𝐫𝐨 𝐀𝐝𝐨𝐩𝐭𝐢𝐨𝐧 𝐨𝐟 𝐏𝐫𝐨𝐠𝐫𝐚𝐦𝐦𝐚𝐛𝐥𝐞 𝐅𝐢𝐧𝐚𝐧𝐜𝐢𝐚𝐥 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞

Management heavily leaned into the macro tailwinds of Ethereum maturing into the dominant settlement layer for the global digital economy. The continued acceleration of tokenized real-world assets, stablecoins, and Layer 2 network resilience provides the foundational bedrock for Sharplink's 'institutional super cycle' thesis.

🔴 𝐒𝐮𝐫𝐠𝐢𝐧𝐠 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬 [NEW]

Selling, General, and Administrative (SG&A) expenses accelerated massively, hitting $9.9 million for the quarter compared to $1.1 million in the prior year. Management attributes this to infrastructure, talent, and systems needed to actively manage the ETH platform in-house. With operating revenue at $12.1 million, the margin profile is currently thin on a cash basis.

⚪ 𝐀𝐜𝐜𝐫𝐞𝐭𝐢𝐯𝐞 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐀𝐥𝐥𝐨𝐜𝐚𝐭𝐢𝐨𝐧 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲

The company continues to successfully execute its primary objective: compounding ETH per share. The 'ETH Concentration' metric has grown from 2.0 at the strategy's launch in June 2025 to 4.02 by Q1 2026. This stable, upward trajectory acts as the primary driver of underlying shareholder value.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐀𝐟𝐟𝐢𝐥𝐢𝐚𝐭𝐞 𝐌𝐚𝐫𝐤𝐞𝐭𝐢𝐧𝐠 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $0.557 million

This legacy segment is decelerating, down 25% YoY from $0.742 million in Q1 2025. It now represents less than 5% of total revenue and is essentially a run-off asset as the company focuses entirely on its ETH treasury mandate.

𝐂𝐚𝐬𝐡 𝐚𝐧𝐝 𝐂𝐚𝐬𝐡 𝐄𝐪𝐮𝐢𝐯𝐚𝐥𝐞𝐧𝐭𝐬: $16.9 million

Cash balance is reversing, down from $28.5 million at the end of Q4 2025. This $11.6 million cash burn reflects the heavier SG&A load and potential final deployments of fiat into crypto assets.

𝐍𝐞𝐭 𝐑𝐞𝐚𝐥𝐢𝐳𝐞𝐝 𝐆𝐚𝐢𝐧: $12.0 million

Despite the massive paper losses, the company actively generated $12.0 million in net realized gains from ETH-to-LsETH conversions, redemptions, incentives, and rebates. This highlights the active trading and positioning happening beneath the surface.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐆𝐚𝐥𝐚𝐱𝐲 𝐒𝐡𝐚𝐫𝐩𝐥𝐢𝐧𝐤 𝐎𝐧𝐜𝐡𝐚𝐢𝐧 𝐘𝐢𝐞𝐥𝐝 𝐅𝐮𝐧𝐝 𝐂𝐨𝐦𝐦𝐢𝐭𝐦𝐞𝐧𝐭: $125 million

While Sharplink does not provide forward EPS or Revenue guidance, the announced Memorandum of Understanding with Galaxy Digital outlines a $125 million capital deployment into onchain opportunities. This signals a stable commitment to transitioning capital from base staking yields into higher-margin DeFi liquidity provisioning.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐘𝐢𝐞𝐥𝐝 𝐂𝐨𝐦𝐩𝐫𝐞𝐬𝐬𝐢𝐨𝐧

Q1 2026 staking revenue declined sequentially compared to Q4 2025 despite holding more ETH. Are you seeing structural yield compression across the Ethereum network, or was this a temporary gap caused by moving assets in-house?

𝐒𝐆&𝐀 𝐒𝐭𝐚𝐛𝐢𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧

With SG&A hitting nearly $10 million this quarter for talent and infrastructure, is this the new baseline run-rate, or were there one-time setup costs involved in internalization?

𝐆𝐚𝐥𝐚𝐱𝐲 𝐅𝐮𝐧𝐝 𝐓𝐢𝐦𝐞𝐥𝐢𝐧𝐞 𝐚𝐧𝐝 𝐄𝐜𝐨𝐧𝐨𝐦𝐢𝐜𝐬

Regarding the $125 million Galaxy Onchain Yield Fund, what is the expected timeline for finalization, and how do the unit economics and expected yields differ from your current LsETH mix?

𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧 𝐑𝐮𝐧𝐰𝐚𝐲

Cash dropped to $16.9 million this quarter. Are staking rewards being liquidated to cover the $9.9 million in quarterly SG&A, or do you plan to raise additional fiat capital to fund operations?

4

1,176

May 11

以太坊策略公司 Sharplink 公布 2026 年 Q1 财报,截至 2026 年 5 月 4 日,公司共持有 872,984 枚 ETH,总质押奖励累计达 18,800 枚 ETH。Sharplink Q1 营收增至 1210 万美元,上年同期为 70 万美元;净亏损为 6.856 亿美元,主要受 ETH 市场波动导致的 5.067 亿美元未实现亏损及 1.917 亿美元 lsETH 减值影响。公司强调,相关亏损主要源于美国 GAAP 会计处理,并不代表 ETH 持仓实际经济损失,也不会减少持币数量。wublock123.com/news/sharplin…

2

5

3,488

May 4

The AI revolution is here, and it's being redefined by AI agents and the underlying infrastructure that powerqs them! 🚀

Amidst the buzz, a groundbreaking project is emerging: lSETH AI Ecosystem. This isn't just another blockchain; it's an AI-Native Layer 1 Blockchain leveraging Intelligent Proof of Work (iPoW). Co-engineered with powerhouses like Google Gemini, EVM, and Solana VM, SETH is building the foundation for the next generation of AI.

What makes SETH stand out in the trending landscape of AI agents? It's all about decentralized compute and empowering an agentic economy. With its focus on Seth edge mining devices, SETH aims to put the power of AI directly into the hands of users, moving beyond centralized models. This aligns perfectly with the growing sentiment that AI agents are becoming the new workforce, and access to compute is paramount.

As we move towards a future where AI agents manage complex tasks and drive innovation, projects like SETH are crucial for ensuring a decentralized, accessible, and robust AI infrastructure. Keep an eye on SETH as it progresses towards its testnet and mainnet launch in Q2-Q3 2026!

#AI #Blockchain #AIAgents #DecentralizedAI #iPoW #SETH #TechTrends #FutureOfAI

3

6

306

LIQUID COLLECTIVE SEES 37% TVL SURGE

Liquid staking platform @liquid_col has seen its TVL jump by over 37% in the past month, rising to a figure of more than $800 million per DefiLlama data.

It saw an ATH TVL of some $1.55 billion back in August of 2025.

Liquid Collective is and enterprise-grade liquid staking protocol designed for institutions and individuals, offering a compliant way to stake assets like $ETH (via LsETH) and $SOL (via LsSOL).

2

2

13

3,502

📊 Rising Transaction Volume Signal: Top Coins by % Growth | May 01, 2026

Network activity accelerated across multiple ecosystems today.

𝗔𝗰𝘁𝗶𝘃𝗶𝘁𝘆 𝘀𝗽𝗶𝗸𝗲

TROLL | TROLL (SOL) 13.40%

𝗦𝘁𝗿𝗼𝗻𝗴 𝗮𝗰𝘁𝗶𝘃𝗶𝘁𝘆

NOBODY | Nobody Sausage 11.55%

MKR | Maker 11.17%

IXS | IXS 10.44%

𝗦𝘁𝗲𝗮𝗱𝘆 𝗮𝗰𝘁𝗶𝘃𝗶𝘁𝘆

PIN | PinLink 9.28%

RAY | Raydium 8.29%

LSETH | Liquid Staked ETH 8.17%

J | JAMBO 7.45%

RAIL | Railgun 7.42%

FUN | FUNToken 7.28%

RSETH | Kelp DAO Restaked ETH 6.51%

TET | Tectum 5.96%

Rising transaction volume often precedes volatility.

#OnChain

2

53

Apr 21

Tuesday Report for @Sharplink

Total $ETH Holdings: 872,033

Weekly ETH Generated: 470

ETH Concentration: 4.02

Implied ETH Price (at $7.71 $SBET): $1,918

Key Updates:

- $SBET is not affected by the rsETH exploitation; they hold native ETH, ETH as-if redeemed from LsETH, and ETH as-if redeemed from WeETH.

- Partnered with @VitalikButerin, @ethereumfndn, and @SNZHoldings to launch the Ethereum Community Hub in Hong Kong, the first in the region.

We are seeing the increasing importance of risk management in the DeFi space, especially with the increasing capabilities of attackers who have access to AI. Managing risk is @joechalom's specialty, and with @ethereumJoseph, $SBET is by far the most Ethereum-aligned DAT.

2

8

53

3,515

Last 15m - #Coinbase Spot (USD Trades)

📈 Top 3 Gainers:

$BNKR : ↑2.66%

$TURBO : ↑2.09%

$LSETH : ↑1.61%

📉 Top 3 Losers:

$TRIA : ↓-1.25%

$ESP : ↓-1.14%

$BARD : ↓-1.12%

📶 Top 3 by Volume:

$BTC : 4.10M

$XRP : 1.41M

$ETH : 1.13M

🔥 Top 3 by Vol. Change:

$FET : 168.32%

$LINK : 110.31%

$SOL : 77.03%

#Crypto

1

2

156

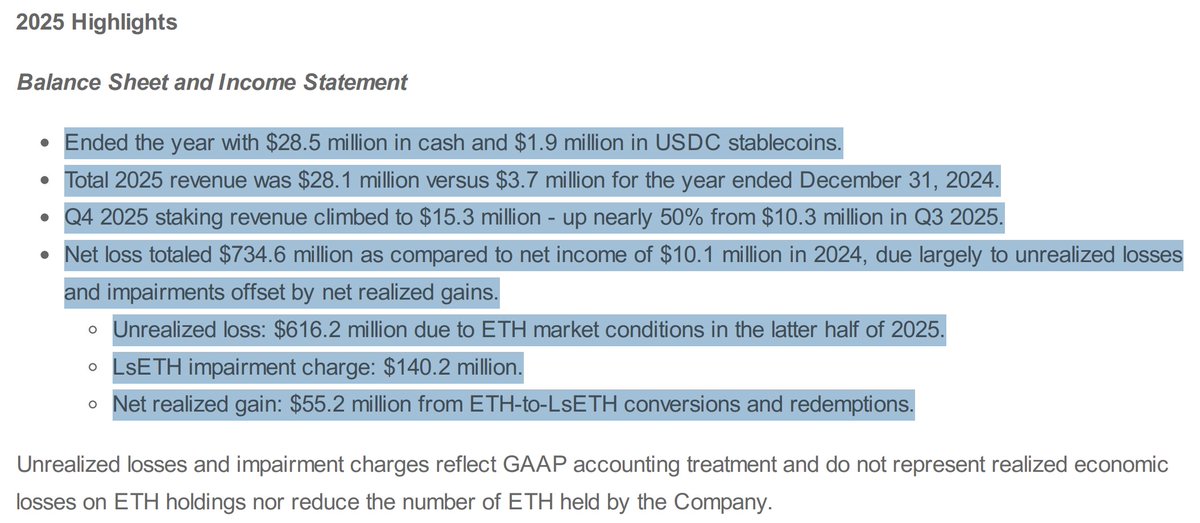

i was reading @Sharplink 's 2025 financials yesterday

$734.6M net loss does sound brutal until you break it down:

> $616.2M is unrealized ETH markdown

> $140.2M is an LsETH impairment charge

> the actual operating business 7.6x'd rev to $28.1M

> Q4 staking alone hit $15.3M

the real question for DATs now isn't the GAAP loss

it's whether staking yield justifies the equity dilution used to accumulate. that math is what actually matters.

and at ~$60M annualized staking run rate vs the scale of equity they're issuing, i'm not sure the math works out yet

3

103

Mar 10

📉 Sharplink encaisse 735 millions de dollars de pertes sur l’ETH

L’Ethereum Treasury Company a dévoilé un lourd bilan pour 2025, plombé par la chute de l’ETH et des dépréciations sur le LsETH.

Tous les détails dans notre article👇

cryptoast.fr/?p=205882

1

3

12

2,929

Mar 10

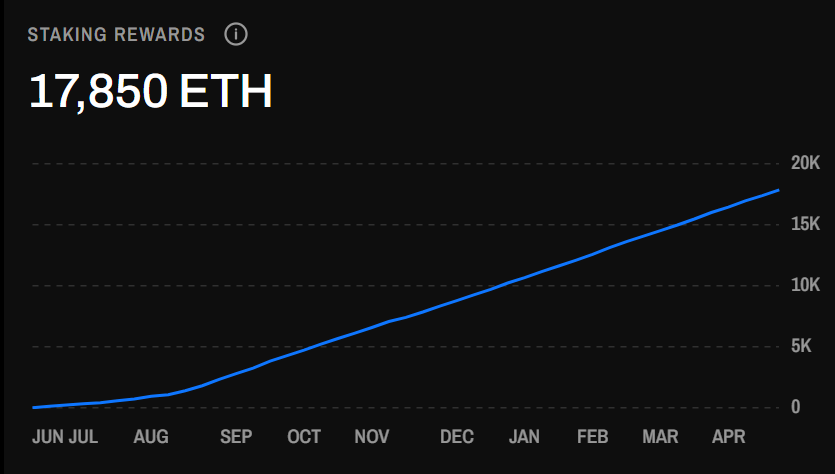

4️⃣ Sharplink 2025 Annual Report: Ethereum Holdings Grow to 868,699 ETH, Staking Rewards Reach 14,516 ETH

Ethereum treasury company Sharplink released its 2025 Annual Report, revealing that it now holds 868,699 ETH, including 604,618 ETH native, 208,893 ETH redeemed from LsETH, and 55,188 ETH redeemed from WeETH.

It has also earned 14,516 ETH in staking rewards, making it the second-largest public Ethereum holder globally.

The company also disclosed holding $28.5 million in cash and $1.9 million in USDC, with plans to continue increasing its ETH holdings and expand staking operations.

#Sharplink #ETH #StakingRewards #Crypto #Ethereum

2

56

📈DOWN BAD: SHARPLINK REPORTS $734.6M NET LOSS MOSTLY THANKS TO UNREALIZED $ETH LOSSES

Sharplink reported a $734.6 million net loss for 2025, primarily driven by $616.2 million in unrealized losses linked to ETH price declines during the second half of 2025, along with a $140.2 million impairment related to LsETH holdings.

Those were partially offset by $55.2 million in realized gains from ETH conversions and redemptions.

But faith in the ethereum ecosystem is still strong, and Sharplink feels Ethereum’s role as a decentralized trust and settlement layer is likely to attract continued institutional demand, bolstering their future success.

1

17

4,041

Mar 9

Here's your punchy $SBET earnings post with actual data:

🚨 $SBET Q4 & FY2025 EARNINGS — THE REAL NUMBERS DECODED 🔷💰⚡

SharpLink just reported and the headline loss is MISLEADING — here's the TRUTH! 🧠

📊 FY2025 SCORECARD:

Metric20252024Change💵 Revenue$28.1M$3.7M 660% 🚀💰 Q4 Staking Rev$15.3M— 50% QoQ 🔥🏦 Cash$28.5M—✅ Solid💲 USDC$1.9M—✅📉 Net Loss-$734.6M $10.1M⚠️ GAAP noise

🧠 THE MOST IMPORTANT THING TO UNDERSTAND:

That -$734.6M loss is NOT real cash leaving the building! 🚫💸

Breaking it down:

📉 -$616.2M = Unrealized ETH price decline = PAPER LOSS ONLY 📄

📉 -$140.2M = LsETH impairment charge = ACCOUNTING ENTRY 📒

✅ $55.2M = REAL realized gains from ETH conversions 💰

ETH holdings UNCHANGED — not one ETH was lost! 🔷💎

🔥 THE REAL BULL STORY:

🚀 Revenue 660% YoY — from $3.7M → $28.1M

⚡ Q4 staking revenue 50% QoQ = $15.3M in ONE quarter

📈 Annualized staking run rate = $61M if Q4 pace continues

💵 $30.4M in liquid assets (cash USDC) = runway solid

🔷 ETH staking machine = COMPOUNDING wealth regardless of price 💪

💡 THE MSTR COMPARISON:

$MSTR$SBETAssetBitcoinEthereumYield0% (no staking)Staking income ✅RevenueMinimal$28M growingQ4 IncomeNone$15.3M staking

$SBET actually GENERATES YIELD on its crypto treasury — $MSTR doesn't! 🎯💎

⚠️ FAIR RISKS:

🔴 ETH price recovery needed for unrealized losses to reverse

🔴 GAAP headlines will scare retail investors

🔴 $734M loss = negative press = short-term selling pressure

🔴 Crypto market correlation = volatility guaranteed

🎯 Key Levels:

📍 Current: $7.32

🚀 Bull target: $15 → $23 (analyst)

🛡️ Support: $7.00 → $6.55

💀 Stop: Below $6.00

Bottom Line: $734M GAAP loss is 84% ACCOUNTING ENTRIES. The real story is revenue 660%, staking income 50% QoQ, $30M cash, ETH holdings INTACT.

When Wall Street sees -$734M they PANIC. When you understand GAAP accounting you see a $28M revenue company with a $1.7B ETH treasury generating passive income. 🧠💎

Dip = opportunity for those who can read financial statements. 😤🔷

globenewswire.com/news-relea…

@SharpLink @unusual_whales @iFinance @Consensys #SBET #SharpLink #Ethereum #ETH #Staking #Earnings #CryptoTreasury #GAAPvsReality

Not financial advice. DYOR. 🙏

2

3

456