May 16

US Equity Rotation, Week Ending May 16, 2026

What happened

Mean ΔSATA across 2,580 names: -0.32 Tuesday, -0.47 Thursday, -0.78 Friday. Decliners crossed a majority on Friday at 54%. Risers fell to 16%. The selling broadened through the week rather than stabilizing after Tuesday's CPI print.

What it means

The regime is rate-driven, not just energy-driven. Tuesday's read was a consumer discretionary squeeze plus an energy producer rotation. By Friday the duration-asset repricing had taken over. Anything rate-sensitive sold off in coordinated fashion: banks, all REIT sub-types, financial services, consumer finance, utilities. The defensive utility bid that held the first half of the week gave way Friday. The hard-assets trade narrowed to energy producers and energy services only. Miners, chemicals, utilities all rotated back out.

The typical "rotate to defensives" reflex isn't working because rate sensitivity is overriding sector defensiveness. Utilities, REITs, and most income-style names sold with the market, not against it.

Beneficiaries

Oil & Gas Producers. Mean ΔSATA 0.72 across 123 names, 56% positive. Strengthened through the week. Midstream names doing the heavy lifting: $OKE, $WMB, $EPSN at Stage 2D.

Energy Equipment & Services. 0.44, 51% positive. $USAC, $MATR.TO, $TCW.TO each ΔSATA 3.

Health Care Providers (managed care specifically). Industry held flat at -0.03. The defensive bid that utilities lost rotated here. $CNC, $CVS, $UNH, $HUM, $AGL, $CLOV all positive. Fits a labor-softening / Medicaid-enrollment-grows scenario.

Ground Transportation, but only the freight side. Sharp split inside the industry. Truckers and rails working: $JBHT, $SNDR, $HTLD, $ODFL, $KNX, $UNP, $CSX, $NSC. Mobility platforms got hit: $UBER, $LYFT, $GRAB.

Communications Equipment, the narrow part of the AI infrastructure trade that still works. $AAOI, $LITE, $CSCO, $EXTR, $FFIV, $ANET, $VIAV, $HLIT all held.

Losers

Textiles, Apparel & Luxury Goods at -2.07 across 27 names, 81% negative. Now the weakest industry.

Air Freight & Logistics at -2.00, 89% negative.

Personal Care Products at -1.80, Household Products at -1.56. Staples broken.

Banks at -1.43, 85% of 131 names negative. From quiet weakness Tuesday to most uniformly broken large industry by Friday.

REIT complex with every sub-type negative. Mortgage REITs -1.68, Specialized REITs -1.64, plus Office, Retail, Industrial, Health Care, Diversified.

Industrials cracking late in the week. Building Products -1.53, Machinery -1.06, Aerospace & Defense -0.73.

Metals & Mining reversed from 0.58 Tuesday to -0.90 Friday. Only the energy producer side of the hard-assets trade held.

Price action confirms the rotation

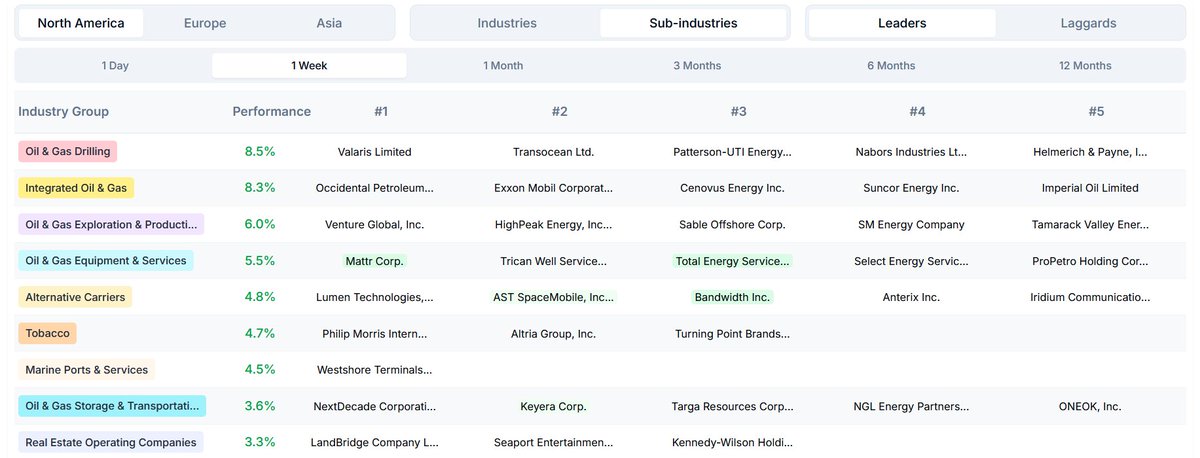

Five of the top eight performing US sub-industries this week were oil & gas value chain: Oil & Gas Drilling 8.5%, Integrated 8.3%, E&P 6.0%, Equipment & Services 5.5%, Storage & Transportation 3.6%.

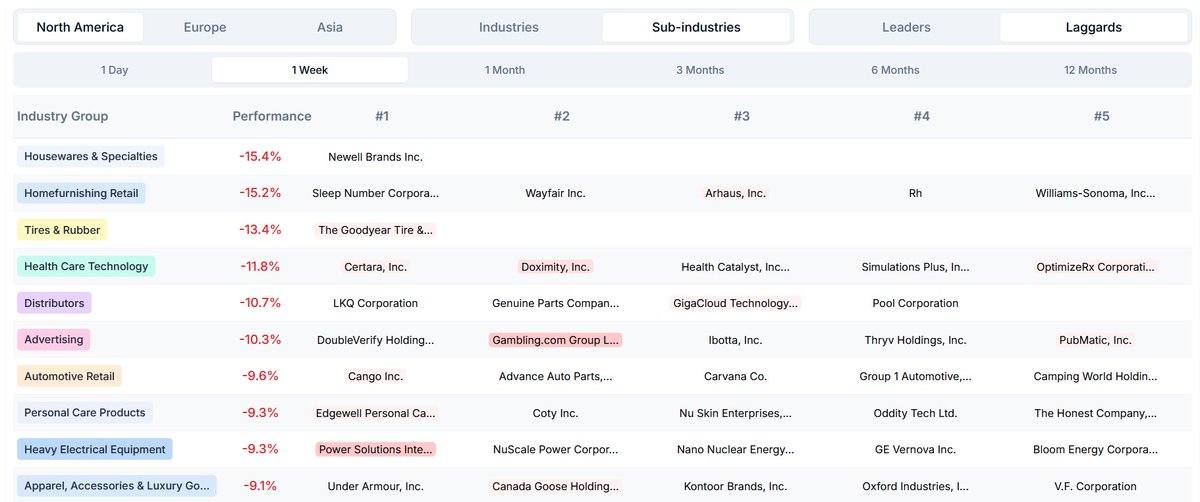

On the laggard side: Housewares -15.4%, Homefurnishing Retail -15.2%, Tires & Rubber -13.4%, Health Care Technology -11.8%. Nine sub-industries down 9% or more in a single week. Correction-grade magnitudes concentrated in consumer durables and discretionary.

One unexpected laggard worth flagging: Heavy Electrical Equipment -9.3%. The grid and generation side of the AI infrastructure trade broke this week, while the networking and optics side held. The trade narrowed further than the SATA data alone suggested.

Two unexpected leaders: Alternative Carriers 4.8% (specialty telecom infrastructure), Tobacco 4.7% (single-bucket defensive bid that the rest of staples didn't get).

How to position

Energy producer and services value chain is the only durable long exposure the data confirmed through five sessions. Screen Oil & Gas with EC Sentiment 20 , Stage 2, ATR ext under 2 for fresh entries. Midstream leading.

Reduce or avoid the rate-sensitive complex: banks, REITs, financial services, consumer finance. Same regime driver, broad breadth deterioration, no stabilization yet.

Consumer-facing names are a structural avoid, not a tactical trade. Five days of accelerating breadth deterioration.

Defensives didn't work this week. Utilities flipped negative Friday. Watch whether utility breadth stabilizes next week before adding.

Managed care is the only defensive that caught a bid. Position-sizing question if you want defensive exposure that isn't getting punished by rates.

With mean ΔSATA at -0.78 and 54% of the universe negative, this is breadth weakness consistent with a deeper correction. The question shifts from "where do I rotate" toward "do I have the right gross exposure at all."

Leaders and laggards tickers in replies below.

1

1

5

773

May 15

I am pretty sure there is alpha in looking at stocks where the analysts say "no positive catalysts for the next yr" when it's in relation to a cyclical that has been beaten to pieces $matr.to

1

2

10

2,826

May 14

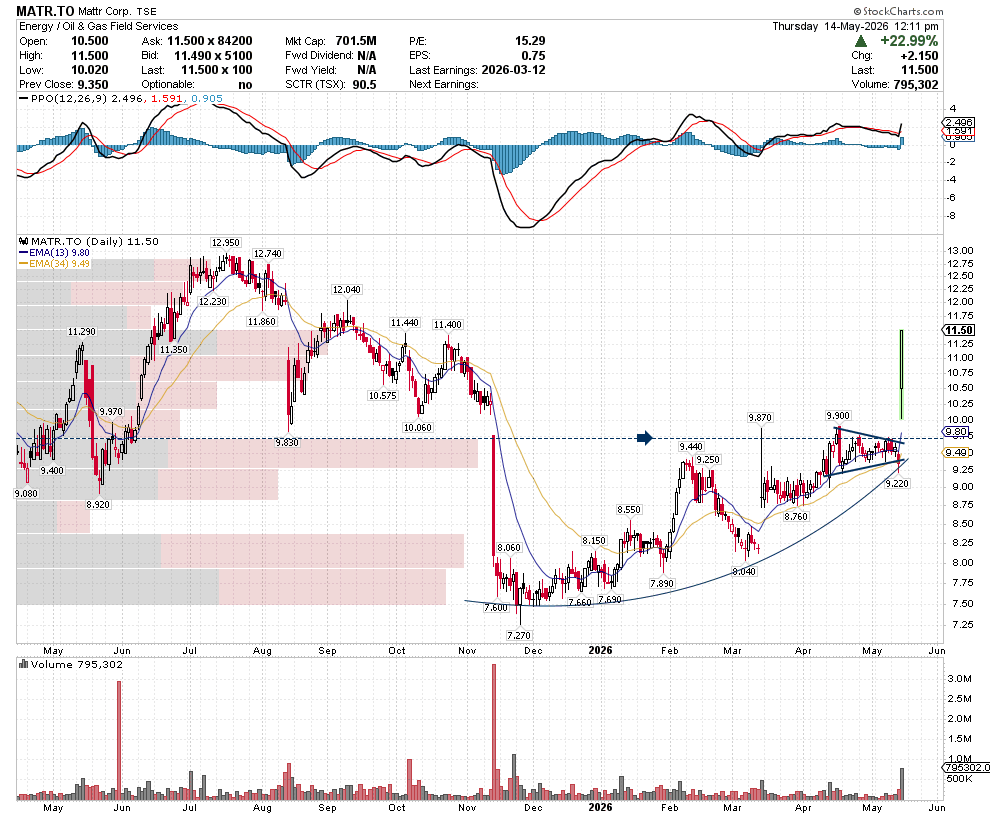

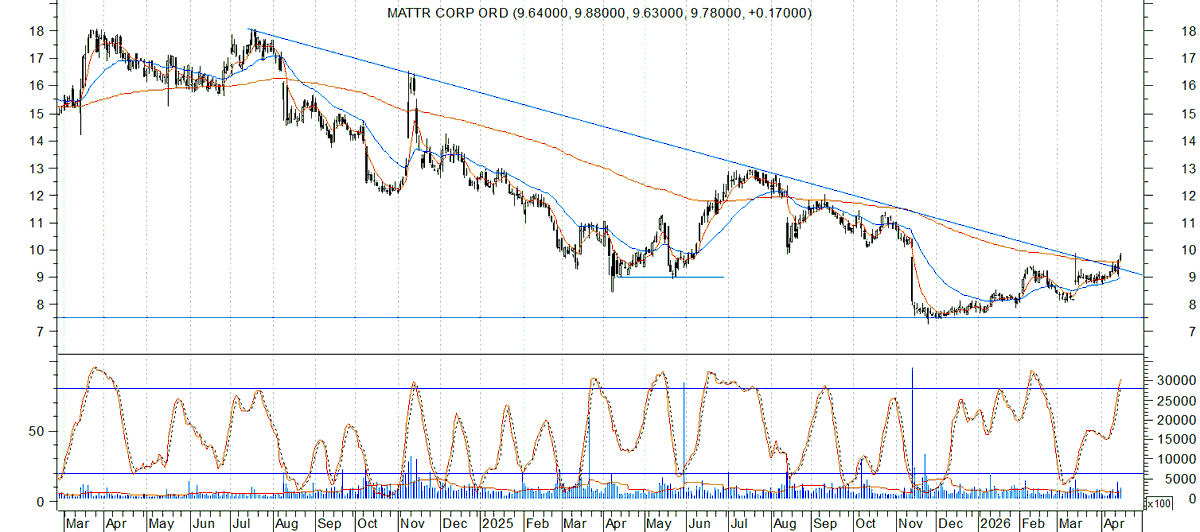

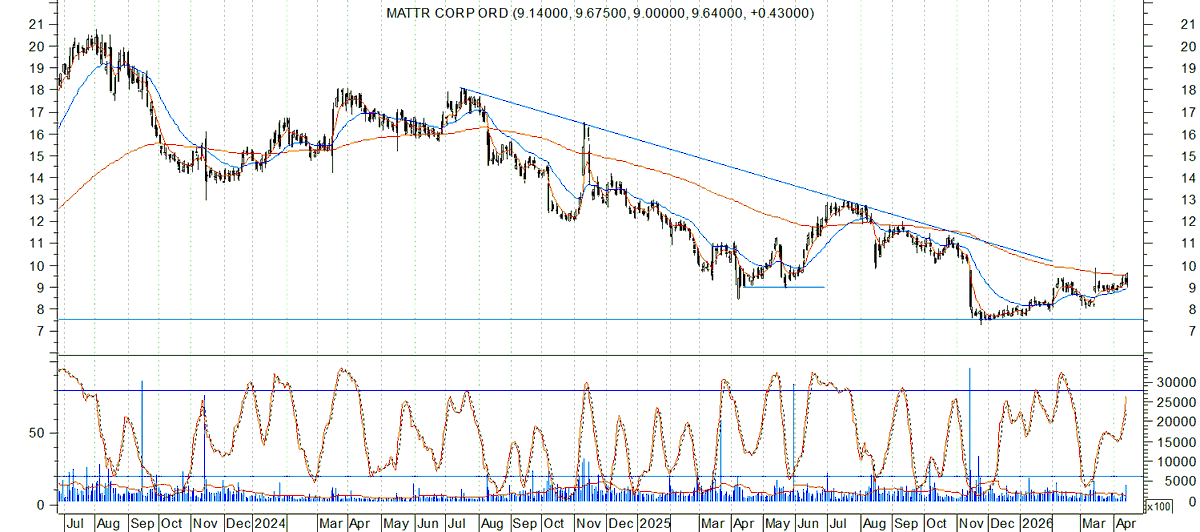

$MATR.TO just made sense. ✅

The technical setup was repeatedly highlighted in our daily setups report as price action coiled on the right side of a bottoming pattern. 📝

Today, price is breaking out, up over 22%. 🏁

2

9

605

May 14

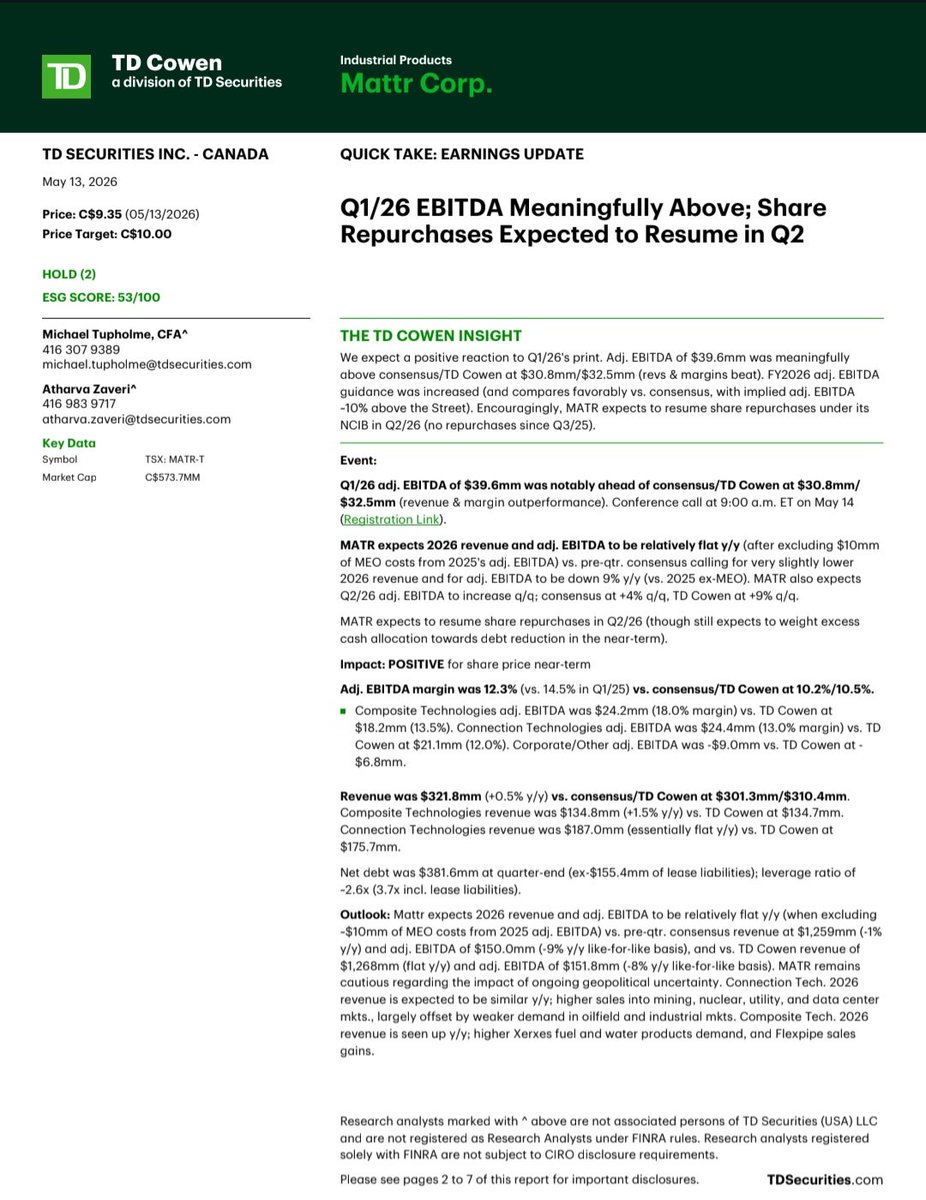

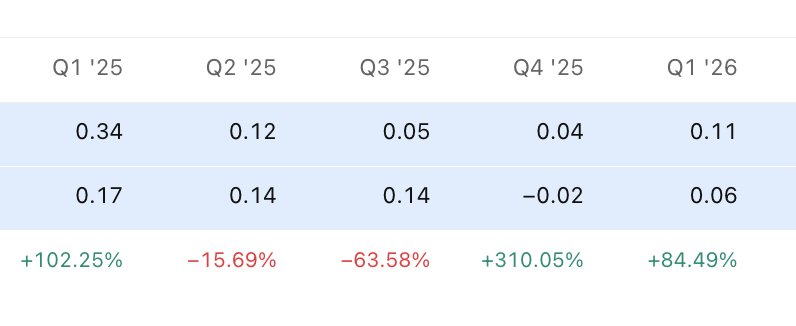

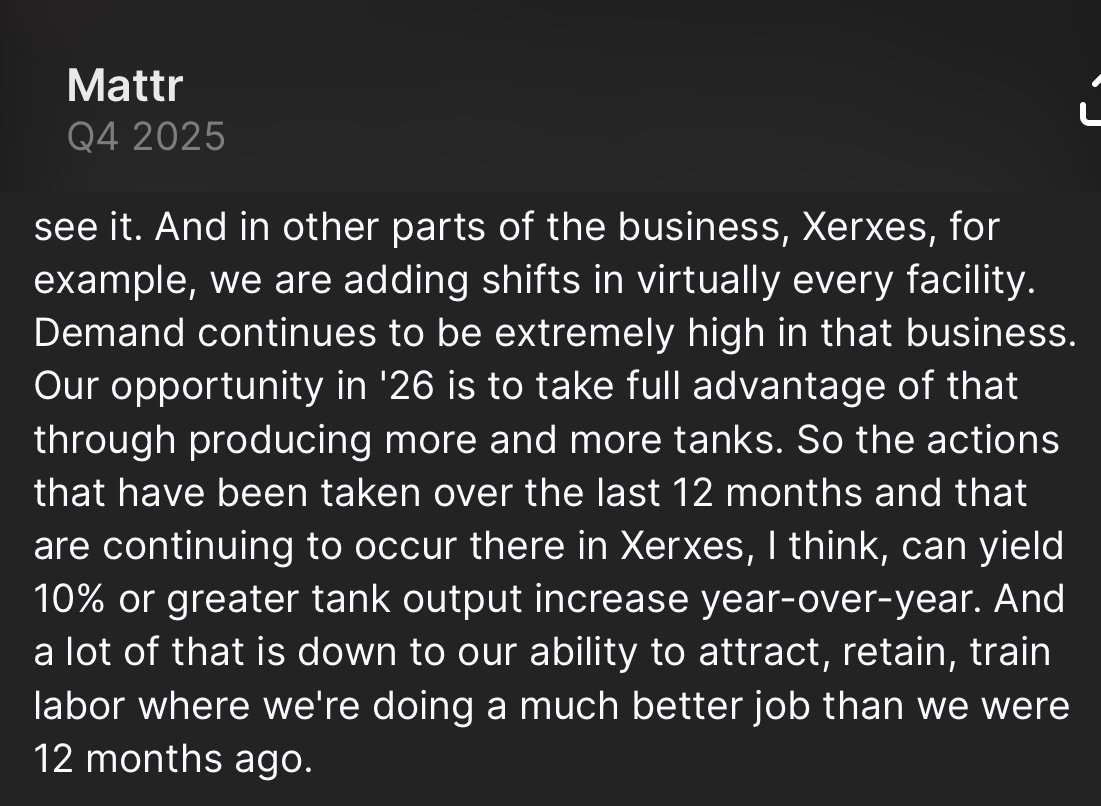

$MATR.TO — Mattr Corp. | Q1 2026 Results

Materials technology company serving infrastructure markets through Composite Technologies (Xerxes, Flexpipe) and Connection Technologies (wire & cable, heat-shrink tubing).

📊 Q1 2026 Highlights:

• Revenue: $321.8M ( 0.5% YoY) — Composite 1.5%, Connection -0.2%

• Operating Income (continuing): $22.6M ( 22.3% YoY)

• Adjusted EBITDA (continuing): $39.6M (-14.9% YoY)

• Net Income: $7.4M vs. $52.7M prior year (prior included $4.7M discontinued large deferred tax recovery)

• Diluted EPS: $0.12 vs. $0.84

• Adjusted EPS: $0.11 vs. $0.34

🏗️ Segment Performance:

• Composite Technologies: Revenue $134.8M ( 1.5%), Adj EBITDA $24.2M ( 15.3%, 18% margin) — Xerxes fuel/water Flexpipe strength

• Connection Technologies: Revenue $187.0M (-0.2%), Adj EBITDA $24.4M (-20.0%, 13% margin) — mix headwinds Ohio heat-shrink ramp drag

💰 Capital & Balance Sheet:

• OCF (continuing): -$24.9M (seasonal WC build)

• Total debt: ~$576M; net seasonal $10M revolver draw

• Subsequent: US$300M revolver extended to Oct 2030

• No NCIB repurchases in Q1; resumption expected Q2

🔮 Outlook (raised):

• Full year 2026 revenue & Adj EBITDA outlook moved higher

• 2026 capex: $35-$45M

• Q2 Adj EBITDA expected higher than Q1

• Large international Flexpipe order secured subsequent to quarter

A tale of two segments, with composite doing the heavy lifting while connection works through commissioning costs at the ohio site. the headline net income drop is optical — prior year was inflated by a one-off tax recovery. underlying continuing operations grew operating income 22%, and management raised full-year guidance on the back of a big flexpipe order and easing tariff concerns on canadian-made product. tariff-insulated infrastructure exposure with improving margins is a setup worth watching.

Full analysis:

investorlens.io/stocks/MATR.…

#TSX #CanadianStocks #Infrastructure #Industrials #Composites #Manufacturing

1

3

365

May 14

Beating all expectations $MATR.TO is ready to move up. tradingview.com/news/urn:sum… #MATTR #TSX #Canada

2

230

May 14

2

147

May 13

yeah was actually a beat, though on the surface the YoY comp looks bad since last Q1 $MATR.TO got a one-time income tax recovery of $38.9 million

anyhow maybe they are finally at the inflection point...?

1

323

May 6

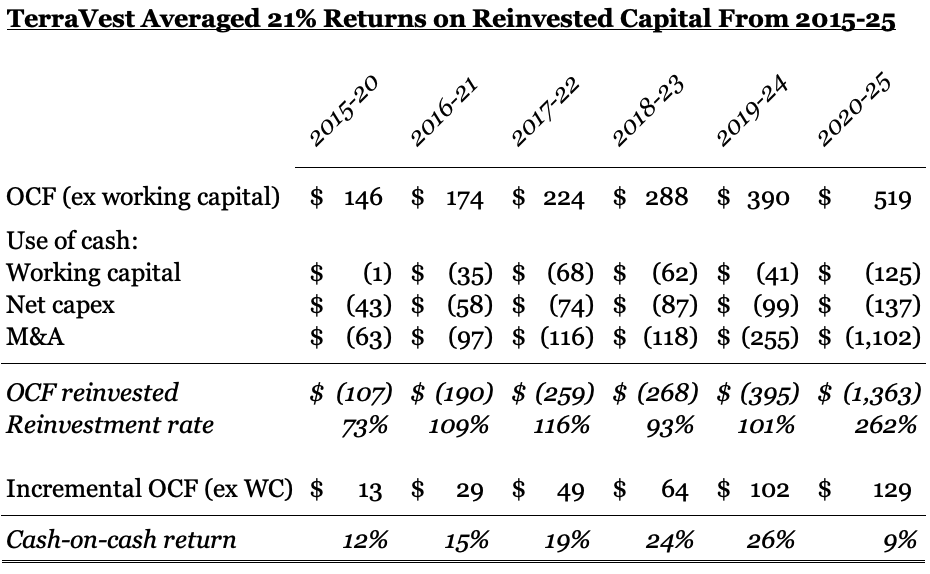

I believe TerraVest can still earn ROIICs of 15% as it expands. Here's how:

Phase one of the company's history involved buying mom & pop tank and trailer companies at 10-11x FCF, and reducing procurement (steel) costs and implementing a profit focused mindset to cut the multiple to 5-6x FCF.

That generated ROIICs of 20% for a decade.

The Entrans deal, which resulted in the company’s reinvestment rate soaring to 262% across 2020-25, marked the beginning of phase two.

This will increasingly involve buying larger companies more adjacent to these industries where the multiples paid are higher and synergies less substantial.

But TerraVest is also expanding into industries with higher organic growth, like datacenters and water storage.

ROIIC tends to reduce at this point, and was just 9% from 2020-25 by my calculation (below), weighted down by the Entrans acquisition (US$546mm at 7x EBITDA at the time, probably 12x EBITDA now).

Entrans is in a cyclical slowdown so I don’t think 9% ROIIC will be normal going forwards, but expect something close to 15%.

If we assume acquisitions going forward average 6x EBITDA (Entrans was 7x but KBK was 5.6x) that implies about 11x FCF using the company’s cash conversion from the last two years.

Assuming lower synergies than in the past but a higher growth rate, I could see an ROIIC algorithm of 9% FCF yield 2% synergies 5% organic growth = 16% ROIIC.

For more details, take a look at my article on TerraVest's next chapter (link in the next comment), which looks at the company's:

1. M&A runway

2. Clue on new markets from Q1

3. Competition with Mattr $MATR.TO

4. Conditions in Q2

5. A scenario for a 21% IRR from here

$TVK.TO

3

3

32

4,095

Apr 14

$MATR.TO is approaching a critical level, and a breakout could create major upside for investors. Recent early-2026 reports suggest Mattr Corp. may also benefit from the industrial and economic agenda being pushed by Prime Minister Mark Carney. #TSX #MATR #MATTR #StockMarket

1

416

Mar 28

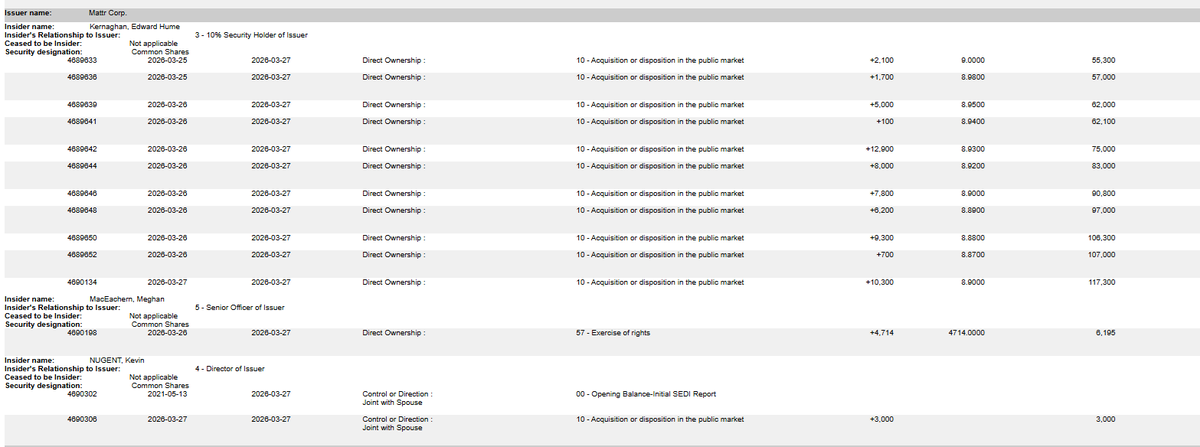

$MATR.TO up ~14% YTD. Insiders continue to load.

Was a tariff hit name last year.

2 Dec 2025

$MATR.TO an OFS name I'm not very familiar with. Seen alot of people lose and make alot of money on it since the Shawcor era. Big guns adding now and insiders have been buying the latest dip. On my to-do list of names to look into over the weekend.

finance.yahoo.com/news/kernw…

1

13

3,417

Mar 13

Pure vibes has been an excellent way to play $matr.to

Not a wildly painful q4 all things considered and likely bottoming. Can also use fintwit sentiment on cyclicals as a contra

Still limited chatter on this name so still upside from here

3 Dec 2025

Took a small position in $matr.to - capital allocation has been disastrous the past couple yrs b/w horribly timed buybacks and expanding facilities at the top of the cycle across its biz

However, analyst ests are now feeling close to reality with risk to the upside imo

1

8

1,331

Mar 13

$MATR.TO — Mattr Corp. | Q4 & Full Year 2025 Results

Mattr corp. makes materials technology for critical infrastructure — wire & cable, composite pipe, and FRP tanks. added amercable in jan 2025, nearly doubling the company's size.

📊 Full Year 2025 Highlights:

• Revenue: $1.27B ( 43.3% YoY) — amercable acquisition driving the jump

• Gross Profit: $317.9M (25.1% margin, up from 27.6%)

• Operating Income: $59.6M ( 48.5% YoY)

• Net Income (cont. ops): $48.3M vs. $(6.0)M last year

• OCF (cont. ops): $91.0M vs. $60.2M — strong cash conversion

• FCF (cont. ops): $27.7M

• EPS (diluted): $0.75 vs. $(0.06)

⚡ Q4 2025:

• Revenue: $312.5M ( 50.4% YoY)

• Operating Income: $13.4M ( 242.7% YoY)

• Net Income (cont. ops): $0.8M — profitable quarter despite macro headwinds

• D&A: $17.1M | Q4 EPS: $(0.03) (drag from discontinued ops loss)

💰 Capital Allocation:

• Repurchased 2.1M shares for $23.3M under NCIB in 2025

• Repaid $43.5M on credit facility in Q4 alone

• Net debt: $495M | Net debt/EBITDA: 3.1x (above 2.0x target — debt reduction priority)

🔮 2026 Outlook:

• Revenue and Adjusted EBITDA expected similar to or slightly below 2025

• Connection Technologies revenue expected lower (canadian industrial/mining softness)

• Composite Technologies revenue expected higher (xerxes capacity flexpipe market share)

• Capex guidance: $35–45M (below normal range)

• Q1 2026 Adjusted EBITDA expected similar to Q4 2025

The amercable deal transformed mattr's scale but also loaded up the balance sheet. the story now is debt reduction operational maturation at newly commissioned facilities — both progressing. margin compression from the acquisition's ramp costs should ease, but tariff uncertainty and canadian industrial softness add near-term pressure. watch FCF generation and leverage ratio improvement through 2026.

Full analysis:

investorlens.io/stocks/MATR.…

#TSX #CanadianStocks #Manufacturing #Infrastructure #Electrification

4

571