Apr 2

TOP ANNOUNCEMENTS FOR THE DAY

#GRINFRA: The company has executed a ₹1,897 Cr EPC contract for a new railway line project in Madhya Pradesh.

#ENVIROINFRA: The company secures five major projects worth ₹1,481 Cr expanding in the renewable and BESS segments.

#SAVYINFRA: The company has received a ₹408 Cr work order from Aakshya Infra Projects Pvt. Ltd and JSW Utkal Steel Limited.

#ASTRAMICRO: The company in JV has secured ₹250.58 Cr HAL order for the supply of Software Defined Radio.

#HBLENG: The company has received ₹179.79 Cr LOA for onboard KAVACH systems from Banaras Locomotive Works.

#BONDADA: The company secures ₹42.5 Cr orders from Telangana Police Housing Corp and Fixity Technologies.

#SATTRIX: The company receives an LOI of ₹9.3 Cr LOI from a leading PSU bank for managed security services.

#SUNTECHINFRA: The company secures ₹6.86 Cr piling work order from Linde Engineering India.

#GGBL: The company has receives ₹6.15 Cr NTPC Vidyut Vyapar order for 1.5 MW rooftop solar project at Goa Shipyard.

#MATRIXGEO: The company secures ₹5.14 Cr LOA from MP State Electronics Development Corporation.

#TEXMACO: The company receives ₹93 lakh developmental order from West Central Railway for bogie frames

2

65

5,075

18 Dec 2025

Value Discovery Summit 2025 - Beyond the Numbers Compilation

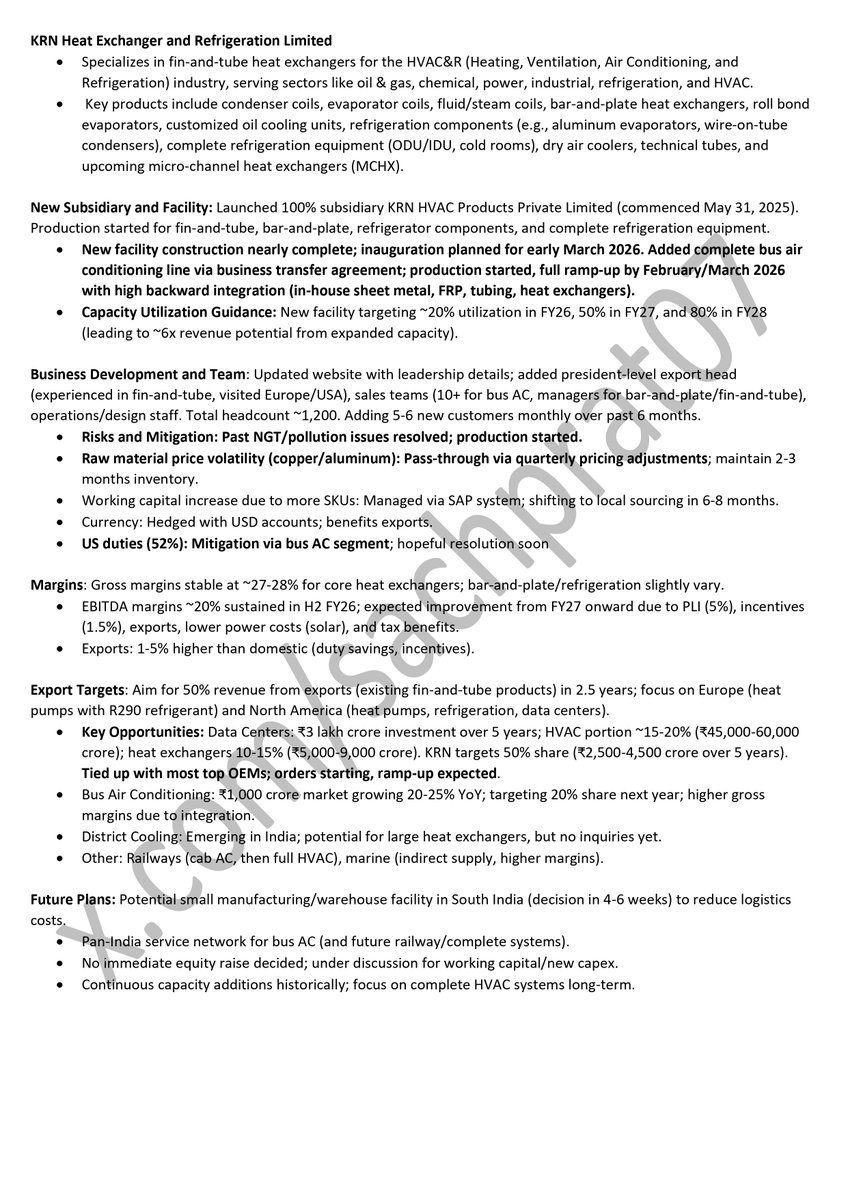

▫️ KRN Heat Exchanger

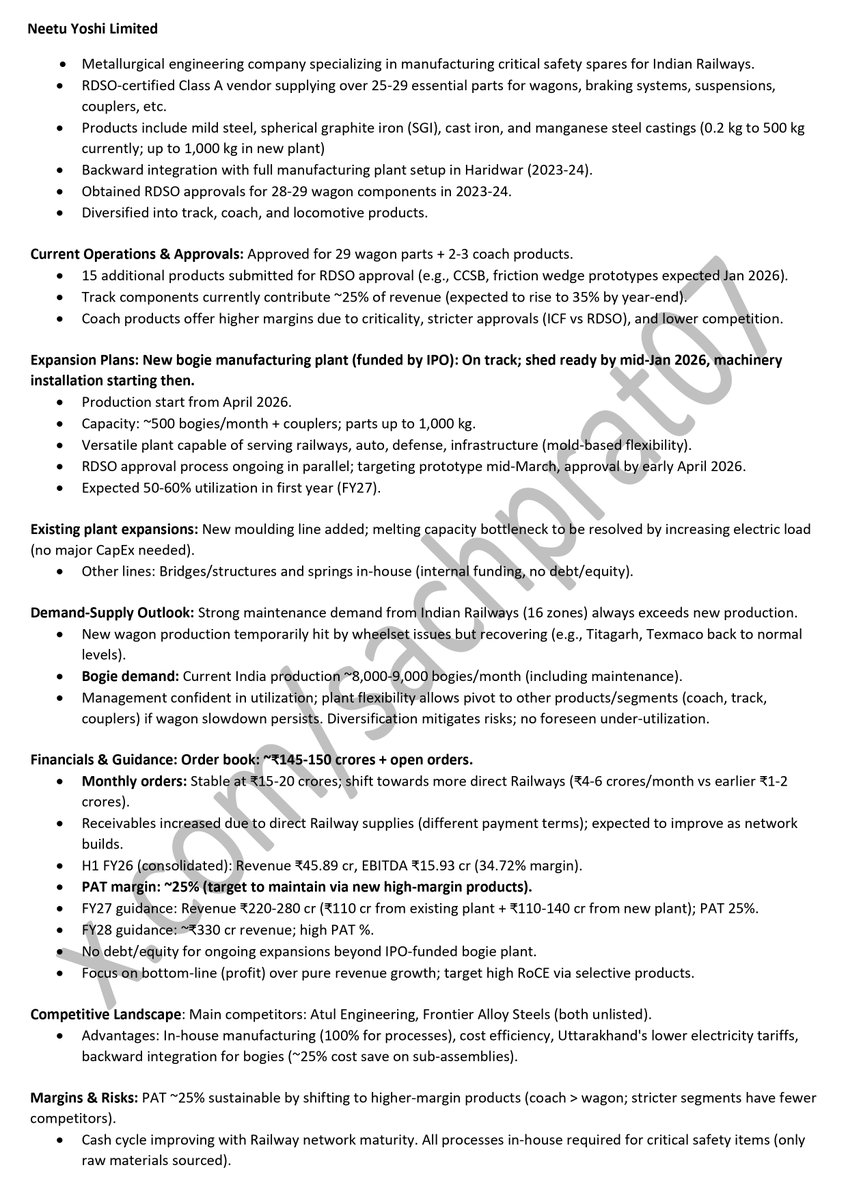

▫️ Neetu Yoshi

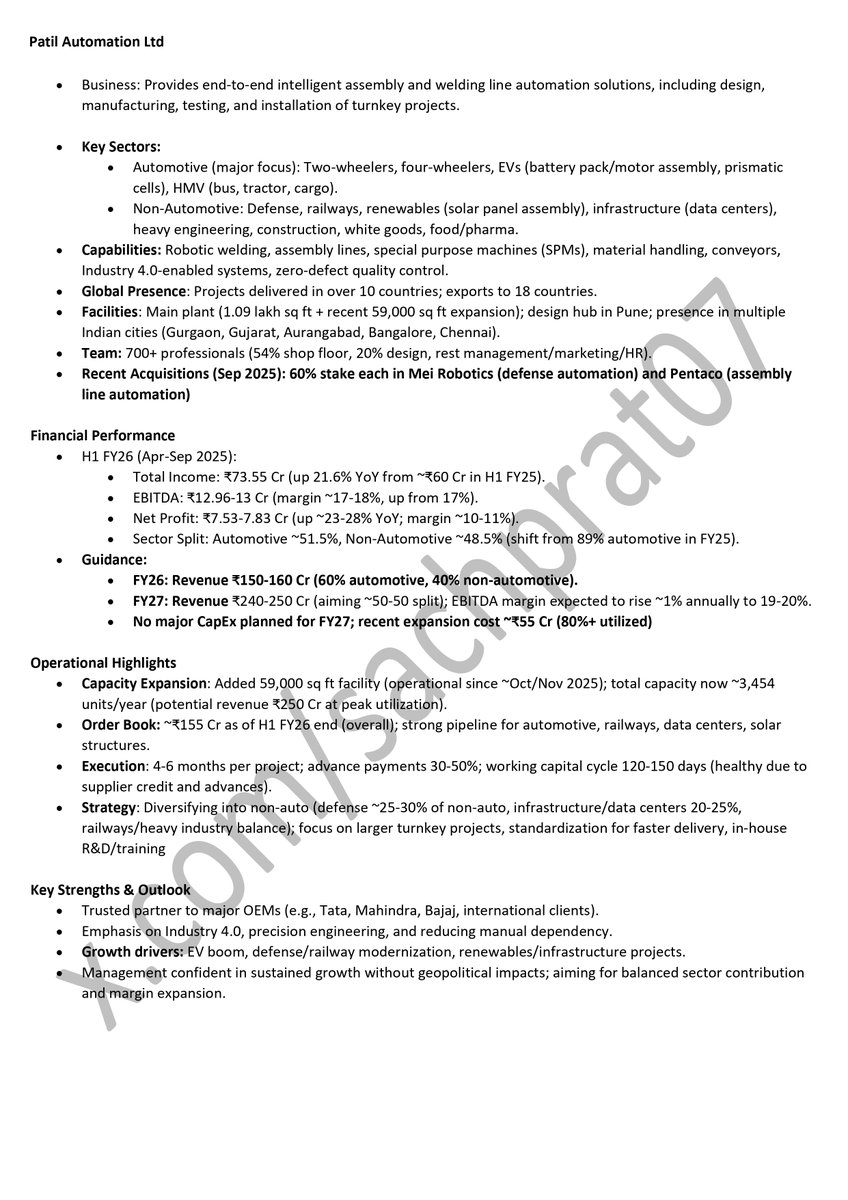

▫️ Patil Automation

▫️ Matrix Geo Solutions

▫️ Chandan Healthcare

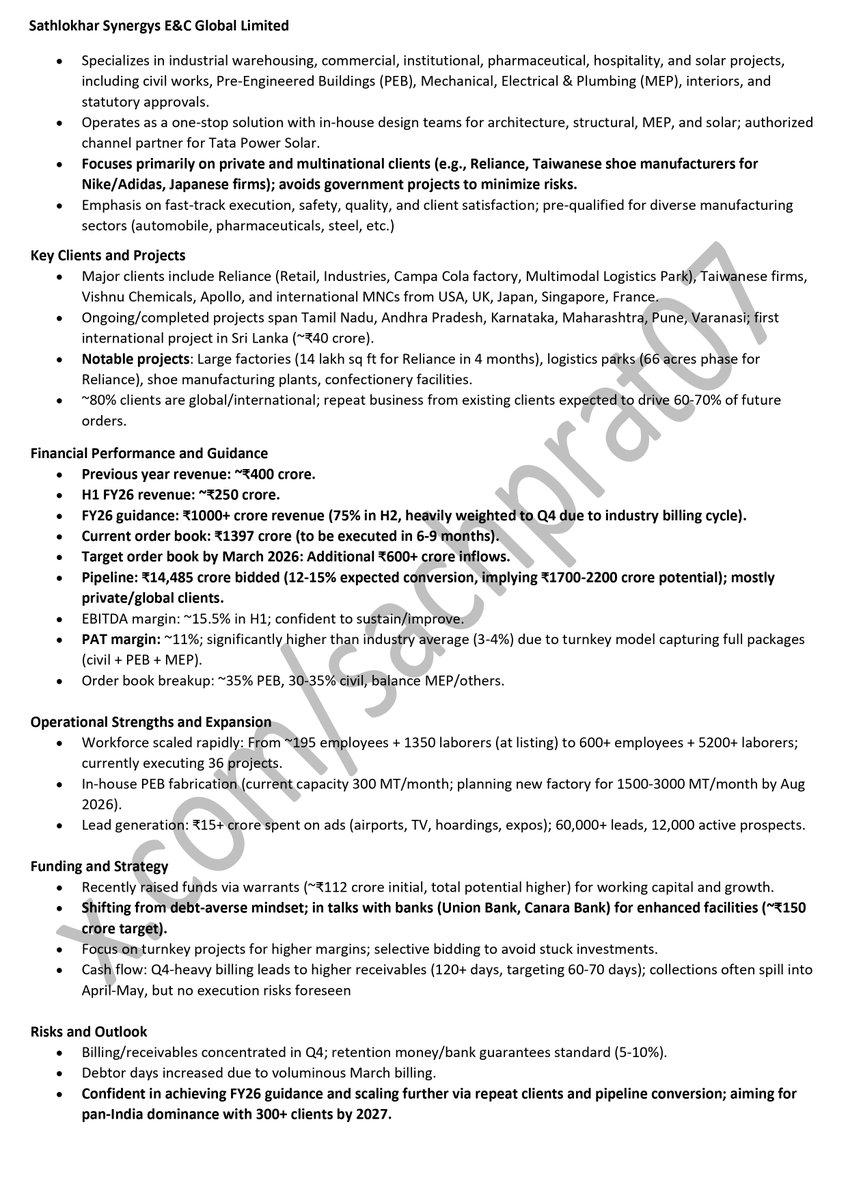

▫️ Sathlokhar Synergys E&C Global

▫️ Z-Tech (India)

▫️ Airfloa Rail Technology

▫️ AVP Infracon

▫️ Unihealth Hospitals

▫️ Cash Ur Drive

▫️ NIS Management

▫️ Oval Projects Engineering

▫️ HVAX Technolgies

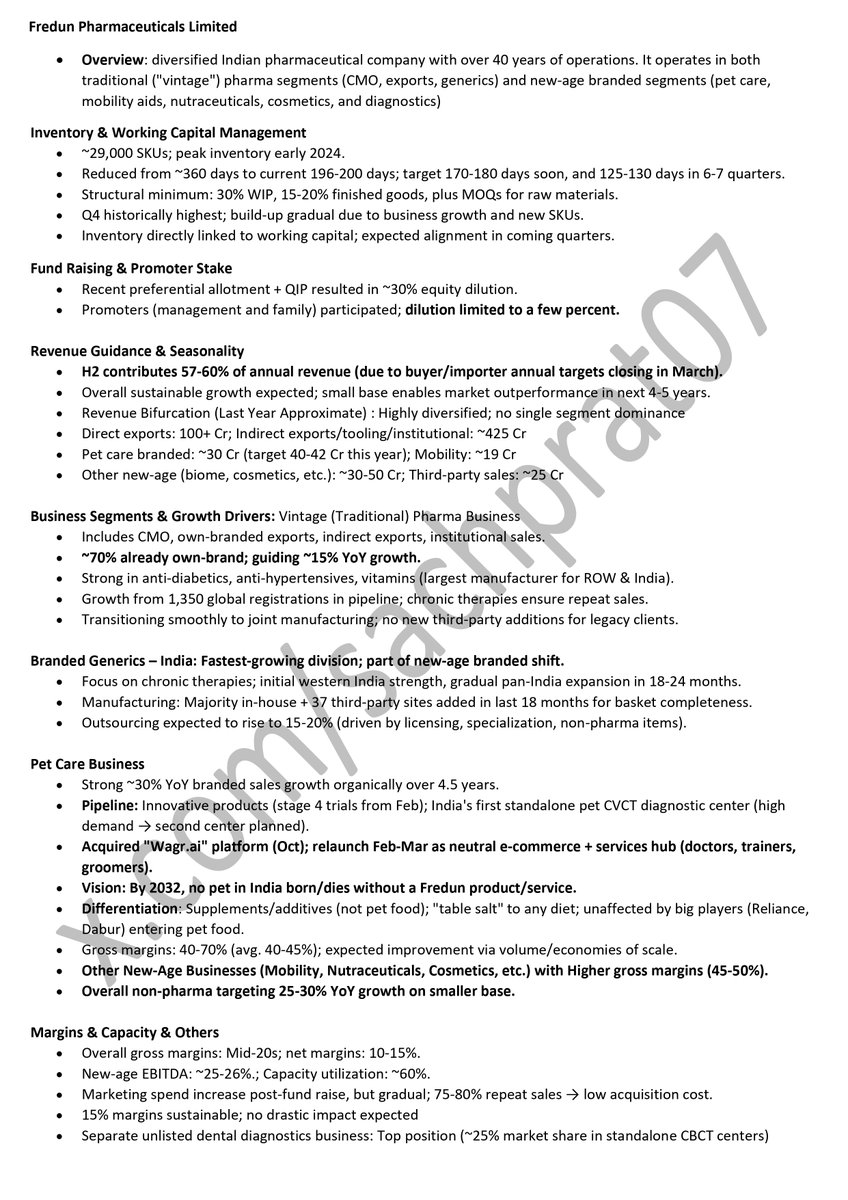

▫️ Fredun Pharmaceuticals

▫️ Praveg

▫️ Swastika Castal

▫️ Braceport Logistics

👉Day 1:

x.com/sachprat07/status/2000…

👉Day 2:

x.com/sachprat07/status/2001…

#KRN #NeetuYoshi #PatilAutoM #MGSL #MatrixGeo #Oval #HVAX #NISMGMT #Airfloa #AVP #AVPInfracon #Unihealth #UnihealthHospital #CUDML #CashUrDrive

#Chandan #ChandanHealthcare #Sathlokar #ssegl #ztech #ztechindia #braceport #swastika #praveg #fredun

#BeyondTheNumbers #ValueEducator #ValueDiscoverySummit

16 Dec 2025

Value Discovery Summit 2025 - Beyond the Numbers

👉Day 2:

▫️ Chandan Healthcare

▫️ Sathlokhar Synergys E&C Global

▫️ Z-Tech (India)

▫️ Fredun Pharmaceuticals

▫️ Praveg

▫️ Swastika Castal

▫️ Braceport Logistics

#Chandan #ChandanHealthcare #Sathlokar #ssegl #ztech #ztechindia #braceport #swastika #praveg #fredun

#BeyondTheNumbers #ValueEducator #ValueDiscoverySummit

4

38

153

29,246

17 Nov 2025

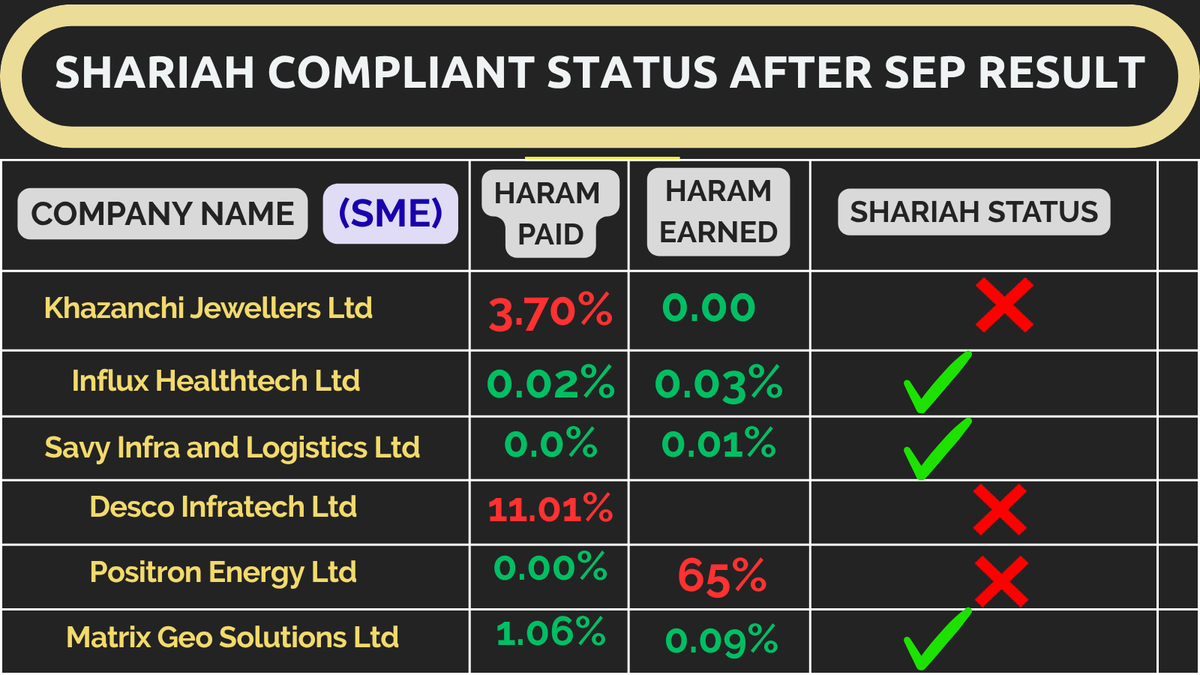

anyone who cares about purity of these earning and want to learn to check shariah status independently then

JOIN US👇👇

#khazanchijewellers #influx #savy #desco #positron

#matrixgeo

24 Oct 2025

🌙 SHARIAH COMPLIANT MENTORSHIP PROGRAM

“Your rizq is already written — but your effort defines how pure it is.”

✨ Learn to invest the halal way through Shariah-compliant stocks.

#HalalInvesting #ShariahCompliant #StockMarketEducation

3

285

10 Nov 2025

Good #Q2FY26-10/11/25 post 8pm

KEC International

#KEC

#KECInt

#KECInternational

Blockbuster Q2FY26 🔥

Record set with good margin expansion as guided by management

H2 should be even better on execution

Big orderbook provides good visibility

Rev at 6092cr vs 5113cr, Q1 at 5023cr

Solid QoQ and YoY uptick across all parameters

PBT at 213cr vs 113cr, Q1 at 158cr

PAT at 161cr vs 85cr, Q1 at 125cr

OCF at -917cr vs -489cr

Recievables under control almost at March levels

Orderbook at 44000cr

Pipeline of 1.8 lakh cr

T&D business ⏫44%

Kanpur Plastipack

#KanpurPlasti

Rev at 162cr vs 151cr, Q1 at 179cr

Solid margin expansion QoQ and YoY

PBT at 10.5cr vs 2.5cr, Q1 at 9.7cr

PAT at 8cr vs 1.6cr, Q1 at 7cr

OCF at 15cr vs 37cr in March

Matrix Geo Solutions

#MGSL

#MatrixGeo

H1FY26:

Rev at 14cr vs 9cr

PBT at 5.3ce vs 4cr

PAT at 4cr vs 3cr

Lords Chloro Alkali

#LordsChloro

Rev at 98cr vs 61cr, Q1 at 100cr

PBT at 14cr vs 0.5cr flat QoQ

PAT at 9cr vs 0.3cr, Q1 at 10cr

OCF at 27cr vs 9cr

Thejo Engineering

#Thejo

Rev at 153cr vs 133cr, Q1 at 133cr

PBT at 20cr vs 14.6cr, Q1 at 13.3cr

PAT at 14cr vs 12cr, Q1 at 10cr

OCF at 28cr vs 25cr

HiTech Corporation

#HiTechCorp

Rev at 164cr vs 146cr, Q1 at 165cr

PBT at 5.6cr vs 3.9cr, Q1 at 6.5cr

OCF at 26cr vs 29cr

Aarti Surfactants

#AartiSurf

Rev at 179cr vs 150cr, Q1 at 215cr

PBT at 2cr vs loss, Q1 at 4cr

OCF at 22cr vs -8cr

Orient Ceratech

#OrientCeratech

Good Q2FY26 with solid QoQ and YoY uptick

Big margin expansion

Rev at 114cr vs 70cr, Q1 at 98cr

PBT at 9.8cr vs 2.5cr, Q1 at 5.5cr

PAT at 7.5cr vs 1.8cr, Q1 at 4.3cr

OCF at 29cr vs 13cr

Reliance Power

#RelPower

Rev at 1974cr vs 1759cr, Q1 at 1885cr

Other income at 93cr vs 203cr, Q1 at 139cr

OCF at 1365cr

PBT at 108cr vs loss, Q1 at 72cr

Vigor Plast India

#Vigor

Rev at 17cr vs 11cr, Q1 at 11cr

PBT at 3.2cr vs .13cr, Q1 at 2.2cr

PAT at 2.4cr vs 1cr, Q1 at 1.6cr

Abate AS Industries

#AbateAS

Rev at 42cr vs nil, Q1 at 41cr

PBT at 4.1cr vs nil , Q1 at 2.3cr

OCF at 6cr

Easb India

#Esab

Rev at 381cr vs 338cr, Q1 at 352cr

PBT at 70cr vs 59cr, Q1 at 58cr

OCF at 49cr vs 88cr

Patil Automation

#PatilAuto

Decent H1FY26

Rev at 71cr vs 58cr, H2 at 59cr

PBT at 10.4cr vs 8.2cr, H2 at 6.9cr

PAT at 7.5cr vs 6.1cr, H2 at 5.5cr

OCF at 3.6cr vs 0.6cr

ONGC

#ONGC

Topline down, margin expansion QoQ and YoY

PBT at 16944cr vs 12691cr, Q1 at 15755cr

PAT at 12614cr vs 9852cr,Q1 at 11554cr

OCF at 60786cr vs 47675cr

SMS LifeSciences

#SMSLife

Muted revenue growth,solid margin expansion QoQ and YoY

Rev at 81cr vs 78cr, Q1 at 83cr

EBITDA at 14cr vs 8.5cr, Q1 at 12cr

PAT at 6.4cr vs 3.3cr, Q1 at 4.4cr

Decent:

#KalyaniCastTech

#RoyalArc

#EmeraldTyres

#GoyalSalt

#PowerMech

#NRBBearings

#DynamaticTech

#GRInfra

#CelloWorld

2

9

220

29,545

29 Sep 2025

🚨 10 IPOs listing tomorrow 🚨

Which ones to flip for listing gains & which to hold for the long run?

Here’s my breakdown 👇

🚀 Likely to List at a Premium

These have strong oversubscription, sector tailwinds, or attractive financials:

- Seshaasai Technologies 💻

- QIB subscription ~190x, PAT ₹222 Cr FY25, RoE ~33%.

- BFSI-focused card & IoT solutions, high entry barriers.

- Valuation stretched (28x PE), but demand scarcity of float = strong listing pop.

- Verdict: Likely strong premium; book profits on listing if you’re short-term. Long-term growth moderate.

- Solarworld Energy Solutions ⚡

- Revenue ₹545 Cr FY25, order book ₹2,500 Cr, but IPO priced aggressively at ~33x PE.

- Sector tailwinds (solar EPC backward integration).

- Verdict: Premium listing possible due to demand sector buzz. But valuations leave little on table → better to sell on listing unless you want solar exposure.

- Anand Rathi Share and Stock Brokers 📊

- Established brokerage, PAT ₹104 Cr FY25, RoE ~23%.

- Valuation ~18x PE, in line with peers like Angel One/Motilal.

- Verdict: Likely premium listing; can be held medium-term as a steady financial services play.

- True Colors SME

- FY25 revenue ₹234 Cr, PAT ₹25 Cr, margins improving, RoE ~44%.

- Digital textile printing niche, high growth.

- GMP ~₹30 above issue price.

- Verdict: Premium listing expected; also has medium-term growth legs.

- Matrix Geo SME 🛰️

- FY25 revenue ₹22 Cr, PAT ₹5.9 Cr, RoE ~35%.

- Drone GIS services, marquee clients (Railways, Adani, NTPC).

- Valuation ~25x PE, but niche high growth.

- Verdict: Likely premium listing; could be held medium term if you want exposure to geospatial/infra tech.

⚖️ Mixed — Premium Possible but Risky Beyond Listing

- Jaro Institute of technology 🎓 (EdTech)

- FY25 revenue ₹252 Cr, PAT ₹52 Cr, RoE ~30%.

- Attractive vs peers (Veranda loss-making).

- Valuation ~25x PE, reasonable.

- Verdict: Premium listing likely. Could be held medium term, but monitor dependence on Tier-2 institutes.

- Ecoline Exim SME 🌱

- FY24 revenue ₹281 Cr, PAT ₹22 Cr, export-driven eco packaging.

- Margins ~8%, debt moderate.

- Order book strong, but export dependency risk.

- Verdict: Mild premium possible. Medium-term hold only if you believe in sustainability/export story.

🛑 Weak Balance Sheets / Overpriced — Sell on Listing

- Aptus Pharma SME 💊

- FY25 revenue ₹25 Cr, PAT ₹3.1 Cr, but debt ₹10 Cr vs net worth ₹7 Cr.

- Working capital stress (high receivables/inventory).

- Valuation ~15x PE, aggressive for small pharma distributor.

- Verdict: Sell on listing; avoid long-term.

- NSB BPO SME 📞

- FY25 revenue ₹138 Cr, PAT ₹8.5 Cr, margins thin (6%).

- RoE ~6%, PE ~34x → expensive for a BPO.

- Verdict: Sell on listing; weak fundamentals.

- BharatRohan SME 🚁

- Drone-based agri analytics. FY25 revenue ~₹22 Cr, PAT ~₹2.3 Cr.

- Interesting niche, but very small scale, profitability thin.

- Verdict: Speculative. May list flat to mild premium. Safer to exit on listing.

📌 Summary

- Premium Hold (medium/long-term): Anand Rathi, True Colors, Matrix Geo, maybe Jaro.

- Premium Sell on Listing: Seshaasai, Solarworld.

- Flat/Weak → Sell on Listing: Aptus Pharma, NSB BPO, BharatRohan.

- Niche/Export Play (Hold selectively): Ecoline.

#IPO #StockMarket #IndiaInvesting #SMEIPO #ListingGains #StockMarketIndia #solarworld #SeshaasaiTechnologies

#jaro #anandrathi #nsb

#ecoline #matrixgeo #TrueColors #bharatrohan #aptus #pharma #IPOAlert #IPOGMP #IPOnews #ipoallotment #ipolisting

4

7

1,881

26 Sep 2025

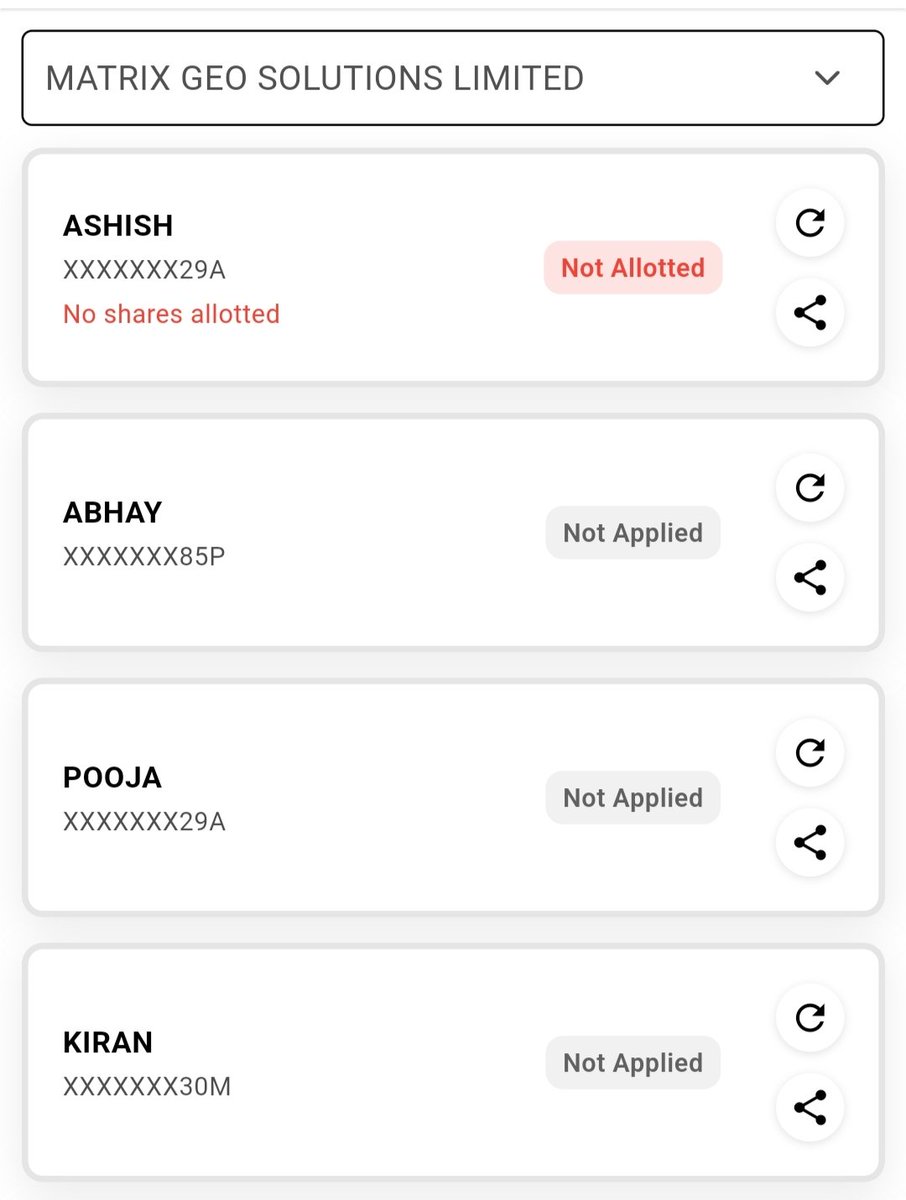

Matrix Geo solutions ( Sme Ipo ) allotment has been announced…

As happens 99.9% of the time, the result was the same — zero allotment.

Congratulations to those who received the allotment.

#Matrixgeo #Smeipo #ipoallotment

3

11

1,697

25 Sep 2025

IPOs Closing on 25 September 2025 ( Thursday ) -

Anand Rathi Share & Stock Brokers Limited ( Mainboard IPO ) -

Post-IPO valuation stands at ~25× P/E.

Peer comparison -

#motilaloswal → ~20 × P/E

#AngelOne → ~20 × P/E

#IIFL → ~13 × P/E

The IPO is not coming at a cheap valuation compared to peers.

Final View -

Apply only for a small listing gain.

Seshaasai Technologies Limited ( Mainboard IPO ) -

Jaro Institute of Technology Management & Research Limited ( Mainboard IPO ) -

SolarWorld Energy Solutions Limited ( Mainboard IPO ) -

Valuations and fundamentals appear to be average.

Final View -

Can be considered for a small listing gain.

Possibility -

One of them may deliver up to 15% positive listings.

In the long term, stock re-rating is possible.

True Colours Limited ( SME IPO ) -

Lead Manager -

#GYR Capital, which has a strong track record.

Final View -

Suitable for a 10 – 14% listing gain.

Bharat Rohan Airborne Innovations Limited ( SME IPO ) -

Matrix Geo Solutions Limited ( SME IPO )

Both companies have a decent business model.

Listing gains are not assured.

Strategy -

If allotted and listing performance is weak, I am prepared to hold for the medium term.

Final View -

Apply with a cautious approach.

For detailed IPO analysis, check the link below and decide accordingly -

Anand Rathi Share & Stock Brokers Limited -

x.com/Ashishkafunda/status/1…

Seshaasai Technologies Limited -

x.com/Ashishkafunda/status/1…

Jaro Institute of Technology Management & Research Limited -

x.com/Ashishkafunda/status/1…

SolarWorld Energy Solutions Limited -

x.com/Ashishkafunda/status/1…

True Colours Limited ( SME IPO ) -

x.com/Ashishkafunda/status/1…

Bharat Rohan Airborne Innovations Limited -

x.com/Ashishkafunda/status/1…

Matrix Geo Solutions Limited -

x.com/Ashishkafunda/status/1…

In SME IPOs, the risk is higher compared to Mainboard IPOs.

Before applying for an IPO, think carefully and definitely take advice from a good financial expert.

I am Not Sebi Registered ...Views are Personal . DYDD

#Solarworldenergy #jaroinstitute #Bharatrohan #Matrixgeo #Anandrathi

#seshaasai #IPOAlert #IPOs

23 Sep 2025

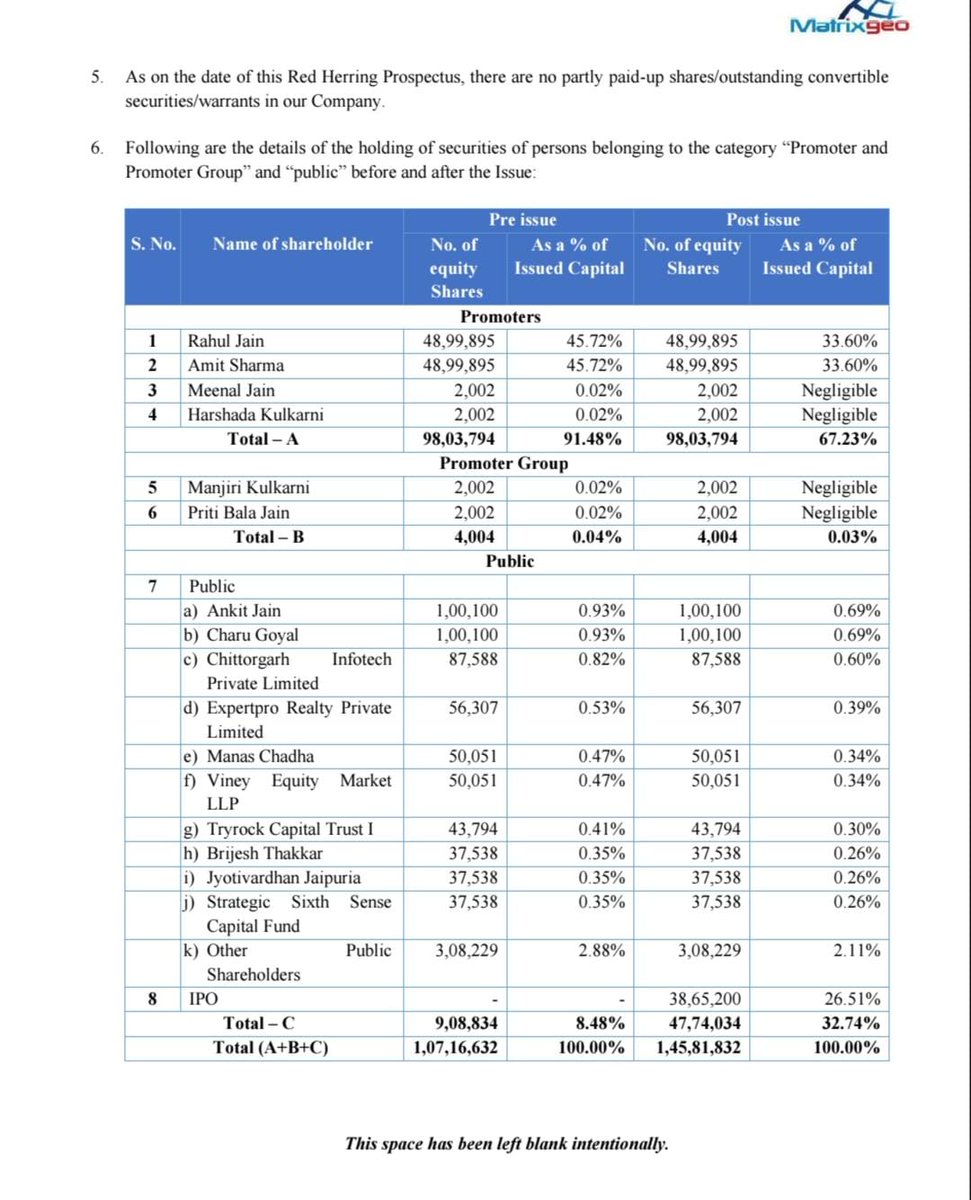

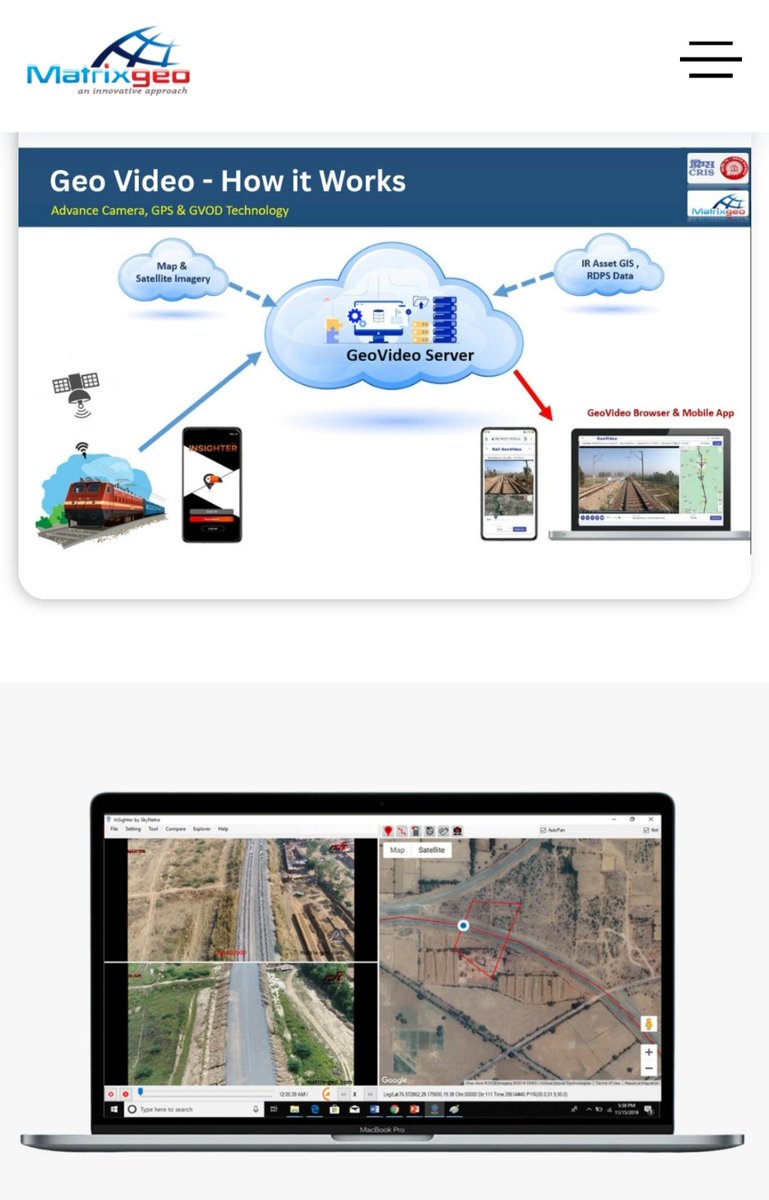

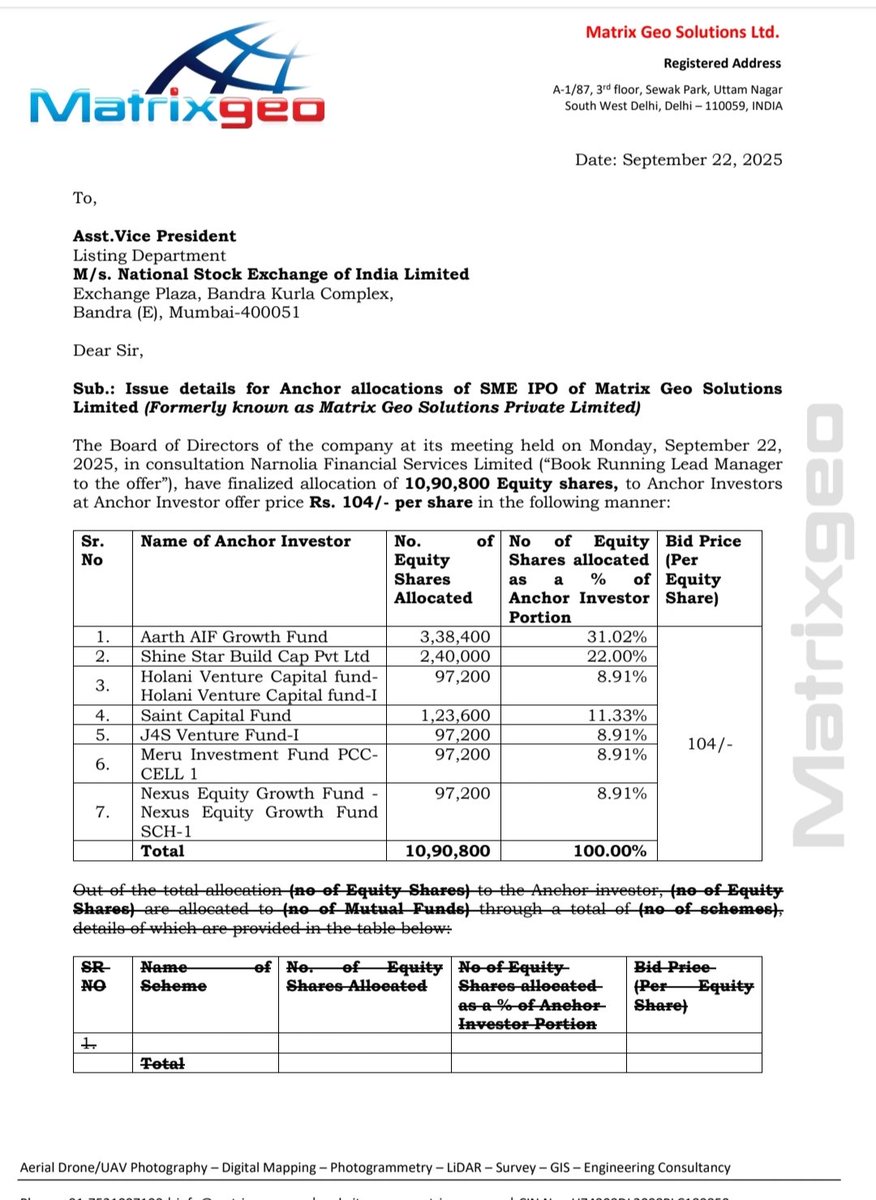

Matrix Geo Solutions Limited ( NSE SME IPO ) Analysis -

IPO Details -

IPO Date: 23 – 25 Sept 2025

Price Band: ₹98 – ₹104

Lot Size: 1,200 shares

Face Value: ₹10

Issue Size: ₹40.20 Cr ( Full Fresh )

Business Activities -

Core Focus -

Geospatial & Consulting Services with Drone-as-a-Service ( DaaS ) and Remote Sensing.

Drone-as-a-Service ( DaaS ) -

High-resolution aerial surveys via drones.

Deliverables -

#Orthophotos

#3D models

#DEM

#Topographical maps

#Geo-referenced videos.

Applications -

#mapping

#Surveillance

#Infrastructure Inspection

#Project Monitoring.

Geospatial & Remote Sensing Consulting -

Uses #LiDAR, satellite imagery & drone surveys.

Provides end-to-end advisory data analysis reports.

New Vertical – Drone Training & Education -

#DGCA Authorised Remote Pilot Training Organisation ( RPTO ).

Certified training programs under #drone Rules 2021.

RPC valid for 10 years.

81 drone pilots trained ( as of July 31, 2025 ).

Financial Highlights ( Crore ) -

Net Worth -

FY25: 21

FY24: 11

FY23: 8

Revenue from Operations -

FY25: 22

FY24: 13

FY23: 6

PAT ( Profit After Tax ) -

FY25: 5.86 , Margin -

FY24: 3.35 , Margin -

FY23: 1.09 , Margin -

EPS -

FY25: 5.86

FY24: 3.35

FY23: 1.09

RoNW -

FY25: 35%

FY24: 34%

FY23: 14%

Total Borrowings -

FY25: 1.68 ( almost debt-free )

FY23: 1.64

FY24: 1.62

Pros / Strengths / Positives -

Strong Order Book –

₹22.89 Cr in FY25 ( higher than FY25 revenues ).

Strong Financial Growth –

Revenue grew from ₹6 Cr ( FY23 ) → ₹22 Cr ( FY25 ); PAT grew 5x in 3 years.

Diversified Client Industries –

#railways

#Roadways

#water

#Renewable Energy

#Agriculture

#Mining

#Urban & Rural Planning.

Prestigious Projects Delivered –

#IndianRailways High-Speed Corridor

#Bharatmala

#Hemkund Sahib Ropeway

#statue of Unity development

#chenab River survey.

Low Debt –

Borrowings only ₹1.68 Cr vs Net Worth ₹21 Crore..

Healthy Profitability –

RoNW > 35% in FY25, showing efficient use of capital.

Cons / Risk / Weaknesses -

Business Dependency –

71% of revenue from Drone-as-a-Service ( DaaS ).

New Vertical ( Drone Training ) – No revenue contribution yet.

Industry Dependency –

#railways contributed 55% of FY25 revenue.

Geographical Concentration -

65% revenue from 3 states -

#Delhi ( 32% )

#UP ( 17% )

#Telangana ( 16% ).

Supplier Concentration Risk –

Top 1 Supplier: 42% of purchases ( ₹3 Cr ).

Top 5 Suppliers: 90% of purchases.

Scale Risk –

Current revenue ( ₹22 Cr ) is still relatively small compared to larger peers in infra-tech consulting.

Customer Concentration Risk –

Top 1 Customer: 19% of revenue.

Top 5 Customers: 59% of revenue.

Top 10 Customers: 84% of revenue.

Overall Observation -

Matrix Geo is a high-growth niche tech company in geospatial & drone-based solutions, with strong profitability and expanding opportunities ( training vertical ). However, high dependency on DaaS, limited geography, and customer concentration are key risks to watch.

I am Not Sebi Registered ...Views are Personal . DYDD

Apply Or Avoid Decision Upto 25 September ,,, 2 P.M

#Matrixgeo #Smeipo #IPOAlert

8

2,730

24 Sep 2025

Matrix Geo Solutions SME IPO (₹98-₹104) closes 25 Sep. ₹124.8 Cr for geo-tech upgrades. Vadodara infra surveyor w/ 22% growth to ₹28 Cr rev. GMP ₹4-6. Budget infra bet. Apply now!

#IPO #MatrixGeo #SME

3

297

24 Sep 2025

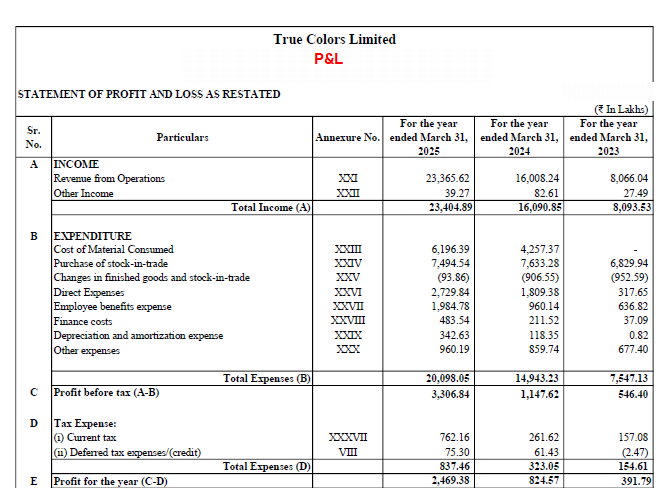

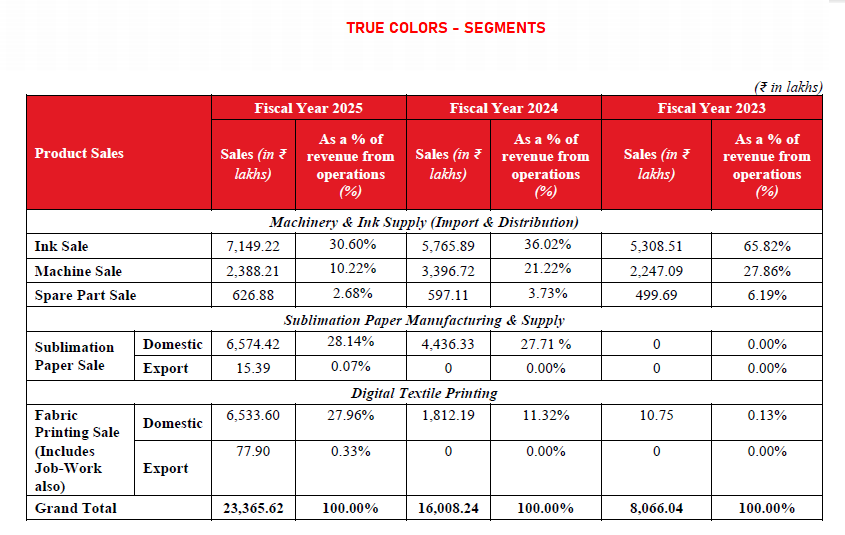

TRUE COLORS SME IPO BUSINESS REVIEW

3 Full Reviews in 1 day! BHARATROHAN and MATRIXGEO was posted earlier, today. Here is TRUE COLORS

TRUE COLORS SME IPO BUSINESS REVIEW. 🌟AVOIDED NOW, only due to post listing price behavior of KAYTEX👎 and ARBIL Paper👎.

BUT YOU MAY APPLY 👍 AFTER STUDYING POTENTIAL OF DIGITAL PRINTING in TEXTILES.

Company imports and trades digital printing machines and inks used by textile industry. It manufactures Sublimation Paper( used in digital textile printing). It also does digital printing by itself on fabrics and sells 🩷LIKE, READ, RETWEET FULL REVIEW & DECIDE

This business review is based on DRHP/RHP filed by the company at Exchange & is based on reviewer’s understanding of the documentation. For a full understanding of risks, financials, objectives & prospects suggest to go through the RHP in detail & form own opinion.

OBJECTS:

Out of Rs.127.96 Cr Raised, Rs.19.1Cr is OFS and Rs.108.86Cr is Fresh Issue. Rs.48.9Cr for Working Capital and Rs.42Cr for Loan Repayment and rest for general and listing expenses

Crisil Ratings 👍has been retained for Monitoring IPO Fund Usage

BUSINESS & PROSPECTS:

Out of Total FY25 Revenue of Rs.234Cr, 44% came from Trading of Ink and Digital Textile Printing Machines and 56% from manufacturing carried out in their factory units. (ie 28% from Sublimation Paper and 28% from Digital Printed Textiles)

So 44% is trading revenue by selling imported printing ink and printers. Rest is from sales of Submilation Paper and printed textiles.

As of Set 2025, company has total debt of Rs.74Cr including 35Cr for WC. Out of this 42Cr will be retired using IPO Funds 👍

VALUATION AND DECISION:

Company’s Sublimation paper manufacturing is exactly like recently listed and bombed ARBIL Paper(Down 17% from IPO Price).

Company’s Digital Textile Printing work is exactly like recently listed and bombed Kaytex Fabrics (Down 40% from IPO Price)

Rs.191 is at 19x its TTM earnings, on post IPO equity basis. Kaytex Fabrics IPO price of Rs.180 was at 16x and currently due to price crash, it is available at 10x.

The 42Cr debt repayment and 35Cr working capital from IPO funds should help boost bottom line 👍in Fy26 and Fy27

Direct digital printing on textiles is a good business 👍especially for fashion fabrics. But market has ignored KAYTEX . Considering the market reaction to KAYTEX and ARBIL paper, AVOIDED now.

But certainly this company need to be monitored for possible entry,👍 if market sentiment related to valuation of this segment improves.

Suggest to assess by yourself and take your own decision, after further study, considering various factors discussed and any other info available.

Images: P&L & SEGMENTS

🩷LIKE 🔖 BOOKMARK TRUE COLORS SME IPO REVIEW

#StocksInFocus #StockToWatch

3

5

65

22,867

24 Sep 2025

MatrixGeo is buying 40 drones from manufacturers with clear cut specs including LIDAR, Thermal Cameras etc. No delay. No bullsh**! (The manufactures would get DGCA approval) If the asking valuation was low this would have been MUST APPLY.

The other, "BetterIndia Magazine type company", (BharatRohan) is going to take upto 1.5 years to buy parts, do 3D printing, do research and experiment with many trainees and engineers to assemble drones and then have to get DGCA approval by themselves! STUPID & INSANE!

3

1

46

8,729

23 Sep 2025

Matrix Geo Solutions Limited ( NSE SME IPO ) Analysis -

IPO Details -

IPO Date: 23 – 25 Sept 2025

Price Band: ₹98 – ₹104

Lot Size: 1,200 shares

Face Value: ₹10

Issue Size: ₹40.20 Cr ( Full Fresh )

Business Activities -

Core Focus -

Geospatial & Consulting Services with Drone-as-a-Service ( DaaS ) and Remote Sensing.

Drone-as-a-Service ( DaaS ) -

High-resolution aerial surveys via drones.

Deliverables -

#Orthophotos

#3D models

#DEM

#Topographical maps

#Geo-referenced videos.

Applications -

#mapping

#Surveillance

#Infrastructure Inspection

#Project Monitoring.

Geospatial & Remote Sensing Consulting -

Uses #LiDAR, satellite imagery & drone surveys.

Provides end-to-end advisory data analysis reports.

New Vertical – Drone Training & Education -

#DGCA Authorised Remote Pilot Training Organisation ( RPTO ).

Certified training programs under #drone Rules 2021.

RPC valid for 10 years.

81 drone pilots trained ( as of July 31, 2025 ).

Financial Highlights ( Crore ) -

Net Worth -

FY25: 21

FY24: 11

FY23: 8

Revenue from Operations -

FY25: 22

FY24: 13

FY23: 6

PAT ( Profit After Tax ) -

FY25: 5.86 , Margin -

FY24: 3.35 , Margin -

FY23: 1.09 , Margin -

EPS -

FY25: 5.86

FY24: 3.35

FY23: 1.09

RoNW -

FY25: 35%

FY24: 34%

FY23: 14%

Total Borrowings -

FY25: 1.68 ( almost debt-free )

FY23: 1.64

FY24: 1.62

Pros / Strengths / Positives -

Strong Order Book –

₹22.89 Cr in FY25 ( higher than FY25 revenues ).

Strong Financial Growth –

Revenue grew from ₹6 Cr ( FY23 ) → ₹22 Cr ( FY25 ); PAT grew 5x in 3 years.

Diversified Client Industries –

#railways

#Roadways

#water

#Renewable Energy

#Agriculture

#Mining

#Urban & Rural Planning.

Prestigious Projects Delivered –

#IndianRailways High-Speed Corridor

#Bharatmala

#Hemkund Sahib Ropeway

#statue of Unity development

#chenab River survey.

Low Debt –

Borrowings only ₹1.68 Cr vs Net Worth ₹21 Crore..

Healthy Profitability –

RoNW > 35% in FY25, showing efficient use of capital.

Cons / Risk / Weaknesses -

Business Dependency –

71% of revenue from Drone-as-a-Service ( DaaS ).

New Vertical ( Drone Training ) – No revenue contribution yet.

Industry Dependency –

#railways contributed 55% of FY25 revenue.

Geographical Concentration -

65% revenue from 3 states -

#Delhi ( 32% )

#UP ( 17% )

#Telangana ( 16% ).

Supplier Concentration Risk –

Top 1 Supplier: 42% of purchases ( ₹3 Cr ).

Top 5 Suppliers: 90% of purchases.

Scale Risk –

Current revenue ( ₹22 Cr ) is still relatively small compared to larger peers in infra-tech consulting.

Customer Concentration Risk –

Top 1 Customer: 19% of revenue.

Top 5 Customers: 59% of revenue.

Top 10 Customers: 84% of revenue.

Overall Observation -

Matrix Geo is a high-growth niche tech company in geospatial & drone-based solutions, with strong profitability and expanding opportunities ( training vertical ). However, high dependency on DaaS, limited geography, and customer concentration are key risks to watch.

I am Not Sebi Registered ...Views are Personal . DYDD

Apply Or Avoid Decision Upto 25 September ,,, 2 P.M

#Matrixgeo #Smeipo #IPOAlert

1

3

1,159

22 Sep 2025

1

7

1,464

27 Oct 2023

📌📌📌

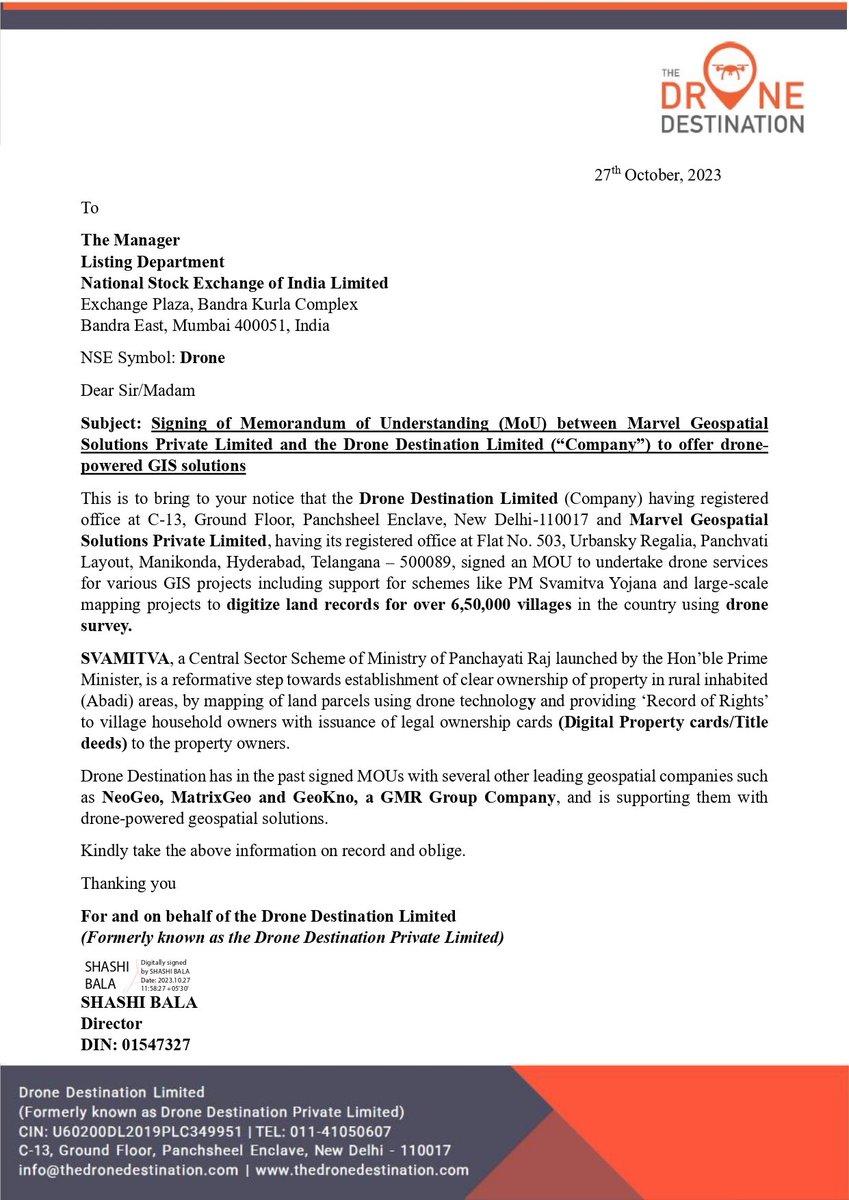

Drone Destination Limited informed the exchange about the signing of a Memorandum of Understanding (MoU) with Marvel Geospatial Solutions Private Limited to offer drone-powered GIS solutions. They will provide drone services for various GIS projects, including support for schemes like PM Svamitva Yojana and large-scale mapping projects to digitize land records for over 6,50,000 villages in the country using drone survey.

📍Drone Destination has previously signed MOUs with leading geospatial companies like NeoGeo, MatrixGeo, and GeoKno, a GMR Group Company, to support them with drone-powered geospatial solutions.

#SME #Drone 📢🔗✨🔖💡👉

1

13

1,727

Help students understand models

Integrates & weaves together many types of geological models @matrixgeo

youtube.com/watch?v=Y2XnpDX5… …

#GreatGeoVideos

#map #Geology #EarthScience #models #NGSS #STEM #STEAM

3

7