🚀 New AI tool I'm obsessed with: Recall.ai

It automatically records and indexes every meeting, call, and even casual conversation, then lets you search them like Google.

Never forget what was said again.

If your work involves lots of calls, this is next level.

Anyone using Recall or similar memory tools?

#AITools #Productivity #MemoryAI

3

Jun 11

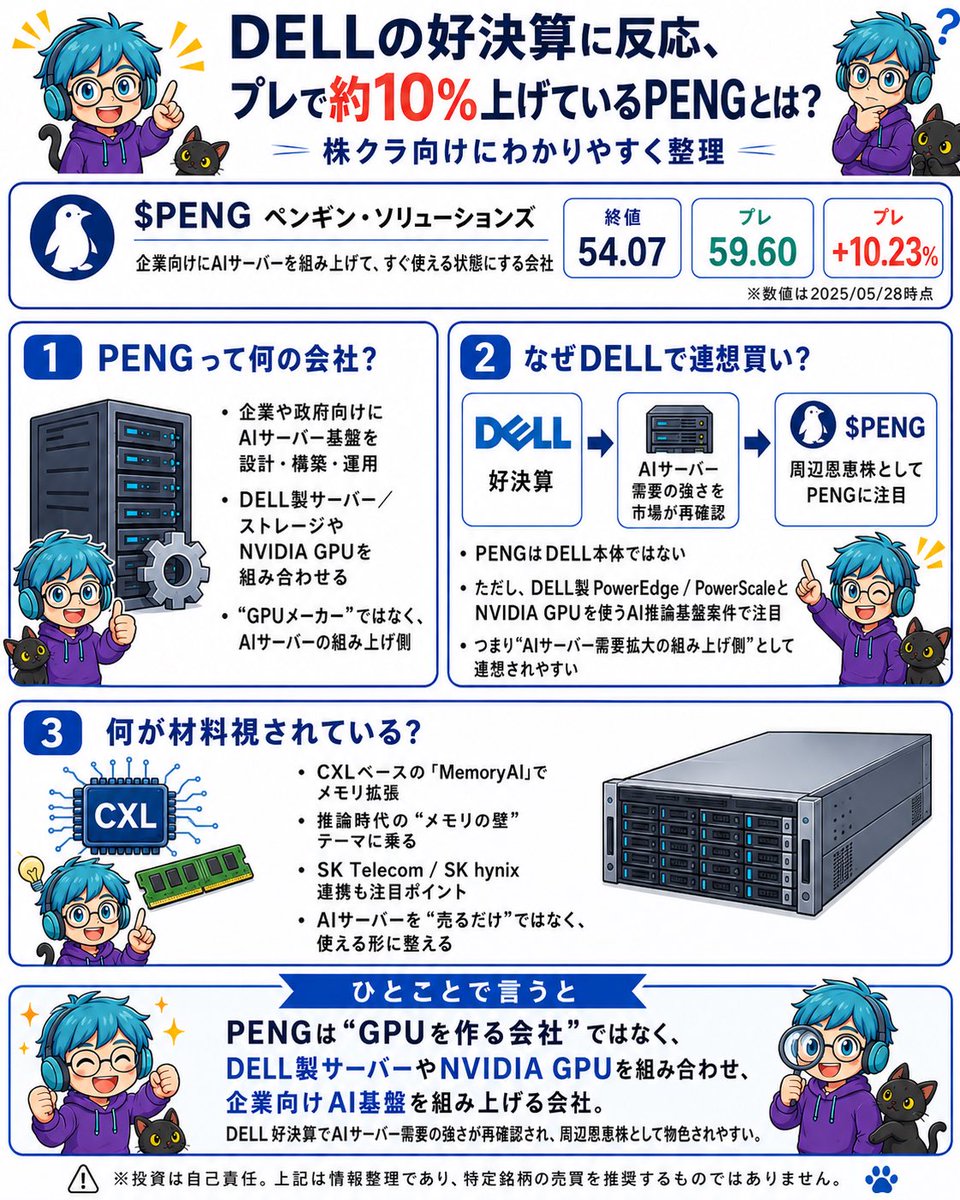

$PENG 注目してます。

Penguin Solutions(PENG)

KVキャッシュ戦略の核心

PENGの今年最大の話題は、業界初の「量産対応CXLベースKVキャッシュサーバー(MemoryAI)」の発表です。DDR5メインメモリ3TB+最大8枚の1TB CXLアドインカードでGPUメモリからKVキャッシュをオフロードし、TTFT(最初のトークン生成時間)短縮とスループット向上を実現する もの。最大11TBのCXLメモリを提供し、NVIDIA Dynamo(KVキャッシュオフロード用ソフトウェア)と互換、3月のGTCで披露されました 。推論時代の「メモリウォール」問題に正面から挑む製品で、SMART Modular由来の30年のメモリ技術が強みです。

直近業績と通期予想

•Q2 FY26(2026年2月期):売上$343M(前年比-6%)、Non-GAAP EPS $0.52 。コンセンサスは上回りました

•セグメントではメモリ部門がAI需要と価格上昇で 63%と急成長。一方Advanced ComputingはPenguin Edge事業終了で減収

•ガイダンス:通期売上成長率を 6%から 12%に上方修正 、EPSは$1.30±$0.15へ引き上げ(旧$0.85±$0.25)

•さらに6月1日に「エージェント型AI需要を背景に、通期の売上・EPSともレンジ上限で着地見込み」と再確認

•アナリスト予想はFY26売上$1.58B、EPS $1.22、来期純利益 157%成長見込み、目標株価コンセンサス$50.14

1

1

249

Jun 11

Exactly. The “intelligence layer” is where the business value shows up, but my second-order angle is the infrastructure constraint underneath that layer.

For SMEs or enterprises to turn raw data into decisions quickly, the system still needs to retrieve, hold, and process context efficiently. So that's where inference becomes memory-heavy. More context, more agents, more retrieval, more concurrent users = more KV-cache / memory pressure.

That is the $PENG angle for me.

Not “copycat GPU infrastructure,” and not “next Nvidia.” More like: if enterprise AI moves from pilots to real workflows, the bottleneck shifts toward memory expansion, CXL, KV-cache infrastructure, and AI/HPC deployment for companies that cannot build like hyperscalers.

Penguin’s Integrated Memory segment grew ~63% YoY in Q2 FY26 and is now the largest part of the business. Their MemoryAI KV Cache Server is directly aimed at that inference memory wall.

The risk is that the stock already re-rated hard while total company revenue has not fully broken out yet, so I’m not calling it cheap. But the second-order angle is real: the intelligence layer needs infrastructure that can actually feed it fast enough.

1

20

Jun 11

$PENG AI memory bottleneck thesis

I’ve been digging into Penguin Solutions ($PENG), and this is one of the more interesting second-order AI infrastructure names on the market. The thesis is not “next Nvidia.” That is lazy. The cleaner thesis is that Penguin sits near a real AI infrastructure constraint: inference memory.

As AI workloads move from training-heavy to inference-heavy, the bottleneck shifts. GPUs still matter, but inference at scale also stresses memory capacity, bandwidth, latency, KV-cache management, CXL expansion, and cluster utilization. If memory cannot keep up, expensive GPU clusters become less efficient. That is where $PENG becomes relevant.

Penguin has three main business lines: Advanced Computing, Integrated Memory, and Optimized LED. Advanced Computing designs, deploys, and manages AI/HPC clusters for enterprises, governments, neoclouds, and customers that cannot build like hyperscalers. Integrated Memory includes SMART Modular / SMARTsemi, DRAM modules, flash/SSD, specialty/rugged memory, CXL memory expansion, and the MemoryAI KV Cache Server. Optimized LED is the Cree LED business, which is mature, cyclical, and not the core of the AI thesis.

The real story is Integrated Memory. In Q2 FY26, Integrated Memory revenue was $171.6M, up from $105.3M in Q2 FY25, or roughly 63% YoY. That segment was about 50% of total Q2 revenue and has become the largest and fastest-growing part of the company. This is what the market is paying for.

But the important nuance: total company revenue is not yet breaking out. Q2 FY26 net sales were $343.0M, down from $365.5M in Q2 FY25. Over the last several quarters, total revenue has mostly stayed inside a ~$324M to ~$366M range. So the stock move is not being driven by broad absolute revenue acceleration yet. It is being driven by mix shift, guidance revisions, AI-memory narrative, and multiple expansion.

That distinction matters. $PENG is not a simple “revenue inflecting everywhere” story. It is a company where the market is re-rating the whole business because the Integrated Memory segment is becoming more strategically important.

The bull case is that this mix shift is exactly the point. Penguin is moving away from lower-quality / declining pieces and toward higher-value AI memory infrastructure. The company’s MemoryAI KV Cache Server is a CXL-based product designed for enterprise inference workloads and marketed around up to 11TB of disaggregated memory. That directly targets the AI inference memory wall, especially for long-context workloads, RAG, agentic AI, financial/legal document processing, and high-concurrency enterprise inference.

The second bull angle is AI factory deployment. Penguin is not just selling memory modules. Through Advanced Computing, it also helps design, deploy, manage, and optimize AI/HPC infrastructure. That matters because the next wave of AI infrastructure is not only the hyperscalers. Enterprises, sovereign AI buyers, financial institutions, universities, labs, and specialized cloud providers all need AI infrastructure, but many cannot build like Microsoft, Amazon, Google, or Meta.

This is where Penguin can sit: not as the GPU owner, not as the hyperscaler, but as the infrastructure integrator, memory specialist, and AI deployment layer.

The ecosystem validation is real but needs to be stated accurately. Penguin has Dell ecosystem relevance and was named Dell Technologies Global Alliances Americas AI Partner of the Year. SK Telecom is also strategically involved through a $200M convertible preferred investment. The Celestial AI / Marvell angle is more nuanced. Penguin was an early investor in Celestial AI, which Marvell acquired. Penguin realized a gain from that stake, and the photonic memory appliance development relationship appears to continue through the inherited Celestial AI relationship now under Marvell. But I would not call this a clean formal “Marvell JV” unless the company itself uses that language. The thesis is already strong enough without overstating it.

Now the risk side.

First, valuation. $PENG has already had a major move and recently traded near an all-time high around $73. At current levels around the low-$60s, the stock is no longer undiscovered. The report I reviewed had PENG at roughly 27x FY26 non-GAAP EPS, around 2.2x forward sales, roughly 25x P/FCF, and meaningfully above where SGH/PENG historically traded as a memory-module company. That does not make it uninvestable, but it means the market is already pricing in execution.

Second, the company still has hardware-cycle exposure. Integrated Memory growth is partly tied to favorable memory pricing. That helps in an upcycle, but it can reverse. If memory pricing rolls over, revenue growth and margin can both get hit. This is not a pure recurring software story.

Third, margin pressure needs to be watched. The company raised revenue and EPS guidance, but gross margin guidance moved lower. That tells me investors need to focus on the quality of growth, not just the headline revenue number. If Integrated Memory grows but gross margin compresses, the market may start asking how much of this is structural AI demand versus cyclical memory pricing.

Fourth, Advanced Computing is still weak. Q2 FY26 Advanced Computing revenue was $115.7M, down from $200.2M in Q2 FY25. The bull explanation is that Penguin is moving away from lower-quality work and shifting toward AI infrastructure and memory. That may be true, but until Advanced Computing stabilizes, Integrated Memory has to carry the whole narrative.

Fifth, governance is a yellow flag. CEO transition earlier in 2026. CFO transition announced June 1. The company stated the CFO departure was not due to disagreement over accounting, controls, financial reporting, or operations. That matters. But two C-suite changes in a short window, while the stock is near highs, still deserves attention. There was also insider selling into the run-up from directors/officers. Insider selling is not automatically bearish, but the timing is not something I would ignore.

Sixth, dilution. The balance sheet does not look distressed, and the company retired near-term 2026 converts. But SK Telecom’s $200M convertible preferred and the remaining in-the-money convertible notes create potential share-count overhang. Buybacks help offset this, but investors need to watch diluted share count, not just headline EPS.

So the setup is not simple. The business thesis is real. The stock setup is less clean.

The bull case:

AI inference creates a real memory wall

CXL memory expansion becomes more important

KV-cache infrastructure becomes a larger enterprise problem

Integrated Memory is now the largest and fastest-growing segment

Penguin has AI/HPC infrastructure deployment capability

Dell/SKT ecosystem ties add credibility

MemoryAI and photonic memory appliance optionality create upside

Balance sheet is not distressed

Buybacks are offsetting some dilution

The bear case:

Total company revenue has not decisively broken out

Advanced Computing declined sharply YoY

Integrated Memory may be partly riding memory pricing

Gross margin guidance moved lower

Stock already re-rated aggressively

Governance churn is a yellow flag

Insider selling into strength is not ideal

Convertible/preferred dilution needs monitoring

Retail attention is no longer early

The key proof points I want from here:

Total revenue needs to break above the old ~$365M ceiling for more than one quarter.

Integrated Memory growth needs to stay strong without gross margin collapsing.

Management needs to show the growth is product/volume-driven, not just DRAM pricing.

Advanced Computing needs to stabilize and return to YoY growth.

The company needs to name a credible permanent CFO.

Diluted share count needs to stay controlled.

Penguin needs to disclose harder metrics around MemoryAI, CXL, PMA, ClusterWare, AI/HPC bookings, or customer adoption.

Fiscal Q3 FY26 needs to confirm the high-end FY26 guide rather than expose the stock as priced for perfection.

My view: $PENG is a real AI infrastructure bottleneck company, but it is not obviously cheap at current levels. The cleanest thesis is not that Penguin is “the next Nvidia.” The cleanest thesis is that Penguin is a second-order AI memory/inference infrastructure play that the market has started to re-rate before the full financial proof has arrived.

That makes it watchlist-worthy for me

One-line thesis: $PENG is a real AI inference memory-bottleneck play scaling CXL, KV-cache, memory integration, and AI/HPC infrastructure deployment.

One-line risk: $PENG is still a hardware-cycle exposed company that has already re-rated hard while total revenue has not yet decisively broken out.

For me, this is a “real thesis, price matters” name. I want proof before chasing

1

4

365

Join us for our webinar tomorrow, “Enterprise-Scale AI Inference is Memory Bound: How to Overcome the Memory Wall,” on June 9 from 9-10 AM PT.

We'll discuss how traditional infrastructure can no longer efficiently keep pace with growing query volumes and memory demands, the crucial role memory plays in AI performance, and how our MemoryAI™ KV cache server addresses the memory wall.

Register today and tune in tomorrow: bizclick.registration.goldca…

2

4

25

813

$PENG

Bernstein’s lift of HBM4 toward $53/GB for the 2027 Vera Rubin volume ramp sharpens the cost architecture of AI racks, with memory and storage now pressing against 35% of the ~$9.1M unit.

I mean the $PENG memory segment thesis writes itself from here.

Penguin Solutions’ CXL MemoryAI platform addresses this directly by inserting a coherent, low-latency expansion layer that offloads KV cache and other inference working sets from the GPU’s premium HBM stacks into far cheaper, higher-capacity DDR5 pools.

The result is a practical memory tiering arbitrage: hyperscalers can sustain larger contexts and higher GPU occupancy without proportionally scaling the most expensive memory component. PENG’s Integrated Memory segment, already growing 63% year-over-year, sits at the center of this efficiency layer through both its module business and production-ready CXL appliances.

Not to mention, Penguin’s relationship with SK telecom is about to pay serious dividends in the AI factory segment.

🐧👀

“We expects the prices to increase to $53/GB in 2027, when Vera Rubin will be shipping in volume.”

Bernstein is very bullish on 2027 HBM4 pricing. LFG!!!

2

13

1,597

Jun 8

No new conviction buys this week. Added AMPG to the catalyst-watch board, refreshed PENG, and BWA stays removed because it is a value/FCF idea, not asymmetric enough for this list.

$VST @ $147.99 — 🔴 ENTRY ZONE. Cleanest liquid AI-power/nuclear scarcity play. Entry: common add only around $146-$151 dislocation with thesis intact; no fresh calls.

MRAM @ $23.98 — Hold existing sleeve only. Defense/edge-memory proof is real, but Kerrisdale/insider-sale/GM risk keeps add-size blocked. Entry: do not add before Q2 proof.

CEG @ $253.34 — 🟡 APPROACHING. Nuclear plus Calpine AI-power platform, but secondary overhang and option breakeven matter. Entry: common first watch $255-$265, preferred $240-$255; no calls.

MNDY @ $84.82 — Software reset is interesting after the squeeze cooled. Entry: $86-$90 / $79.5-$83 only if Q2 ARR/NDR/AI proof stays intact.

PDFS @ $54.37 — Semiconductor analytics proof is real, but valuation and FCF still cap urgency. Entry: $35-$38 if thesis intact, or after Q2 revenue/RPO/eProbe proof.

CAMT @ $170.05 — Real HBM/advanced-packaging inspection winner. Entry: no auto-add; wait for 2H revenue conversion, order/backlog strength, and margin recovery.

ONTO @ $265.49 — Quality metrology name, not cheap enough after the convert. Entry: $220-$239 if thesis intact or after FY26/Dragonfly shipment proof.

POET @ $12.01 — Photonics option, not earnings yet. Entry: tiny tracker only; add-size waits for module qualification, payment-backed PO conversion, and 2027 deployment proof.

OSS @ $16.91 — Defense/edge-compute proof is improving. Entry: no chase; Q2 must show GM above 40%, book-to-bill above 1.2x, and positive adjusted EBITDA.

OUST @ $41.06 — Physical AI perception play with real revenue growth. Entry: keep starter; add only after Q2 guide beat, margin stability, and narrower EBITDA losses.

RDW @ $19.07 — Space-defense order proof is real, but dilution/EBITDA risk remains. Entry: no chase; wait for backlog conversion, GM above 25%, and cash burn narrowing.

VPG @ $118.67 — Robotics sensor proof, but the stock already did the fun part. Entry: no chase; needs Q2 beat/raise and sensors conversion.

KEEL @ $5.32 — AI/HPC powered-site optionality. Entry: no chase; needs named lease with counterparty, MW, term, economics, and financing clarity.

AEHR @ $96.65 — AI/SiPh burn-in signal is real, but valuation is still science-project-ish. Entry: tiny tracker only; add after FY2027 guide/order conversion resets estimates.

FLNC @ $24.33 — AI data-center design validation is useful, not a purchase order. Entry: no add; wait for hyperscaler order/backlog/economics proof.

RDDT @ $172.21 — Q1 proof is excellent, but current sleeve is enough. Entry: add only on $148-$155 / $154-$163 support or after Q2 beat/raise.

NVTS @ $25.30 — 800V GaN/SiC optionality, but narrative is way ahead of backlog. Entry: token only; proof-gated add $20.50-$23.80, better $16-$17.65.

BE @ $252.60 — Real AI-power leader, still no chase. Entry: first look $274-$285 already hit but proof matters; preferred $220-$244 reset.

VRT @ $304.50 — Quality 800VDC compounder, expensive. Entry: tactical $275-$307, preferred $242-$275; add above spot only with named 800VDC production proof.

AEIS @ $303.48 — Real AI PSU beneficiary, but no named hyperscaler backlog yet. Entry: optional tiny tracker $288-$304, better reset $253-$260.

NBIS @ $224.76 — Event validated, but neocloud concentration risk is not cute. Entry: do not add here; $221-$208 intact reset or new financing/customer proof.

PENG @ $63.40 — Refreshed today. Five AI/HPC customers and MemoryAI proof are real, but spot is above the average target. Entry: token only; 0.5%-1% on $44-$52 reset or Q3 order/backlog/estimate proof.

VLN @ $2.24 — Connectivity semi with automotive/robotics optionality. Entry: tiny scout only after Q2/Q3 revenue guide, GM, and OEM production proof.

AMPG @ $5.09 — Newer micro-cap RF/5G O-RAN/quantum-LNA watch. Entry: optional tiny scout only; add after Q2/Q3 revenue, backlog, MNO conversion, and GM proof.

LPTH @ $15.15 — Backlog proof is real, but valuation and customer opacity leave thin asymmetry. Entry: first look $15, better $13.90-$14 / $13.10.

Highest conviction today: VST common in the red entry zone, but only if the broader tape stops trying to punch everyone in the face.

We'll see how it goes.

281

Jun 8

9. $PENG - Penguin Solutions

Integrated memory revenue up 63% YoY. Their MemoryAI CXL-based server adds up to 11TB of memory for AI inference workloads. 7 new AI/HPC customer logos in H1. Raised full-year guidance to 12% net sales growth, up from 6%. Solves the inference memory bottleneck.

1

4

3,784

Jun 7

$PENG --- This high-impact award directly validates Penguin’s expertise in delivering Full-Stack AI Factory Platforms, sharply boosting its bidding credibility in the mainstream enterprise market.June 3, 2026: $PENG Named Dell Technologies “Global Alliances Americas AI Partner of the Year”

$PENG ’s management explicitly stated the core driver behind its recent blowout performance: enterprise deployment of inference workloads and agentic AI systems is accelerating rapidly. This signals AI is fast transitioning from early-stage large-model training to enterprise-grade production—and PENG is perfectly positioned to capture this wave.

1.The “Full-Stack Pickaxe Play” for AI Adoption

While NVIDIA provides GPU chips, most traditional enterprises and government agencies lack the know-how to assemble, optimize, and operate massive AI data centers. PENG’s OriginAI Platform delivers end-to-end integration, cabling, thermal management, and full-stack software control (AI Infrastructure). It’s the architect that stitches NVIDIA, AMD, and Micron hardware into a seamlessly optimized, high-performance entity.

2.Perfect Fix for the AI Bottleneck — Advanced Memory Tech

As large models shift to inference and agentic workloads, the top hardware bottleneck is no longer just compute, but memory bandwidth and cache speed. PENG brings deep engineering expertise in Integrated Memory. Its CXL-based MemoryAI KV Cache Server drastically cuts AI inference latency.

3.From Cyclical to Structural Growth

The market previously labeled it a cyclical legacy hardware/LED assembler (with Cree LED and other units), leading to a depressed valuation. But 2026 results confirm its AI Infrastructure & Integrated Memory segment is now the dominant revenue driver. The stock is undergoing a major re-rating: from a “legacy hardware name” to a high-growth AI infrastructure pure-play.

1

1

24

1,987

OpenAI just upgraded ChatGPT's memory system.

It now carries context across conversations more effectively and stays useful as your situation evolves. Tell it about a July trip, and it understands when the trip is upcoming, in progress, or complete.

The update includes a memory summary for reviewing and steering what ChatGPT remembers, giving users more visibility and control. It tracks important details automatically while letting you switch back to the legacy experience if preferred.

This rolls out today to Plus and Pro users in the US, with 2x more memory capacity. Update the iOS or Android app for access. Expansion to more plans and countries is coming soon.

Read the full announcement here: openai.com/index/chatgpt-mem…

This strengthens ChatGPT as a reliable long-term assistant.

#AI #ChatGPT #OpenAI #MemoryAI #Productivity #Dreaming

2

78

Jun 3

$PENG is basically a pure play picks and shovels bet on CXL AI memory bottlenecks.

They sit at the intersection of:

Proven CXL hardware (SMART Modular NV‑CMM just made the CXL Integrators List, so not vaporware).

A production ready CXL KV‑cache server (MemoryAI) built specifically to fix the memory wall in large scale inference, with up to ~11TB of pooled CXL memory per box.

They've got a Full‑stack AI factory integration, so they’re not just selling modules but designing/deploying whole racks for hyperscalers and AI data centers.

That being said, if your thesis is connectivity CXL pooling, $PENG gives you:

1) working silicon and systems in market today

2) leverage to AI inference growth without paying GPU‑like multiples

3) a sub‑3B cap name that can re rate fast if CXL becomes standard in AI racks.

You’re effectively long the transition from DIMM‑bound nodes to pooled, composable memory across the rack.

9

923

Penguin Solutions is the 2026 Dell Technologies AI Partner of the Year in the Global Alliances category.

This prestigious award reflects our proven success in delivering full-stack AI factory platforms, combining Penguin’s proven AI infrastructure, MemoryAI solutions, ClusterWareAI software, and end-to-end services including design-build-deploy and manage with Dell Technologies’ AI-optimized servers and storage solutions. Proud to partner with @DellTechPartner. Read the full announcement: ir.penguinsolutions.com/news…

#PartnerOfTheYear #PartneringTogether

4

18

86

8,243

May 31

📌 تقرير رقم (18)

🔷 شركة Penguin Solutions

▪️(الرمز: $PENG)

▪️قطاع التكنولوجيا (Information Technology).

✍️ نبذة عامة:

▫️عندما يسمع المستثمر اسم (Penguin Solutions) يعتقد أنها مجرد شركة Memory أو Hardware.

▫️الشركة في السابق كان تخصصها الأساسي تصميم وتصنيع وحدات الذاكرة، في 2024 غيرت اسمها رسميًا إلى Penguin Solutions ( $PENG ) لتعكس تحولها من شركة يُنظر إليها كشركة ذواكر إلى شركة بنية تحتية للذكاء الاصطناعي وحلول HPC.

▫️بعد دراسة عشرات الملفات والتقارير والبيانات الرسمية، اتضح أن الشركة تحاول التحول إلى شيء أكبر بكثير شركة (Penguin Solutions)

هي AI Infrastructure & AI Factory Platform.

🔥 وهنا تبدأ القصة.

العالم اليوم يركز على NVIDIA والـ GPUs (معالجات الرسومات) لكن مع توسع الذكاء الاصطناعي بدأت تظهر مشكلة جديدة وهي امتلاك الـ GPU لم يعد كافيا.

🔥 التحدي الحقيقي أصبح:

▫️تشغيل الذكاء الاصطناعي

▫️إدارة البنية التحتية

▫️تحسين الأداء

▫️تقليل زمن الاستجابة (Latency)

▫️رفع كفاءة الذاكرة والشبكات

💡وهنا تتموضع $PENG.

اليوم الشركة تقول:"نحن لا نبيع أجهزة فقط، بل نبني ونشغل بيئات الذكاء الاصطناعي الكاملة للعملاء”.

لذلك دخل الشركة لم يعد فقط من بيع الأجهزة، بل من:

▪️التصميم

▪️التركيب

▪️التشغيل

▪️التحسين (Optimization)

▪️الدعم المستمر

😎بختصاار السالفة👇

ياطولين الاعمار التشغيل ورفع الكفاءة والاداء والادارة تحتاج شركة متخصصة فيها خاصة ان مشاكل منشأت الذكاء الاصطناعي كثيرة وفي تطور مستمر ومتابعة لحظية.

وهذا النوع من الأعمال والمشاريع عادة:

✅ أرباحه أعلى

✅ عقوده أطول

✅ العملاء يعتمدون عليك أكثر

🧐 لذلك الإدارة تريد أن ينظر لها السوق كشركة بنية تحتية للذكاء الاصطناعي وليس كشركة ذاكرة وتخزين فقط.

❌ أحد أهم الأخطاء المنتشرة في السوق: الاعتقاد أن الذكاء الاصطناعي امتلاك GPU او وحدات تخزين فقط.

✅ الحقيقة أن تشغيل AI على ملايين المستخدمين الذين يتطلب توفير لهم :

• ذاكرة ضخمة

• شبكات فائقة السرعة

• إدارة متقدمة للأحمال

• مراقبة مستمرة

• تحسين مستمر للأداء

💡وهنا تبدأ قيمة $PENG الشركة

تراهن على سوق:

AI Inference

(( وهي مرحلة التشغيل ورفع الاداء ))

وليس فقط AI Training.

⁉️ما الفرق؟

Training:

تدريب النموذج.

Inference:

تشغيل النموذج فعليًا لخدمة المستخدمين ومع انتشار:

• AI Agents

• Copilots

• Voice AI

• Enterprise AI

💡قد يصبح سوق Inference أكبر من سوق Training مستقبلًا.

✅ أيضا الشركة تتميز بأحد أهم منتجات الشركة:

MemoryAI KV Cache Server

وهو حل مصمم لمعالجة واحدة من أكبر مشاكل الذكاء الاصطناعي الحديثة:

Memory Bottleneck

أي اختناق الذاكرة ( يعني ان سرعة المعالج اكبر من سرعة الذاكرة وهنا يحصل اختناق في ارسال الملفات بين المعالج والذاكرة )

👌كلما زادت أحجام النماذج وعدد المستخدمين تزداد الحاجة إلى:

• Context Length أكبر

• Concurrency أعلى

• Latency أقل

💎 وهنا تحاول $PENG تقديم حلول متخصصة تعتمد على الذاكرة والـ KV Cache لرفع كفاءة الـ Inference.

💪الشركة لا تنافس NVIDIA بل تستخدم تقنيات NVIDIA.

🧐بعض حلولها مبنية على:

• NVIDIA RTX PRO 6000 Blackwell

• NVIDIA B300

وتضيف فوقها:

• Memory Architecture

• Optimization

• Cluster Management

• Deployment Services

😎(( بمعنى آخر ))

NVIDIA تبيع المحرك أما $PENG فتساعد العميل على بناء السيارة كاملة وتشغيلها بأعلى كفاءة.

🧐من أهم ما لفت انتباهي أن الشركة تتحدث كثيرًا عن:

Optimization

أي تحسين الأداء.

😎ففي عالم AI:

تحسين الكفاءة بنسبة 10% فقط قد يوفر ملايين الدولارات من تكاليف:

• GPUs

• الطاقة

• التشغيل

💡ولهذا السبب أصبحت خبرات:

Networking

Infrastructure ( البنية التحتية)

Scaling (القدرة الاستعابية) مهمة جدًا في عصر الذكاء الاصطناعي.

💎 ومن هنا نفهم لماذا عينت الشركة:

David Heard في مجلس الإدارة وهو الرئيس السابق لقطاع Network Infrastructure في Nokia.

📌 خبرة David Heard ليست في الهواتف فقط، بل في:

• شبكات ضخمة

• Optical Networking

• Scaling

• Hyperscale Infrastructure

وهي نفس التحديات التي تواجه AI Clusters الحديثة.

💡أكثر ما أعجبني في القصة:

أن الشركة لا تبيع "الذكاء الاصطناعي" بل تحاول حل مشكلة حقيقية وهي كيف تجعل الذكاء الاصطناعي يعمل بكفاءة وعلى نطاق واسع داخل المؤسسات⁉️

عن طريق الادارة والتشغيل السليم والمعرفة التامة بجميع المشاكل والحلول، وهذه قد تكون واحدة من أهم الفرص في دورة الذكاء الاصطناعي القادمة لشركات التشغيل والصيانة في معامل الذكاء الاصطناعي.

📊 اما مايخص التجميع المؤسسي

فيمثل ≈ 74% أي أن هناك اقبال عالي جدا من قبل المؤسسات على السهم و الشراء الداخلي يقدر 3% فقط.

🔥أهم مخاطر شركة Penguin Solutions

1. فشل التحول إلى AI Infrastructure إذا لم تنجح الشركة في التحول من Memory إلى AI Infrastructure فقد يعيد السوق تقييمها كشركة هاردوير عادية.

2. المنافسة القوية تواجه منافسين كبار جدًا، مثل:(NVIDIA،Dell،HPE،Supermicro)

3. إيرادات AI ما زالت غير واضحة.

4. ضغط الهوامش.

5. تأجيل العقود والمشاريع، بعض مشاريع AI قد تتأخر، مما يؤخر الإيرادات والنمو.

6. الاعتماد على موجة AI الحالية

إذا تباطأ الإنفاق على الذكاء الاصطناعي قد يتأثر السهم بقوة.

7. التقييم يعتمد على المستقبل

السوق يسعر الشركة على أنها قصة نمو AI، لذلك أي خيبة أمل قد تؤدي إلى هبوط قوي.

8. عدم وجود شراء داخلي قوي

الإدارة لا تقوم حاليًا بعمليات شراء كبيرة من السوق المفتوح، وهذا ليس خطرًا كبيرًا لكنه ليس نقطة قوة.

💪 نقاط القوة في $PENG :

1. تتمركز في أسرع قطاع نموًا حاليا

ليس فقط AI، بل:

AI Infrastructure AI Inference (تشغيل النماذج) وهذا القطاع ما زال في بدايته مقارنة بالـ GPUs نفسها.

2. ليست مجرد شركة Memory

3. خبرة قوية في الذاكرة (Memory)

لديها أكثر من 30 سنة خبرة في الذاكرة وحلولها، والآن بدأت تستغل هذه الخبرة لحل مشكلة حقيقية في AI:

Memory Bottlenecks وهي من أكبر مشاكل الـ Inference الحديثة.

4. تركز على Inference وليس Training فقط لكثير يركز على تدريب النماذج.

5. منتجات متخصصة وليست مجرد سيرفرات

6. لديها عملاء حقيقيون بالفعل

7. شراكات مع عمالقة القطاع

8. (((التجميع المؤسسي قوي))) 🔥

9. الإدارة تبني فريقًا مناسبًا للمرحلة القادمة

👌أما $PENG فتراهن على:

تشغيل النماذج يوميًا (Inference)

وهو سوق قد يصبح أكبر من التدريب مستقبلًا.

🏦 المعاير القوية بالشركة من أهم 3 نقاط قوة برأيي:

🥇 التمركز في AI Inference و AI Infrastructure

🥈 التجميع المؤسسي القوي

🥉 حل مشكلة الذاكرة و Memory Bottleneck و KV Cache

🔥 أكبر نقطة قوة في $PENG ليست أنها شركة Memory أو Servers، بل أنها تحاول أن تصبح:👇

الشركة التي تجعل الذكاء الاصطناعي يعمل بكفاءة وعلى نطاق واسع داخل المؤسسات وإذا نجحت في ذلك، فهذا هو السبب الذي قد يجعل المؤسسات تستمر في بناء مراكزها بالسهم.

😎الراي الفني:

▪️السهم متشبع شراء زخم عالي جدا ولكن ممكن ينزل لمناطق الدعم وهي مناطق طلب مثل 50$ - 53$ - 48$

▪️السهم لديه اهداف عند سعر 60$ - 65$ - 70$ وأيضا اعلى ممكن نشوف سعر 90$

▪️النموذج الأقرب لشارت هو علم صاعد من سعر 22$ الى 58$

🚫 في اخر هذا التقرير جميع ماذكر لا يعد توصية ابدا الشراء والبيع مسؤليتك انت

1

2

7

1,997

May 31

regarding $PENG

the interesting part is MemoryAI and CXL.

As AI inference scales, the bottleneck increasingly shifts from compute to memory capacity and KV cache management.

If that thesis plays out, PENG isn't selling servers. It's selling a solution to one of AI's next infrastructure constraints.

4

1

44

7,074

May 30

ここから先では、PENGを単なる「CXLメモリ銘柄」としてではなく、AI推論インフラの詰まりを解く会社として見ていく。

・CXLとは何か、なぜAI推論で重要になっているのか

・MemoryAIが狙うKVキャッシュ問題と、最初のトークンまでの待ち時間

・PENGをCXL部品企業と分けて見るべき理由

・AIファクトリー戦略

・数字、顧客集中、粗利率から見た「期待できる点」と「まだ怖い点」

note.com/koziii/n/n01a64ab83…

18

10,953

May 30

$PENG のMemoryAIとは何か?KVキャッシュを逃がす、AI工場の11TB冷蔵庫

AI銘柄を見ていると、主役はいつも派手だ。GPU、巨大データセンター、電力、冷却。いかにも「ここが戦場です」という顔をしている。ところが今回、目が止まったのは少し違う場所だった。

冷蔵庫だった。

もちろん本物の冷蔵庫ではない。Penguin Solutionsが出した、最大11TBのCXLベースメモリを積む MemoryAI KV cache server の話である。だが、これを「新しいメモリ製品」とだけ読むと、たぶん一番おいしいところを取り逃がす。

これは、AI工場の台所に置かれた巨大な業務用冷蔵庫みたいなものだ。

料理人がGPUなら、材料を置く場所がメモリだ。料理人がどれだけ腕利きでも、使う材料が毎回遠くの倉庫にあったら手が止まる。包丁を持ったまま待つ。火は入っているのに、肉が来ない。あの感じだ。

PENGの話は、そこから始まる。

🟦会社名より先に、まず違和感を見る

Penguin Solutionsは、もともとSMART Global Holdingsを母体にした会社だ。2024年10月に今の名前へ変わり、AIファクトリー向けの会社として見せ方を変えた。

事業は大きく三つある。

📍Advanced Computing:AIや高性能計算基盤の設計、構築、運用

📍Integrated Memory:DRAM、DDR5、CXL、SSDなどの特殊メモリ

📍Optimized LED:Cree LEDブランドのLED部品

ここで一つ引っかかる。

PENGは、純粋なAIメモリ専業ではない。LEDも持っている。耐障害コンピューティングもある。だから「CXLど真ん中のきれいな銘柄」として見ると、少し輪郭がぼやける。

だが逆に、そこが面白い。

PENGは部品を一個売る会社というより、AIの計算基盤を現場で動かす会社に近い。電源、冷却、ネットワーク、メモリ、サーバー、運用ソフト。全部をつなげて、顧客のAI工場を実際に立ち上げる側にいる。

この会社を「裏口の工場長」と呼びたい。

ステージ中央でスポットライトを浴びる主役ではない。でも本番前に搬入口を開け、機材を並べ、照明と音響のずれを直し、主役が出てくる前に現場を成立させる。そんな立ち位置だ。

🟦MemoryAIは何をしているのか

2026年4月、PENGはMemoryAI KV cache serverを発表した。会社側は、業界初の生産準備済みCXLベースKVキャッシュサーバーとうたっている。

目立つ数字はこうだ。

最大11TBのCXLベースメモリ

3TBのDDR5メインメモリ

最大8枚の1TB CXLアドインカード

AI推論、特にエージェント型AIや長い文脈処理を想定

GPUメモリの圧迫、再計算、応答遅延を抑える狙い

NVIDIA Dynamoとの互換性を訴求

NVMeベース手法より10倍速い、という会社側の主張

専門語が続くと、急に読む気が落ちる。

なので、簡単にまとめる。

生成AIは、会話の途中で「さっき何を話したか」を覚えておく必要がある。そのメモがKVキャッシュだ。短い会話なら机の上に置ける。でも会話が長くなり、利用者が増え、AIエージェントが何十個もの作業を同時に走らせると、机の上がすぐ埋まる。

机の上がGPUメモリだ。

この机は速い。ものすごく速い。ただし高いし、狭い。だからPENGは「机のすぐ横に、取り出しやすい大型冷蔵庫を置こう」と言っている。冷凍倉庫ほど遠くない。机の上ほど高くない。その中間に、CXLメモリの棚を作る。

この発想が刺さるのは、AIの重心が学習だけでなく推論へ移っているからだ。

学習は巨大なトレーニング合宿のようなものだ。一方、推論は毎日の試合である。利用者が質問し、AIが答え、また質問し、前の内容を覚えながら返す。ここでは、計算そのものだけでなく、記憶をどれだけ近くに置けるかが効いてくる。

1

10

59

30,110

May 30

$PENG: the memory angle on AI infrastructure

While everyone fights over GPUs, the next bottleneck is quietly becoming memory. Penguin Solutions is positioned right at that chokepoint.

The pitch: as AI shifts from training to inference, workloads become memory-bound. Penguin builds integrated memory products, CXL-based MemoryAI servers, and full-stack AI infrastructure that boost GPU utilization and tackle context-size and latency limits.

The momentum is showing up: AI-driven business now tops 60% of H1 FY26 sales, integrated memory revenue up 53% YoY to $308M, and management raised FY26 guidance to 12% sales growth and $1.30 EPS. Demand is broadening from hyperscalers to enterprise, neocloud, and sovereign customers.

The risk is real: lumpy Advanced Computing revenue, customer concentration, tariff exposure in the LED segment, and a stock that’s already run hard (forward P/E ~37x). Some fair-value models actually flag downside from here.

A higher-quality, already-profitable AI infra play than $SLNH, but priced like the market knows it. Size accordingly.

NFA

2

737