I see, you're right. Could be that later DVD and BD player lack MPEG Multichannel decoding capabilities and there's some graceful degradation to 2.0 or in this case 1.0 audio?

7

sanjay dubey retweeted

Feb 13

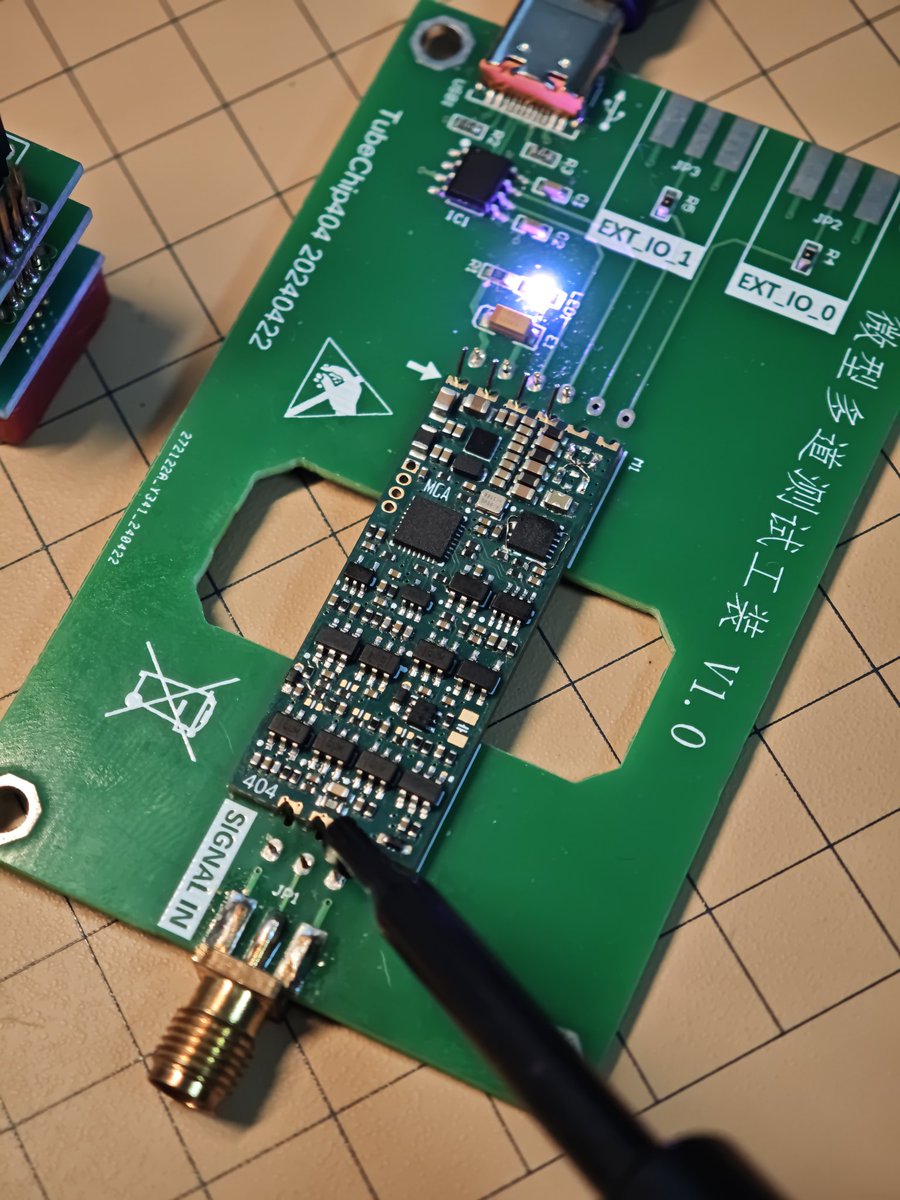

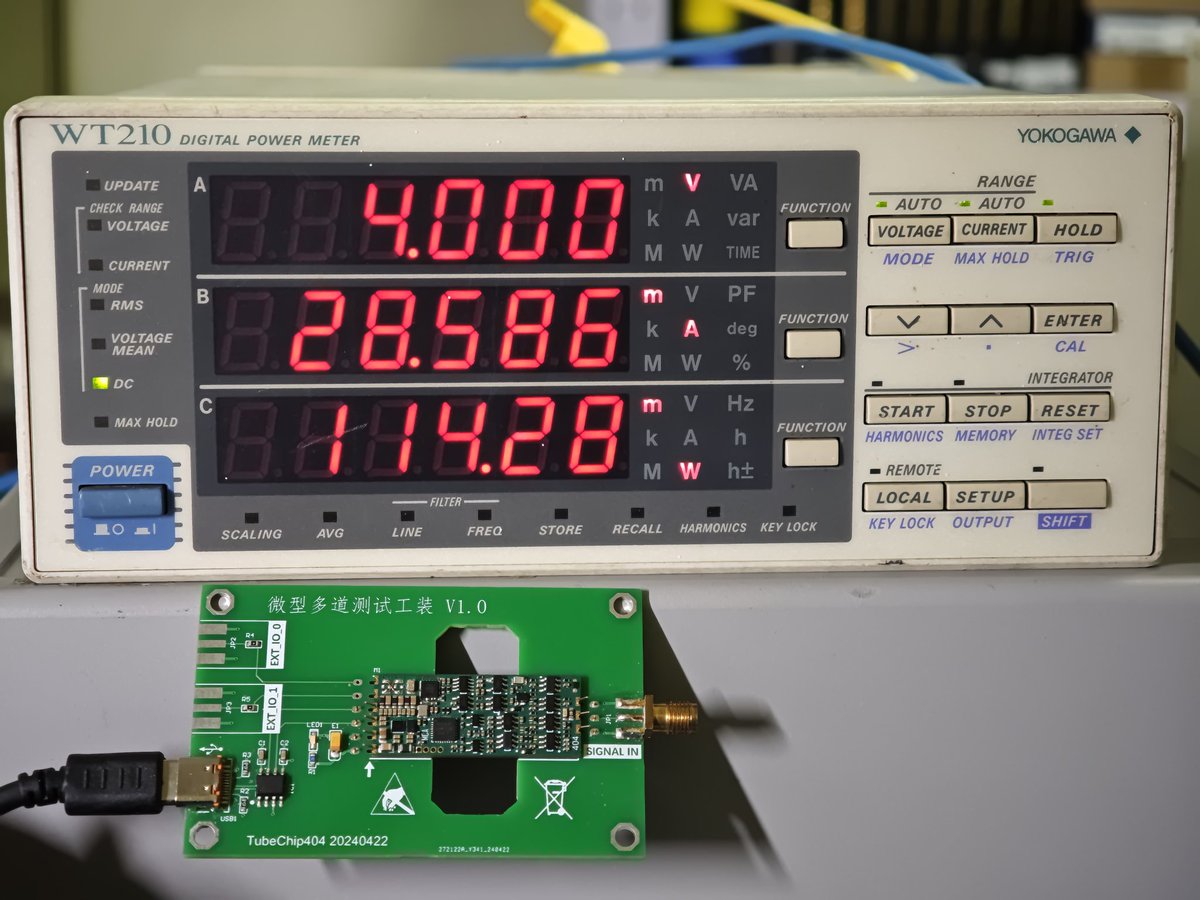

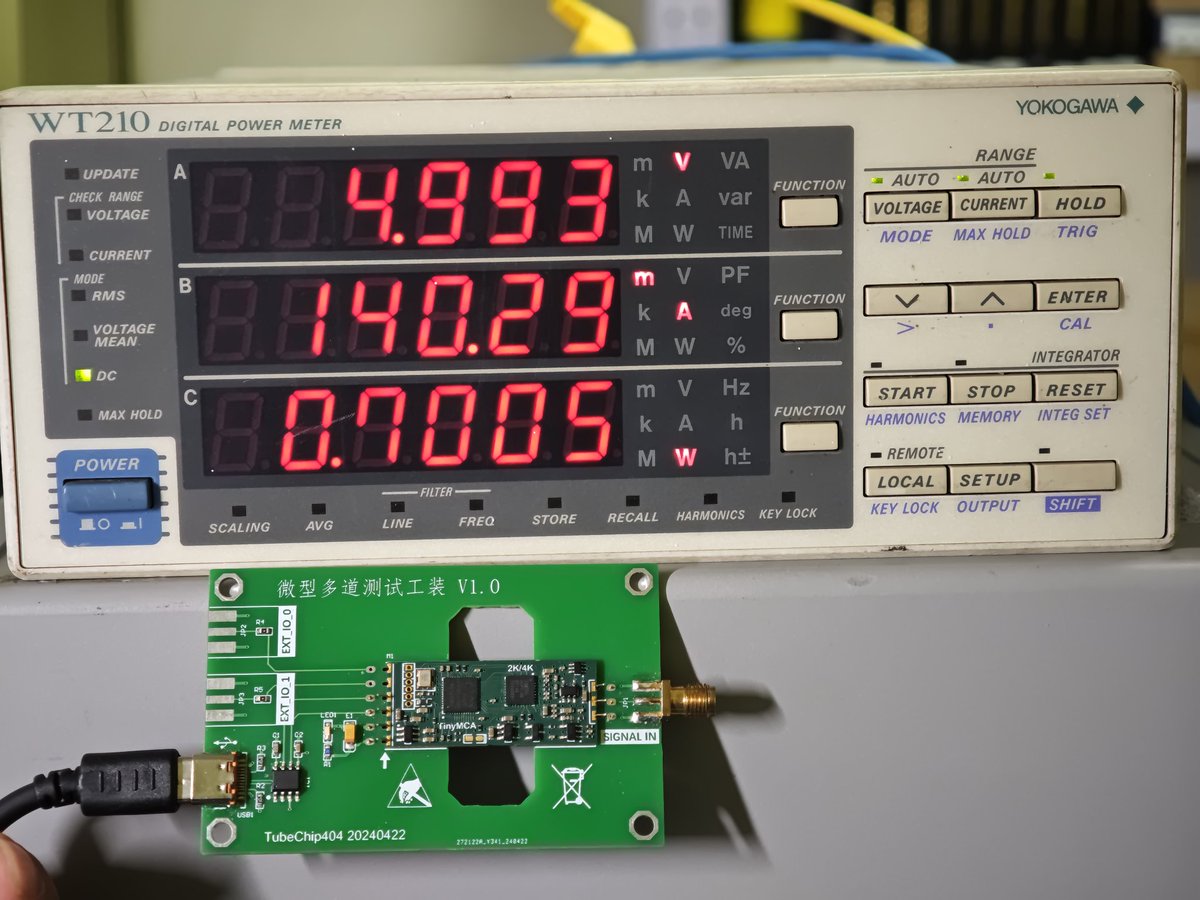

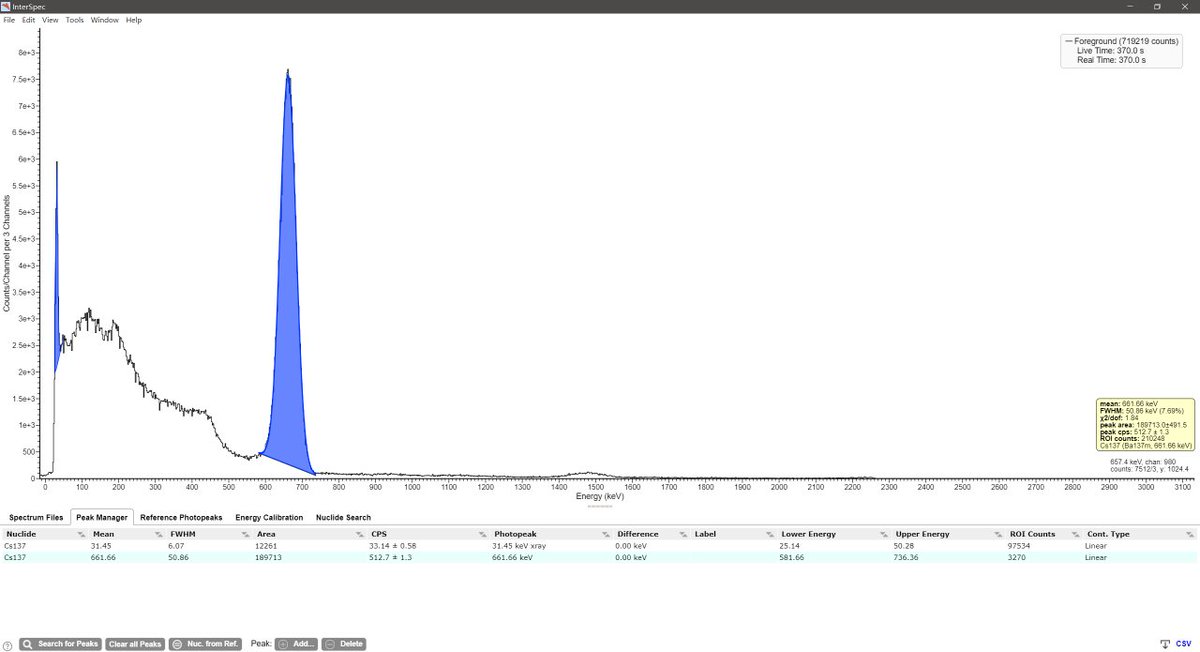

To reduce power consumption, I went back to building a multichannel analyzer based on analog circuitry. Compared to a digital multichannel analyzer of the same size, it consumes only one-sixth the power.

7

10

131

7,169

Part 1

Preliminary Evaluation of Metastable Dynamics in EEG Signals Using Hidden Markov Models and Block Permutation Surrogates

Abstract

This study evaluates the ability to detect stable dynamical states in electroencephalography (EEG) signals using a Hidden Markov Model (HMM) combined with a Block Permutation Surrogate testing framework. The results indicate that only a small subset of state trajectories survives a stringent surrogate test, suggesting the presence of highly stable dynamical structures within the data. However, because all analyzed datasets were derived from the same original EEG recording, the current findings primarily reflect the stability of the analytical pipeline rather than providing sufficient evidence for biologically generalizable metastable neural states.

1. Background and Methods

The analyses were conducted on multichannel EEG data using a Gaussian Hidden Markov Model. The optimal number of hidden states was automatically selected using the Bayesian Information Criterion (BIC). After state inference, trajectories with sufficiently long dwell times were extracted and evaluated using a composite metric designed to reflect state stability, model confidence, and persistence.

To assess the statistical significance of the detected trajectories, a Block Permutation Surrogate approach was employed. Unlike complete random shuffling, this method preserves local state-sequence structure while disrupting long-range temporal dependencies. As a result, the surrogate test is more conservative and reduces the risk of overestimating metastability in the data.

2. Main Results

In the representative analysis of EEG(43), the HMM consistently identified an optimal model with Best K = 8 across multiple initialization seeds.

A total of 45 state trajectories were detected, of which only 10 survived the significance threshold (p < 0.05) when compared against the surrogate distribution. These significant trajectories exhibited several notable characteristics:

Relatively long durations (mean ≈ 449 samples).

Extremely low posterior entropy (mean ≈ 0.0152), indicating high confidence in state assignment.

High H_norm values (mean ≈ 0.89), reflecting strong agreement between the observed data and the corresponding state model.

High and stable verification scores (V-scores).

Notably, 8 of the 10 statistically significant trajectories belonged to the same latent state, labeled State 6 in the corresponding model fit. This finding suggests that this state plays a prominent role in the dynamical organization identified by the model.

3. Discussion

The observed results are consistent with the hypothesis that highly stable dynamical structures exist within the recorded EEG signal. The fact that only a small proportion of trajectories survived the stringent surrogate test suggests that most stable intervals can be explained by the background statistical structure of the data, whereas only a limited subset exhibits stability beyond that expected under the surrogate model.

A particularly noteworthy finding is the concentration of significant trajectories within a single latent state (State 6). This state is characterized by long dwell times, low posterior entropy, and high model fit. Collectively, these properties make State 6 a compelling candidate for a stable dynamical structure within the analyzed data.

However, it is important to emphasize that HMMs identify latent statistical states rather than directly revealing physiological brain states. Because no advanced analyses such as phase-space reconstruction, attractor topology characterization, or basin-of-attraction analysis were performed, there is currently insufficient evidence to conclude that State 6 represents a genuine neural attractor. A more appropriate interpretation is that State 6 exhibits properties consistent with a candidate dynamical attractor.

1

18

The OSD seems to suggest it's mono though - hence me asking if many/any MPEG multichannel audio (i.e. not mono or stereo) discs were released.

1

1

5

Inventory chaos killing your margins? Sebastiaan Debrouwer on automation that forecasts, reorders, & syncs multichannel—prevent stockouts forever. Essential for scaling. Open Podcast Episode ecommercecoffeebreak.com/inv…

1

Spectrum-Analyzer Software Toolkit Adds Free Multichannel I/Q Analysis mwrf.com/technologies/test-m…

2

Make more video about the hardware and less the soft. it the most complex part since there is so much type of computer and different way to compute (ARM x86, new devices, multichannel...)

102

Outputs of the two systems are measured by pulse timing circuit and resistance bridge followed by simple analogue computer which feeds multichannel recorder.

20

14h

Oh what other sources? I like the idea of intent selling. Leadpoet does something similar and it’s multichannel. But I think I like your entire stack (from this presentation)

1

9

Viajero Impenitente retweeted

Jun 13

Immediate alerts matter when systems fail.

This guide shows how to build multichannel monitoring with SMS, WhatsApp, and Slack using #InfluxDB 3's embedded Python engine.

No external orchestration needed! bit.ly/4kbGTzg via @thenewstack

1

4

495

Some Euro players had an MPEG Multichannel logo on their faces while I've never seen that logo on any US decks.

1

1

22

$BRZE

-36% YTD.

Don’t miss the next $CRM.

Almost nobody is focused on the software layer that actually activates AI inside enterprises.

That’s where $BRZE sits.

Braze is a leading customer engagement platform built for real-time, personalized, multichannel marketing across email, push, SMS, in-app messaging, WhatsApp, and more — all powered by first-party data and increasingly AI-driven decisioning.

Think of it like this:

$CRM stores the customer.

$BRZE activates the customer.

At a ~$2.4B market cap, Braze is still being priced like a mid-tier marketing tool.

But the business is behaving like a high-growth, mission-critical engagement infrastructure platform.

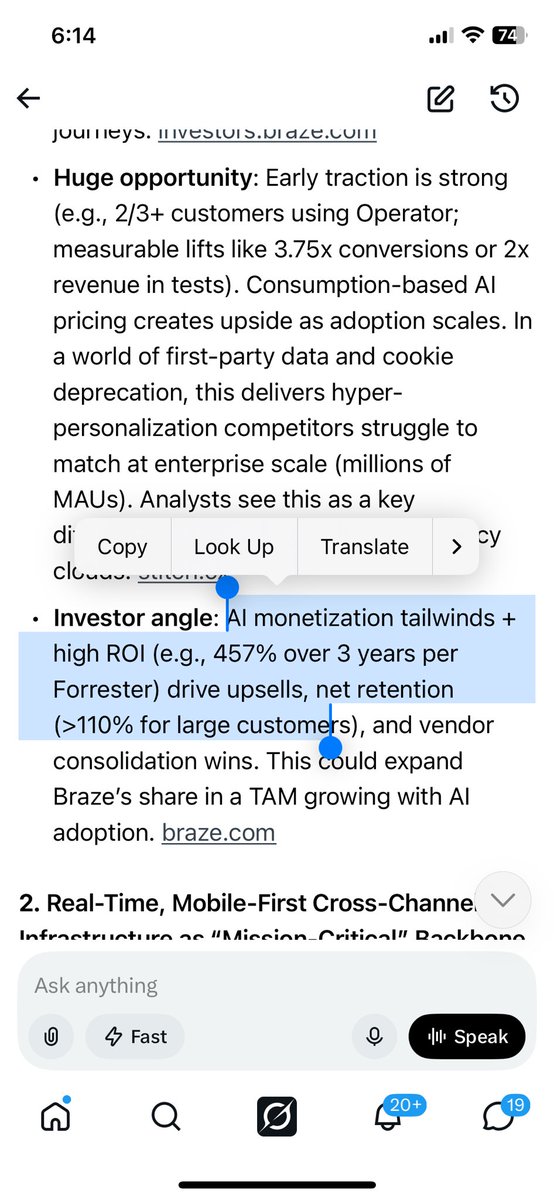

📝The numbers:

~$2.4B market cap

~$787M TTM revenue

~$895–899M FY27 revenue guidance

~$1.08B RPO (contracted backlog)

~93% recurring revenue

~2,713 customers globally

110% DBNR

349 customers >$500K ARR ( 35% YoY)

Q1 FY2027 alone:

→ $211M revenue ( 30.2% YoY)

→ ~27% organic growth

→ $27M free cash flow ( 54% YoY)

→ Record large customer expansion

And importantly:

Braze has now posted four consecutive quarters of organic revenue acceleration.

THIS IS HUGE.

In enterprise SaaS, that usually signals something changing in the underlying demand curve.

It’s designed to sit at the center of the modern enterprise stack.

Key integrations span the entire data AI ecosystem:

☁️ Cloud & Data Platforms

AWS, Snowflake (including Cortex AI), Databricks

📊 CDPs & Data Activation

Segment, mParticle, Amplitude, Hightouch, Census, Tealium, RudderStack

📈 Analytics Layer

Mixpanel, Contentsquare, Snowplow

🛒 Commerce Layer

$SHOP deepened personalization commerce journeys)

🤖 AI / Content Systems

Jasper, $GOOG Gemini, Bedrock-compatible LLMs, OpenAI/Anthropic integrations via agent framework

📡 Activation & Growth Tools

Meta, Lob, Jampp, Remerge, referral lifecycle tooling via Braze Alloys ecosystem

What this really means:

Braze is becoming the “activation layer” between data warehouses, AI models, and customer-facing channels.

It doesn’t replace $CRM , $SNOW , or CDPs.

It connects them.

This is where the narrative starts shifting from “marketing software” to “AI engagement infrastructure.”

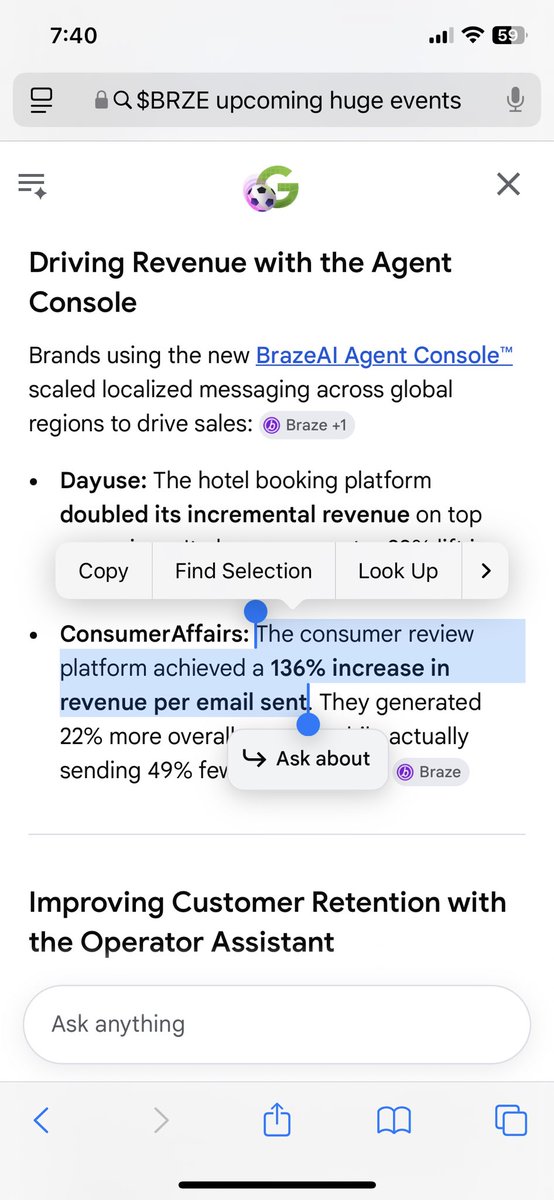

BrazeAI is not a single feature — it’s a suite of agentic systems:

🤖 BrazeAI Decisioning Studio™

→ Optimizes message, timing, channel, and offer using reinforcement learning

🤖 BrazeAI Operator™

→ Natural language campaign building analytics execution

🤖 BrazeAI Agent Console™

→ Custom AI agents that can autonomously run customer engagement workflows

🤖 Content Optimizer MCP Server

→ Connects external AI tools (Claude, Bedrock, etc.) directly into Braze workflows

The direction is clear:

Marketers move from manually building campaigns → to supervising AI agents that run customer engagement in real time.

And this is already showing up in the numbers:

→ 30% revenue growth

→ Expanding large customers ( 35% YoY >$500K ARR)

→ 110% retention

→ Rising FCF generation

→ Strong enterprise adoption of AI features

Now zoom out to the peer group:

$CRM → ~$150B market cap, slower growth, platform incumbent

$HUBS → ~$10B, solid but lower growth

$TWLO → ~$30B, communications layer

$BRZE → ~$2.4B, growing ~30%

That’s the disconnect.

Braze is posting top-tier SaaS growth while trading at ~3.1x sales and ~2.6x forward sales — often below peers growing slower.

This is where the asymmetry starts to matter.

On top of that:

→ $1.08B backlog visibility

→ 93% recurring revenue base

→ Improving profitability FCF

→ $100M buyback authorization

Management is not behaving like a company in distress.

They are behaving like a company with long-term confidence in intrinsic value.

Every enterprise now needs to answer the same question:

How do we communicate with millions of customers in real time, across every channel, with personalization?

That is exactly what Braze was built for.

The market is still pricing it as a marketing SaaS vendor.

10

5

34

1,735

Yes, this was MPEG Multichannel. Philips had negotiated that PAL DVD discs should have that, but the Hollywood studios wanted to stick with Dolby Digital worldwide, and that's how things ended up.

2

1

26

Are any of the MPEG releases multichannel? (i.e. not mono or stereo?)

1

15

Outreach shouldn't stop when you clock out. 🚀

Meet Stan: your AI Employee that manages multichannel conversations while YOU’re at the beach.

More replies. More booked calls. Less “stuck to your phone.”

Join us: marblism.com/?via=mypersonal…

#Ai

7

Jun 13

Thank you to @Independent_ie and @MediahuisIRL for the invitation to last Thursdays local voices national reach event hosted by @MaryERegan highlighting the importance of trusted journalism, effective marketing and multichannel communications for businesses in Ireland 💻📰🗞️

59

Jun 13

📊 Sales Stat — The five priority sales skills for 2026: discovery & qualification, objection handling, negotiation & closing, multichannel prospecting, and consultative selling. (Gartner / Pitchbase, 2026) — The skills that close haven't changed. #B2BSales

1

🇺🇸🇺🇸 Brad 🇺🇲🇺🇲🐕🏖 retweeted

Jun 13

These are built as interdimensional multichannel picture frames if you know how 🤔 to turn them on .

I dont think anyone has shown these people where the remote 🤔 control is kept.....

1

1

50