Jun 16

من يبحث عن اكبر العرووض⎐كُـود⎐كوبِون⎐خـِصم⎐والمفاجات كل ماتبحثو عنها من اقوى التخفيـ ضااات

ايهرب⊴ ايهيرب⊴ GCA5893

❮نون❯ S3Q

⎐نمشي⎐ AABN

❮⊴تيمو ⊴❯ TEB72

⎐وايـتس ❯ A102

▬المطار▬ M24

الياقه⎐وقت⎐اللياقة ❯ F99

___

oPVC

1

Massage in juffair gate hotel

massage in bahrain

bahrain body

bahrain to

bahrain body

⛓️wa.me/447886722592🥈

#bahrain

#manama

#juffair

opvc

1

69

Jun 12

今日の配信のソロランクやるとしたら、OPVCでキモオタも良いけど

何かの報告の最後に 広辞苑参照って言っとけば

何とかなる説で検証してみようかな

頭のネジなんて外れすぎてるから、もはや人類には早すぎる領域とポジティブに思ってやっとこ

1

158

Jun 11

🚨 Registration is officially open for OPVC classes! 🚨

🔗ohiopremiervc.com/youth-clas…

#opvcc #ohiopremiervc #volleyball #youthvolleyball

16

Jun 1

人見知りなんで初見全然喋らんと思いますが

めちゃくちゃ頑張って直そうとしてます

手始めに野良のopvcは付けて報告はしまくってますᐢ. ̫. ᐢ

14

589

May 27

今日ちょっとだけエペしたけど

野良さん2人でopvcで楽しそうに

話しながらしてたけどそーゆー時に

自分下手 コミュ障でて一切絡めないという辛み😢😢

だれかフレンドなってよ、、😇

#apex募集 #apexフレンド募集中

2

219

May 23

3番過ぎてアモアス、アヒル人狼などのopvcに声が入りません

May 23

【声の8タイプ】

実際は複数の要素があります

(ハスキー×甘い声etc)

⬇声の特徴まとめへ

ALT ① ハスキー 息っぽさやザラつきがある声。色気・雰囲気が出やすい。 代表例:Ado、椎名林檎 ② クリア 輪郭がはっきりしていて聞き取りやすい声。配信・ナレーション向き。 代表例:天海祐希、宇多田ヒカル ③ ウィスパー 囁くような息多めの声。ASMR・深夜配信系で強い。 代表例:Cocco、yama ④ 鼻声系(ナザル) 鼻にかかる成分が強め。特徴が出やすく、刺さる人にはかなり刺さる。 代表例:あいみょん、山寺宏一 ⑤ 低音系 落ち着き・安心感・大人感がある。雑談やラジオ向き。 代表例:大塚明夫、GACKT ⑥ 高音系 明るい・若い・可愛い印象になりやすい。アニメ声寄りもここ。 代表例:西野カナ、花澤香菜 ⑦ 中性的 男女どちらにも聞こえる系。V系・ボカロ系と相性いい。 代表例:HYDE、まふまふ ⑧ 甘い声 柔らかくて距離感近め。恋愛系・雑談配信と相性が良い。 代表例:石田彰、佐倉綾音

1

10

1,260

May 23

India’s OPVC Revolution 🇮🇳💧

Propipes is driving indigenous OPVC machinery development in India with advanced extrusion, orientation & automated socketing technology. Stronger, lighter & sustainable PVC-O pipes are shaping the future of water infrastructure. #OPVC #MakeInIndia

1

1

15

223

May 21

𝗪𝗲𝗹𝘀𝗽𝘂𝗻 𝗖𝗼𝗿𝗽 𝗟𝘁𝗱 𝗗𝗲𝗹𝗶𝘃𝗲𝗿𝘀 𝗦𝘁𝗿𝗼𝗻𝗴 𝗙𝗬26 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲 & 𝗦𝗲𝘁𝘀 𝗔𝗺𝗯𝗶𝘁𝗶𝗼𝘂𝘀 𝗙𝗬27 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲 🚀:

Welspun Corp Ltd (WCL), the flagship company of Welspun World, announced its consolidated financial results for the fiscal year ended March 31, 2026, showcasing a robust performance that surpassed its guidance and a healthy financial position.

𝗞𝗲𝘆 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀:

- 𝗙𝗬26 𝗘𝗕𝗜𝗧𝗗𝗔: Reached ₹2,371 crore, exceeding the guidance of ₹2,200 crore, with an EBITDA margin of 14% and ROCE at 22%.

- 𝗡𝗲𝘁 𝗖𝗮𝘀𝗵 𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻: Strengthened to ₹1,627 crore, demonstrating effective financial management despite significant capex investment of ₹2,532 crore during the year. The company maintained a negative net working capital, supported by customer advances.

- 𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄 𝗚𝗲𝗻𝗲𝗿𝗮𝘁𝗶𝗼𝗻: Operating Cash Flow (OCF) and Free Cash Flow (FCF) saw significant improvements, reaching ₹3,204 crore and ₹672 crore respectively for FY26.

- 𝗣𝗿𝗼𝗳𝗶𝘁 𝗔𝗳𝘁𝗲𝗿 𝗧𝗮𝘅 (𝗣𝗔𝗧): For FY26, PAT after exceptional items increased by 42% YoY to ₹1,613 crore. For Q4 FY26, PAT grew 28% YoY to ₹370 crore.

𝗥𝗼𝗯𝘂𝘀𝘁 𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸 & 𝗙𝘂𝘁𝘂𝗿𝗲 𝗢𝘂𝘁𝗹𝗼𝗼𝗸:

- 𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸: WCL maintained an all-time high consolidated order book of approximately ₹25,350 crore, encompassing line pipes (India & USA), ductile iron pipes, and stainless steel bars & pipes. Notably, the USA spiral mill's orders extend through FY28.

- 𝗙𝗬27 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲: The company has set ambitious targets for FY27, projecting revenue of ₹20,000 crore and EBITDA of ₹2,850 crore, representing a 19% and 20% growth respectively over FY26 actuals.

𝗦𝗵𝗮𝗿𝗲𝗵𝗼𝗹𝗱𝗲𝗿 𝗥𝗲𝘁𝘂𝗿𝗻𝘀:

- 𝗗𝗶𝘃𝗶𝗱𝗲𝗻𝗱: The Board has recommended a dividend of ₹5 per equity share (100%) of the face value of ₹5 each.

𝗠𝗮𝗿𝗸𝗲𝘁 𝗘𝗻𝘃𝗶𝗿𝗼𝗻𝗺𝗲𝗻𝘁 & 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗔𝗱𝘃𝗮𝗻𝘁𝗮𝗴𝗲𝘀:

- 𝗚𝗹𝗼𝗯𝗮𝗹 𝗗𝗲𝗺𝗮𝗻𝗱: Higher oil prices and a renewed focus on energy security are expected to drive new investments in global line pipe projects. WCL's strategic global presence across key regions (USA, KSA, India) and strong execution capabilities provide a competitive edge.

▸ 𝗨𝗦𝗔: Strong multi-year demand visibility driven by LNG, AI data centers, and oil pipeline infrastructure.

▸ 𝗞𝗦𝗔: Significant investments in onshore/offshore fields, Hydrogen & CCUS ventures, and water infrastructure projects.

▸ 𝗜𝗻𝗱𝗶𝗮: Robust export prospects complemented by domestic demand from O&G pipelines (PNG, LPG) & water infrastructure projects.

- 𝗔𝘀𝘀𝗼𝗰𝗶𝗮𝘁𝗲 & 𝗦𝘂𝗯𝘀𝗶𝗱𝗶𝗮𝗿𝘆 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

▸ East Pipes Integrated Company (KSA) achieved its highest-ever profitability and margin performance.

▸ Welspun Specialty Solutions Ltd (WSSL) reported 52% YoY EBITDA growth, focusing on value-added products.

▸ Sintex is focusing on premiumisation and channel expansion, with OPVC pipes gaining traction.

Mr. Vipul Mathur, MD & CEO, highlighted the strong operational and financial performance, the robust order book providing medium- to long-term visibility, and the competitive advantage derived from WCL's global presence and execution capabilities in the evolving global landscape. He also emphasized the integration of sustainability across the business, reflected in improved ESG rankings. 🌟

𝗔𝗯𝗼𝘂𝘁 𝗪𝗲𝗹𝘀𝗽𝘂𝗻 𝗖𝗼𝗿𝗽 𝗟𝘁𝗱:

WCL is a global leader in manufacturing large diameter line pipes, ductile iron pipes, stainless steel products, and water storage tanks (Sintex). The company serves customers across six continents with manufacturing facilities in India, the USA, and Saudi Arabia. WCL is recognized for its commitment to sustainable growth, ranking high globally and in India for its ESG performance. 🌍

📊 WELSPUN CORP LTD | 🏷️ Press Release / Media Release

🌐 Details: wegro.app/0lir7n

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

2

421

May 18

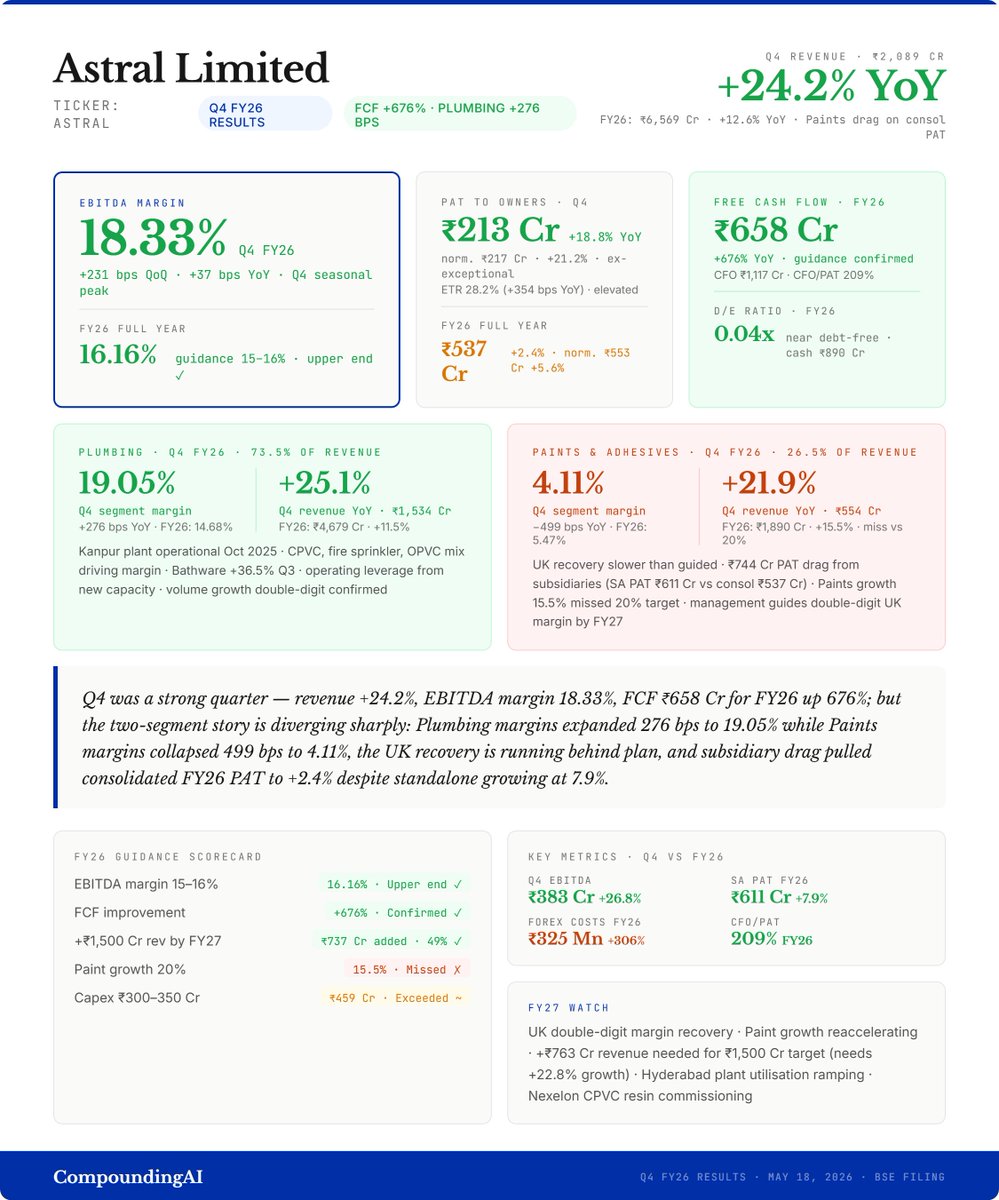

Stop scrolling, log in to CompoundingAI !

Astral Limited (ASTRAL) - Q4 FY26 Results

Plumbing delivering. Paints dragging. Cash flow exceptional.

Q4 Numbers

Q4 revenue: ₹2,089 Cr, 24.2% YoY, 35.5% QoQ - strong seasonal demand recovery exactly as management had guided.

Q4 EBITDA: ₹383 Cr, margin 18.33%, 37 bps YoY, 231 bps QoQ.

Q4 PAT to owners: ₹213 Cr, 18.8% YoY. Normalised Q4 PAT (ex-exceptional ECL provision): ₹217 Cr, 21.2% YoY.

FY26 Full Year

FY26 revenue: ₹6,569 Cr, 12.6% YoY. FY26 EBITDA margin: 16.16% - within and at the upper end of the 15–16% guidance.

FY26 PAT to owners: ₹537 Cr, 2.4% YoY reported. Normalised FY26 PAT: ₹553 Cr, 5.6% YoY - exceptional items (Labour Codes provision ₹165 Mn in Q3, ECL provision ₹61 Mn in Q4, goodwill impairment ₹41 Mn) suppressed the reported number.

Standalone PAT: ₹611 Cr, 7.9% - the ₹74 Cr gap to consolidated is entirely subsidiary drag, primarily UK.

The two-segment divergence

Plumbing (73.5% of Q4 revenue): Q4 revenue ₹1,534 Cr 25.1% YoY. Q4 segment margin 19.05%, 276 bps YoY. Operating leverage from Kanpur plant (operational Oct 2025), value-added product mix (CPVC, fire sprinkler, OPVC), and pricing discipline as polymer prices stabilise. FY26 Plumbing: ₹4,679 Cr 11.5%.

Paints & Adhesives (26.5% of Q4 revenue): Q4 revenue ₹554 Cr 21.9% YoY. Q4 segment margin 4.11%, −499 bps YoY. FY26 Paints margin: 5.47% vs 7.03% in FY25. UK recovery running slower than management's "substantially improved by FY26-end" guidance. FY26 Paints growth: 15.5% - missed the 20% target.

Cash - the standout

FY26 CFO: ₹1,117 Cr, CFO/PAT 209% - high earnings quality. FCF: ₹658 Cr, 676% YoY. Trade payables grew ₹341 Cr (favorable creditor financing) while receivables and inventory increases were moderate.

Capex: ₹459 Cr - exceeded the ₹300–350 Cr guidance range, driven by Al-Aziz acquisition, Nexelon CPVC resin plant, and facility upgrades. D/E: 0.04x. Cash balance: ₹890 Cr.

Exchange fluctuation losses were ₹325 Mn in FY26 vs ₹80 Mn in FY25 - forex volatility on UK/international subsidiary transactions is the finance cost to watch.

FY26 Guidance Scorecard

1) EBITDA margin 15–16% → 16.16% - Upper end met

2) FCF improvement → 676% - Confirmed

3) ₹1,500 Cr revenue by FY27 → ₹737 Cr added in FY26 - 49% of two-year target done

4) Paint growth 20% → 15.5% - Missed

5) Capex ₹300–350 Cr → ₹459 Cr - Exceeded

FY27 Watch

The ₹1,500 Cr cumulative revenue addition target needs ₹763 Cr more in FY27 - requiring 22.8% growth against FY26's 12.6%. That demands Paint segment acceleration and UK margin recovery. Management guides double-digit UK margin in FY27.

Hyderabad plant utilisation (15–20% currently) ramping adds operating leverage. Nexelon CPVC resin plant coming online provides backward integration for Plumbing margins. Forex cost drag (₹325 Mn FY26) needs stabilising.

Note: This is not investment advice.

1

5

1,241

May 17

野良が打って来たから

opvcで言ってんのに

言い返せてこないなら

挑発行為してくんなよ😅😅😅

怖すぎるって挑発行為してくるくせに、喋れんやつ😩

6

327

🚨Top 10 land allotments by BIADA from January to May 5, 2026

UltraTech Cement Ltd

Katoria, Banka | Cement

Area: 59.47 acres

Nirani Sugars Ltd

Banmankhi, Purnea |Citric Acid Monohydrate Manufacturing

Area: 52.04 acres

Green Excel Pvt Ltd

Lohat, Madhubani | E-waste & Recycling

Area: 12.77 acres

SSIL Paint Industries

Sasaram, Rohtas | Paints & Varnishes

Area: 10.85 acres

HR Food Processing

Dumaria, Muzaffarpur | Bio-Plastics

Area: 7.15 acres

Sada Industries LLP

IGC Begusarai | OPVC Pipes

Area: 6 acres

CF Biotec Gujarat

Bariyarpur, Muzaffarpur | Biogas Plant

Area: 5.45 acres

Shrinath Bio Fuels

Kumarbagh, West Champaran | CBG

Area: 5 acres

NIDL Surfactants

IGC Begusarai | Sulphuric Acid & LABSA

Area: 4.93 acres

Ishika Paper & Packaging

Bihiya, Bhojpur | Corrugated Boxes

Area: 3.28 acres

3

18

163

7,299

May 15

BirlaNu Ltd Concall Summary for Q4FY26

🔹 MANAGEMENT COMMENTARY

• FY26 described landmark year

• HIL transitioned into Birlanu

• Portfolio transformation accelerated strongly

• Sustainable-building focus intensified

• Demand environment remained challenging

• Pricing pressure persisted across segments

• FY27 momentum remained encouraging

• Clean Coats integration prioritized

🔹 FY27 OUTLOOK

• Portfolio doubling targeted long term

• BCG benefits expected from FY27

• Double-digit EBITDA margins targeted

• Billion-dollar revenue aspiration maintained

• Jal Jeevan spending recovering gradually

• Rural roofing demand remained resilient

• Product-mix optimization continuing actively

• Infrastructure recovery green shoots visible

🔹 INDUSTRY TRENDS

• Competitive intensity remained elevated

• Middle-East tensions impacted logistics

• Energy costs remained volatile

• Resin prices fluctuated sharply

• PVC prices spiked 60% March

• Rupee depreciation impacted roofing margins

• Steel prices created substitution opportunity

• Infrastructure demand gradually improving

🔹 COMPETITIVE POSITIONING

• Roofing leadership maintained strongly

• Pricing premium sustained successfully

• Innovation engine remained differentiator

• Pipe portfolio exceeded 3,000 SKUs

• Premium Parador positioning maintained

• Germany-made branding emphasized quality

• Product-range breadth remained competitive

🔹 RISKS & CONCERNS

• Parador demand remained weak Europe

• Q4 Parador loss ₹35 crore

• Impairment booked ₹74 crore

• Debt increased to ₹851 crore

• December debt peak ₹929 crore

• Employee costs increased materially

• Severance costs impacted profitability

• Currency fluctuations remained monitorable

🔹 GROWTH DRIVERS

• Clean Coats acquisition completed

• Construction chemicals portfolio expanded

• Nellore boards plant progressing

• Patna OPVC facility commissioned

• BCG-led efficiency program ongoing

• Sales acceleration initiatives implemented

• Operational excellence focus intensified

🔹 PRODUCT MIX TRENDS

• Construction chemicals grew 58%

• Annual revenue crossed ₹100 crore

• Boards, panels growth remained strong

• Designer boards gaining traction

• Premium HD boards scaling steadily

• Pipes mix shifted premium

• CPVC share reached ~40%

• OPVC demand improving gradually

🔹 FINANCIAL HIGHLIGHTS

• FY26 revenue ₹3,730 crore

• Revenue growth 3% YoY

• Q4 revenue ₹1,080 crore

• Q4 growth 9% YoY

• Standalone EBITDA growth 39%

• Q4 margins expanded 380bps

• Debt stood ₹851 crore

• Asset monetization gain ₹47 crore

🔹 KEY TAKEAWAYS

• India business momentum remained strong

• Construction chemicals scaling rapidly

• Margin recovery improving steadily

• Parador remained key overhang

• Portfolio transformation accelerating

• Debt levels remain monitorable

• BCG initiatives key catalyst

• Long-term outlook remained positive

#BirlaNu

2

3

336

Strengthening Bihar’s Manufacturing Future

BIADA is enabling growth across emerging sectors like OPVC Pipes & Fittings Manufacturing, paving the way for innovation-driven industrial development in the state.

Sada Industries LLP is setting up a state-of-the-art manufacturing unit at IGC Begusarai for OPVC Pipes & Fittings. The project marks a significant boost to Bihar’s manufacturing ecosystem by strengthening industrial infrastructure, generating employment opportunities and accelerating economic growth in the state.

#BiharHaiTaiyar

🚨उद्योग और रोजगार के क्षेत्र में रफ्तार पकड़ता बिहार!

#BuildAndBelieveInBihar

@PMOIndia @PiyushGoyal @CimGOI @GovernorBihar @samrat4bjp @officecmbihar @Office_Shreyasi @kundan_ias @PTI_News @ddnewsBihar @PIB_India @DoC_GoI @investindia @BiharIndustries @BiharCabinet @ficci_india @bimcgl @BSPCBOfficial @idabihar @startup_bihar @DM_Begusarai @IPRDBihar

12

58

1,912

Company: Chemfab Alkalis

Update Type: Investor Presentation

Summary: FY27 triggers: Modernized plant, hybrid power (May-2026), 20,000 TPA OPVC capacity. JJM revival from Q2. Stronger profitability expected; OPVC target ₹1,000cr by FY29.

📁Details: bseindia.com/stockinfo/AnnPd…

2

847