Recently, I made some purchases from the Co-optex store in Pune and was pleasantly surprised to see they have started including a small intro about the weaver who has taken so much effort to weave this beautiful piece of elegance.

Such little details are so heart warming. I have become a life long customer of Co-optex!

#SareeTwitter

3

1

8

232

From #CTAN:

Petr Olšák submitted an update to the OpTeX bundle.

Version: 1.20

License: pd

Summary description: LuaTeX format based on Plain TeX and OPmac

ctan.org/pkg/optex

#TeXLaTeX

3

118

May 22

தந்தை பெரியார் மற்றும் அறிஞர் அண்ணா அவர்களின் பிறந்த நாளைப் போற்றிடும் வகையில் 1993-ம் ஆண்டு co - optex செய்த விளம்பரம் @cooptexindia

1

12

561

May 20

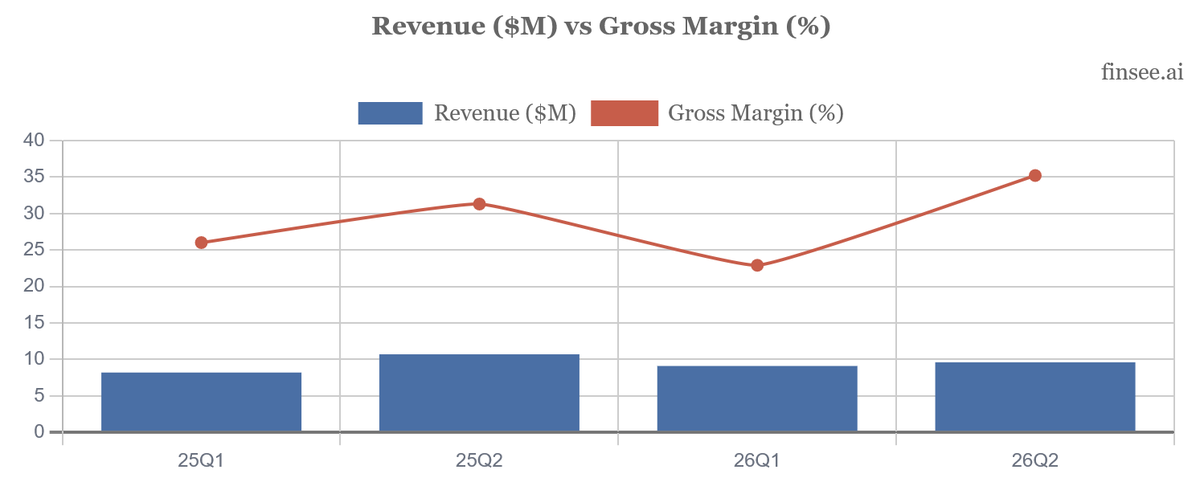

$OPXS Q2 2026 earnings: Margin inflection arrives, but top-line growth pauses on DC gridlock

Optex Systems delivered a mixed Q2, highlighted by a massive structural improvement in profitability despite a 10% YoY revenue contraction. The long-awaited burn-off of legacy fixed-price periscope contracts finally materialized, driving gross margins to a robust 35.2% (up from 31.3% a year ago). However, revenue decelerated to $9.6M as the federal government shutdown and delayed appropriations pushed contract awards into H2. Despite the top-line miss, management reiterated its full-year guidance of $43-$45M in revenue, implying a steep acceleration in the back half of the year backed by a healthy $36.6M backlog.

Full article with charts - link in bio

🐂 𝗕𝘂𝗹𝗹 𝗖𝗮𝘀𝗲

𝗠𝗮𝗿𝗴𝗶𝗻 𝗦𝘁𝗼𝗿𝘆 𝗩𝗮𝗹𝗶𝗱𝗮𝘁𝗲𝗱: The long-telegraphed margin expansion has arrived. By completing legacy loss-making 2020 periscope contracts, Q2 gross margin surged 390 bps YoY to 35.2%, proving the company's core Abrams/Bradley/Stryker component business is highly profitable under current pricing.

𝗛𝟮 𝗦𝗽𝗿𝗶𝗻𝗴-𝗟𝗼𝗮𝗱𝗲𝗱 𝗳𝗼𝗿 𝗚𝗿𝗼𝘄𝘁𝗵: H1 revenue was flat YoY entirely due to macro government delays. With $36.6M in backlog and appropriations now cleared, H2 is mathematically set up for significant acceleration to hit the $43-$45M full-year target.

🐻 𝗕𝗲𝗮𝗿 𝗖𝗮𝘀𝗲

𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄 𝗮𝗻𝗱 𝗢𝗽𝗘𝘅 𝗥𝗲𝗱 𝗙𝗹𝗮𝗴𝘀: While net income was positive, operating cash flow reversed to a negative $1.3M in H1 due to aggressive inventory builds. Simultaneously, operating expenses exploded 54% YoY in Q2, chewing into the newly gained gross profit.

𝗥𝗲𝗹𝗶𝗮𝗻𝗰𝗲 𝗼𝗻 𝗧𝗶𝗺𝗶𝗻𝗴: The company is highly exposed to U.S. government budget dysfunction. Lumpy contract awards create quarter-to-quarter volatility that obscures underlying business health and stresses working capital.

⚖️ 𝗩𝗲𝗿𝗱𝗶𝗰𝘁

⚪ Neutral to Bullish. The structural gross margin improvement is the most important takeaway, proving the business model works when not burdened by pre-inflation contracts. If the government orders normalize in H2 as guided, earnings will inflect sharply higher.

— • — • —

𝗧𝗵𝗲𝗺𝗲𝘀

🟢 𝗧𝗵𝗲 𝗟𝗲𝗴𝗮𝗰𝘆 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁 𝗔𝗹𝗯𝗮𝘁𝗿𝗼𝘀𝘀 𝗶𝘀 𝗟𝗶𝗳𝘁𝗲𝗱

Gross margin accelerated dramatically to 35.2% in Q2, up from 22.9% just a quarter prior. This is a direct result of completing firm-fixed-price periscope contracts signed in 2020. As the mix shifts entirely to newly priced programs, the company is demonstrating substantial operating leverage within its manufacturing base.

New: 🔴 𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄 𝗗𝗲𝗰𝗼𝘂𝗽𝗹𝗲𝘀 𝗳𝗿𝗼𝗺 𝗡𝗲𝘁 𝗜𝗻𝗰𝗼𝗺𝗲

A notable red flag emerged in the cash flow statement. Despite reporting $1.6M in net income for H1, Operating Cash Flow reversed from $4.0M last year to -$1.3M this year. Management attributes this to purchasing inventory ahead of expected H2 revenue acceleration. While plausible, building working capital during a period of delayed government orders carries inventory risk if those awards slip further right.

New: 🔴 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗘𝘅𝗽𝗲𝗻𝘀𝗲𝘀 𝗦𝘂𝗿𝗴𝗶𝗻𝗴

The gross margin gains were heavily muted by an aggressive deceleration in cost control. Operating expenses surged by $600K ( 54% YoY) to $1.7M in Q2. Drivers included severance/transition costs for new CEO Chad George, higher stock compensation, and increased R&D. Management explicitly warned these expenses will 'remain elevated' due to ongoing Cybersecurity Maturity Model Certification (CMMC) mandates.

New: 🟢 𝗕𝗮𝗰𝗸𝗹𝗼𝗴 𝗦𝗲𝗰𝘂𝗿𝗲𝘀 𝗛𝟮 𝗔𝗰𝗰𝗲𝗹𝗲𝗿𝗮𝘁𝗶𝗼𝗻

Despite the Q2 top-line miss, the company booked $16.3M in new orders in H1 ( 3.8% YoY). The ending backlog of $36.6M provides deep visibility. To hit the midpoint of FY26 revenue guidance ($44M), Optex needs to generate $25.2M in H2, implying a ~12.5% YoY growth rate over H2 FY25. With appropriations passed in February, the table is set for rapid execution.

🔴 𝗠𝗮𝗰𝗿𝗼: 𝗪𝗮𝘀𝗵𝗶𝗻𝗴𝘁𝗼𝗻 𝗚𝗿𝗶𝗱𝗹𝗼𝗰𝗸 𝗣𝘂𝗻𝗶𝘀𝗵𝗲𝘀 𝗦𝘂𝗽𝗽𝗹𝘆 𝗖𝗵𝗮𝗶𝗻

The defense procurement cycle was paralyzed by the U.S. government shutdown (Oct-Nov) and continuing resolutions through January 2026. This created a vacuum in Q2 revenue as expected contract awards stalled. While defense spending remains robust structurally, the political mechanics of funding are injecting severe lumpiness into Optex's quarterly cadence.

⚪ 𝗤𝘂𝗶𝗲𝘁 𝗼𝗻 𝗖𝗼𝗺𝗺𝗲𝗿𝗰𝗶𝗮𝗹 𝗩𝗲𝗻𝘁𝘂𝗿𝗲𝘀

Notably absent from this quarter's commentary was any mention of the 'Speedtracker' or 'Reacher' commercial product lines, which were impaired by $804K in late FY25. The new leadership team appears to be refocusing entirely on the core, high-barrier military optics business (Abrams, Stryker, Bradley).

— • — • —

𝗢𝘁𝗵𝗲𝗿 𝗞𝗣𝗜𝘀

𝗛𝟭 𝗙𝗬𝟮𝟲 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗘𝗕𝗜𝗧𝗗𝗔: $𝟮.𝟳𝟲 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Decelerating. Down 22.6% YoY from $3.57M in the prior year. The decline is driven entirely by the drop in H1 revenue volumes and the sharp increase in transition and compliance-related operating expenses, masking the underlying gross margin improvements.

𝗪𝗼𝗿𝗸𝗶𝗻𝗴 𝗖𝗮𝗽𝗶𝘁𝗮𝗹: $𝟮𝟮.𝟲 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Stable and strengthening. Increased from $21.1M at the end of FY25. Supported by $4.2M in cash and absolutely zero debt on the revolving credit facility, providing an ample safety net to weather the delayed government funding cycle.

— • — • —

𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

𝗙𝗬𝟮𝟲 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: $𝟰𝟯.𝟬 - $𝟰𝟱.𝟬 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Accelerating vs current run-rate. H1 generated only $18.8M. To achieve the $44M midpoint, H2 revenue must reach $25.2M. Given the $36.6M backlog and the clearing of the federal appropriations bottleneck, achieving this target is highly likely, though it requires flawless supply chain execution.

𝗙𝗬𝟮𝟲 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗘𝗕𝗜𝗧𝗗𝗔: $𝟳.𝟱 - $𝟴.𝟱 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Stable. The $8.0M midpoint is exactly flat compared to FY25's actual $8.03M. This implies that while gross margins are improving materially, the gains are being fully absorbed by the structural increases in operating expenses (CMMC compliance, R&D, leadership changes) going forward.

— • — • —

𝗞𝗲𝘆 𝗤𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀

𝗢𝗽𝗘𝘅 𝗥𝘂𝗻-𝗥𝗮𝘁𝗲

You noted operating expenses will remain elevated due to CMMC and systems upgrades. What is the new normalized quarterly OpEx run-rate we should model once the leadership transition costs roll off?

𝗜𝗻𝘃𝗲𝗻𝘁𝗼𝗿𝘆 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝘆

Operating cash flow was negative as you built inventory for H2. If government awards slip again, how much of this inventory is at risk of obsolescence versus being standard components usable across multiple vehicle platforms?

𝗖𝗼𝗺𝗺𝗲𝗿𝗰𝗶𝗮𝗹 𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀 𝗨𝗽𝗱𝗮𝘁𝗲

There was no mention of the Speedtracker or Reacher product lines this quarter. Has the new leadership team decided to pivot away from the commercial market entirely following last year's impairment?

1

6

762

May 18

hard pass, thx though. Here is a comprehensive Due Diligence (DD) check on the X post regarding Syntec Optics Holdings, Inc. (NASDAQ: OPTX), cross-referenced against their latest Q1 2026 SEC filings and corporate disclosures.While the poster accurately lifts several metrics from recent PR headlines, they omit critical fundamental decay, capital structure risks, and paint an incredibly misleading picture of the company's real financial health.1. Company Profile CheckFirst, a point of clarification: $OPTX is Syntec Optics Holdings (based in Rochester, NY). It is frequently confused by retail investors on social media with $OPXS (Optex Systems Holdings), which is an entirely separate defense optics company. Syntec specializes in molded polymer optics and optical components for space, defense, and biomedical applications.2. Fact vs. Hype: Dissecting the Post's Claims🟢 What is Factually Accurate (Per Press Releases)The Production Run Rate: Syntec did put out a press release on May 4, 2026, stating that they quadrupled monthly production of space optics in March 2026 compared to March 2025.Q1 Shipping Volume: The company confirmed that by the end of Q1 2026, they shipped nearly 50% of their entire 2025 space product sales volume.Macro Projections: The references to Goldman Sachs ($108B satellite market by 2035) and Morgan Stanley ($1T space economy by 2040) are real macro studies explicitly quoted in Syntec’s own PR fluff.🔴 The Wrong, Highly Questionable, or Misleading Statements"Every single satellite that goes up needs what $OPTX makes"The Reality: This is completely false hyperbole. Syntec is a custom component manufacturer. While they provide polymer lenses for certain low Earth orbit (LEO) constellations, there is absolutely no public documentation or contract indicating they are a sole-source or universally required provider for Starlink, Amazon Kuiper, or AST SpaceMobile. The LEO space sector uses a mix of glass, polymer, and hybrid optical systems from dozens of global competitors (such as LightPath Technologies, $LPTH)."Sitting right in the middle of that compounding demand curve"The Reality: While the poster implies massive operational scale, Syntec’s total trailing twelve-month (TTM) revenue sits at an incredibly small $28.08 million. Space optics is a fast-growing segment for them internally, but it is currently a tiny sliver of a microcap's broader business.3. The Real DD: Critical Red Flags Omitted from the PostThe poster published this on May 17, 2026, completely ignoring the devastating Q1 2026 10-Q Financial Report filed just two days prior on May 15, 2026. The underlying fundamentals reveal severe operational stress:📉 Catastrophic Margin Compression & Revenue DeclineShrinking Revenue: Despite the "quadrupled space production," Syntec's total Q1 2026 net sales actually declined 8% year-over-year to $6.5 million (down from $7.1 million in Q1 2025). This proves their non-space business segments are actively deteriorating.Margin Collapse: Gross margins collapsed from a healthy 33% in Q1 2025 down to just 15% in Q1 2026. The company blamed surging material costs, specifically aluminum, and operational inefficiencies.Swinging to a Net Loss: Syntec swung from a net income of $323k last year to a net loss of $897,857 for the quarter. Adjusted EBITDA also turned negative.💸 Desperate Cash Crunch & Toxic Dilution OverhangThe Cash Position: As of March 31, 2026, Syntec was sitting on a dangerously low cash balance of only $617,007 against $11.2 million in current liabilities.Emergency Capital Raise: Because they were facing severe covenant stress with their lenders, Syntec was forced to launch an underwritten public offering in late April/early May 2026. They raised roughly $21.5 million in net proceeds to pay down debt and survive.Massive Dilution Moat: The poster pitches the $305M market cap as a cheap entry point. However, they ignore that this recent emergency equity raise immediately diluted existing shareholders by $9.59 per share against net tangible book value. Furthermore, there is a massive toxic overhang of 26 million Contingent Earnout Shares and 21 million warrants waiting to flood the float.Summary Verdict for an InvestorThe X post is a classic retail "pump" that isolates a single positive operational metric (volume of polymer space lenses shipped) while hiding a fundamentally troubled business.The statement that $OPTX is a comfortable long-term compounder "hitting its stride" is a dangerous conclusion. In reality, Syntec is a microcap dealing with a negative net income, collapsing gross margins, flat-to-declining top-line growth, and massive structural dilution that will cap equity upside for the foreseeable future.

3

251

May 12

$OPXS 2.16% Today — Small-Cap Optics Leader with Strong Buy Rating & 54% Upside Optex Systems Holdings ($OPXS) closed at $10.42 and continues to show steady strength. Key Highlights: Market Cap: $71.77M ( 65.4% in the past year)

Revenue (ttm): $42.28M ( 20.0%)

Net Income: $4.55M ( 8.7%)

EPS: $0.65 ( 6.8%)

PE Ratio: 16.05 (reasonable for growth)

Analysts: Strong Buy with price target $16.10 ( 54.51% upside)

Optex is a U.S. leader in precision optical systems, sighting devices, and periscopes for defense, aerospace, and high-performance applications. Low beta (0.51) consistent growth strong analyst backing make it a standout small-cap name in the optics/photonics space.@OptexSystems

— the defense and optics tailwinds are clearly supporting the move. This is a high-quality, under-the-radar name benefiting from onshoring and increased military spending. Are you watching $OPXS? Bullish on the optics/defense theme? Drop your thoughts below Not financial advice. DYOR. #OPXS #OptexSystems #DefenseTech #Optics #SmallCap #StrongBuy

1

1

197

𝐃𝐞𝐜𝐢𝐬𝐢𝐨𝐧𝐬 𝐛𝐲 𝐓𝐓𝐃 𝐁𝐨𝐚𝐫𝐝 𝐟𝐨𝐫 𝐭𝐞𝐦𝐩𝐥𝐞 𝐝𝐞𝐯𝐞𝐥𝐨𝐩𝐦𝐞𝐧𝐭𝐬

✅₹36.95 Cr temple development works at Venkatapalem (Amaravati)

✅Approval given for construction of a Srivari temple in Khammam on 20 acres allotted by Telangana Government.

✅₹43.40 crore sanctioned for modern infrastructure in TTD educational institutions, taking the total allocation to ₹161.40 crore.

✅₹4.55 crore approved for construction of additional toilets in Srivari Sarvadarshan queue lines.

✅Approval granted to merge 19.43 acres of donated land in Coimbatore district into TTD.

✅Roads and circles in Tirumala will be named with spiritual and mythological significance.

✅₹6 crore approved for a new water pipeline from Gogarbham Dam to the Filter Plant.

✅Silk items and blankets worth ₹44.20 crore to be purchased from APCO and Co-optex.

✅₹55 lakh sanctioned for construction of a Shiva temple in Vardhanapalli.

✅Free kits to be distributed to children under the “Akshara Govindam” initiative.

✅Steps initiated for appointment of staff at the newly built Sri Venkateswara Swamy Temple.

✅TTD Board member Saurabh Bora to bear expenses for construction of Sri Padmavathi Ammavari Temple.

✅₹3.61 crore approved for development works at Varahaswamy Rest House–1 in Tirumala.

✅₹4.75 crore approved for Yagasala construction at Alipiri for Srinivasa Divyanugraha Homam.

✅Shobha Raju appointed as TTD Asthana Vidwan.

✅₹2.71 crore approved for Rajagopuram construction at Ananthavaram Temple.

✅Proposal approved for construction of a centralized administrative building in Tirumala.

✅Approval granted for construction of Kalyana Mandapam at Lepakshi.

✅Committee to be formed for donor privileges policy.

✅Darshan and laddu facilities to be extended to contract and outsourcing employees.

✅Employee health reimbursement enhanced by ₹2 lakh, increasing the total limit to ₹5 lakh.

✅Permanent shelters to be constructed at Alipiri bus check points to ease traffic congestion.

✅Free hearing aids to be provided to 150 hearing-impaired children under the “Sravanam” project.

#AndhraPradesh #Amaravati #Khammam

5

54

2,050

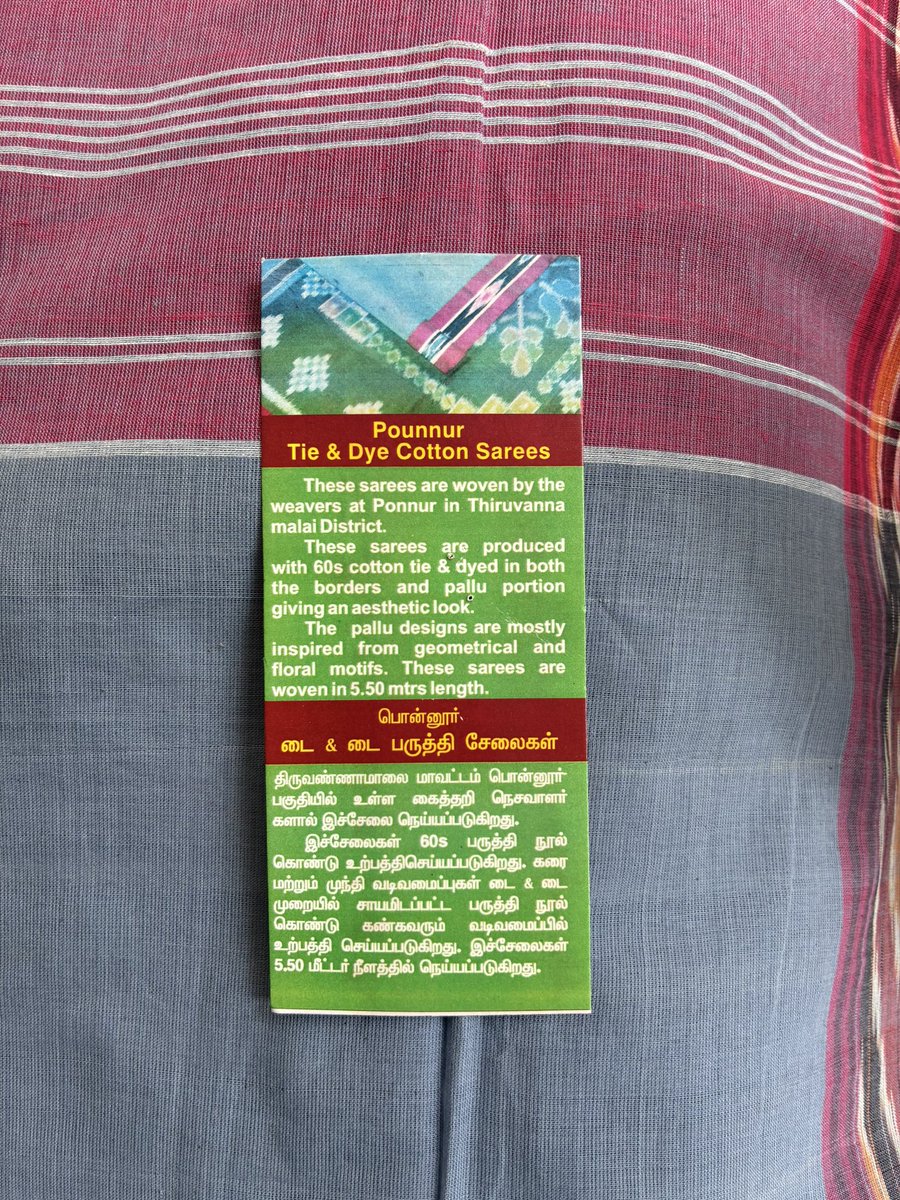

Co-optex లో నాకు బాగా నచ్చేది,ప్రతి చీరకు ఆ చీర నేసిన చేనేత కార్మికుల పేరు ఊరు తో సహా డీటెయిల్స్ ఉంటాయి.

2

12

443

Apr 30

📜 BILAN de ma sélection du secteur de la défense/armement !

Ces derniers jours je vous ai présenté 3 valeurs qui me semblent attractives :

▫️elles opèrent toutes les trois dans des niches spécifiques

▫️elles possèdent des fondamentaux solides 🛡️

▫️leur valorisation paraît attractive comparée au secteur qui est actuellement en plein boom 📊

▫️elles ne sont pas au centre d'attention du marché actuel 🧐

Après plusieurs décennies de paix, la situation géopolitique mondiale actuelle est assez tendue.

💥 La tendance des Etats est au réarmement partout dans le monde : Ukraine, Iran, tension USA/Chine, Taïwan, Moyen-Orient et depuis quelques jours le Mali. Malheureusement je n'ai pas le sentiment que cette tendance va se renverser dans les prochains mois, bien au contraire.

📈 Les valeurs du secteur de la défense ont extrêmement montés ces 3/4 dernières années. Les valorisations atteignent des sommets, certains acteurs qui ne dégagent même pas un centime de bénéfice voient leurs cours exploser comme des shitcoins !

Le but de cette sélection était donc de trouver quelques acteurs qui peuvent montrer du potentiel et qui se payent à des prix raisonnables :

💥 RSL ELECTRONICS $RSEL 🇮🇱

Petite capitalisation, société d'ingénierie qui propose des solutions de maintenance prédictive grâce à des capteurs et des logiciels IA.

Son modèle asset-light me semble intéressant, car il sera peu impacté par le coût des intrants (énergie, matières première) contrairement à l'industrie lourde.

Basée en Israël, son business est tout de même diversifié géographiquement 🗺️

💥 CMER INDUSTRIE (MER GOURP) $CMER 🇮🇱

On est également sur de l'ingénierie plus que de l'industrie, donc là aussi un profil intéressant dans un contexte qui risque d'être inflationniste à court/moyen termes.

Son business orienté infrastructure/télécom la rend tout aussi attractive et nécessaire aux opérations, donc un peu plus défensive.

Elle est moins diversifié que RSL ELECTRONICS mais bénéficie d'un soutien important de l'Etat Israëlien.

Malheureusement le cours est dans une forte tendance haussière.

💥 OPTEX SYSTEMS HOLDINGS $OPXS 🇺🇸

Micro-cap de 70M USD qui opère dans la niche des systèmes optiques de visée, principalement pour véhicules militaires types blindés.

Elle bénéficie des énormes budgets US et semble posséder un moat technologique difficile à surmonter. Par contre son activité est dépendante quasi à 100% des budgets US puisque son activité est centrée sur le continent américain.

La récente baisse du cours me semble être un bon point d'entrée dans une optique de long terme, éventuellement sous forme de DCA.

📜 Conclusion :

Les trois me plaisent, notamment $RSEL que je trouve vraiment intéressante et qui à mon avis est loin d'avoir découvert tout son potentiel. Néanmoins, sa capitalisation n'est vraiment pas grande et il n'est pas facile d'obtenir les rapports financiers.

Si je devais en choisir qu'une seule, mon choix se porterait vers OPTEX SYSTEMS $OPXS ! Sa valorisation me semble raisonnable et même si elle fait face à un risque de concentration, ce même risque peut s'avérer être une force. On parle de l'économie américaine et de la super puissance militaire du monde.

1

2

94

Apr 29

Aujourd'hui je te présente Optex Systems $OPXS : la petite société américaine de systèmes optiques de visée pour la défense que le marché traite comme une micro-cap ordinaire… alors qu’elle équipe les véhicules blindés les plus critiques de l’US Army !

1

1

4

686

Apr 26

In the Co-optex showrooms in Tamil Nadu, the sarees also display the name and photo of the weavers who have woven the sarees. That's a good initiative that should be replicated across all handicraft and state textile showrooms. #TamilNadu #textiles

Apr 25

In Japan, some fruit and vegetable boxes show photos of the farmers who grew them.

4

27

84

1,678

One of my 1st purchases from Co-optex post marriage, we use these during Navaratri poojé when ladies visit for haldi-kumkum.

1

2

5

405

Apr 22

Vote for Co optex Kanchipuram saree & Mysorepak.....

Apr 22

I promise every voter 3 kg par-boiled rice, 5 coconuts, 7 drumsticks, 2 Cooptex sarees, 2 pairs Geetha veshti and vest, 1 mixer grinder, and 1 moped. Please vote for me. Symbol: Ghee Mysorepak.

(Beware: other parties have put up proxy candidates with Milk Mysorepak as symbol.)

1

2

149

Apr 18

Every thread..Every Vote..Counts..A Video by woven by Co-Optex

@cooptexindia @kavitharamu

1

3

604

Apr 18

Co-Optex Voter Awareness Video.

Had a wonderful experience curating this cute video! Hope you all find it interesting 💜

@ECISVEEP @TNelectionsCEO @cooptexindia

3

1

12

388

Apr 10

Si usan LaTeX les será más fácil aprender OpTeX que funciona más o menos como Typst

3

261

Apr 9

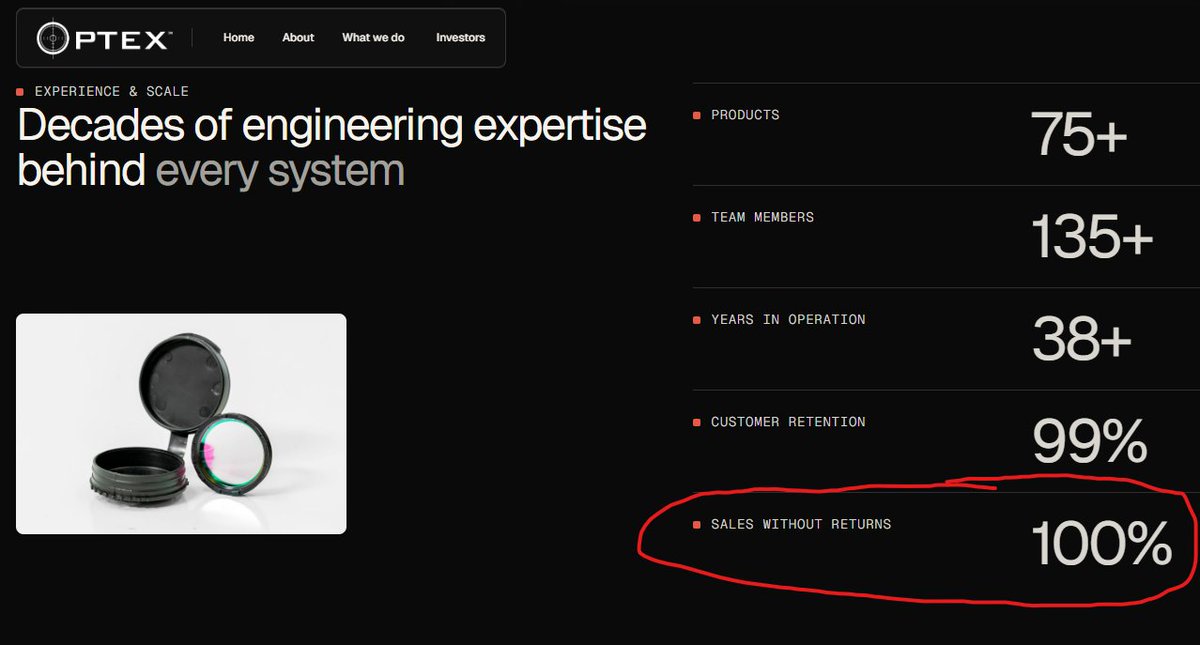

Optex Systems $OPXS scared the hell out of me with their new home page.

"Sales without returns" may require some rewording.

9

4,014

Mar 27

$OPXS - Optex Systems Announces $1.23 Million Order for Laser Protection Filters Supporting Night Vision Binocular Programs .

482

Mar 25

3 Dojis just mean compression is done and expansion is coming.

It can break either way.

April 2017 went up but that’s not a rule.

Optex says exhaustion.

Dojis say compression.

Time is the trigger.

Direction comes after the break, not before.

If it shakes out first, fine.

If it rips higher, fine.

I trade the move, not the guess.

1

4

339